VWAP Strategy Will Blow Your Mind!

The video walks viewers through a VWAP‑based trading plan, emphasizing that traders must first confirm the market has enough volatility—typically 60‑80% of the Average True Range (ATR)—before deploying any band‑fade strategy. Using the Dow Jones as an example, the presenter notes the current ATR sits near 784 points, comfortably exceeding the six‑hundred‑point threshold needed for a viable trade. He then illustrates a short entry around the 48,880 level, labeling the initial move as “1L” (line‑to‑line) and targeting a 128‑point profit target. The stop is placed roughly 9,920 points away, reflecting a one‑to‑one risk‑reward ratio, and the speaker stresses that this stop would have been respected even if the trade failed. Key remarks include the rhetorical “do I have enough range?” and the insistence on avoiding cherry‑picking by trading “blind” once the range condition is met. The presenter also clarifies terminology such as “1L” and the importance of aligning targets with market movement rather than static price levels. For traders, the takeaway is a disciplined framework: confirm ATR‑derived range, enter with clear entry/exit points, and maintain strict risk controls. Applying this method can improve consistency in VWAP‑driven strategies, especially in high‑volatility indices like the Dow Jones.

How To Trade With VWAP Profitably

The video tackles the practical challenges of trading with VWAP, emphasizing that profitability stems from disciplined execution rather than reliance on flashy indicators. The presenter argues that most bottom‑line tools simply echo price action and add little value, urging traders...

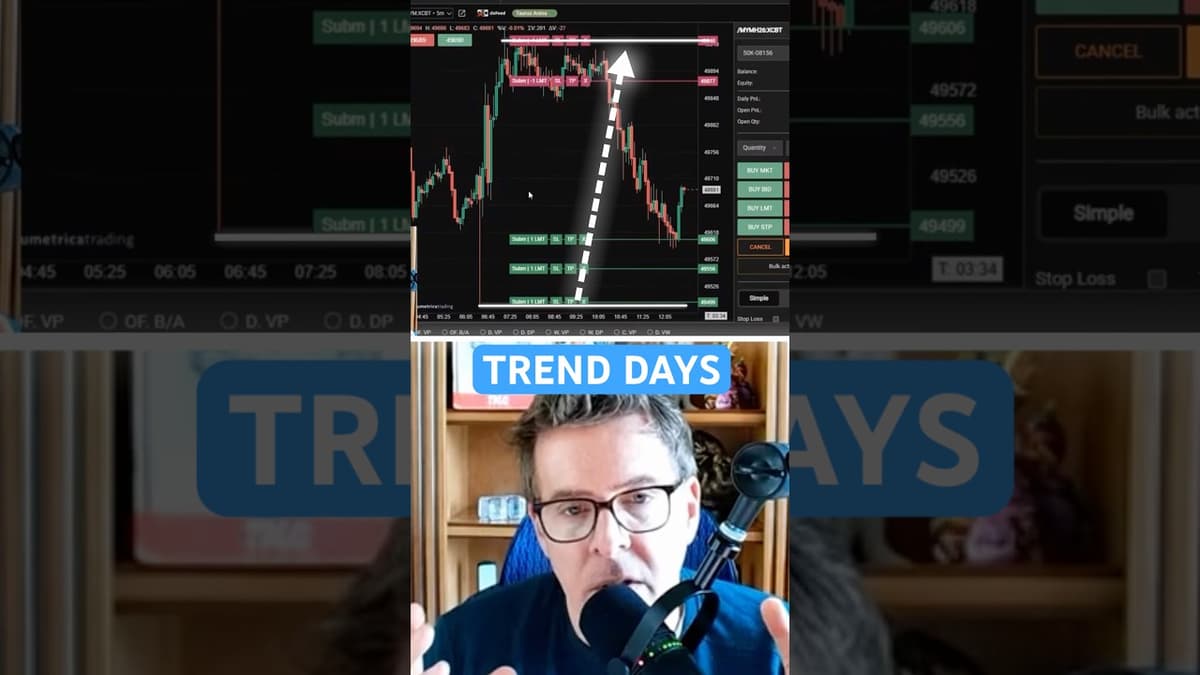

How Trade Trends With Mean Reversion Strategy!

The presenter explains how to distinguish trend days from range days by measuring intraday expected range (example: Dow Jones 78R of 650 points) rather than relying on visual impressions. On range days the recommended tactic is a mean-reversion approach: post...