What AI Stock Selloffs May Be Getting Wrong in Wealth Management

•February 24, 2026

0

Why It Matters

The data shows that underlying business health, not headline volatility, drives wealth‑management profitability, signaling a stable investment theme for the industry. Investors and advisors can rely on strong cash flows and tech‑enabled efficiency despite market swings.

Key Takeaways

- •Wealth managers hit record client assets despite stock drops

- •Net revenue up 17%, pretax earnings up 21%

- •AI-driven tools spurred trading volume spikes in 2025

- •Schwab’s net‑interest margin expansion offsets rate‑cut risk

- •Raymond James allocated $1.1B to technology for efficiency

Pulse Analysis

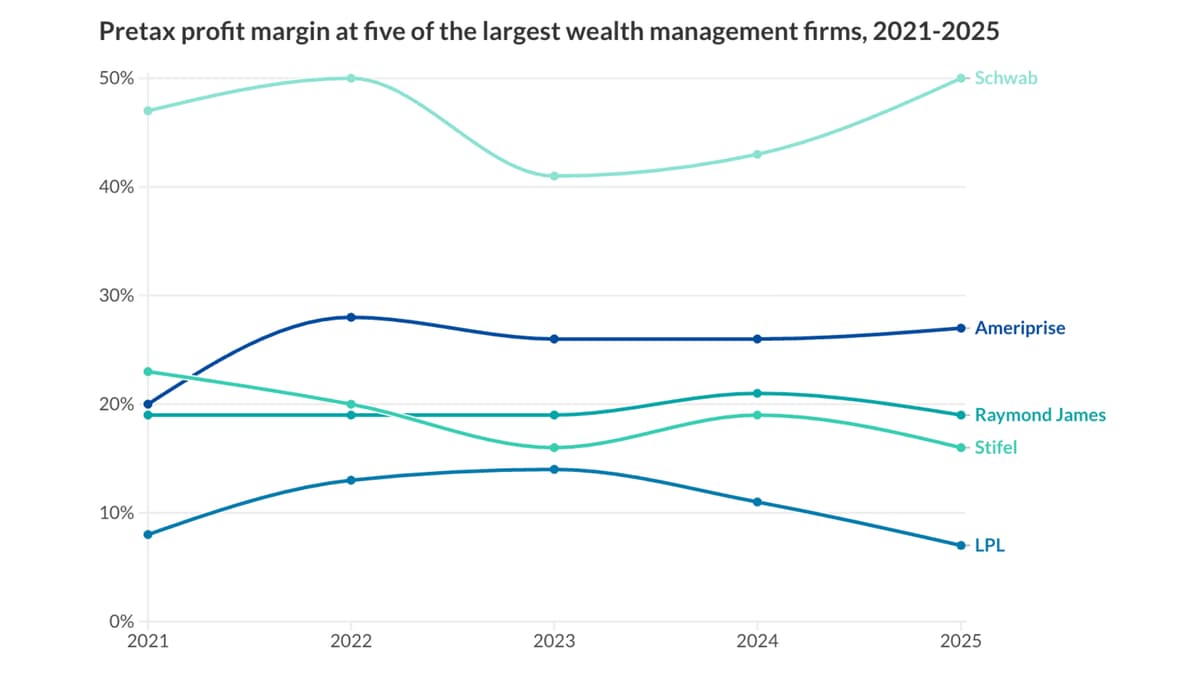

The recent wave of AI‑centric headlines has rattled the share prices of publicly traded wealth‑management firms, but the sector’s core metrics tell a different story. Fitch’s analysis highlights that a half‑dozen leading brokers collectively amassed record client assets, driven by organic growth, strategic acquisitions, and a bullish market environment. This asset surge translated into a 17% lift in net revenue and a 21% jump in pretax earnings, underscoring the resilience of fee‑based models even when equity markets wobble.

Technology spending is now a decisive competitive lever. Raymond James earmarked $1.1 billion for AI and platform upgrades in 2026, while Schwab leveraged its sizable cash balances to expand net‑interest margins, insulating earnings from potential Fed rate cuts. Record trading volumes in 2025, fueled by heightened volatility and extended‑hours access, boosted transactional revenue across the board. However, firms face cost pressures from advisor recruitment, M&A integration, and one‑off regulatory charges, making efficient capital allocation essential for sustaining profit margins.

Looking ahead, consolidation is likely to accelerate as firms chase scale and talent. M&A activity will deepen platform synergies, allowing larger players to spread technology costs and enhance client experiences. Meanwhile, independent advisory boutiques, exemplified by Robertson Stephens, will continue to target high‑net‑worth segments, emphasizing fiduciary stewardship over pure product distribution. For investors, the message is clear: despite short‑term price turbulence, wealth‑management companies with strong balance sheets, diversified revenue streams, and robust tech roadmaps are positioned for steady growth through 2026 and beyond.

What AI stock selloffs may be getting wrong in wealth management

0

Comments

Want to join the conversation?

Loading comments...