Omdia Lifts 2026 Semiconductor Outlook as AI-Driven Memory Constraints Intensify

Why It Matters

The forecast signals a structural shift toward AI‑intensive workloads that will reshape capital allocation, pricing power, and supply‑chain dynamics across the semiconductor ecosystem.

Key Takeaways

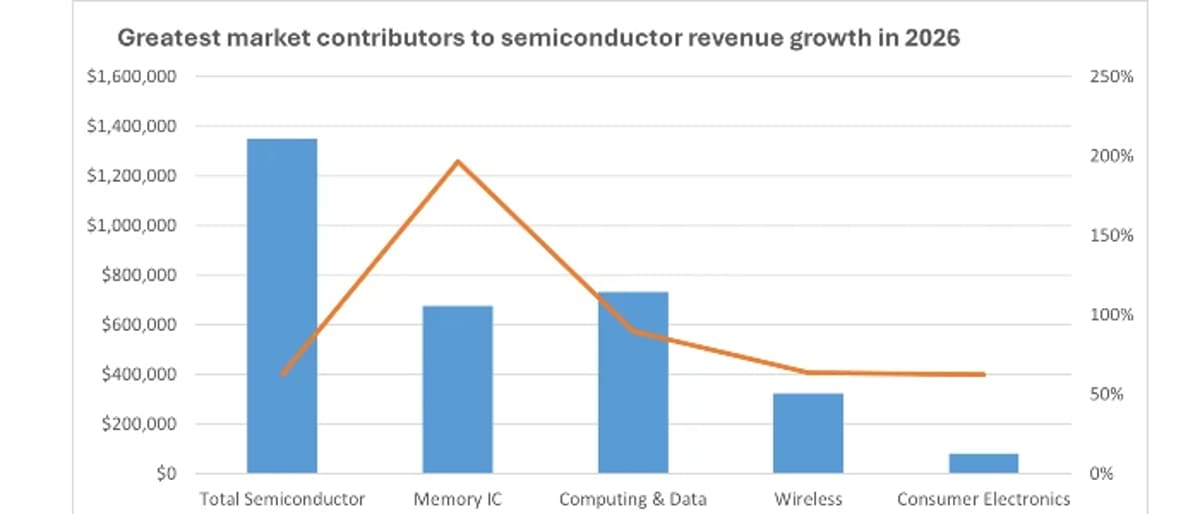

- •Omdia forecasts 62.7% semiconductor revenue growth by 2026

- •DRAM value expected to double; NAND to quadruple versus 2025

- •AI‑driven server refreshes push average selling prices higher

- •Memory price hikes boost revenue despite flat smartphone shipments

Pulse Analysis

The latest Omdia outlook underscores how artificial‑intelligence workloads are redefining the semiconductor market’s growth engine. While traditional drivers such as smartphone volume have plateaued, AI‑centric applications are creating a voracious appetite for high‑bandwidth memory and compute power. This demand surge is forcing manufacturers to prioritize premium products like HBM, which command higher margins but exacerbate supply constraints. As a result, analysts now anticipate a revenue surge that eclipses $700 billion in 2026, a milestone that reflects both price inflation and genuine volume expansion in data‑center hardware.

Server refresh cycles, accelerated by hyperscalers’ aggressive capex plans, are a key catalyst behind the upward price trajectory. Enterprises are retiring legacy infrastructure to accommodate larger model parameters and real‑time inference, prompting OEMs to bundle more advanced silicon and connectivity solutions. The resulting lift in average selling prices benefits the top line even as unit shipments remain modest. Meanwhile, the focus on HBM—offering superior throughput at lower volumes—tightens the supply of conventional DRAM and NAND, reinforcing a pricing feedback loop that sustains revenue growth across the value chain.

Beyond the immediate financial uplift, the outlook raises strategic questions for investors and policymakers. Persistent memory shortages could spur new fab investments, yet geopolitical tensions, tariff exposure, and rising energy costs pose material risks to scaling capacity. Consumer segments, though experiencing flat device shipments, will still see revenue gains from higher‑priced memory components in flagship smartphones and foldables. Stakeholders must therefore monitor both the macro‑economic environment and the evolving AI application landscape to gauge the durability of this price‑driven expansion.

Omdia lifts 2026 semiconductor outlook as AI-driven memory constraints intensify

Comments

Want to join the conversation?

Loading comments...