A Tale of Two Consumer Sentiment Gauges

Why It Matters

The split underscores how survey design can shape the narrative on consumer sentiment, influencing monetary policy and corporate strategy. A worsening outlook threatens spending, which could slow the broader recovery.

Key Takeaways

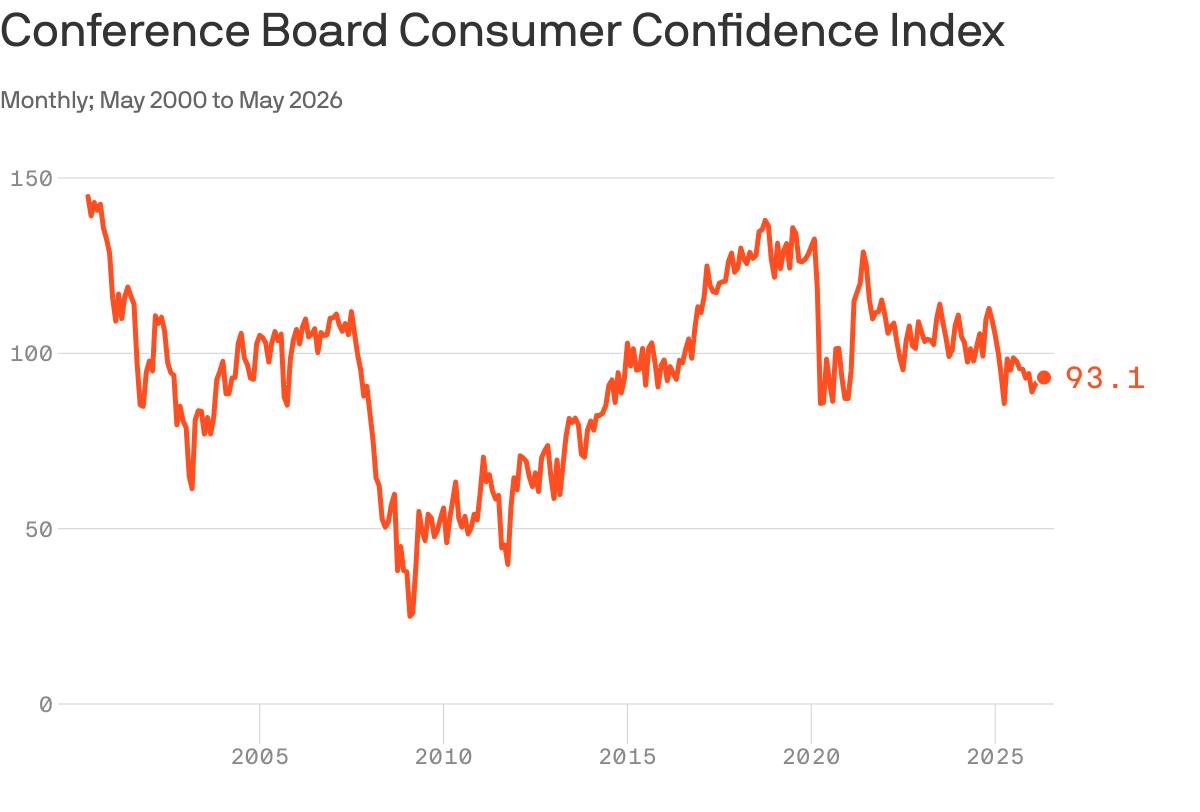

- •Conference Board confidence index fell 0.7 points to 93.1 in May

- •University of Michigan survey hit new lows, signaling weaker purchasing power

- •Energy shock from Middle East war inflates consumer price concerns

- •Labor market perception remains relatively positive despite hiring softening

- •Future expectations modestly improved, offsetting current condition decline

Pulse Analysis

The latest readings from the Conference Board and the University of Michigan illustrate a growing rift in how economists gauge consumer mood. The Conference Board’s index, which leans heavily on labor‑market perceptions, showed only a modest dip, buoyed by slightly brighter expectations for the next six months. In contrast, the Michigan survey, which places greater weight on purchasing power and personal finances, fell to its lowest level in half a century. This methodological split means that analysts must interpret the data in context, rather than treating either number as a definitive barometer of sentiment.

Underlying both surveys is the same macro backdrop: a war‑driven energy shock that has pushed global oil and gas prices higher, squeezing household budgets. Inflationary pressures remain elevated, eroding real wages and prompting consumers to cite price concerns more frequently. While the labor market has shown resilience, with unemployment still low, the cost of living surge is reshaping spending patterns, prompting a shift toward essential goods and away from discretionary purchases. These dynamics are feeding the pessimistic tone captured by the Michigan index and tempering optimism in the Conference Board’s outlook.

For policymakers and business leaders, the divergent signals serve as a cautionary tale. Monetary authorities must balance the need to curb inflation against the risk of choking consumer demand, especially as sentiment deteriorates on the financial‑condition side. Companies, particularly in retail and services, should monitor both gauges to fine‑tune pricing, inventory, and marketing strategies. Ultimately, the twin surveys highlight that consumer confidence is not monolithic; it reflects a complex interplay of employment security, price pressures, and geopolitical uncertainty that will shape the U.S. economy’s trajectory in the months ahead.

A tale of two consumer sentiment gauges

Comments

Want to join the conversation?

Loading comments...