COMMENT: Iran War’s Geopolitical Risks Alone Is Not Enough to Cause a Global Recession

Why It Matters

The analysis signals that investors and policymakers should focus on secondary channels—energy prices and financial conditions—rather than assuming geopolitical events will automatically trigger a global slowdown. This nuance shapes risk‑management and growth forecasts across markets.

Key Takeaways

- •Geopolitical risk spikes rarely trigger global recessions

- •$10 oil price rise cuts global growth by ~0.1%

- •Oxford Economics cut 2026 GDP forecast by 0.6%

- •Europe felt sharper impact from gas price surge

- •Strait of Hormuz disruption poses bigger risk than confidence loss

Pulse Analysis

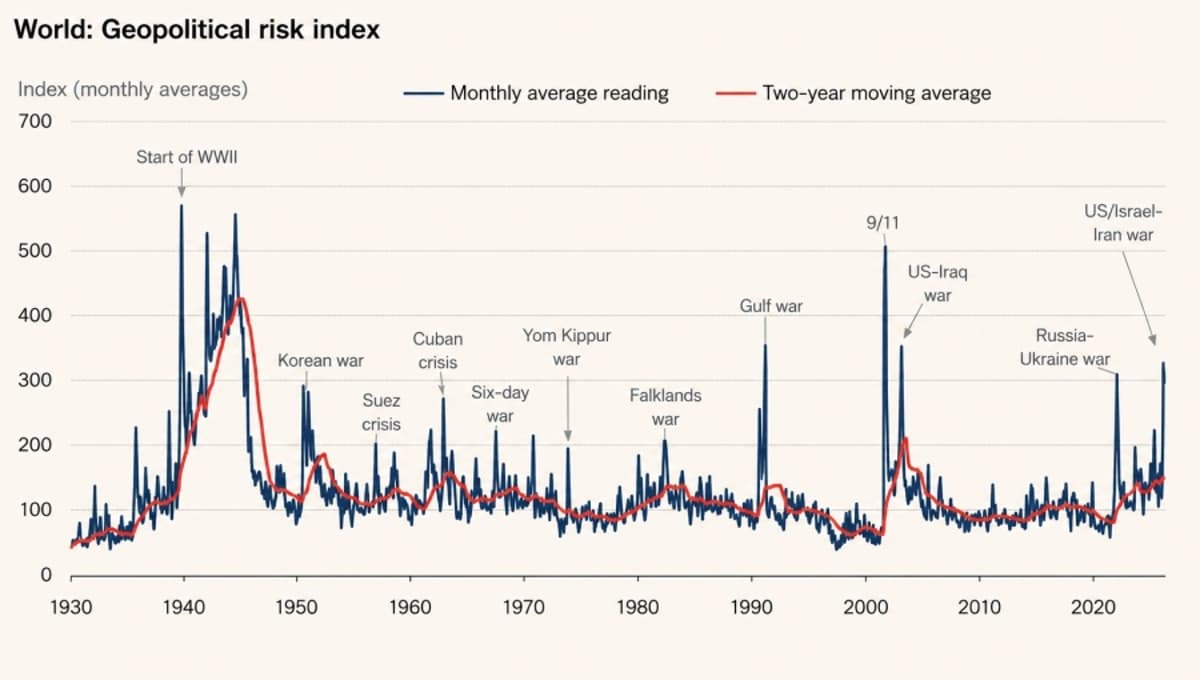

The Geopolitical Risk (GPR) index has surged amid the Iran‑Israel confrontation, echoing past spikes from World War II, the Korean War and 9/11. Yet history shows these peaks rarely translate into sustained economic contractions. Oxford Economics’ latest note underscores that, despite heightened headlines, global GDP growth has held steady, prompting only a modest 0.6‑percentage‑point downgrade to its 2026 outlook. This resilience stems from diversified growth drivers and the fact that geopolitical events, while disruptive, are not primary engines of downturns.

The real transmission pathways lie in commodity and financial channels. A sustained $10 rise in oil prices typically trims global growth by about 0.1 percentage points, a modest drag compared with the broader macro backdrop. Europe’s 2022 gas price shock illustrates how regional energy dependencies can amplify local pain, even as the global economy absorbs oil fluctuations without major derailment. The Gulf war adds a new layer of risk, especially if shipping through the Strait of Hormuz faces prolonged blockage, but current baseline forecasts already embed a reasonable buffer for such supply shocks.

Looking ahead, elevated geopolitical risk may still generate lagged effects on investment decisions, food prices and inflation, especially as other stressors—like a projected super El Niño and consecutive disaster seasons—compound market volatility. While uncertainty measures have not spiked dramatically, the cumulative impact of higher energy costs, tighter monetary policy and structural adjustments could shape growth trajectories through 2027. Stakeholders should therefore monitor secondary spillovers rather than over‑react to headline conflicts, aligning strategies with the nuanced, multi‑factor reality of today’s global economy.

COMMENT: Iran war’s geopolitical risks alone is not enough to cause a global recession

Comments

Want to join the conversation?

Loading comments...