Should Your Mom Have Private Equity in Her 401K?

Key Takeaways

- •Private equity outperformance has faded; median returns match public markets

- •Retail fees can cut private equity returns by double‑digit percentages

- •Illiquid lock‑up periods of 10‑15 years hinder retirement investors

- •Publicly listed PE firms give similar exposure with lower costs and liquidity

- •Fund‑of‑funds routes consistently underperform direct or listed private market alternatives

Pulse Analysis

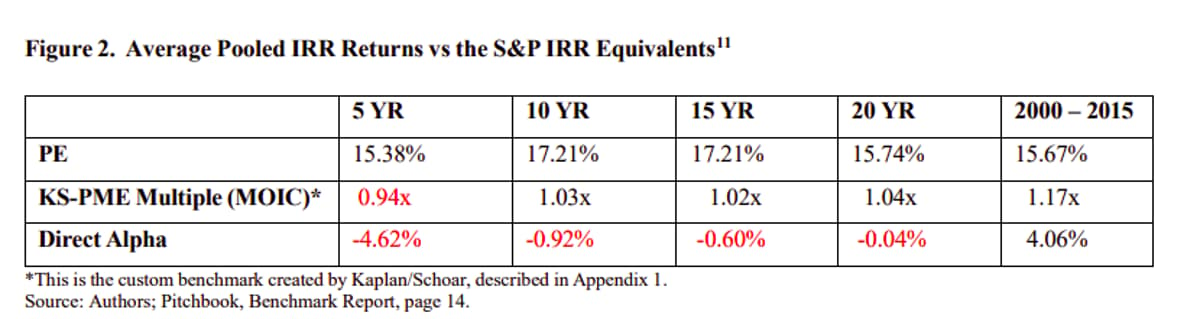

Private‑equity has long been sold as a high‑return, exclusive asset class, and recent marketing campaigns have tried to democratize access by inserting PE into 401(k) plans. The Harvard paper by Nori Gerardo Lietz dismantles this narrative with a rigorous cash‑flow‑matched comparison to the S&P 500, revealing that the historical outperformance of top‑quartile funds has evaporated. For most investors, especially those without institutional bargaining power, the realistic expectation is a median return that mirrors public markets, not the headline‑grabbing alpha often cited in promotional materials.

The study highlights three practical barriers that turn the PE promise into a net loss for retail savers. First, fee drag is severe: institutional PE already carries substantial management and performance fees, and retail vehicles add another layer through wealth‑manager commissions, fund‑of‑funds structures, and distribution costs—often eroding returns by double‑digit percentages annually. Second, liquidity risk is pronounced; capital can be locked for a decade or more, a mismatch for retirement accounts that may need to meet unforeseen cash demands. Third, the industry’s rapid growth has inflated entry valuations and left large pools of uninvested capital, creating headwinds that further diminish future returns.

Advisors should therefore shift focus from the allure of private‑equity labels to the economics of implementation. Publicly listed PE firms provide a liquid, fee‑efficient proxy that captures much of the private‑market upside without the operational complexities. By prioritizing low‑cost, liquid alternatives and rigorously controlling fee exposure, retirement portfolios can preserve capital and maintain flexibility, aligning with the fiduciary duty to act in clients’ best interests. This approach also positions investors to benefit from any future resurgence in private‑market performance without being locked into illiquid, underperforming structures.

Should Your Mom Have Private Equity in Her 401K?

Comments

Want to join the conversation?