Investment Banking Pulse Daily Digest

Investment Banking Pulse Daily Digest

Investment Banking Pulse

EMAIL DIGESTS

Daily

Every morning

Weekly

Tuesday recap

EMAIL DIGESTS

Daily

Every morning

Weekly

Tuesday recap

Wednesday, April 8, 2026

Market Intelligence for Investment Banking Professionals

Deep‑sea mining firms AOM and Odyssey merge in $1 billion all‑stock deal

Former Rio Tinto CEO Tom Albanese’s American Ocean Minerals will combine with Odyssey Marine Exploration in a $1 billion all‑stock transaction, creating one of the largest portfolios of polymetallic nodules in the Pacific’s Clarion‑Clipperton Zone.

Also developing:

By the numbers: GMCAR launches $1.27B prime auto‑backed securitization

Despite speculation that the Iran war could scuttle commitments from Saudi Arabia and other Middle Eastern countries, their investments have been secured.

New York Times — Mergers, Acquisitions and Divestitures

Bankers say companies are braving higher oil prices and whipsawing stock prices to seize on the willingness of federal antitrust enforcers to approve mergers.

New York Times — Mergers, Acquisitions and Divestitures

Eilla AI has completed Europe’s first M&A deal executed by an AI-native advisory firm, advising on the acquisition of two Central and Eastern European digital marketing agencies, CreateX and Nativ...

Tech.eu â People

The utility will split into two entities: one for general consumers and a new company, MSAPL, dedicated to agricultural consumers and solar energy. This restructuring aims to improve financial health, service quality, and energy security.

ET EnergyWorld (The Economic Times)

UK lender Barclays plans to continue growing its investment bank in Hong Kong, using the city as a platform to capture the growing fundraising needs in Asia and the rising opportunities from the internationalisation of the yuan, according to its global CEO. “Asia and Hong Kong are very important areas for us,” said C.S. Venkatakrishnan, global CEO of Barclays, in an interview with the South China Morning Post during a recent visit to the city. “In Hong Kong, our investment banking team is...

South China Morning Post — M&A (topic)

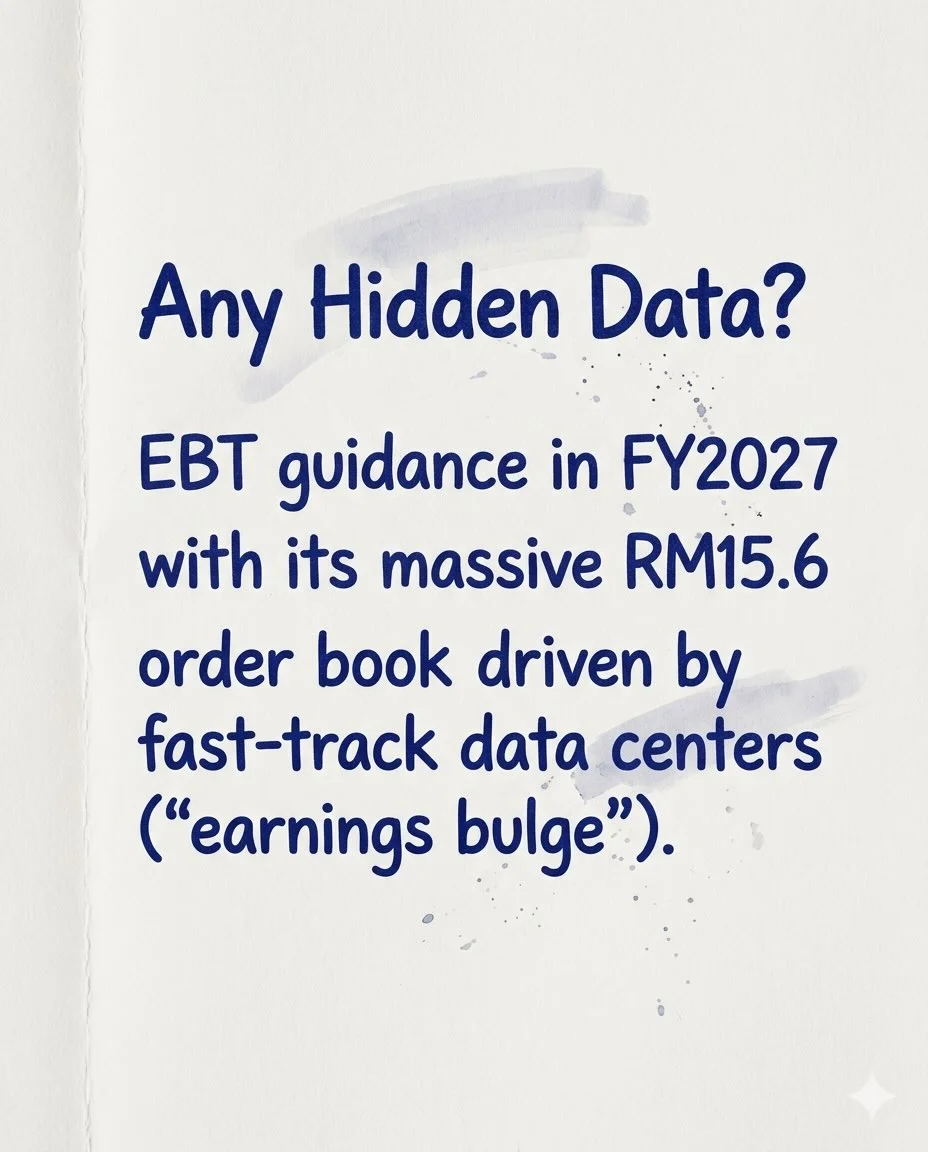

Everyone thinks Sunway's RM11 billion bid for IJM is just about building a "NATIONAL CHAMPION," but the underlying math reveals a brilliant trap. At an implied 46.6x P/E, this isn't a generous premium buyout—there is a ticking time bomb most investors are completely ignoring.

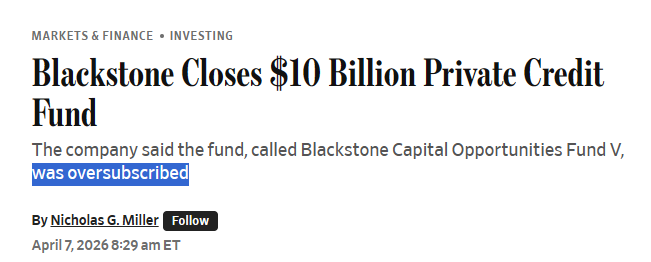

Investors can be prorated on the way in too. “COF V is Blackstone’s largest opportunistic credit fund raised to date, reflecting continued strong institutional demand for private credit." Institutional investors piling in to private credit as retail flees. https://t.co/gjHIJ7Kg2B