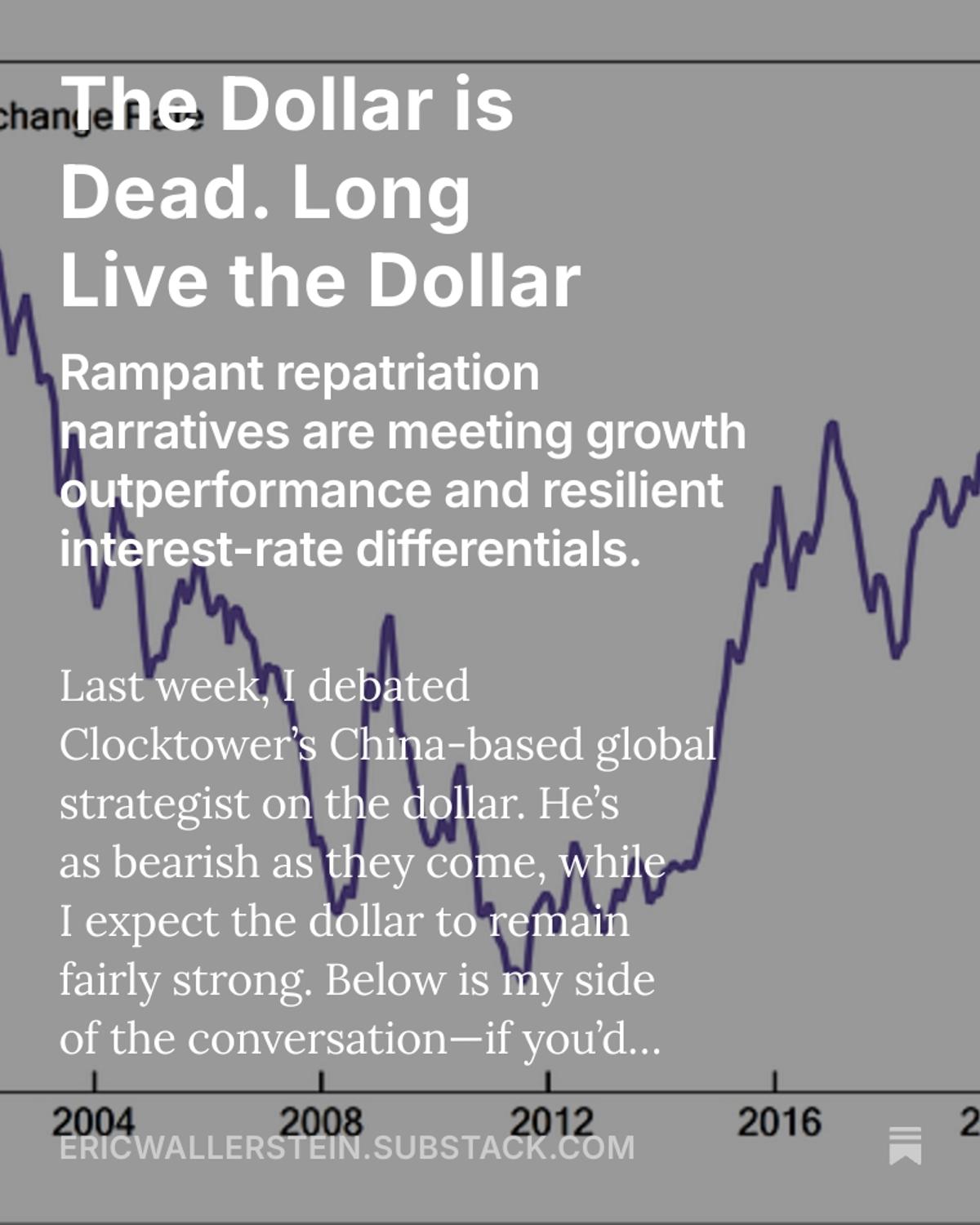

Three Pillars Powering a Strong US Dollar

last week, i debated Clocktower's China-based strategist on the dollar. I laid out three key drivers of a strong USD: 1) US nominal growth outperformance, 2) Interest-rate differentials, 3) Hard power read my side of it: https://t.co/JHqZ8melDk https://t.co/yCvqwgu7zO

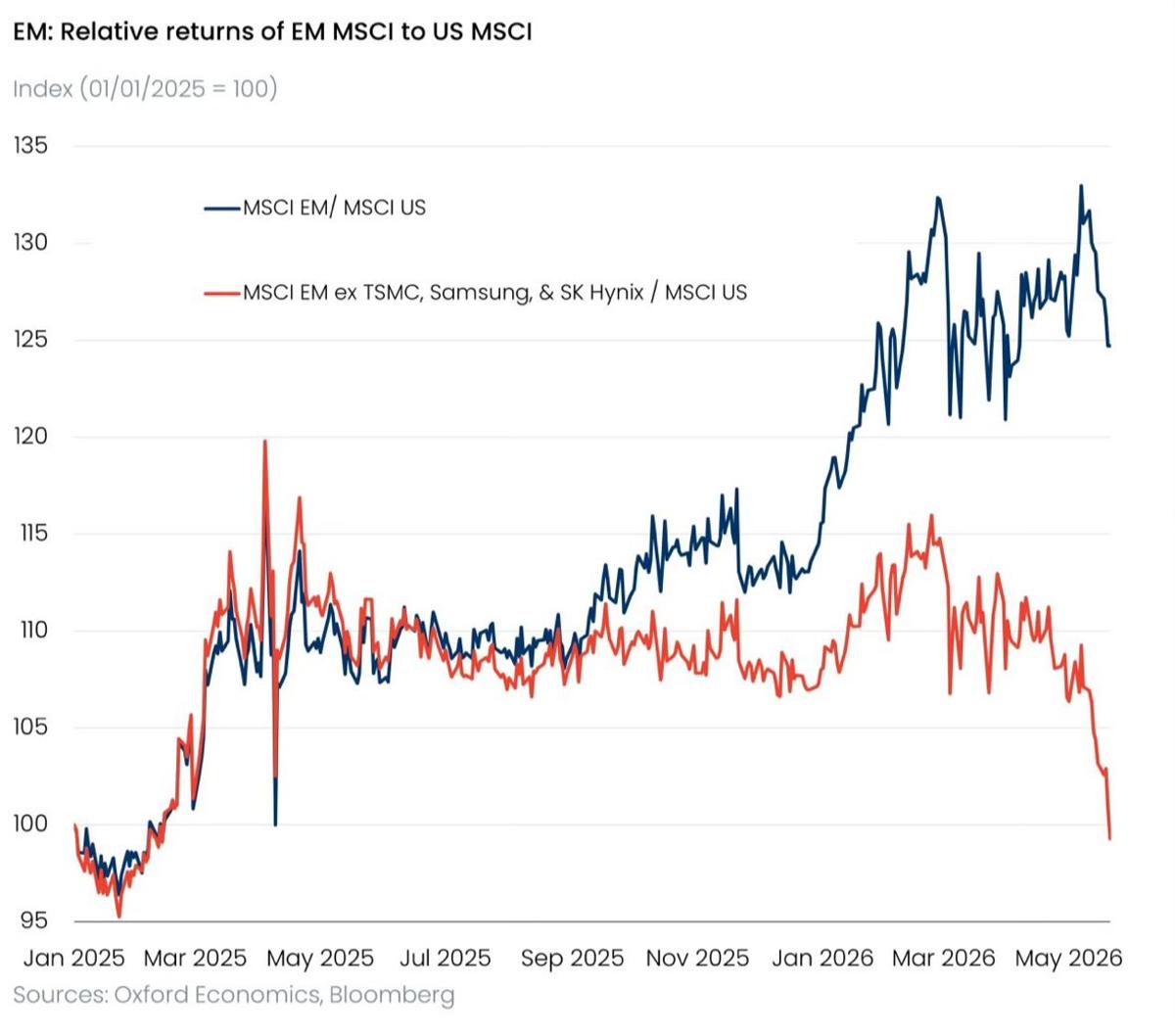

Emerging Markets Slump without TSMC, Samsung, SK Hynix

stole this from Oxford Economics. EM is getting shellacked when you remove TSMC, Samsung and SK Hynix. https://t.co/6HGMppWwmZ

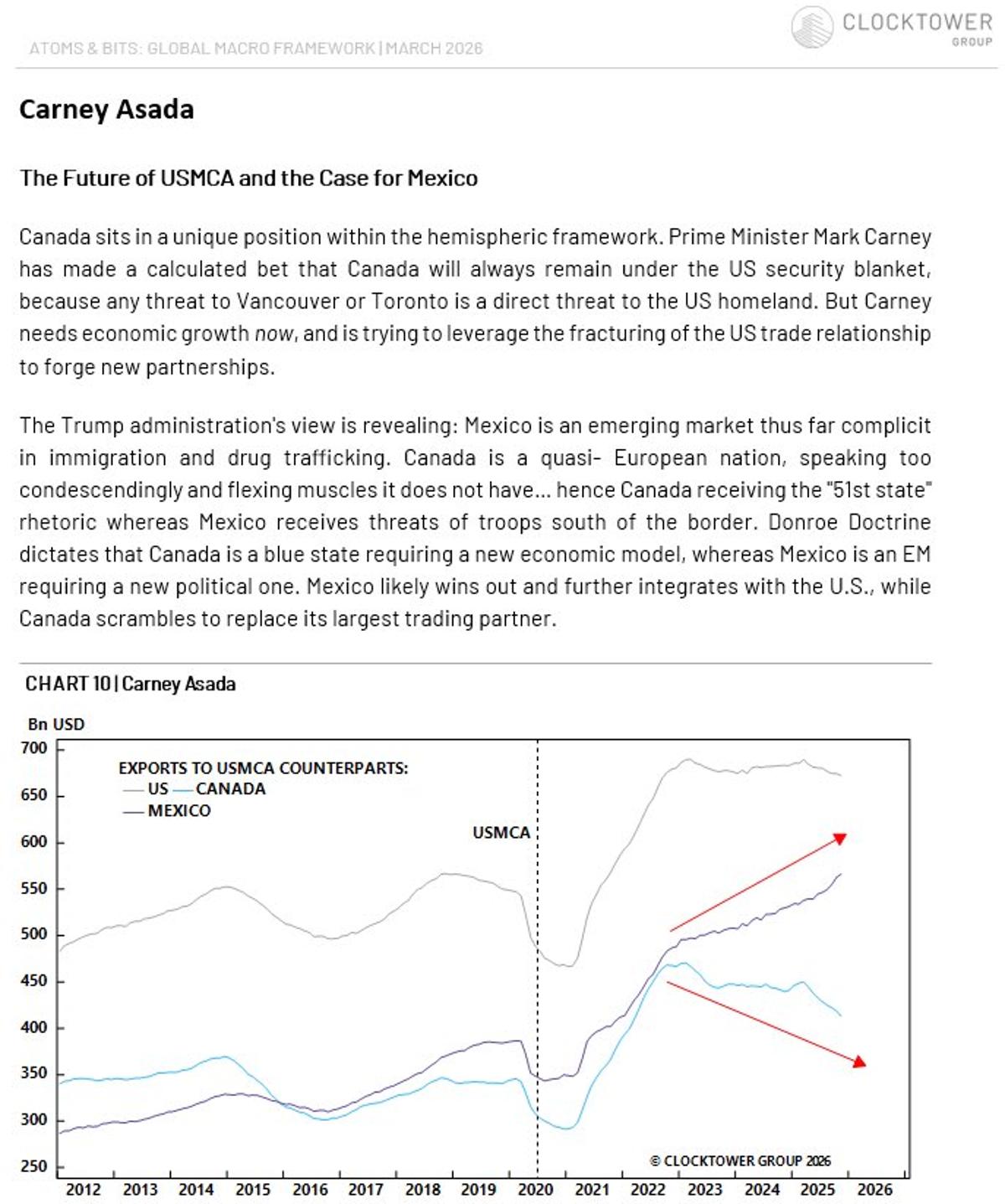

Mexico's April Trade Surplus Surges to 1980 High

“Mexico’s trade surplus widened far more than expected in April to $4.52 billion, well above the median estimate of $476.35 million in a Bloomberg survey, as exports climbed to the highest since the data began in 1980.” Carney Asada in action...

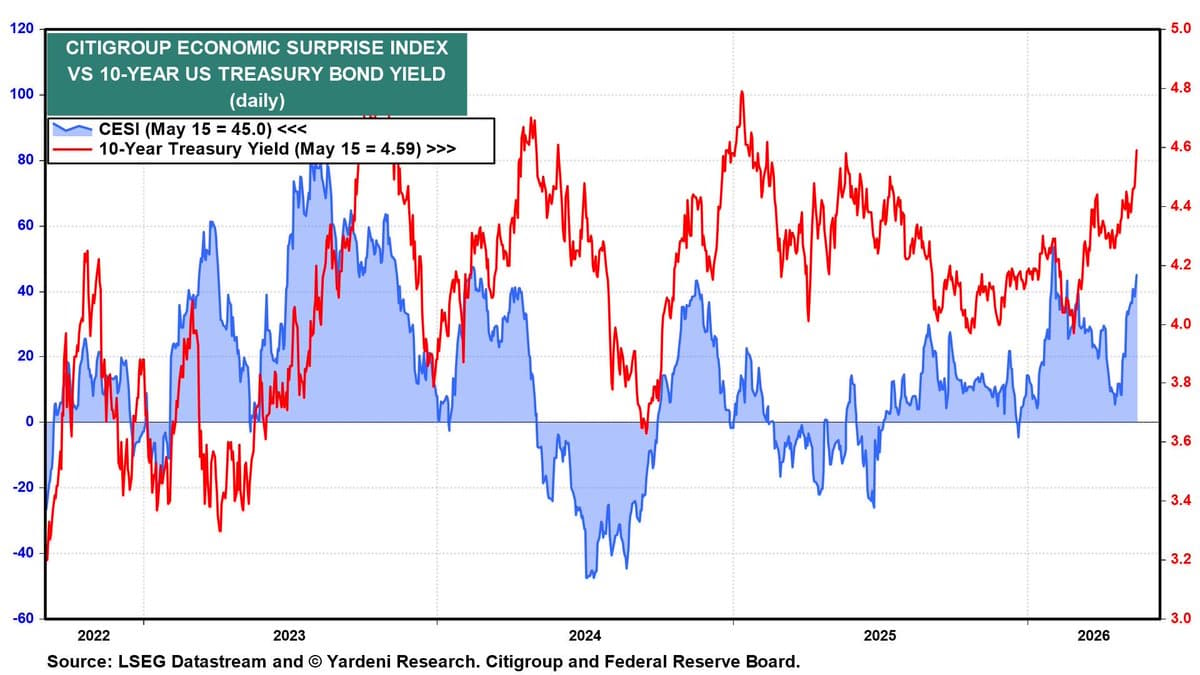

Bond Yields Mirror Mean‑Reverting Economic Surprise Indexes

Economic surprise indexes are mean reverting. Therefore, in an environment where bonds are unsupported by the central bank and thus reflect nominal growth, bond yields are also mean reverting. https://t.co/JvsmHTTqwP

Fed Sets Rates by Labor, Not GDP Growth

i don’t know when commentators adopted this perspective, but the fed doesn’t adjust interest rates based on GDP growth. and no, they would not do so to offset the balance sheet. credible arguments would be to cut rates to get to...

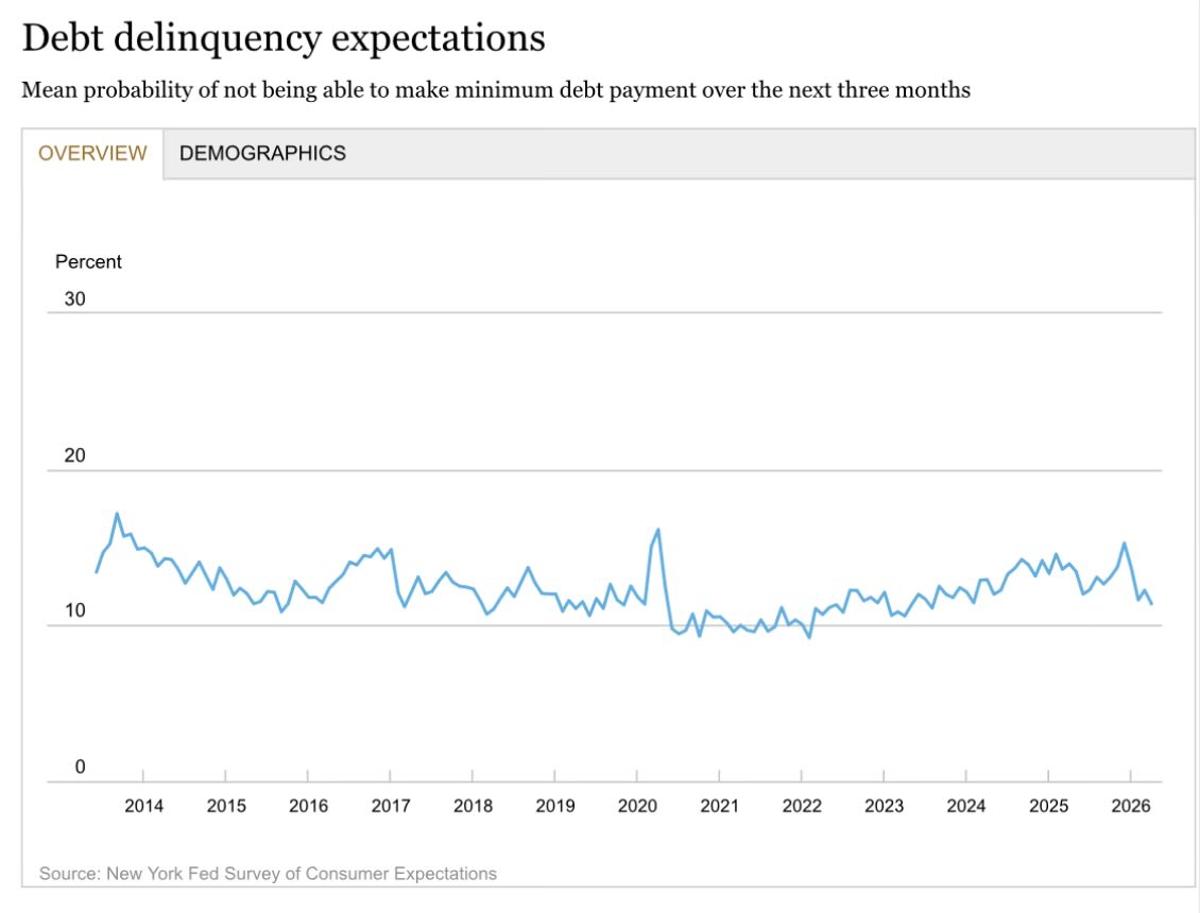

Debt‑payment Default Expectations Hit Two‑year Low

April New York Fed Consumer Survey: expectations for missing a minimum debt payment in the next three months fell to the lowest reading in over two years https://t.co/bkjoY3vzXl

Data Becomes Unlimited Fourth Factor of Production

love this lede from my old boss @yardeni: “Before the Age of AI, economists were taught that there are only three factors of production, namely, Land, Labor, & Capital. The job of economists is to optimize the allocation of these...

Mega IPOs Push New Billionaires Toward US Asset Purchases

the equity supply/demand picture could definitely be complicated by the behemoth IPOs this year. but then i ask, what do newly minted multimillionaires and billionaires do with a flood of liquidity? marginal propensity to consume nearly topped out… i think they...

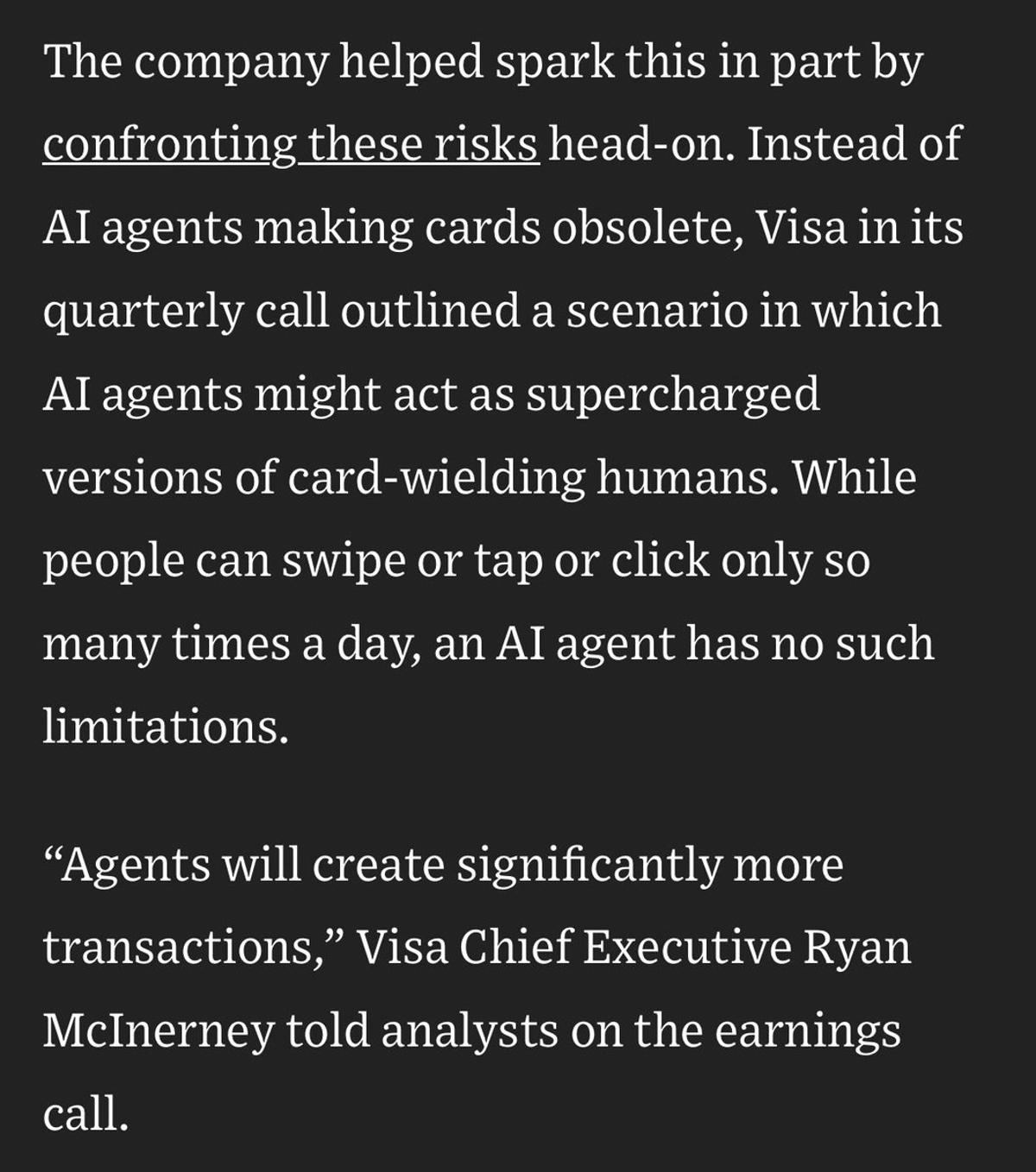

AI‑driven Agents Set to Boost Transaction Volumes

“Agents will create significantly more transactions” - Visa CEO interesting re: AI’s impact on consumption, highlighted by @telisdemos https://t.co/gTAa8tkyw2

Manufacturing's Health Was a Myth; Mass Departures Followed

first slide of my deck when i joined clocktower in Feb was: MANUFACTURING IS IN GOOD SHAPE i lost a lot of people right then & there https://t.co/xwbECgemyw

Takaichi's Low‑Rate Push Risks JGBs, Only Hikes Cure

Takaichi wants to intervene in markets to mitigate inflation, but keep rates low to support her agenda. JGBs will suffer until she realizes hiking rates is the only way to durably keep inflation in check and support JPY. Bank lending has...

Clocktower Seeks Marketing‑Savvy Biz Dev Associate in Santa Monica

Fintwit: Clocktower is expanding our Strategy team, hiring a junior-to-mid level biz dev associate in our Santa Monica office. If you know someone who has a marketing & comms skillset + a deep interest in markets, drop me a line. Details and...

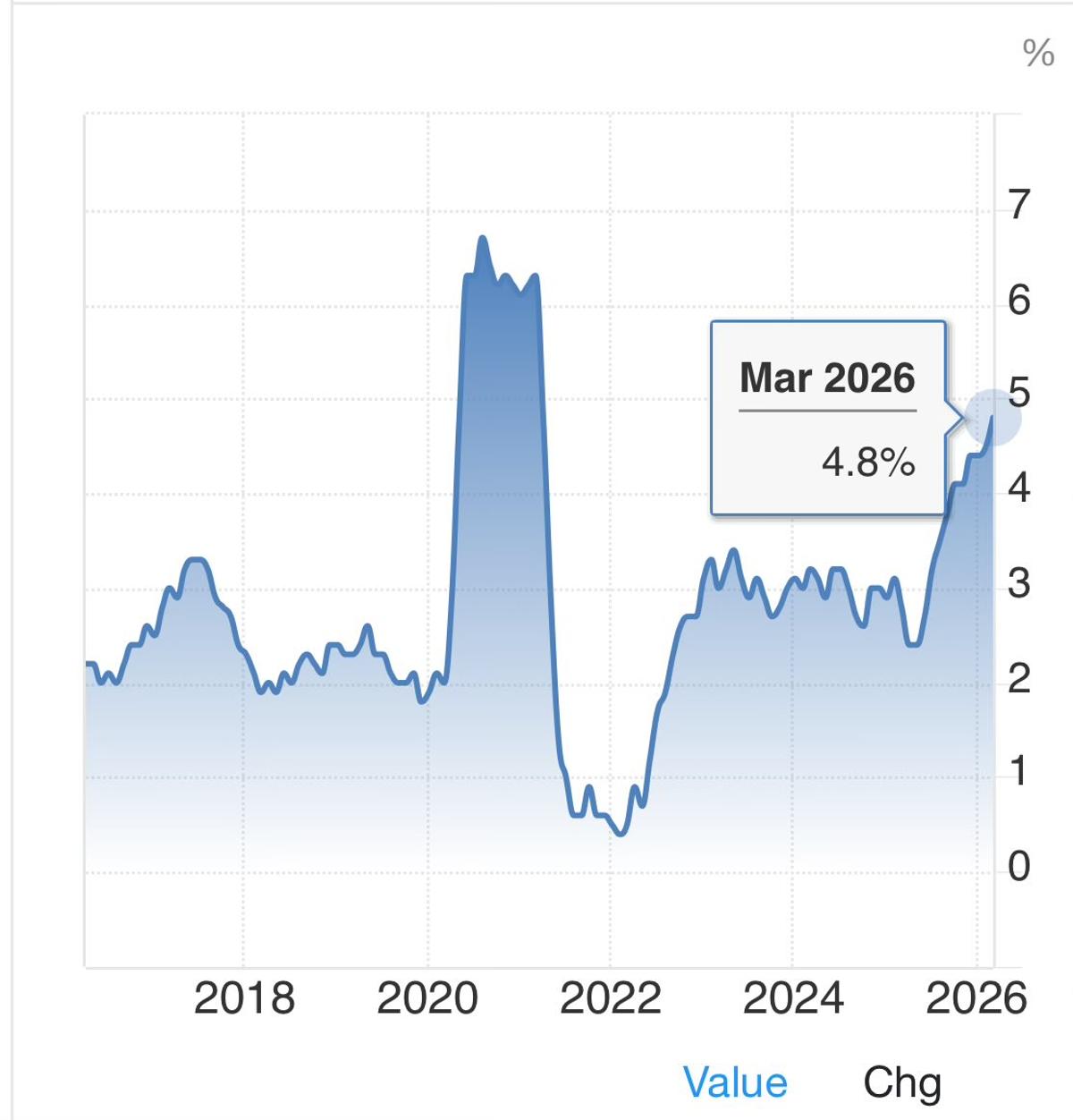

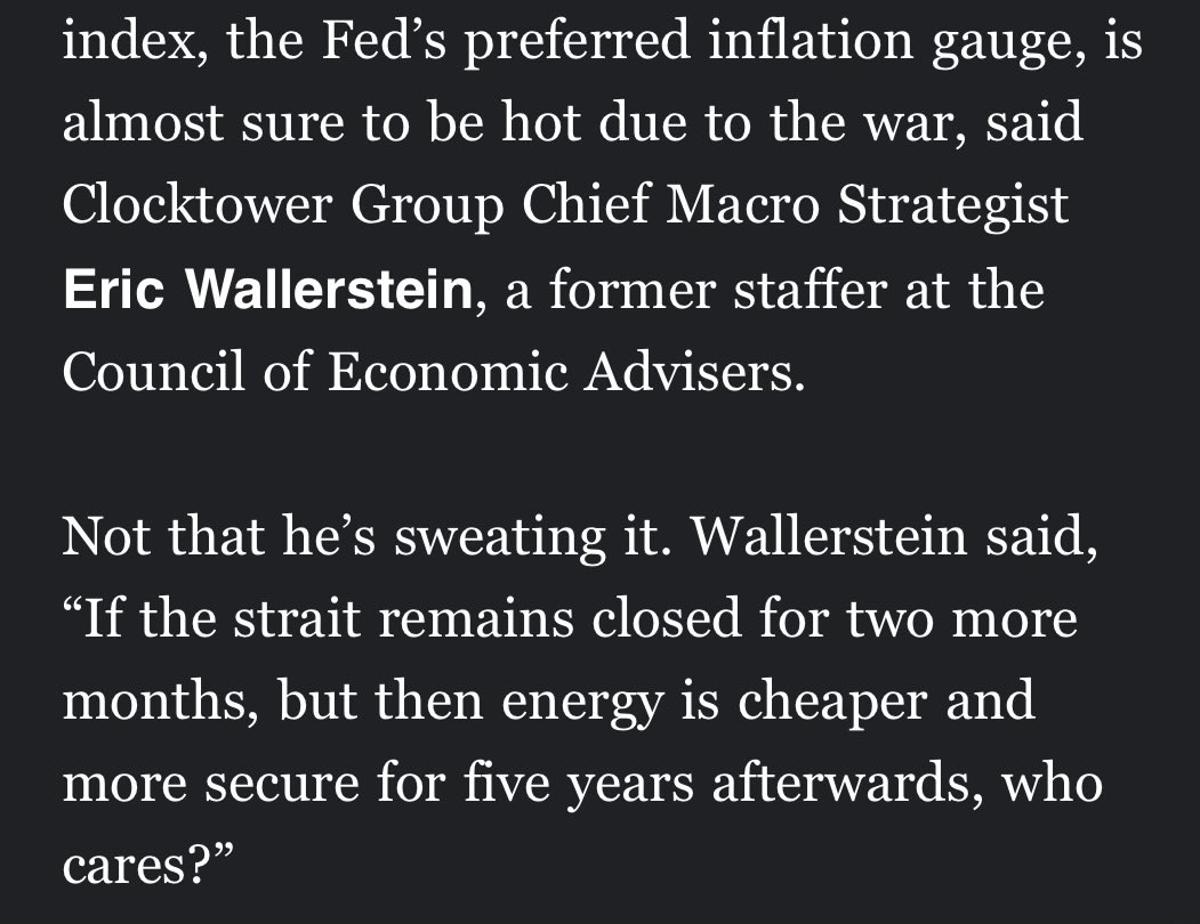

US Sees Limited Economic Impact From Hormuz Blockade

pardon the flippancy, but from a US macroeconomic perspective, i do think the Strait of Hormuz blockade’s impact is limited. more importantly, i believe this is how POTUS is thinking about it. always great catching up with the Politico Morning Money team...

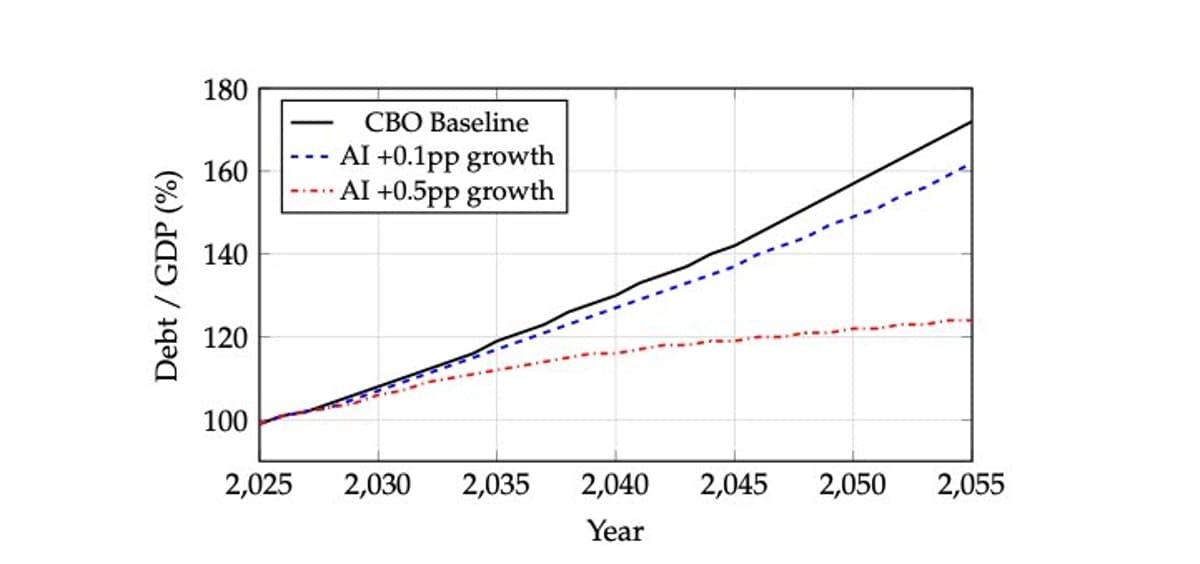

AI Boosts Productivity, Strengthens US Fiscal Outlook

excellent study here, showing that AI-driven productivity growth would be a big benefit for US fiscal dynamics. supports my view that “No, there will not be an AI-induced recession”. recommend reading the entire piece particularly for detail on embedded optionality in...

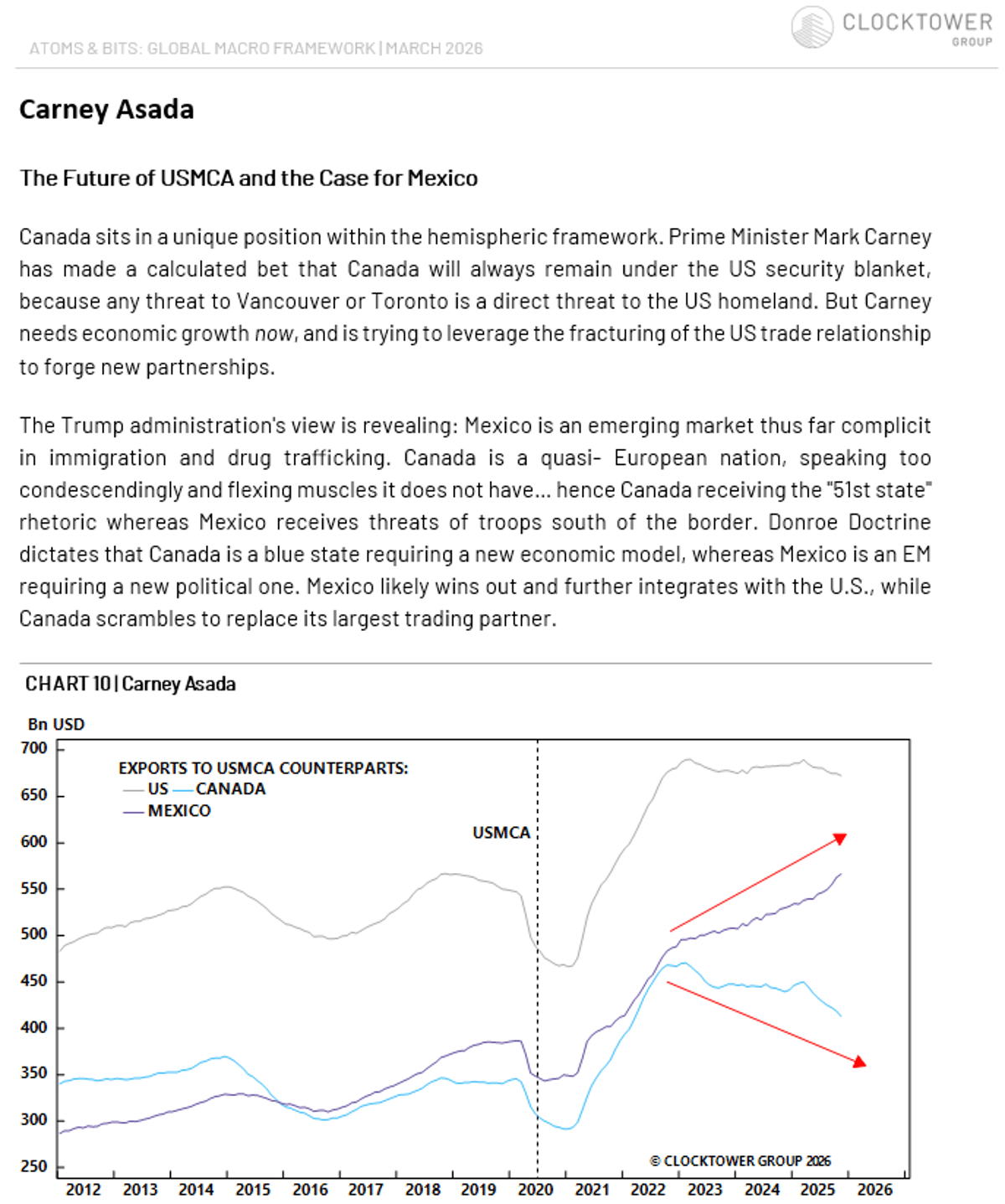

US Threatens Canada Over Wine Ban Amid USMCA Talks

Carney Asada: Canada will get chopped up by USMCA renegotiation. From our early March note 👇 https://t.co/Eca6Me0P8D