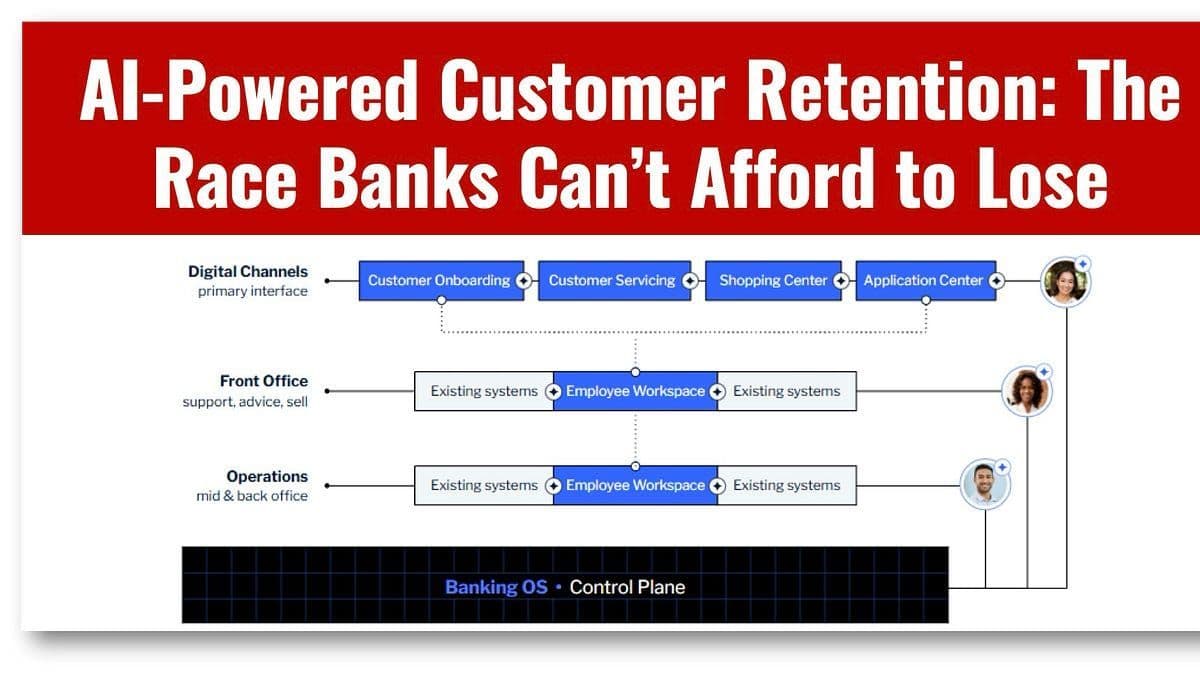

Banking OS: Only Viable AI Path for Legacy Systems

Banks have three options for AI on legacy tech. Only one works. ↳ Do nothing — bolt AI onto fragmented systems. Innovation theater. Never scales ↳ Full cloud rip-and-replace — 94% of modernization projects exceed deadlines, 50%+ over budget ↳ Banking OS — sits above existing core, unified customer view, AI-native without replacing infrastructure 55% of technology providers expect a winner-takes-all or fragmented banking market by 2030. The window to choose is closing. https://t.co/iTQbSzwNsk #fintech #tech #finserv #AI @BetaMoroney @Backbase @efipm @BrettKing @spirosmargaris @jasuja @enricomolinari @mikeflache

Stablecoins Are Risky Structured Products; Banks Favor Tokenized Deposits

Stablecoins are structured products with a better name. That's not a dismissal. It's an accurate description of the credit and settlement risk they carry, a risk that makes them less than ideal for wholesale institutional settlement. Citi flags "settlement risk from private...

AI‑Native Ryt Bank Proves AI Banking Works

Ryt Bank launched in August 2025. Seven months later: 1.2 million users, 25 million transactions, monthly volumes 35x higher than at launch. That is not a perpetual AI pilot. That is a working AI-native bank. ↳ NPS score of 76 — exceptional...

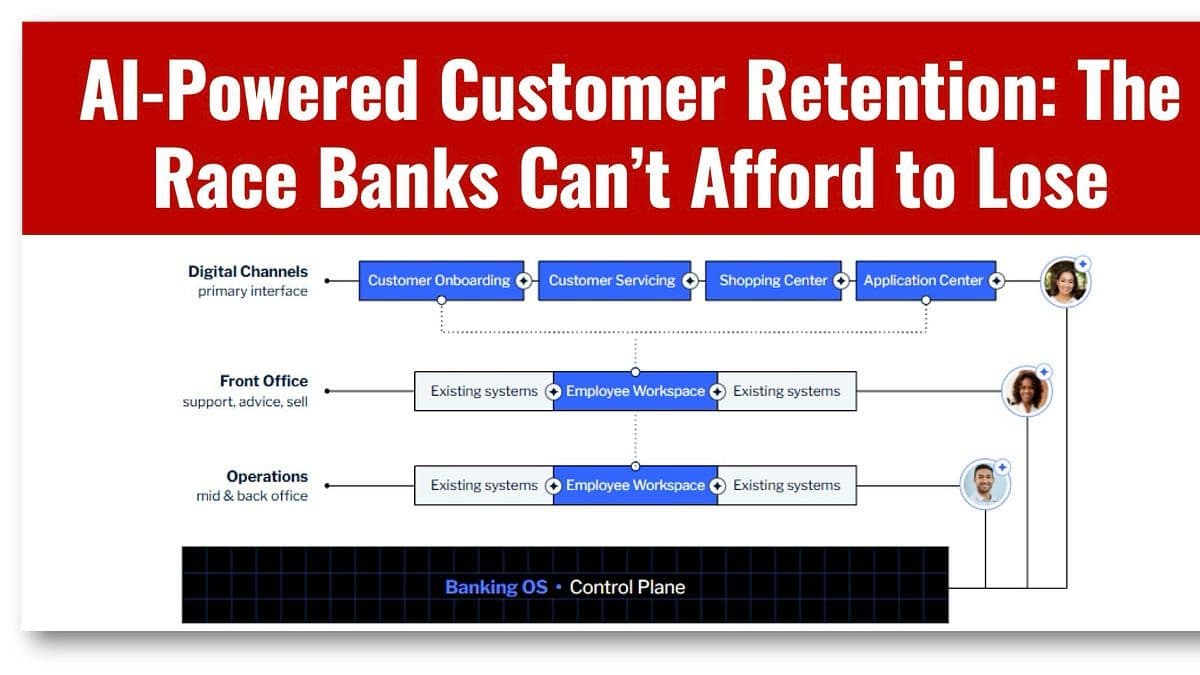

Banking OS Is the Sole Viable AI Path

Banks have three options for AI on legacy systems. Only one works. ↳ Do nothing — bolt AI onto fragmented systems. Limited data access. Innovation theater. Not a retention strategy ↳ Full cloud rip-and-replace — 94% of banking modernization projects exceed deadlines....

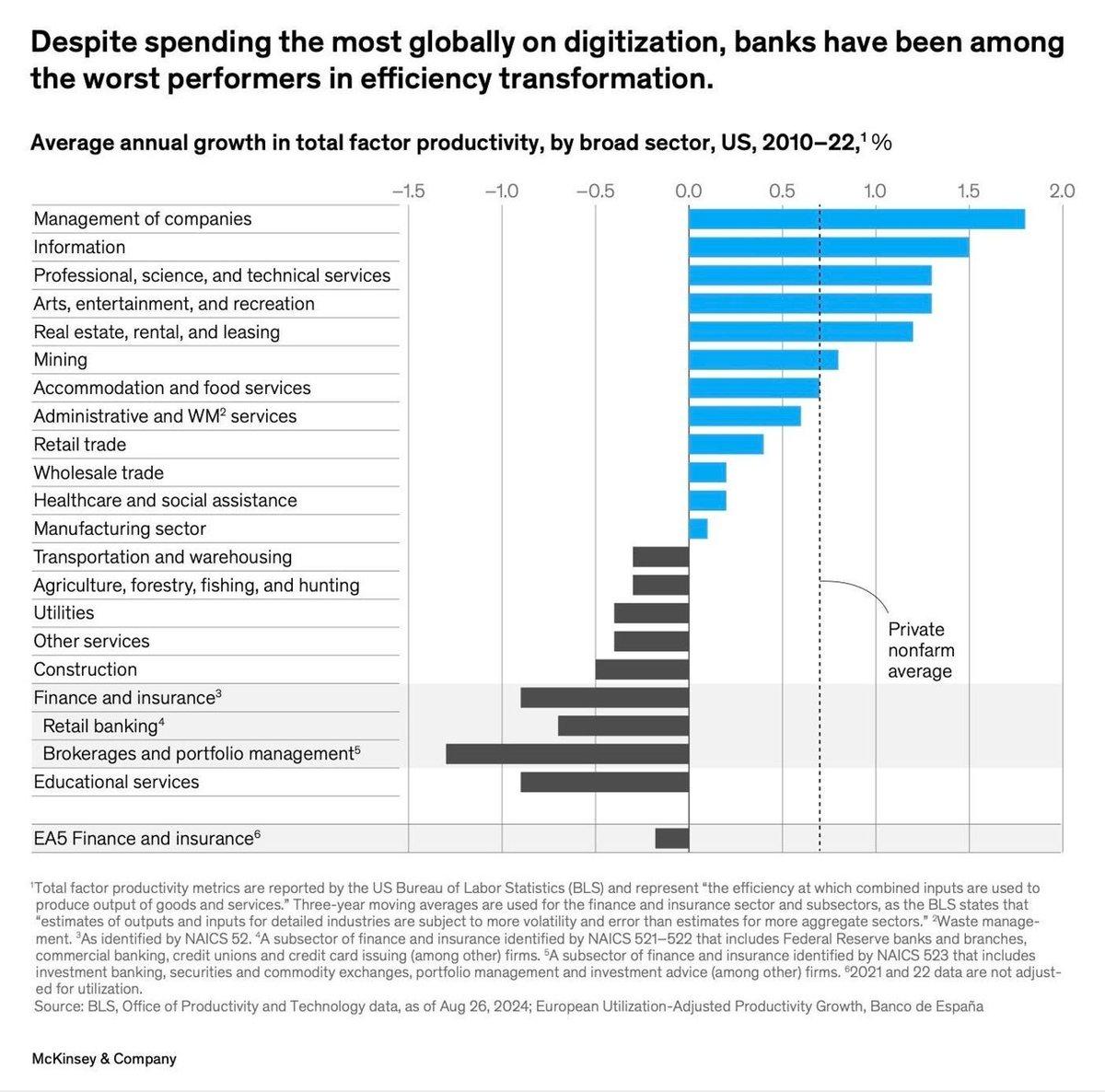

Banks Spend Big on Digital, See Tiny Productivity Gains

Banks are under siege from every direction this week. Neobanks are stealing customers, AI budgets are growing while returns disappoint, and McKinsey delivers a brutal verdict in the Chart of the Day: banks spent more on digitization than almost any...

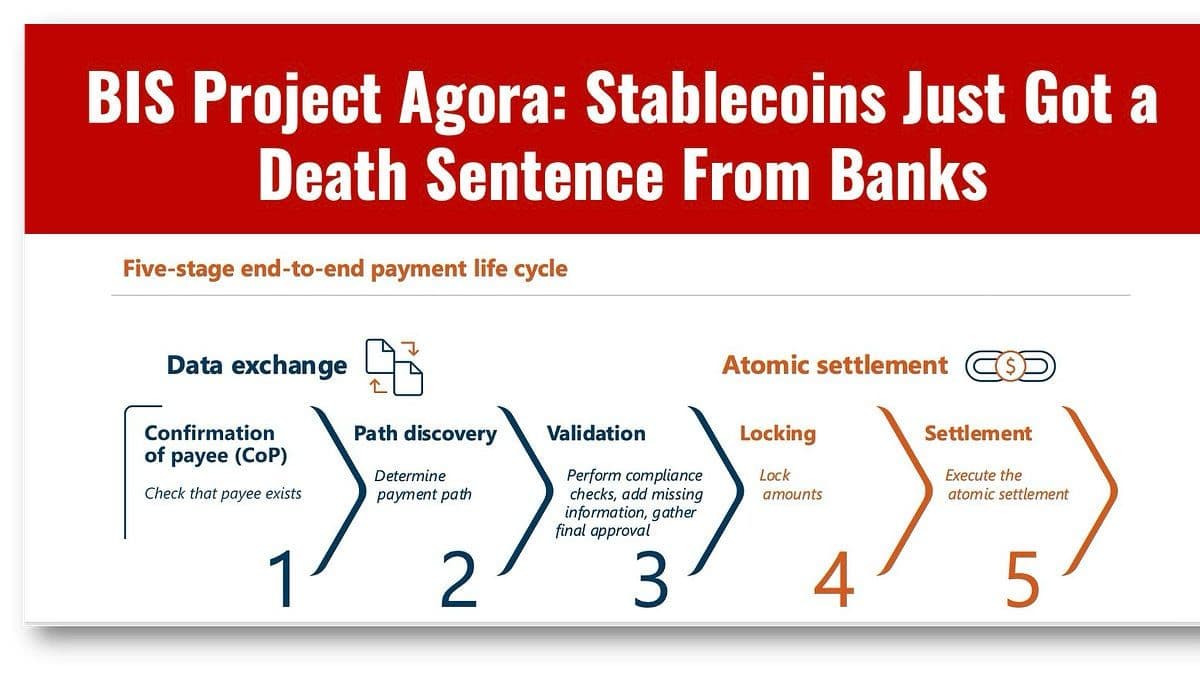

Agora: West’s Sanction‑embedded Counter to China’s mBridge

The BIS's Project Agora has a geopolitical dimension that nobody in the stablecoin or digital currency world is discussing. It is the West's direct counter to China's mBridge. mBridge: routes around the dollar, bypasses SWIFT, allows direct settlement between participating central banks...

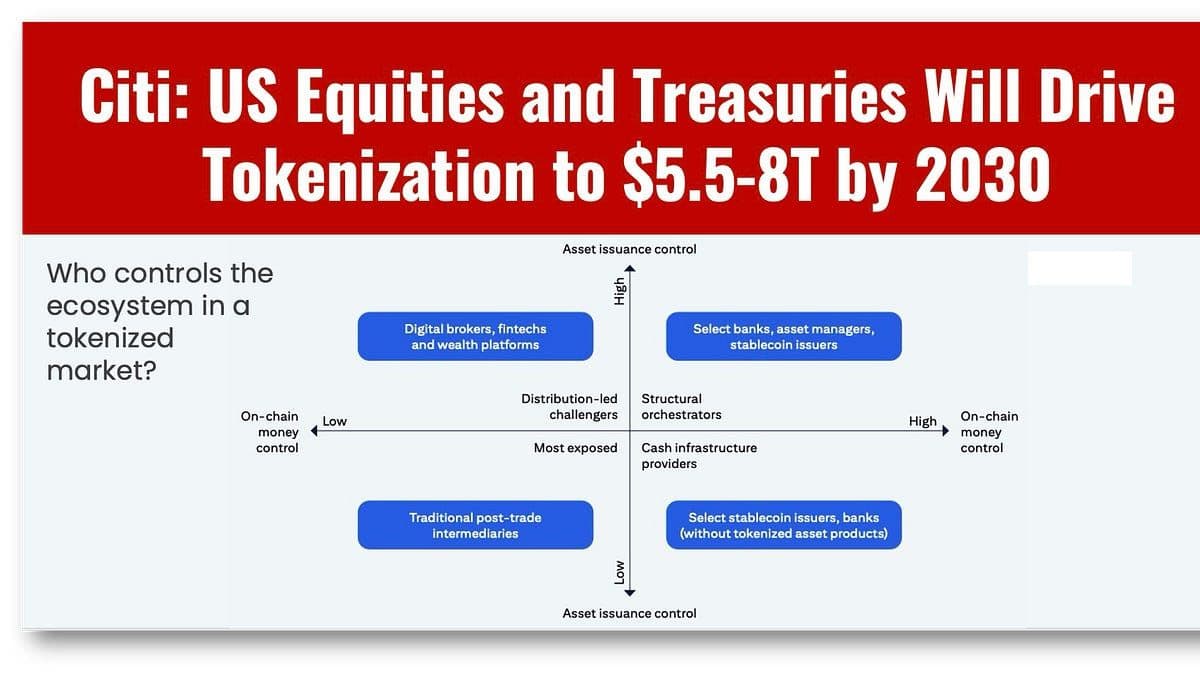

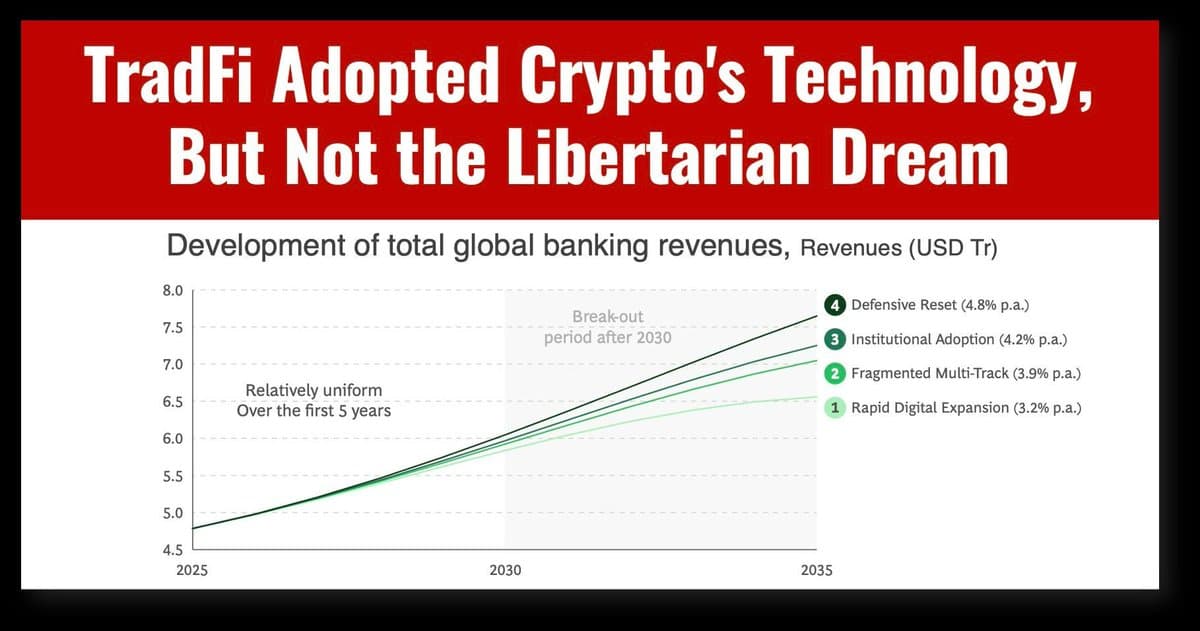

Institutional Tokenized Deposits Replace Libertarian Crypto Dream

The libertarian dream is dead. Here are the four futures that replaced it. 1️⃣ Private-led expansion — stablecoins win, banks lose 30% of profits by 2035 2️⃣ Fragmented multi-track — everyone builds, nobody connects, liquidity pockets not markets 3️⃣ Institutional digital evolution —...

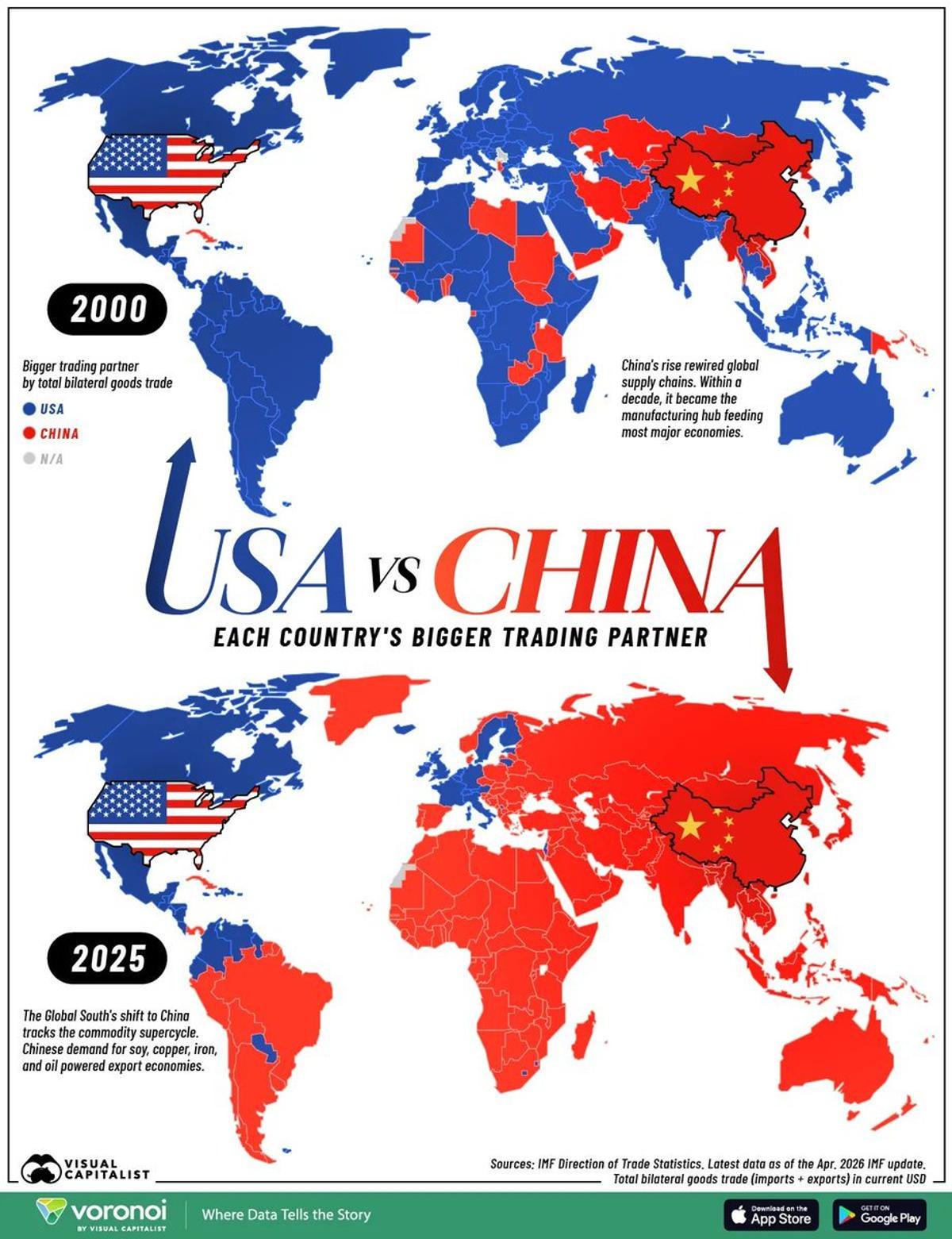

US Neglect Ceded Global Trade Dominance to China

China didn't steal global trade dominance. The US handed it over. What happened between 2000 and 2025 was not a military victory or a political coup but the symptom of decline. It was WTO membership, manufacturing scale, commodity demand, and infrastructure investment...

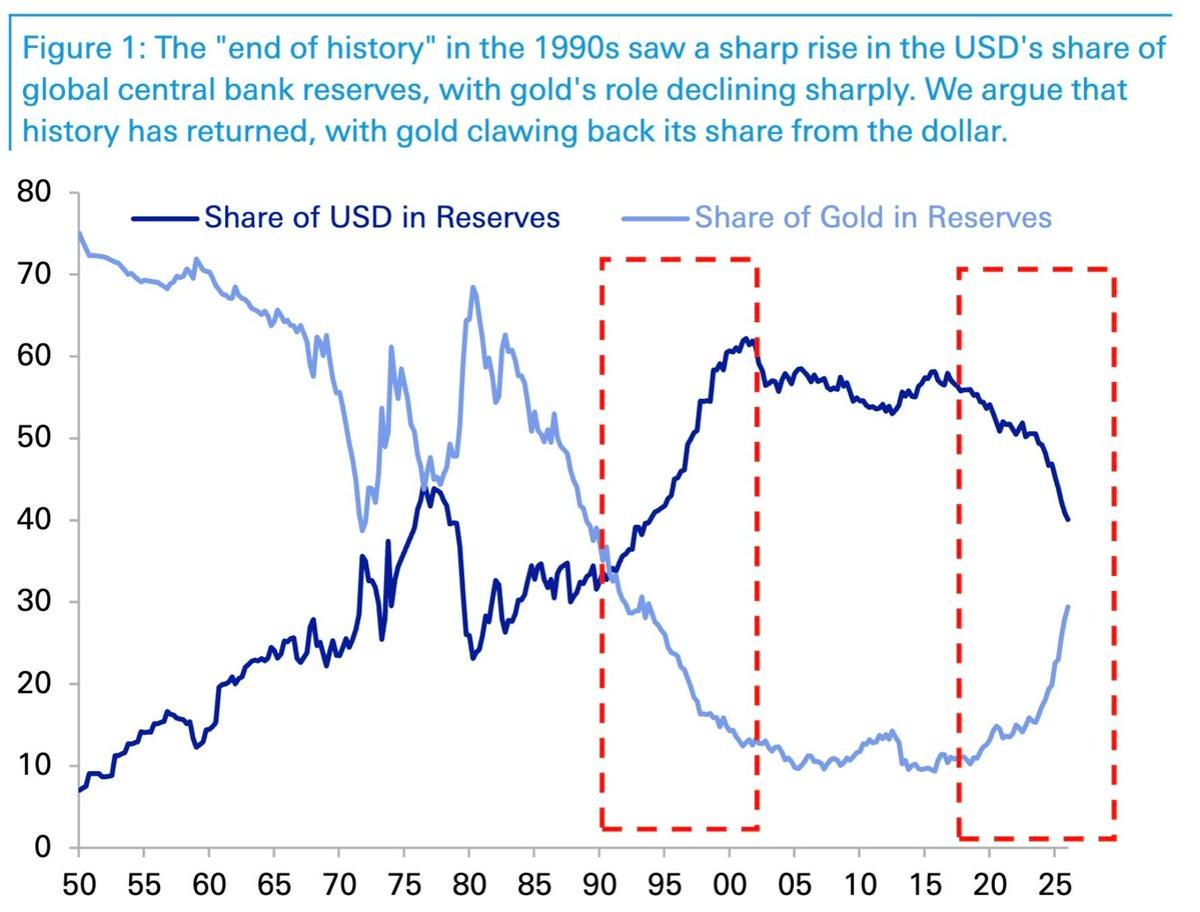

Central Banks Swap Dollar Reserves for Gold Surge

🧵#DEDOLLARIZATION DAILY: History is back, it brought gold, and the dollar is losing. The dollar isn't losing reserve dominance to the euro, yuan, or yen. It's losing to a metal. Deutsche Bank's research is unambiguous: ↳ Dollar share of global central bank reserves:...

Alibaba's Qwen AI Powers End‑to‑End Shopping on Taobao

Alibaba's Qianwen (Qwen) Fully Integrated with Taobao: AI Shopping Covers Full Loop from Discovery to After-Sales Used both the Qwen standalone version and the version built into Taobao, aka Alibaba e-commerce. The Taobao version is more complete as it can...

China Prioritizes AI Deployment, US Chases AGI Myth

Why China is Winning the Race: US chasing AGI myth while China builds the AI future US betting AI future on a goal no one can define, while China prioritizes mass deployment over big bang discovery "The real danger for...

China's AI Agents Foreshadow Commerce via Built-In Delegation

What China’s AI Agents Reveal About the Future of Commerce China matters not because it has the best models, but because the infrastructure for delegated action is already deeply embedded in everyday life. #China #techwar #chips #tech @baoshaoshan @thecyrusjanssen @DOualaalou @lajohnstondr @PSTAsiatech https://t.co/CbmPUYIkbp

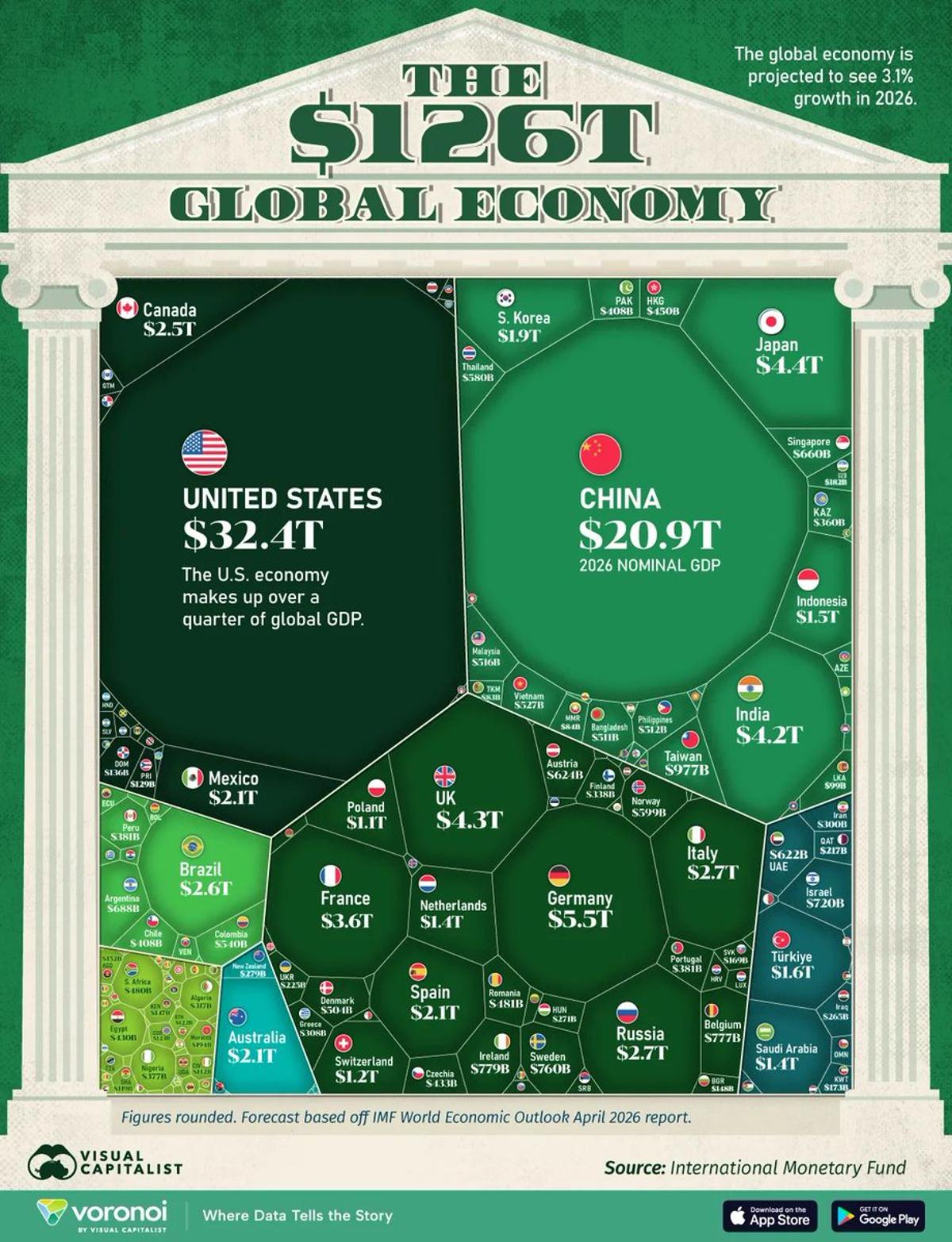

Asia Now Drives Global Economy, Outpacing West

The Shifting Balance of Power Towards Asia Asia isn't catching up to the global economy. It's running it. The $126T global economy chart just dropped — and the story isn't America's $30.6T. It's this: ↳ China: 4.4% growth — fastest of the...

US Chip Ban Fuels China’s Homegrown AI GPU Surge

The US export ban on Nvidia chips to China didn't slow China's AI one bit; it is building it. Jensen Huang just confirmed what anyone watching Asia already knew: Nvidia's China market share is now 0%. Gone. How exactly the US...

Chinese Banks Stuck Between US Sanctions and Beijing Orders

US Sanctions Just Hit a Whole New Level: China's No-Win Crossfire Trap China’s banks are now caught in the sanctions crossfire. Beijing just activated its blocking law & ordered firms to defy US sanctions on its refiners. Comply with US sanctions? Chinese courts...