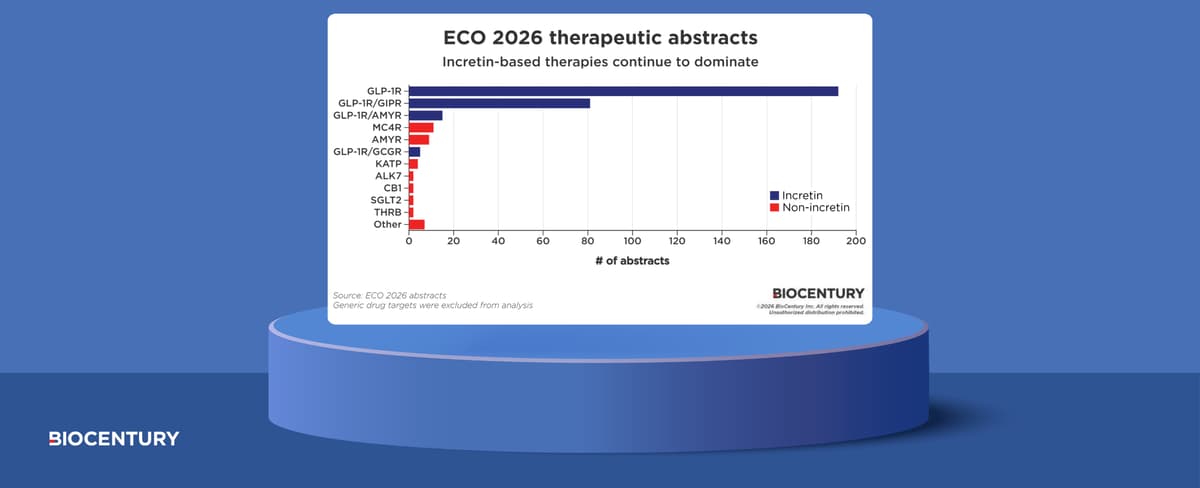

Incretins Continue to Dominate Obesity Conferences

Why It Matters

The focus on incretins signals a rapidly expanding market for prescription obesity drugs and foreshadows changes in clinical guidelines, payer coverage, and competitive dynamics across pharma and biotech.

Key Takeaways

- •GLP‑1 agonist semaglutide achieved up to 20% weight loss in trials

- •Tirzepatide showed superior efficacy, prompting fast‑track FDA review

- •Over $10 billion projected US obesity‑drug market by 2030

- •Multiple biotech firms announced next‑gen incretin candidates

- •Payers anticipate coverage challenges for high‑cost injectable therapies

Pulse Analysis

Incretin hormones, particularly glucagon‑like peptide‑1 (GLP‑1) and glucose‑dependent insulinotropic polypeptide (GIP), have become the headline act at the latest obesity symposia. Researchers showcased phase‑III data for semaglutide, which consistently delivered 15‑20 percent body‑weight reductions, and tirzepatide, a dual‑agonist that outperformed its GLP‑1‑only peers on both efficacy and metabolic endpoints. The robust results have spurred excitement among investors and clinicians alike, as they suggest a viable pharmacologic alternative to lifestyle‑only interventions and set a new efficacy benchmark for the field.

The commercial implications are equally compelling. Analysts now project the U.S. obesity‑drug market to exceed $10 billion by 2030, driven largely by the premium pricing power of injectable incretin therapies. Biotech firms are racing to differentiate their pipelines, unveiling next‑generation molecules that aim for oral delivery, longer half‑lives, or combined mechanisms to mitigate side‑effects and improve adherence. Meanwhile, established players are expanding indications, seeking approvals for obesity‑related comorbidities such as type 2 diabetes, non‑alcoholic fatty liver disease, and cardiovascular risk reduction, thereby widening the addressable patient pool.

Regulatory and payer landscapes will shape the trajectory of this boom. The FDA has granted fast‑track status to several incretin candidates, reflecting confidence in their therapeutic value, but high acquisition costs raise concerns about insurance coverage and health‑system budgets. Payers are beginning to develop tiered formularies and outcome‑based contracts to manage expenditures while ensuring patient access. As the data pool grows and real‑world evidence accumulates, stakeholders will need to balance clinical benefits against economic sustainability, a dynamic that will define the next phase of obesity treatment innovation.

Incretins continue to dominate obesity conferences

Comments

Want to join the conversation?

Loading comments...