Soft Landing Looks More Plausible, but the Fed Isn’t Ready to Call It Done.

Why It Matters

A soft landing would validate the Fed’s tightening strategy and reduce recession fears, but lingering inflation and labor‑market uncertainties could force tighter policy longer than expected.

Key Takeaways

- •Core CPI fell to 2.5% YoY in January

- •Unemployment slipped to 4.3% with modest payroll gains

- •Fed's preferred inflation gauge hovers near 3%, above target

- •Job growth narrow, raising labor market fragility concerns

- •Risks include AI-driven cost cuts and sticky services inflation

Pulse Analysis

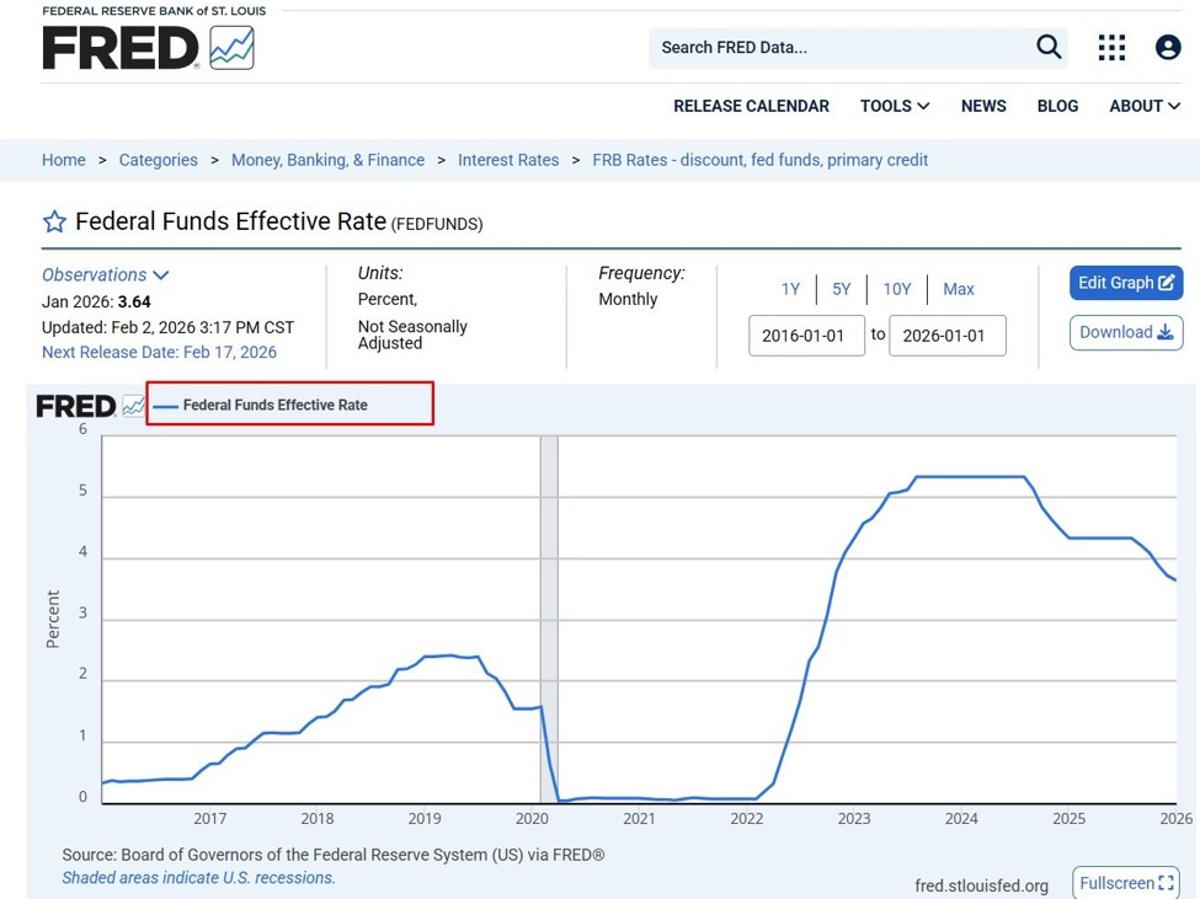

The latest U.S. data package presents the most favorable mix of declining inflation, steady employment, and solid growth since the pre‑pandemic era. Core consumer prices dropping to 2.5% signals that the aggressive rate hikes of the past two years are finally taking hold, yet the Fed’s preferred inflation metric lingering near 3% reminds policymakers that price pressures have not fully receded. This nuanced picture fuels optimism among investors that a soft landing—where growth persists without a recession—is within reach, but it also underscores the delicate balance the central bank must maintain.

Labor‑market dynamics add another layer of complexity. While the headline unemployment rate of 4.3% suggests resilience, payroll additions of roughly 130,000 jobs are modest and heavily weighted toward a narrow set of industries. Such concentration raises concerns that a modest shock—whether from a slowdown in corporate profitability or a rapid AI‑induced restructuring—could quickly translate into broader hiring freezes or layoffs. The Fed, therefore, watches not just the headline numbers but also the depth and breadth of job creation to gauge the economy’s true health.

Looking ahead, the policy horizon remains uncertain. Persistent services inflation and tariff‑related price spikes could keep overall inflation above the 2% target, prompting the Fed to hold rates steady or even consider further tightening. Conversely, a slowdown in consumer spending, potentially triggered by AI‑driven cost‑cutting or a market correction, could accelerate the path to rate cuts. As the Fed’s leadership transition approaches, the next policy cycle will likely hinge on how these competing forces evolve, making the soft‑landing narrative both plausible and precarious.

Soft landing looks more plausible, but the Fed isn’t ready to call it done.

Comments

Want to join the conversation?

Loading comments...