The Bank Charter Gold Rush: What’s Really Happening and What It Means for Banking

Key Takeaways

- •Regulators shifted from zero‑risk to permissive charter stance

- •Preliminary approvals start 18‑month build‑out before opening

- •Charter type choice impacts FDIC, holding‑company status, product scope

- •Fintech banks must adopt rigorous compliance, governance frameworks

- •New banks could revitalize U.S. banking competition and stability

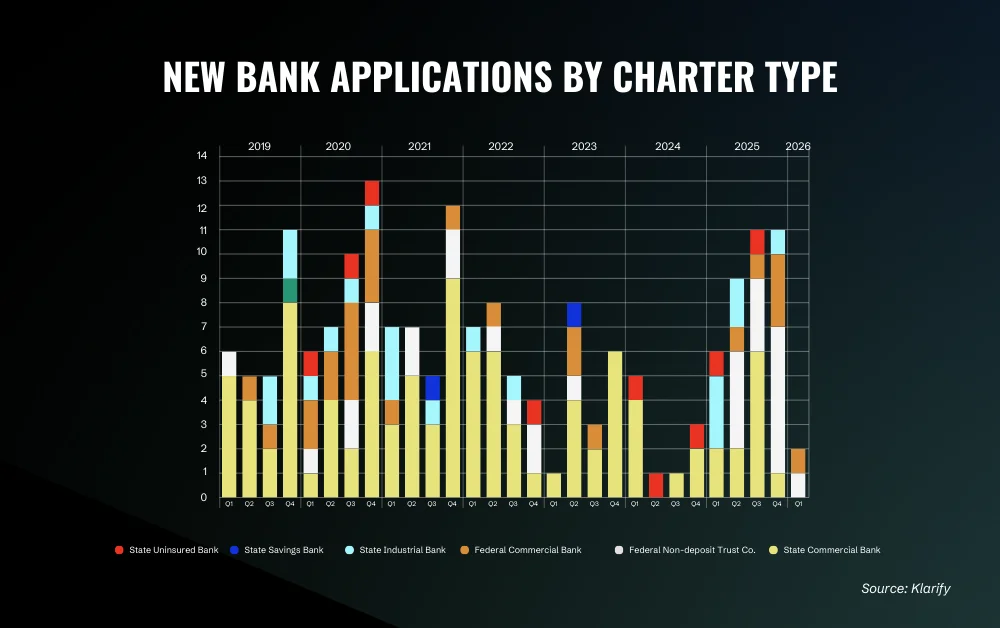

Pulse Analysis

The Office of the Comptroller of the Currency has moved from a near‑zero tolerance stance on new bank formation to an actively encouraging posture, driven by political change and mounting pressure from fintech firms that grew weary of sponsor‑bank constraints. By opening the floodgates to charter applications, regulators aim to bring innovative business models under direct supervision, reducing shadow‑banking risks while capturing emerging technology insights. This policy pivot reflects a broader recognition that the banking ecosystem needs fresh entrants to counteract years of consolidation and to modernize legacy practices.

Securing a preliminary conditional approval is akin to receiving a building permit; the real work begins with an 18‑month “in‑organization” phase where applicants must construct core banking infrastructure, develop comprehensive policies, and assemble seasoned management teams. The choice of charter—national bank, national trust company, or industrial loan company—determines regulatory obligations such as FDIC insurance requirements, holding‑company status, and permissible product suites. Fintechs must therefore align their strategic product roadmap with the regulatory matrix, investing heavily in compliance, risk‑management, and governance structures that differ fundamentally from a partnership model.

If successfully navigated, this charter surge could revitalize the U.S. banking landscape by re‑infusing competition, expanding consumer choice, and restoring the pipeline of small‑bank activity eroded by consolidation. New entrants are expected to introduce digital‑first services, faster credit decisions, and innovative payment solutions, while regulators gain visibility into previously opaque activities. However, the long‑term impact hinges on whether these fintech‑born banks can sustain rigorous supervisory standards without compromising stability, setting a precedent that will shape the regulatory window for future innovators.

The Bank Charter Gold Rush: What’s Really Happening and What it Means for Banking

Comments

Want to join the conversation?