ASML as the Last Polite Monopolist

Why It Matters

The standoff could reshape semiconductor pricing, investment cycles, and supply security, affecting AI hardware, consumer electronics, and national tech strategies.

Key Takeaways

- •TSMC balks at $381 million High‑NA EUV price.

- •ASML controls upgrades, software, and service for all EUV tools.

- •New fab projects (Musk, Rapidus, SMIC) lack critical process know‑how.

- •Memory makers SK Hynix and Samsung already buying High‑NA machines.

- •TSMC’s leverage may peak as ASML’s customer base diversifies.

Pulse Analysis

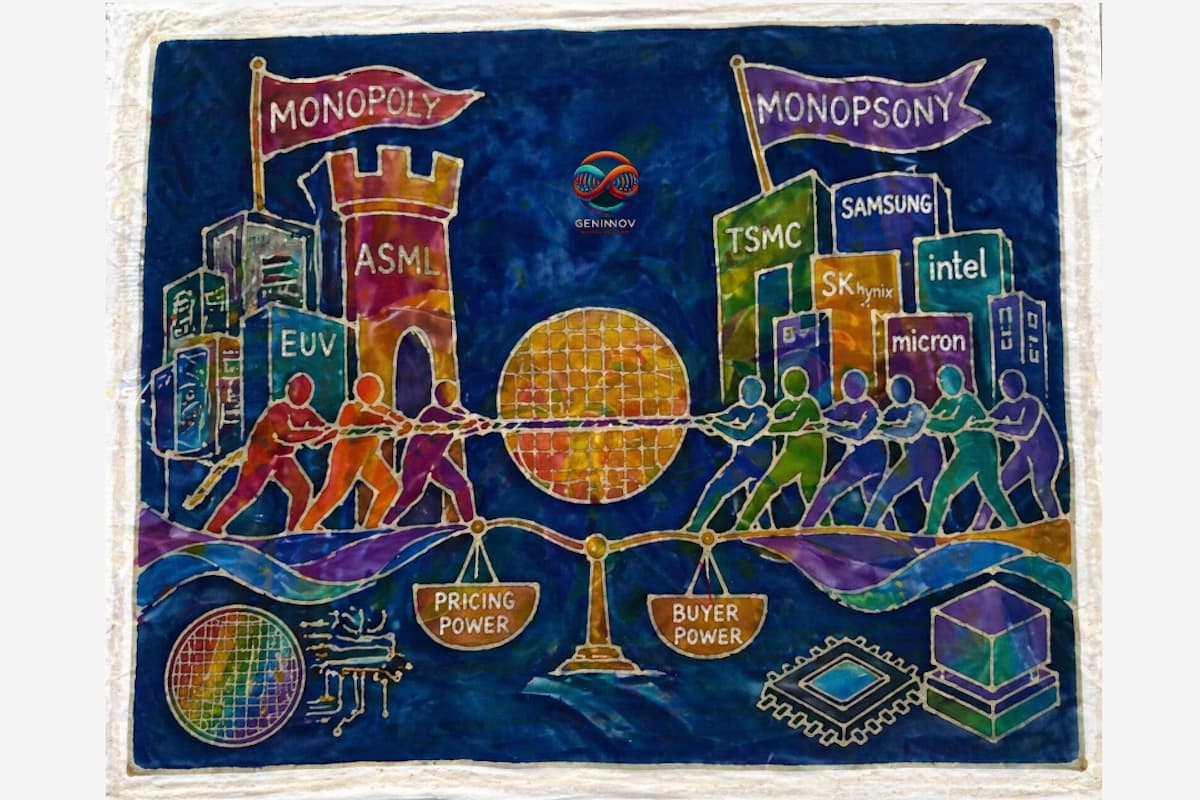

The semiconductor ecosystem is at a crossroads as TSMC, the world’s largest foundry, publicly rebuffed ASML’s €350 million (about $381 million) price tag for the next‑generation High‑NA EUV scanner. This confrontation is unusual because both firms have traditionally operated in a partnership‑like relationship, with ASML supplying the only machines capable of printing sub‑5 nm features and TSMC absorbing the massive capital outlay. The dispute underscores how a single supplier can wield outsized influence over the entire supply chain, from tool upgrades to the software keys that unlock incremental productivity gains. As AI‑driven workloads demand ever‑more compute, the pricing of these lithography tools becomes a strategic lever for the broader tech economy.

Beyond the headline price battle, the article highlights why new entrants cannot simply buy their way into leading‑edge manufacturing. Projects such as Elon Musk’s Terafab, Japan’s Rapidus, and China’s SMIC may have access to the same catalog of deposition, etch, and metrology equipment, but they lack the deep, decades‑long process knowledge that TSMC has codified in thousands of proprietary loops. This tacit expertise—captured in process documents, defect‑reduction methodologies, and yield‑optimization software—remains the true moat. Consequently, even with billions of dollars, newcomers face steep learning curves, higher defect rates, and substantially higher per‑chip costs, limiting their ability to compete at the most advanced nodes.

Looking ahead, ASML’s monopoly is gradually diffusing as a broader set of customers—SK Hynix, Samsung, Intel, and emerging memory makers—are committing to High‑NA EUV purchases. This diversification weakens TSMC’s monopsony leverage and gives ASML room to raise prices across its product line, including Low‑NA EUV and advanced DUV tools. If ASML decides to monetize upgrades more aggressively, the cost of extending the life of older scanners could approach or exceed the price of a new High‑NA system, forcing fabs to adopt the next generation sooner. The outcome of this pricing tug‑of‑war will shape capital allocation, node roadmaps, and ultimately the pace of innovation in chips that power everything from data‑center AI to consumer devices.

ASML as the last polite monopolist

Comments

Want to join the conversation?

Loading comments...