The Future of Palm Payments After Amazon's Pullback

•February 6, 2026

0

Companies Mentioned

Why It Matters

The shift highlights a strategic re‑evaluation of biometric payment methods, where higher‑accuracy palm‑vein solutions could reshape checkout security and convenience for retailers and banks.

Key Takeaways

- •Amazon abandons palm payments, citing low growth

- •JPMorgan Chase pilots palm‑vein checkout in cafeteria

- •Verifone integrates palm biometrics into existing terminals

- •Global pilots in UAE, Uruguay, Olympics indicate rising interest

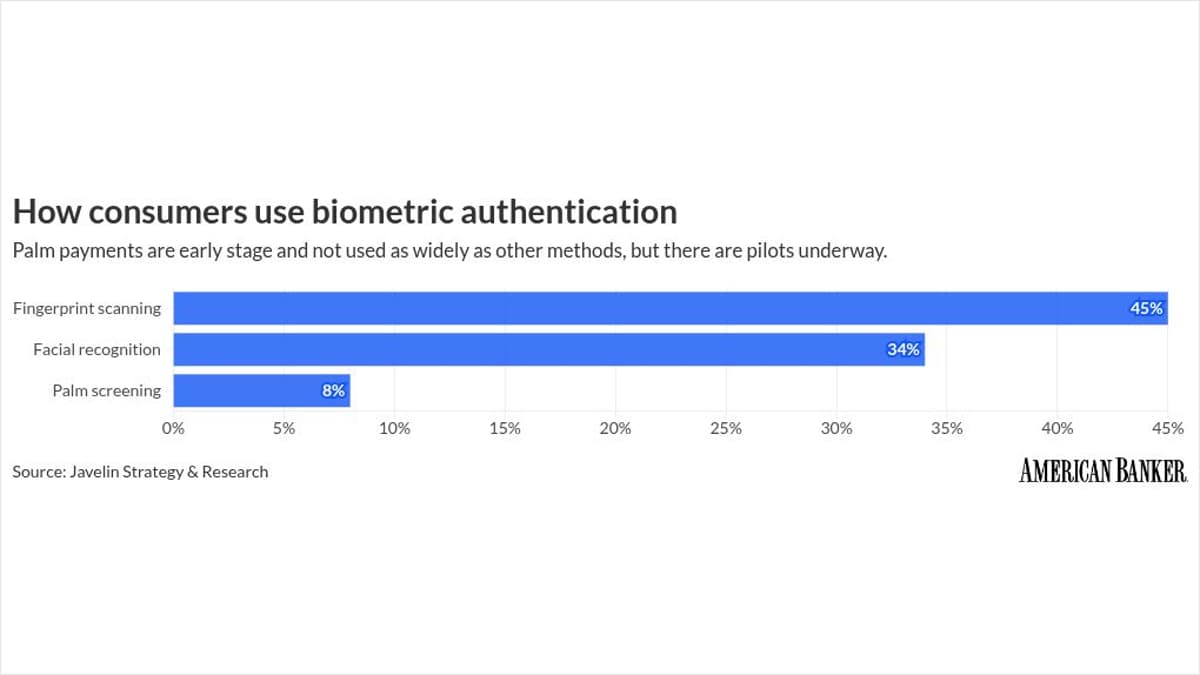

- •US consumer usage remains under 10%, limiting rollout

Pulse Analysis

Amazon’s decision to shelve its palm‑vein readers reflects a broader corporate focus on agentic commerce and a realistic assessment of retailer appetite. While the e‑commerce giant saw limited demand for its proprietary hardware, the move does not signal a technological dead‑end. Industry analysts note that palm biometrics offer higher false‑reject resistance than facial or fingerprint scans, positioning them as a premium security layer for high‑value transactions. This nuanced advantage keeps the technology on the radar of payment innovators despite Amazon’s retreat.

Across the United States, a handful of pilots are quietly testing the waters. JPMorgan Chase is evaluating palm‑vein enrollment in a corporate cafeteria, while Verifone, partnered with PopID, has retrofitted its ubiquitous terminals to support touch‑free infrared scanning. These initiatives aim to gather real‑world data on user experience, transaction speed, and fraud mitigation. Early results suggest that merchants value the optionality of multiple biometric modalities, allowing them to future‑proof point‑of‑sale ecosystems without committing to a single method.

Globally, adoption is accelerating. The United Arab Emirates launched a regional biometric payment system, and Mastercard’s pilot in Uruguay’s Red Expres chain demonstrated seamless palm checkout in a supermarket setting. The technology’s exposure at the Paris Olympics further validated its scalability under high‑traffic conditions. For the U.S. market, the primary hurdle remains consumer familiarity; with only eight percent of shoppers having tried palm scanning, education and seamless integration will be critical. As biometric diversity becomes a competitive differentiator, firms that successfully embed palm‑vein solutions may capture a premium segment of security‑conscious consumers, reshaping the future of frictionless payments.

The future of palm payments after Amazon's pullback

0

Comments

Want to join the conversation?

Loading comments...