Quant Science

Quant trader/educator discussing algorithmic strategies (e.g., time‑series momentum) and portfolio construction—advanced market methods adjacent to derivatives.

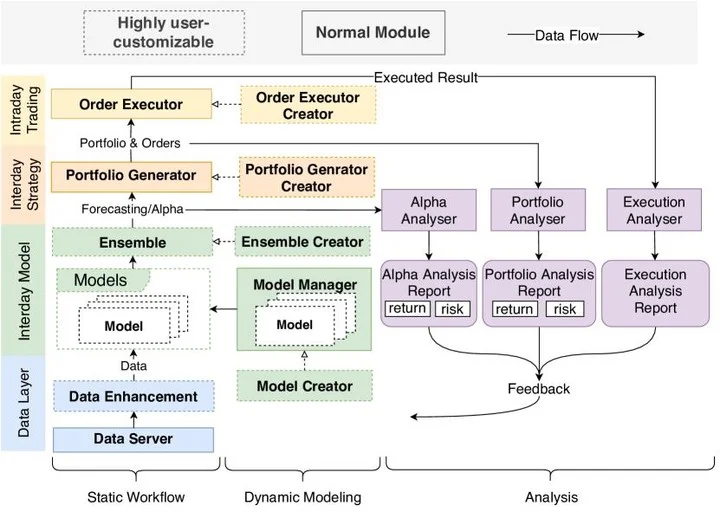

Microsoft Releases AI Quant Investment Platform as Open-Source

Microsoft open-sourced this AI quant investment platform 100% for free Here's what it does (and how to get it for free):

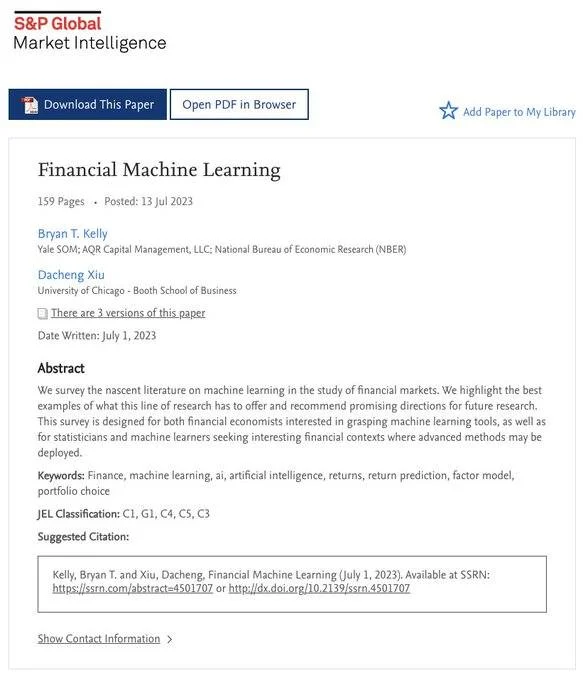

Top Machine Learning Use Cases in Finance & Trading

159 page PDF download. The best examples of how machine learning is used in finance and algorithmic trading. Grab the paper here:

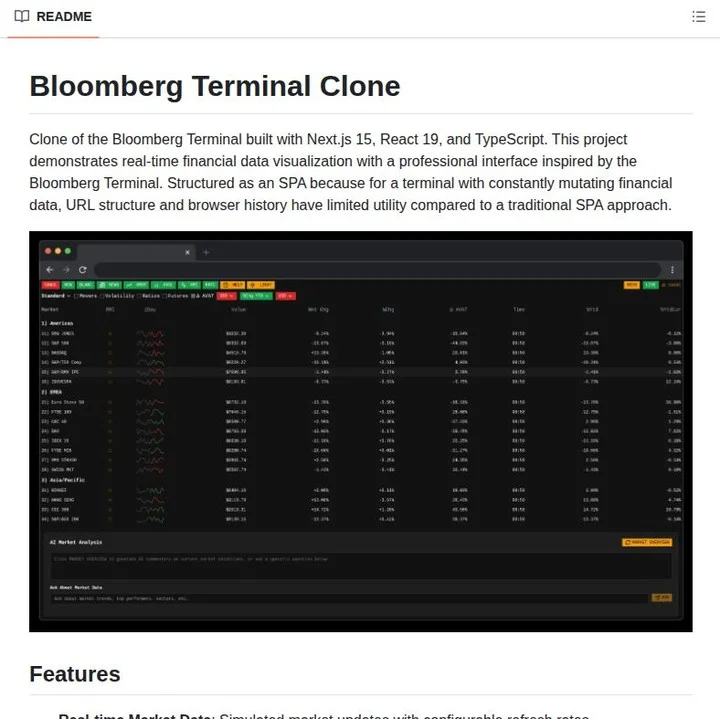

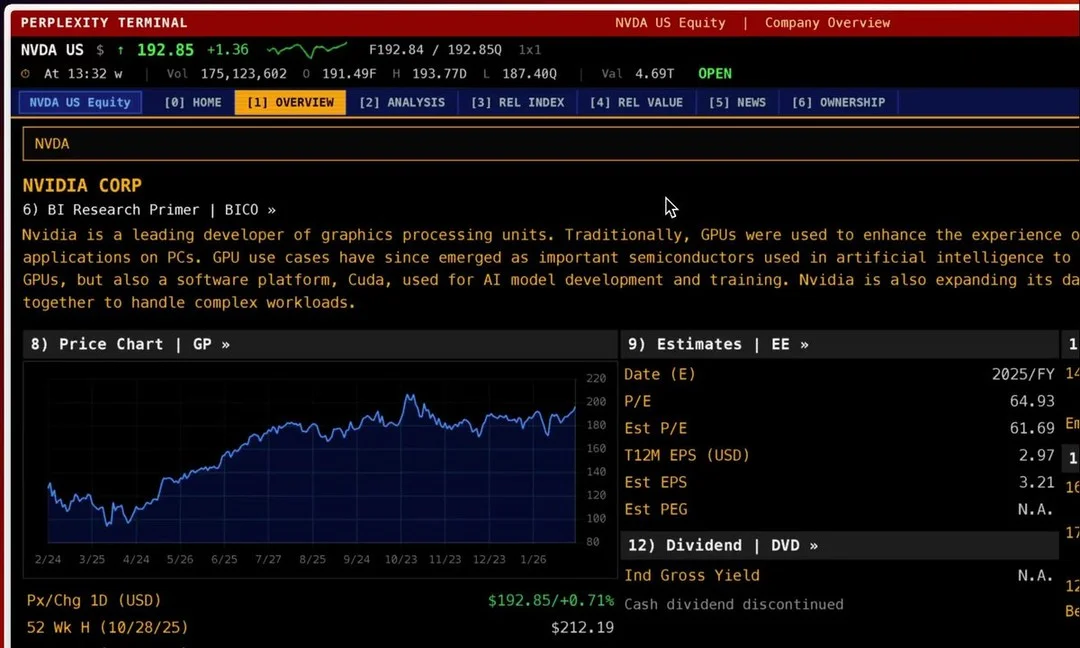

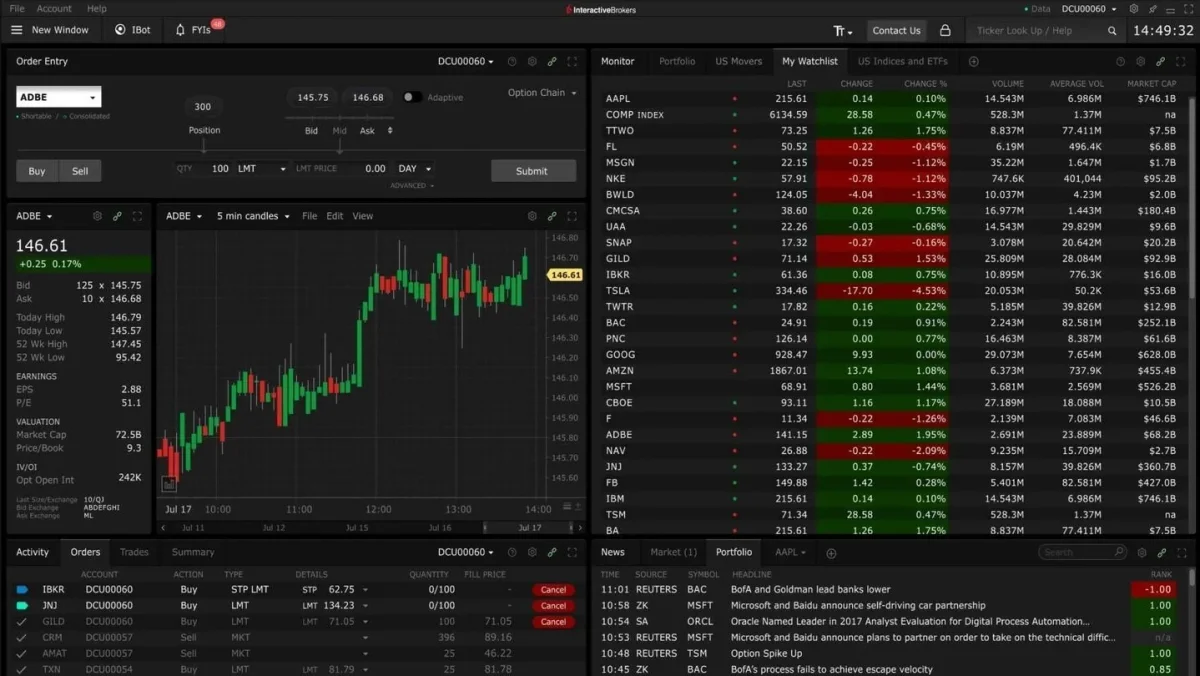

Open‑source Bloomberg Clone Offers Free Alternative to $30k Terminal

A Bloomberg Terminal costs $30,000 a year. This guy made a Bloomberg Terminal clone. Then open sourced it (for free). Get it here:

Free Bloomberg Terminal Clone Built in Minutes, No Setup

A Bloomberg Terminal costs $30,000 a year. Someone just built one for free. In minutes. With no local setup.

Top Factor #3 Drives 10X Stock Returns

The secret of hedge funds is revealed in a 41-page PDF: This paper analyzed 464 stocks that 10X-ed over a 24-year period. Here are the best factors that drive outperformance: (number 3 is the best 🧵)

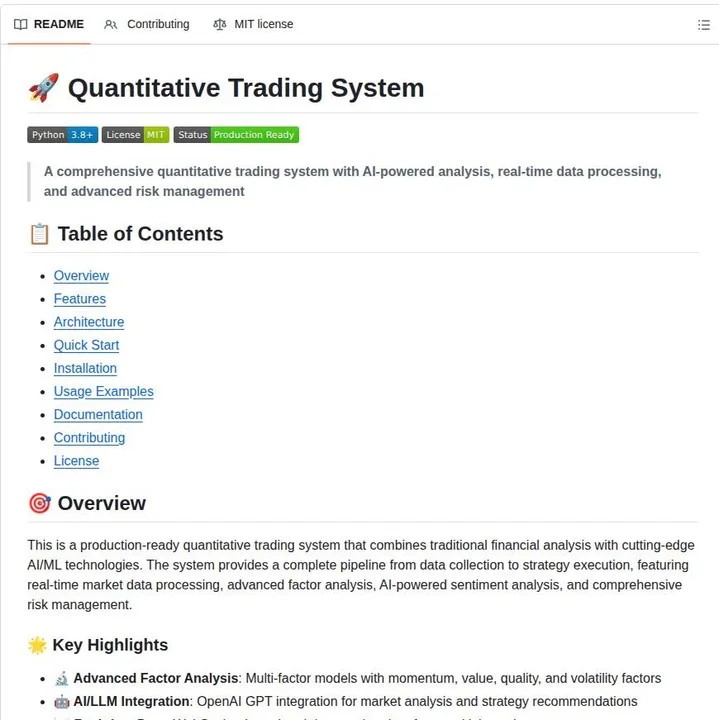

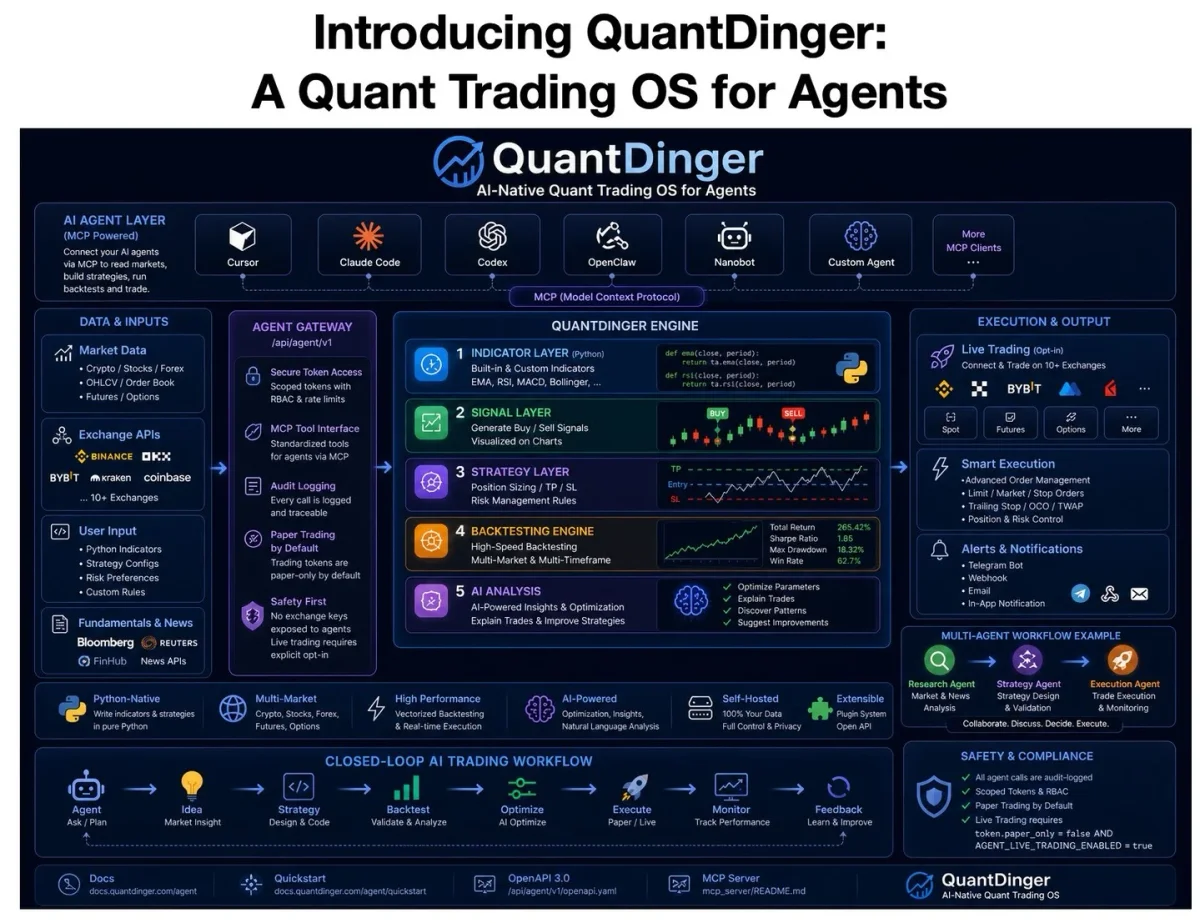

Open‑source AI‑powered Quant Trading System Released in Python

Some guy made a quant trading system that uses AI, real-time data processing, and risk management. Then open sourced it for free in Python. Here it is:

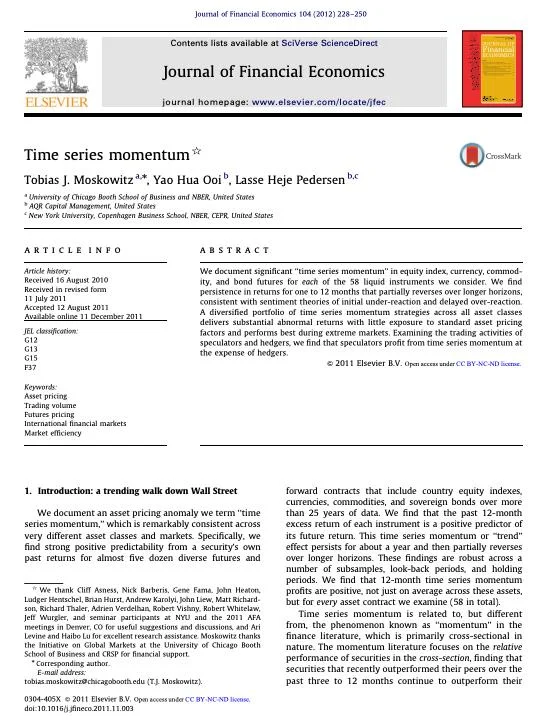

Hedge Funds Beat Market Using Time Series Momentum

A 23-page research paper reveals the number 1 method Hedge Funds use to beat the market: Time Series Momentum This is how: 🧵

Build an Algo Trading Hedge Fund in Six Minutes

This guy literally explains how to build an algorithmic trading hedge fund from scratch in under 6 minutes. This is crazy:

All Hedge Fund Algorithms Revealed in 151 Strategies

This paper unlocks every algorithm used by hedge funds. 151 trading strategies. Get it here (361 page PDF):

Seek Uncorrelated Returns to Simplify Risk Management

According to Ray Dalio, the easiest way to adjust for risk is to seek uncorrelated returns. Ray's made billions from a simple idea. Here's how to do it in a few lines of Python code:

Free Open-Source AI Tool Bridges Gap for Algo Traders

90% of algorithmic traders aren't using AI and Agents for live trading and research. So this guy open-sourced something to help (for free):

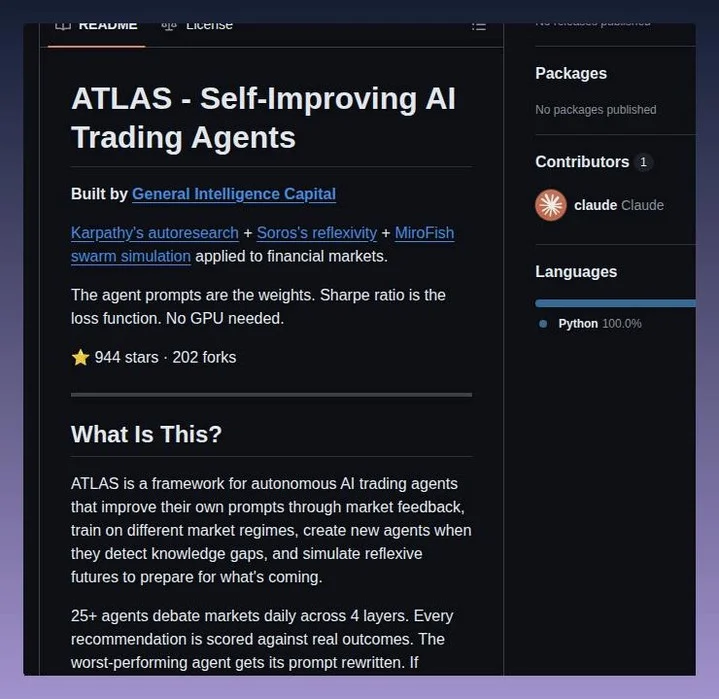

Free Open‑Source Self‑Improving Trading AI Library Released

Some guy made a python library of self-improving algorithmic trading AI agents Then gave it away for free:

Build a Mini Hedge Fund with Python Algo Trading

How to create your own "mini" hedge fund with algorithmic trading and Python A thread 🧵

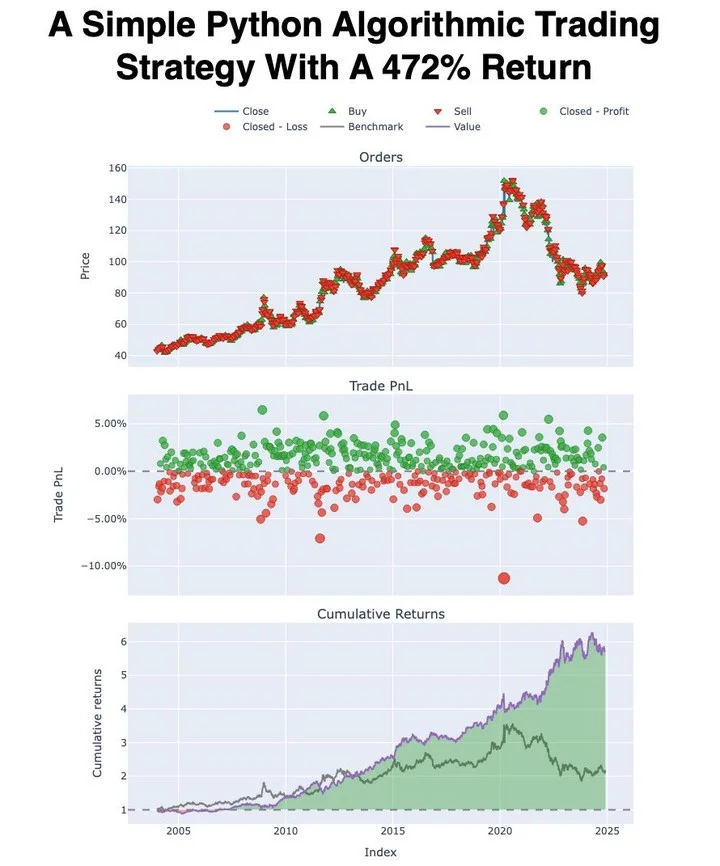

Build a Python Algo for 472% Returns

How to make a simple algorithmic trading strategy with a 472% return using Python. A thread. 🧵

Build an Algo Trading Hedge Fund in Six Minutes

This guy literally explains how to build an algorithmic trading hedge fund from scratch in under 6 minutes. This is crazy: