How Do You Retire at 55?

Key Takeaways

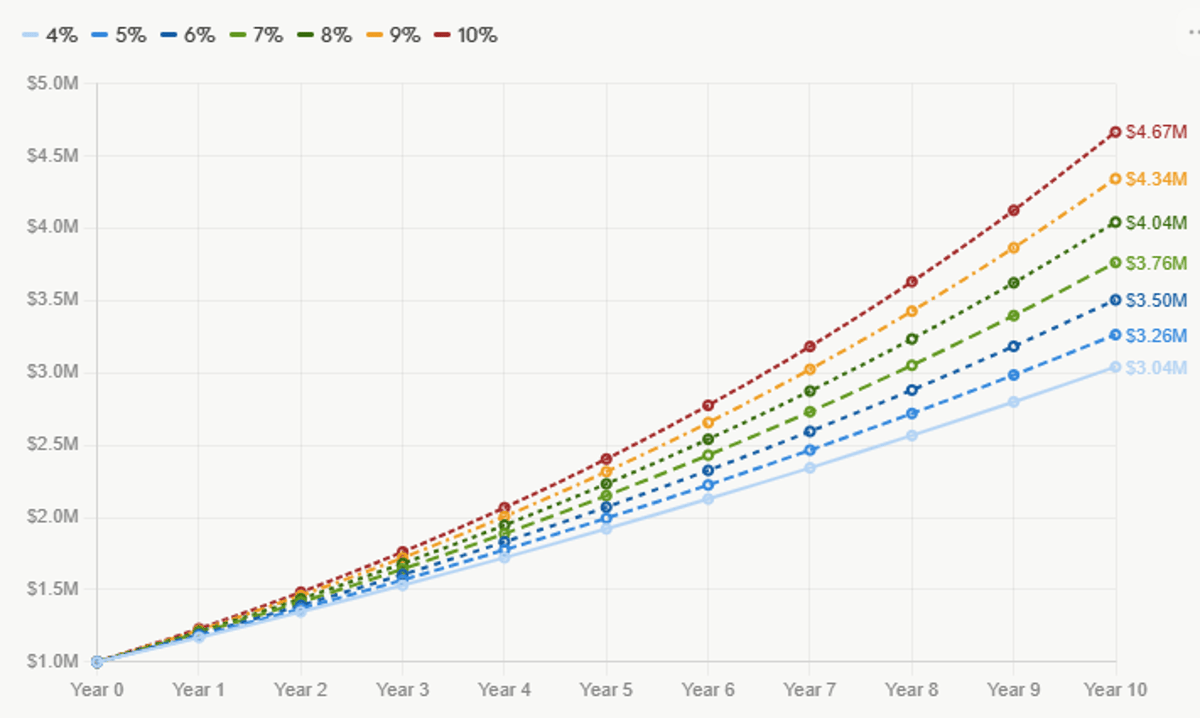

- •$1M plus $130k yearly can reach $3.5M in 10 years at 6%

- •Inflation may push $12k/mo to $16k/mo, raising required nest egg

- •Taxable accounts offer early‑withdrawal flexibility versus tax‑deferred limits

- •Maintain three‑year cash reserve to buffer market downturns

- •Consider career change or advisor to improve retirement certainty

Pulse Analysis

Retirement at 55 is a compelling goal, but it demands disciplined savings and a clear understanding of the numbers. With a $300,000 salary, the reader saves roughly 40 % of pre‑tax income, adding $130,000 annually to a mix of tax‑advantaged and taxable accounts. Assuming a modest 6 % annual return, the portfolio could grow from $1 million to about $3.5 million in a decade, aligning with the 4 % withdrawal rule that supports a $144,000 annual spend. This projection underscores how a high savings rate can offset the uncertainty of market performance.

Yet the headline figure masks deeper complexities. A 3 % inflation assumption would lift today’s $12,000‑per‑month budget to roughly $16,000 per month in ten years, increasing the required nest egg to over $4 million. Moreover, the composition of assets matters: taxable brokerage accounts provide the flexibility needed for early withdrawals, while tax‑deferred accounts such as 401(k)s impose penalties and required‑minimum‑distribution rules. Building a cash reserve equal to three years of living expenses offers a safety net against market volatility and unexpected costs, especially health care and potential college tuition for two children.

Given these variables, the reader faces three strategic choices. Continuing on the current path relies on market optimism and disciplined saving, but carries the risk of shortfall if returns falter or expenses rise faster than expected. Switching to a more fulfilling role—even at a lower salary—could extend the working horizon and improve quality of life, reducing the pressure to retire early. Finally, partnering with a qualified financial advisor can refine assumptions, optimize tax efficiency, and model alternative scenarios, turning the retirement dream into a robust, actionable plan. Each option balances risk, happiness, and financial certainty, guiding the reader toward a sustainable early‑retirement outcome.

How Do You Retire at 55?

Comments

Want to join the conversation?