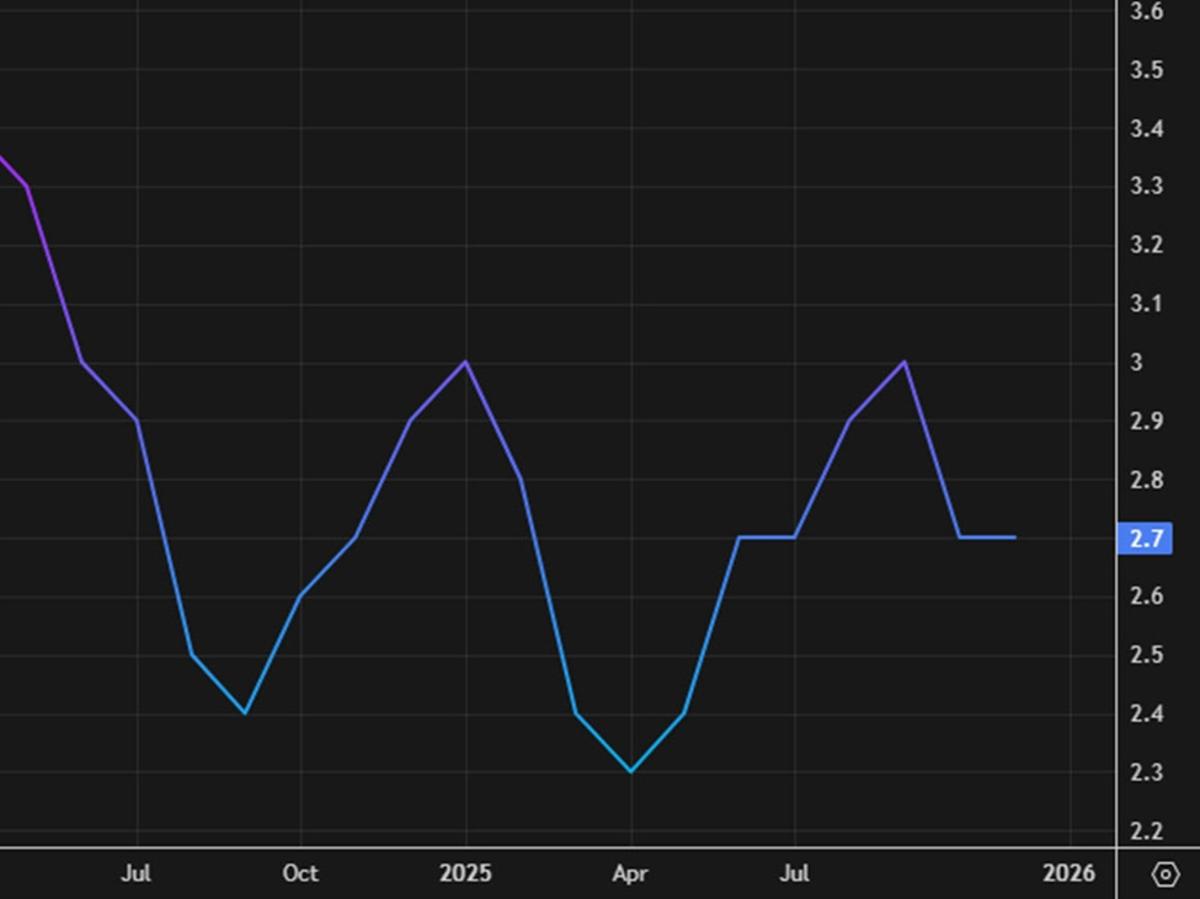

US January CPI +2.4% Y/Y vs +2.5% Expected

•February 13, 2026

0

Why It Matters

Lower‑than‑expected inflation reinforces expectations of continued Fed rate cuts, easing financial market pressures. Persistently high meat and energy prices, however, highlight lingering supply‑side risks.

Key Takeaways

- •CPI Jan 2.4% y/y, below 2.5% forecast

- •Core CPI steady at 2.5% y/y, matching expectations

- •Meat prices jump 8.9% annually, highest since 2022

- •Shelter cost growth slows to 3.0% annual rate

- •Fed pricing outlook turns slightly dovish, dollar weakens

Pulse Analysis

The January CPI report delivered a modest surprise, with headline inflation easing to 2.4% year‑over‑year and the month‑over‑month rise slipping to 0.2%. Market participants welcomed the softening, prompting a brief rally in equities and a retreat in the U.S. dollar as investors recalibrated expectations for the Federal Reserve’s policy path. While the headline number fell short of forecasts, the core CPI remained anchored at 2.5% year‑over‑year, underscoring that underlying price pressures are still present despite the headline slowdown.

A deeper dive into the components reveals a mixed picture. Food prices, led by an 8.9% surge in meat costs, continued to exert upward pressure, while energy inflation moderated to 4.2% year‑over‑year after a sharp jump in electricity costs. Shelter costs, traditionally a sticky driver of inflation, decelerated sharply, rising only 0.2% over the two‑month span and falling from a 3.6% annual pace in September to 3.0% in November. Data collection disruptions—October’s CPI was missed due to a government shutdown and November’s survey started later—may have artificially dampened the readings, prompting analysts to treat the figures with caution.

For policymakers, the report fuels a cautiously dovish narrative. The Fed’s pricing outlook appears to be shifting toward a more accommodative stance, bolstering expectations for additional rate cuts later in the year. However, the persistence of elevated meat and energy prices signals that supply‑side shocks could reignite inflationary pressures. Investors will likely focus on the upcoming December CPI release to confirm whether the current deceleration is sustainable or merely a statistical artifact, shaping bond yields, equity valuations, and the broader macroeconomic outlook.

US January CPI +2.4% y/y vs +2.5% expected

0

Comments

Want to join the conversation?

Loading comments...