Advisors Weigh Pros and Cons of 529 Plans

Why It Matters

Understanding the trade‑offs of 529 plans helps families and financial professionals optimize education funding while avoiding tax pitfalls. The evolving policy landscape makes timely guidance essential for effective college‑savings strategies.

Key Takeaways

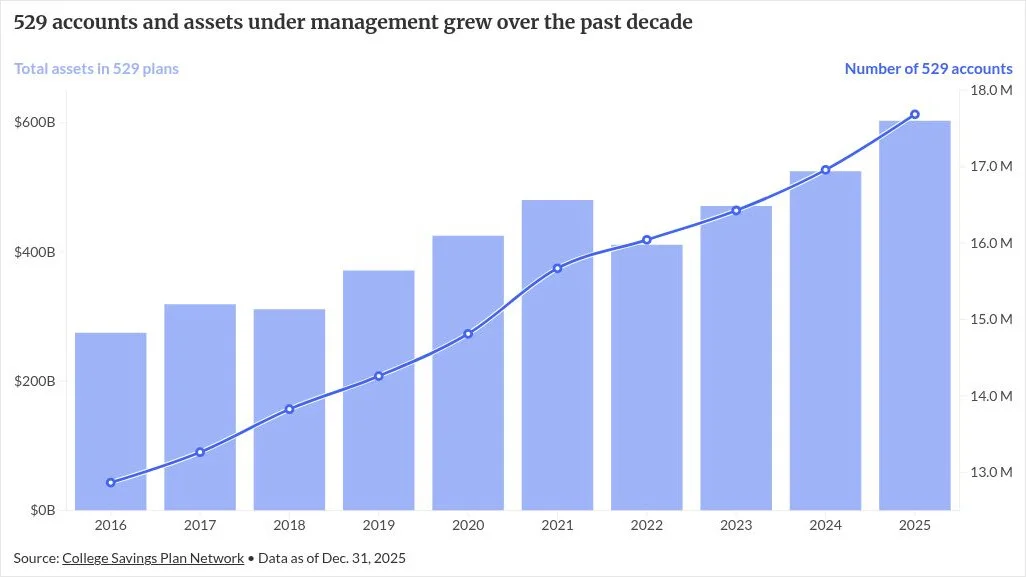

- •17.7 million 529 accounts hold $603 billion assets

- •No income limits make 529s attractive for high‑net‑worth families

- •UTMA accounts avoid 529 restrictions but trigger kiddie‑tax

- •Beneficiary changes allowed; funds can transfer to ABLE for disabilities

Pulse Analysis

College‑savings 529 plans have become a cornerstone of education financing, now covering 17.7 million accounts and nearly $603 billion in assets. Their tax‑free growth, lack of income caps, and state‑level tax deductions make them especially appealing to high‑net‑worth families seeking a dedicated vehicle for tuition and qualified expenses. As "529 Day" draws near, advisors are reminded that the plans’ popularity stems from both the fiscal advantages and the flexibility to change beneficiaries, allowing funds to stay within the family across generations.

Legislative updates in July 2025 broadened the scope of qualified expenses to include K‑12 tuition, reducing the risk of stranded balances that previously forced costly withdrawals. The same reforms enable rollovers to alternative 529 programs and, for beneficiaries with disabilities, transfers to ABLE accounts, preserving tax benefits while adapting to changing family needs. Advisors also stress that many state plans are open‑nationally, debunking the myth that families must use their home‑state offering, which opens the door to competitive fee structures and investment options.

Despite these strengths, 529s are not a one‑size‑fits‑all solution. State‑specific usage rules can limit flexibility for students attending out‑of‑state public universities, prompting some families to favor UGMA or UTMA custodial accounts that allow broader spending on extracurriculars and non‑educational items. While UTMA accounts sidestep 529 restrictions, they introduce the kiddie‑tax, potentially subjecting unearned income to parents' marginal rates. Advisors must therefore balance the tax credits, student‑loan‑interest deductions, and other education‑related incentives against each vehicle's constraints to craft a holistic savings strategy.

Advisors weigh pros and cons of 529 plans

Comments

Want to join the conversation?

Loading comments...