How to Maximize the Benefits of Taxable Munis in Your Portfolio

Companies Mentioned

Bloomberg

Why It Matters

Taxable munis offer higher yields and low‑correlation credit ballast, making them a strategic tool for institutional investors seeking income and risk mitigation. Their performance and limited supply create attractive spread‑compression opportunities in a rising‑rate environment.

Key Takeaways

- •Taxable munis yield 100‑140 bps over tax‑exempt, now 160‑170 bps.

- •Life‑insurance firms favor long‑duration taxable munis for asset‑liability matching.

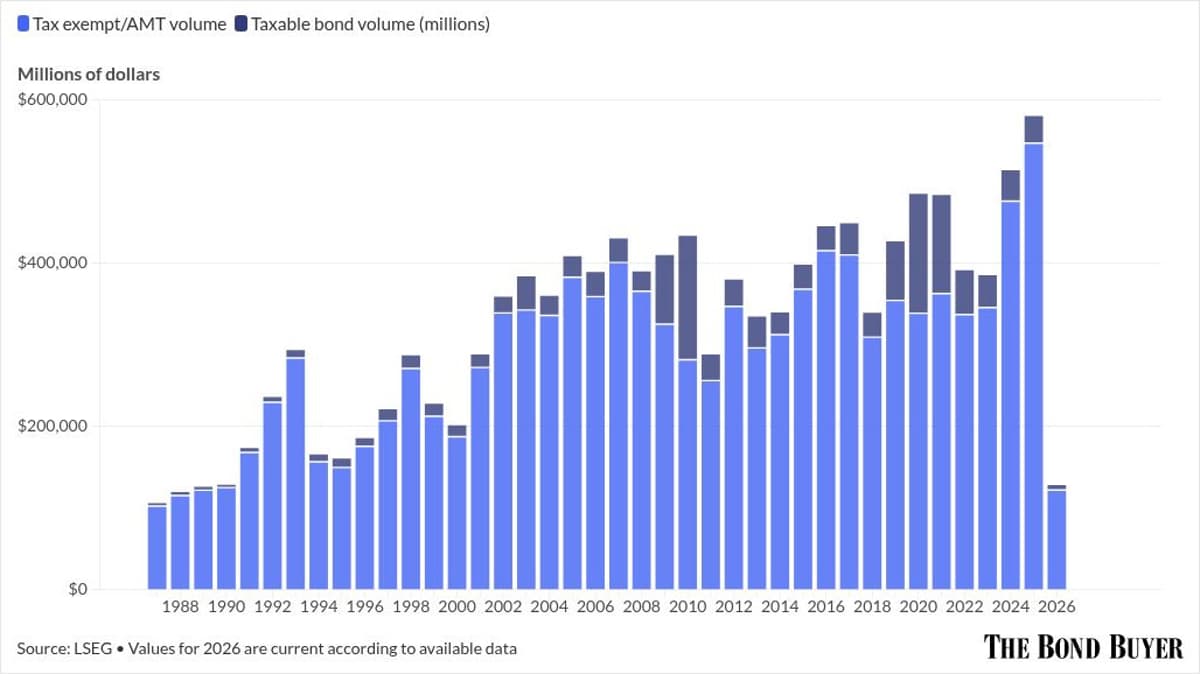

- •Taxable muni issuance fell from 25% (2021) to ~5% (2025) of total.

- •2025 taxable muni index returned 7.89%, beating tax‑exempt and corporates.

- •Foreign investors hold ~2.9% ($125 bn) of municipal market, limited growth.

Pulse Analysis

The current market backdrop—spurred by geopolitical tension and a volatile rate environment—has revived interest in taxable municipal bonds as a high‑yield, low‑correlation asset class. Unlike traditional tax‑exempt munis, taxable issues deliver spreads that can exceed 170 basis points during dislocations, offering investors a premium over comparable investment‑grade corporates. This yield advantage, coupled with historically low default rates and strong recovery prospects, makes taxable munis an appealing supplement for life‑insurance firms and pension funds that need long‑duration assets to match liabilities.

Issuance dynamics further enhance the case for taxable munis. After a pandemic‑driven surge in 2021, supply has dwindled to roughly 5% of total municipal issuance, tightening the market and supporting spread compression. The decline reflects a shift away from advance‑refinancing strategies after the 2017 Tax Cuts and Jobs Act and a higher‑rate environment that favors cheaper tax‑exempt financing. Consequently, the limited pipeline creates scarcity value for existing holdings, especially as investors chase the 7.89% return recorded by the Bloomberg taxable muni index in 2025, outpacing both tax‑exempt and corporate benchmarks.

Looking ahead, the growth ceiling for foreign participation remains modest, with foreign investors holding about $125 billion—just 2.9% of the $4.3 trillion municipal market. Nonetheless, domestic institutional demand is likely to sustain the niche, particularly as issuers seek flexible financing for infrastructure, cyber‑security, and climate projects. With spreads still elevated and the credit quality of taxable munis remaining resilient, investors can expect continued outperformance relative to Treasuries and corporates, provided they manage duration risk in a rising‑rate landscape.

How to maximize the benefits of taxable munis in your portfolio

Comments

Want to join the conversation?

Loading comments...