Private Markets in 401(k)s Face Major Liquidity Challenges: Morningstar

•February 27, 2026

0

Why It Matters

If liquidity constraints cannot be resolved, private‑market allocations may lose their appeal in retirement accounts, reshaping product strategies for asset managers and advisors.

Key Takeaways

- •Semiliquid private CITs need up to 40% liquidity sleeves.

- •Small redemption clusters quickly deplete private‑market liquidity buffers.

- •Larger liquidity buffers dilute expected private‑equity return premium.

- •Performance edge may vanish once liquidity costs are accounted.

- •DOL rulemaking will determine fiduciary feasibility of private assets.

Pulse Analysis

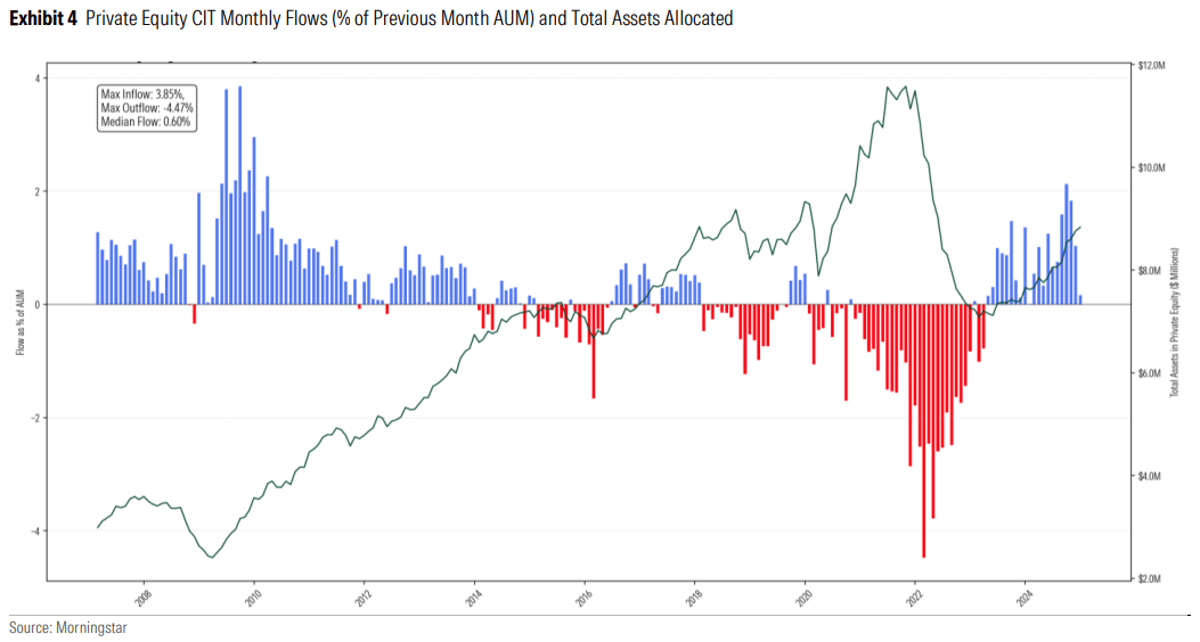

Private markets have surged into the $12 trillion defined‑contribution arena, spurred by regulatory encouragement and the promise of higher returns. Asset managers tout semiliquid structures—often collective investment trusts with a private‑equity core and a liquid sleeve—as a way to blend diversification benefits with retirement‑plan flexibility. Yet the daily contribution, withdrawal, and rebalancing cadence of 401(k) accounts imposes a liquidity demand that traditional private‑equity vehicles were never designed to meet.

Morningstar’s simulation, built on a synthetic population mirroring real participant ages, salaries, and contribution patterns, tested these semiliquid vehicles over an 18‑year horizon. The model showed that modest, clustered redemptions can rapidly drain liquidity buffers, prompting a need for sleeves as large as 40% of assets. Such sizable liquid allocations blunt the private‑market return premium and increase fee pressure, effectively narrowing the performance gap between private and public alternatives. The study also highlighted that during market stress, private‑equity holdings within the CIT could plunge nearly 40%, underscoring the fragility of these products under adverse conditions.

For asset managers and financial advisors, the findings signal a strategic crossroads. Designing vehicles that balance sufficient liquidity with meaningful private‑asset exposure will be critical to satisfy fiduciary duties and participant expectations. The pending Department of Labor rulemaking will further shape the landscape, clarifying how fiduciaries must weigh higher costs against diversification gains. Until clear guidance emerges, firms may adopt more conservative liquidity sleeves, potentially limiting the very upside that originally attracted private‑market interest to retirement plans.

Private markets in 401(k)s face major liquidity challenges: Morningstar

0

Comments

Want to join the conversation?

Loading comments...