The Iran War Exposes Fiscal Fragility Around the World

Companies Mentioned

Why It Matters

Limited fiscal space constrains governments’ ability to cushion the energy shock, raising the risk of debt‑service strain and market volatility worldwide.

Key Takeaways

- •Fitch: most developed economies have exhausted fiscal space after successive crises

- •EU’s disciplined nations still face debt pressure despite austerity legacy

- •US defense requests could push deficit above 8% of GDP, debt 122%

- •India, Pakistan and peers face fiscal strain from higher oil prices

Pulse Analysis

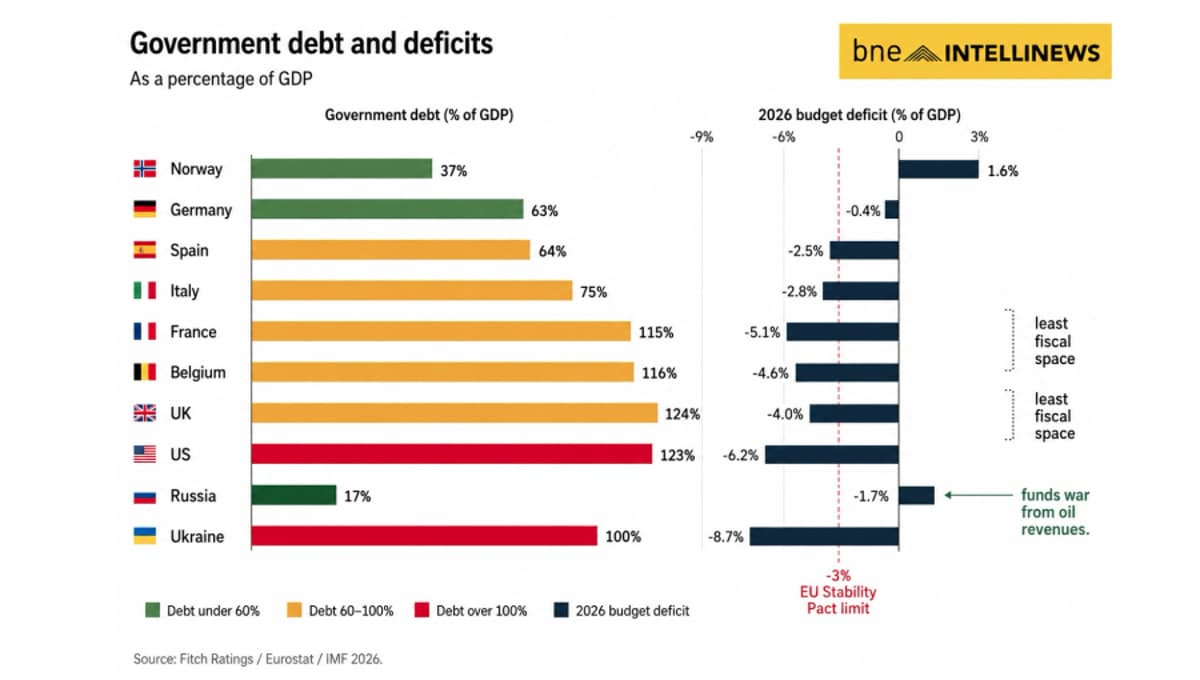

The Iran‑Israel conflict has arrived at a moment when sovereign balance sheets are already stretched thin. Over the past five years, governments in the United States, Europe and Asia have absorbed a pandemic‑induced stimulus, a Ukraine‑driven defence surge, and a 2022 energy price shock, leaving little fiscal headroom for a second energy crisis. Fitch Ratings’ latest note underscores that most advanced economies now operate with “exhausted” fiscal space, meaning any additional spending must be offset by cuts or higher borrowing costs. This backdrop amplifies the market’s sensitivity to even modest policy moves.

Within the euro‑area, the countries that survived the early‑2010s debt crisis—Ireland, Greece, Portugal, the Netherlands and the Scandinavian states—still possess the strongest fiscal cushions, yet Fitch warns they are approaching the limits of credibility. Germany’s historic €500 bn (≈$540 bn) defence and infrastructure programme, financed by a suspended debt brake, tests its growth outlook more than its financing capacity. Spain’s 0.5 %‑of‑GDP support measures sit at the EU deficit ceiling, while Italy’s high debt and financing costs blunt any sizable stimulus. France, Belgium and the United Kingdom, with deficits above 5 % and debt over 100 % of GDP, have the least room for new spending, and the United States faces a potential surge in its deficit—Fitch projects the general‑government gap could exceed 8 % of GDP if the full $440 bn defence request is approved.

In Asia, the fiscal picture is equally uneven. Net fossil‑fuel importers such as India, Pakistan, the Philippines and Thailand confront higher import bills and tighter credit, while China’s large reserves provide a buffer. Malaysia and Mongolia, as net exporters, are better positioned but still feel price pressures. The common thread is a decade of crisis‑driven borrowing without a rebuilding phase, leaving debt markets wary of further expansions. Policymakers will likely rely on targeted relief and offsetting measures, but any misstep could trigger rating downgrades and higher borrowing costs across the globe.

The Iran war exposes fiscal fragility around the world

Comments

Want to join the conversation?

Loading comments...