Follow Charlotte Henry: Your Go‑To Sports Media Expert

Want to give a Friday shout out to the amazing @charlotteahenry who is an essential go to resource on all sports media and business of media news at her site The Addition. She’s also the author of Streaming Wars. And basically just trust me, you should follow her. 🙌🙌 https://t.co/VKkDOE7rfJ

ECB Fears Euro Stablecoins Due to Dollar Deficit

In today's Daily Peg, I allege that the ECB's real paranoia about euro-denominated stablecoins stems from a fundamental and structural dollar deficit across the eurosystem. https://t.co/2oIVNDBppn

Moderna CEO Labels Spike Protein “Garbage” In New Vaccine

Whoa. 🫣 This is incredible. Stephen Hoge, president of Moderna, gave an interview on April 17 to the "why should I trust you?" podcast in which he referred to the spike protein — famously in all the Covid vaccines —...

Join Exclusive Gold Stablecoin Briefing on May 20

Shameless self promo. I'm very excited to reveal that I was asked to contribute a chapter on gold tokenisation for this year's "In Gold We Trust" report, edited by the wonderful @RonStoeferle. The big reveal of the report is on May...

Local Authentication Beats E‑Bay’s Opaque Third‑Party Service

This is super interesting. I sold some old designer stuff on EBay this year and was surprised by how liquid and well bid it was. But also that eBay was now providing a third party authentication service. This definitely added...

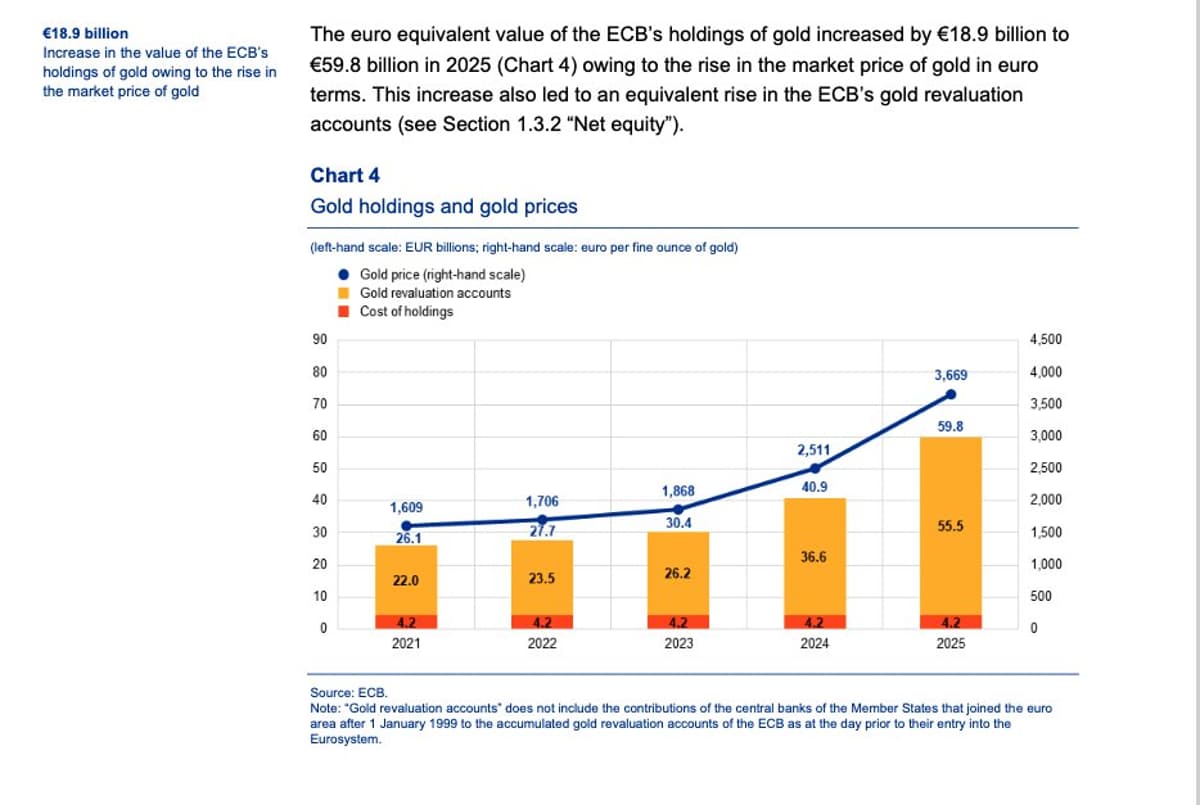

ECB's Gold Revaluation Gains €18.9 Bn From Price Surge

Just catching up on the ECB's 2025 accounts which were out earlier this week and see the gold revaluation account got a nice €18.9 billion uplift from the rise in the price of gold. https://t.co/DDpMzCZMqv

Sovereign Wealth Funds: Backdoor Fiscal Expansion via Investor-Controlled Spending

In this piece, I look at the outbreak of Western Sovereign Wealth Funds from Canada's new proposal to the UK's NWF and conclude they're mostly a way to raise money for industrial policy projects without flipping out bond markets. Aka...

NYTimes' Delayed Coverage Raises Questions About Priorities

What I find more interesting is why it's taken the NYTimes this long to highlight this. https://t.co/ZzT7Hk26XM

Europe's Mispriced US Security Model Demands New Solidarity

MUST READ VoxEU Column from Marco Buti Giancarlo Corsetti Anna Peychev 👇 TLDR: Europe has significantly mispriced the value generated by American Security umbrella and created an economic model that simply doesn't finance itself on strategic autonomy grounds. They refer...

Dollaryuan Market Emerges as Key Global Currency Shift

There are lots of moving parts at the moment. But a key one involves the possible formation of a dollaryuan market (or will it be called a yuandollar market? Yet to be determined). https://t.co/NuEwX8HNB6

Emerging Markets Shift to Gold as Dollar Reserves Shrink

Deutsche’s George Saravelos highlights today that “the share of US dollars in central bank reserves is once more in decline. It has fallen from over 60% to just 40%, while gold’s share has tripled from its lows to 30% today.” And: “...

London’s Eurodollar Rise Stemmed From Belgian, French Rejection

🏴☠️1/ If what I think is happening is really happening, then I can make some predictions. Especially about incoming European problems. But first an important side story, which also relates to the “special relationship”. What a lot of people don’t know is...

Defying OPEC Quotas Invites Invasion, UAE Demands Guarantees

Probably worth reminding that the last time a gulf state defied opec quotas in the context of damages from a wider regional war with Iran, it also got invaded. Context was that after the Iran–Iraq War, Iraq was heavily indebted and...

Most People Prefer Chaos Over Inbox Zero

On average, do you operate: 1) an "inbox zero" policy (all emails processed every time you open your inbox, you have clearly defined filters, which are also at zero), 2) a chronological management inbox policy (you process what you can when...

Trump Highlights Ascension Island's Role in Falklands Victory

In my latest piece for The Blind Spot, I explore how Donald Trump may be seeking to remind Britain just how pivotal US-backed access to Ascension Island was to its ability to retake the Falklands. And what really underpins the...

Chinese Commodity Stockpiles Offer Surplus Investment Alternative

Great perspective on massive Chinese commodity stockpiles. Not necessarily strategic thinking but somewhere to invest one’s surpluses (other than non performing BRI investments).

Modern Lend-Lease: Funding Recovery to Protect Neighborhood Value

The old lend lease was about lending your neighbour a hose when he had a fire to protect the neighbourhood. The new lend lease is about lending your neighbour the capital he needs to repossess his house after a home...

US May Weaponize Dollar Swap Lines Amid Tensions

🧵Some other important swap line factoids: 1/ Robert McCauley has been warning about the potential weaponisation of dollar swap lines for quite a while. In this view, the US is likely to apply statecrafty terms and conditions on dollar...

Falklands War: Censored Conflict, Media Spin, Political Distraction

The funny thing is, when I was reading the Citrini report where they sent their analyst to Oman to count the ships getting through the Hormuz, all I could think of was Brian Hanrahan counting them out and counting them...

USD Swap Lines Misunderstood: Liquidity Shakedowns Explained

Two-part compendium from me on why everyone is getting the wrong end of the stick on USD swap lines and how liquidity shakedowns really work with asset-rich sovereigns. First piece here: https://t.co/DkaYPexxOU https://t.co/2wWxKXkaWz

Putin Orders Oil Profits to Relieve Russian Banking Crisis

Looks like Russia may finally be facing a banking and economic crisis. Putin has told Russia’s oil and gas companies that they should use windfall oil profits triggered by the war in Iran “to reduce their debt burden and pay...

ECB Fuels US‑payment Paranoia to Accelerate Digital Euro

ECB's Piero Cipollone is currently being grilled by Nicolas Veron on the digital euro in a refreshingly sharp way. Veron just pointed out that the ECB's paranoia about the US payment companies pulling out of Europe is somewhat far-fetched, to...

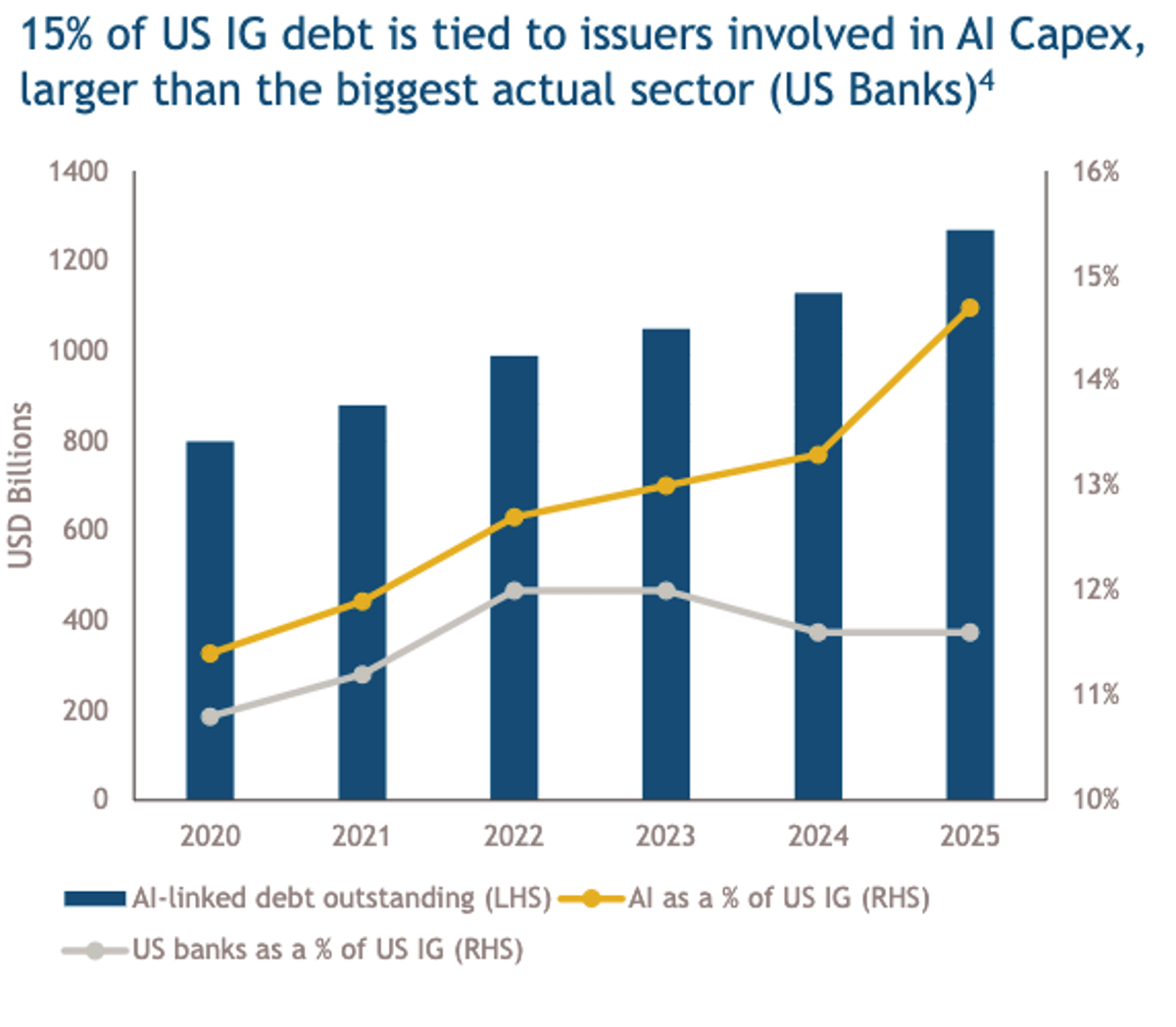

Europe Still Buying U.S. Defense Amid Domestic‑Buy Talk

Interesting detail from today’s Northrop Grumman Q1 earnings call re. European demand. Despite political messaging in Europe about buying domestically and reducing reliance on U.S. suppliers, Northrop made clear that European customers remain highly engaged buyers of American systems.

Seasoned Twitter Users Still Fall Victim to Sophisticated Smear

I have been on Twitter since the earliest of days. In that time I have been subject to a plethora of different pile ons, gaslighting campaigns and silencing attempts. The most egregious and sophisticated of these (which I was pulled...

Palantir Forces Public Sector Transparency, Threatening Opacity

How many people know that Palantir has always explicitly sought to create an operational environment in which decisions, data, and actions by the PUBLIC SECTOR are so thoroughly recorded and linked that they can always be reconstructed and scrutinized after...

Stablecoin Statecraft Mirrors BCCI’s Controversial Model

Putting the statecraft into stablecoin statecraft in a way that makes you wonder if USD1 is just the second coming of BCCI?

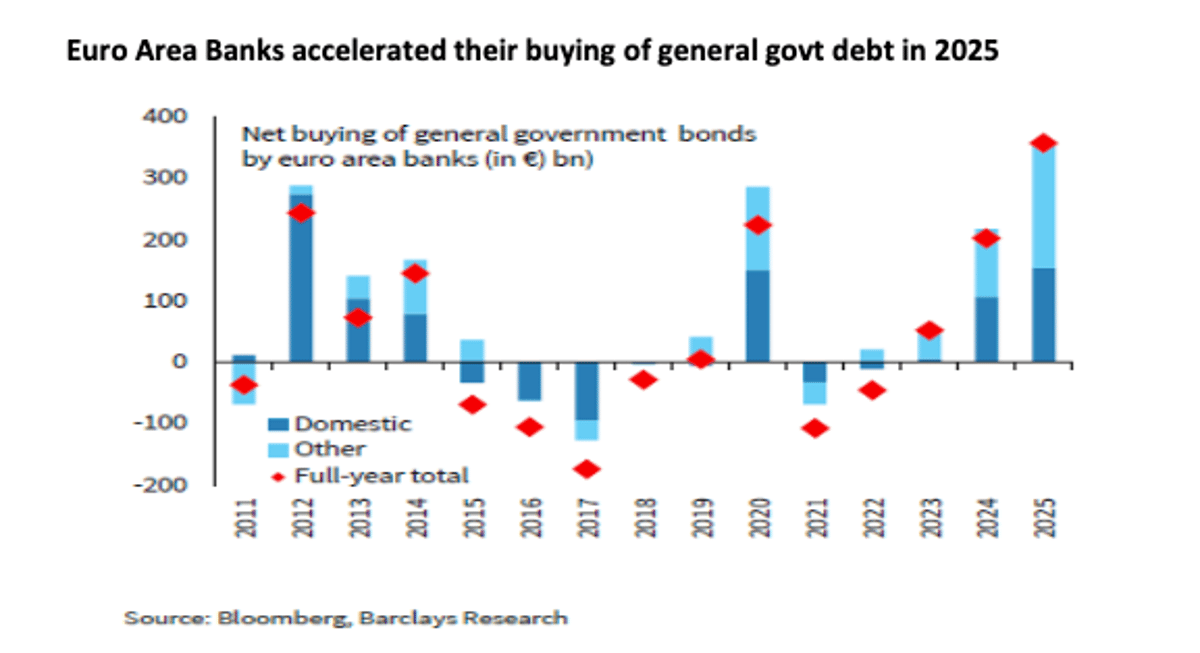

15% of US IG Debt Now Tied to AI Capex

Some 15% of US IG debt is now tied to issuers involved in AI Capex (chart via Muzinich & Co) https://t.co/5F2NY2AnxN

Banks, Not Stablecoins, Already Stabilize Sovereign Debt

So much focus on stablecoins becoming a new source of "stabilising" demand for government debt. But looks like banks — largely due to regulation — already step in when it really matters. https://t.co/52BOQ3n5iM

China Threatens Employee Penalties to Deter Supply‑chain Decoupling

This is extraordinary: China’s response to Western firms diversifying supply chains is to threaten penalties on their own employees and executives inside China if they “decouple.” It’s like an abusive partner reacting to a breakup by threatening the kids or shared...

Gold Plummets, Arab Views Iran, US Creates Defense Unit

In today's daily Discord linkfest: Gold has its worst month in decades, the Arab world has a very different perspective on the Iran crisis and the US launches a new DOD Economic Defense Unit. https://t.co/CJiFQqhl8n

Stablecoins Compared to Civil War Financing Amid USDC Denial

In today's Daily Peg, Circle CEO denies USDC is being used for Hormuz toll payments and Axa's Giles Moec, writing in CEPR's New Global Imbalances report, recounts why stablecoins are a throwback to US Civil War financing structures. https://t.co/5ZwDkmoknk

ECB Remains Noncommittal on Stablecoins Boosting Bond Demand

In today’s Daily Peg (my stablecoin dedicated newsletter) the ECB offers non committal perspectives about whether or not stablecoins create net new demand for sovereign bonds. https://t.co/41t2azueoh

Dollar Exists to Guard Capitalism, Not Just Cover Deficits

There are so many layers to the dollar story that transcend conventional market economic dynamics. Until investors realise this I do believe they will be caught out by narratives that serve political agendas not reality. Crucially, most “end of the dollar”...

Petrodollar Death Rants Are Wishful, Not Insightful

🧵There’s been an acute breakout of death of the petrodollar thought pieces over the weekend. This should have discerning investors thinking twice. Not about the dollar, however. About piling into an obviously crowded and extremely unoriginal perspective that is mostly...

Recreating a 1865 Family Babka Recipe Today

Today I will be trying to recreate this recipe from a family cook book that dates back to 1865 for a “very good babka”. Wish me luck. https://t.co/MH1rOe8zg3

NEOM: Saudi’s Green Steel Powerhouse Driving Future Industry

I think a lot of people overlook that NEOM is as much a strategic play on future green steel production as it is a weird futuristic city. Also, Saudi is via the project positioning itself to be - in the...

Extortion Can't Sustain a Reserve Currency, Bitcoin Shows Why

The other point I make: if extortion was enough to make a reserve currency then we would all be on a bitcoin standard by now. https://t.co/lTW4ry33Lp

Dollar May Fade, But Not Anytime Soon

In my latest Telegraph column I defend the dollar by channelling @TomCruise’s Maverick. To the claim that the dollar is probably headed for extinction, I say: Maybe so. But not today. https://t.co/lTW4ry33Lp https://t.co/q9PtKebSYk

Stablecoins Fail to Escape Bank Balance‑Sheet Limits, Worsen CIP Distortions

Fascinating new paper from Iñaki Aldasoro et al which argues that stablecoins don’t get around existing bank balance sheet constraints. Exacerbate the CIP distortions if anything. https://t.co/p5y5qOA4kX

Russell & Bromley's Collapse Signals Middle‑class Decline

FRIDAY 👢 TRAGEDY 😢. Russell & Bromley has collapsed into administration and is fire-selling all its stock. This is actually incredibly horrible. Where am I going to get my nice shoes from? It was literally the last proper shoemaker in...

BoE Independence Questioned as Letter‑Writing Ritual Sparks US Controversy

Reading this, all I can think is: what does it say about BoE “independence” if even considering its letter-writing model is deemed hyper controversial in the US? Moreover, I suspect a few former UK PMs would dispute the idea that...

Gold May Not Rebound If Fed Shrinks Balance Sheet

So weird anyone is surprised by this. Time and time again, gold falls at the peak of a liquidity/financial crisis because people liquidate emergency supplies. Note Turkey. But then usually corrects higher once things stabilise (especially if Cbanks flood the...

US Fuels Chaos to Cripple China AI, Bind Europe

Really recommend this interview between @freddiesayers and energy expert @HelenHet20 where Helen lays out why markets may be wrong in assuming things will return to normal once Iran is neutralised. The chaos may be the strategy. And whichever way you...

Fake News Flagged, yet Algorithms Boost Contradictory Stories

Fake news is everywhere. The names Paweł and Gaweł were a red flag to begin with. But more so this would have been contra what the govt said earlier. What’s interesting is how this stuff is being pumped into the...

Treasury Tapped Parallel Dollar Market, Used $2.5B, Made Profit

👀 💵Remember the fuss about Bessent conducting an ESF-funded fx swap exchange to support the Argentinian peso back in October 2025? We now have the details of those transactions via the quarterly reporting Congress requires for Treasury’s Exchange Stabilization Fund operations. They...

Poland to Fund Program Using Unrealized Gold Gains

Based on what Glapinski said during his press conference two days ago, all indications are, as I expected, that the plan is to use unrealised gains on the NBP's gold to fund the programme. https://t.co/csre6RPhlr

Gold Not Sold, Gains Funding Rearmament Plan

Lots of very misplaced reporting and speculation about Glapinski's gold "sale" for rearmanent plan. It's not a sale. Latest indications are it's about using the unrealised gains on the gold they bought to fund a rearmament program. The whole back...

Unsure About Hormuz? Check This Detailed Analysis

Lots of people asking me my opinion on the Hormuz situation. The truth is I don’t really know what to think. But my inclination is to direct everyone to this link: https://t.co/YQsMAPHfJr

Western Private Credit Crisis Mirrors Economic Involution

In which I argue that the West’s developing private credit crisis is just its equivalent of “involution”. https://t.co/1wAWnParft

Join Nick Cook for Exclusive Military Tech Dinner

The Blind Spot is hosting former aerospace & defence journalist Nick Cook, author of The Hunt for Zero Point, for an exclusive dinner in West London on March 25. Expect conversation on advanced military tech, disclosure developments, audience Q&A, and book...