The Money Cruncher

Personal finance creator who critically evaluates “fintech banks,” account safety, FDIC/program bank structures, and risk.

Investing Beats Saving: $357k Extra by 65

John saved $200/mo from 25 to 65 in a savings account getting ~3%. At 65, he has ~$190k. Bob invested $200/mo from 25 to 65 getting ~7.25%/yr on average. At 65, he has $548k. $357k difference between saving vs investing. If you want to build wealth, you have to invest for the long term

Sell High‑Basis Shares, Gift Low‑Basis for Tax‑Free Inheritance

Bob has a $5M brokerage account which he will pass down to his 2 kids A smart tax move for him is to sell the right lots It's best to sell stocks with high cost basis (= low capital gains tax) to...

Invest in Few ETFs, Stay Long‑term, Use Tax‑advantaged Accounts

5 principles to follow to become a successful investor: > no individual stocks, 1-2 ETFs only > stay invested regardless of media clickbait > have a long term mindset > invest consistently > prioritize tax advantageous accounts Anything you would add?

Pick Roth if Future Taxes Exceed Today’s Rate

Roth vs Traditional 401k is all about taxes. Say you are in a 32% marginal tax rate and you put $20k in Trad 401k. It doubles to $40k, which is $27.2k after taxes Same example, but contribute $13.6k to Roth (after 32%...

Five Tax‑Smart Accounts to Grow Your Child’s Wealth

5 ways to build wealth for your kid: 1. 529 plan. Get tax deduction for contributing in many states. Grows tax free and withdrawals are tax free for education. 2. UTMA account. Taxable account that child owns. Reduces financial aid. 3. Trump account....

Reevaluate Roth vs Traditional 401(k) After Income Shifts

You need to adjust Roth vs Traditional 401k based on life changes. Say you were doing Roth, but your company promoted you fast, or your spouse started a job, or you got a side hustle. You should adjust and analyze Roth vs...

Build Wealth: Cut Costs, Max Match, Invest Consistently

How to get to the 1% financially: > analyze expenses and cut useless junk > contribute to 401k up to the match > pay off any high interest debt (7%+) > max out Roth IRA > buy low fee, quality ETFs > scale investments to...

Investors Pay Lower Taxes Than Wage Earners

The tax code loves investors. If you work a W-2 job, the max federal tax rate you can pay is 37%. But qualified dividends or long term capital gains are taxed at up to 23.8%. Real estate investors also enjoy tax arbitrage...

Keep a 1.99% Mortgage—Inflation Beats Early Payoff

My coworker has a 1.99% mortgage. That is something you should NEVER pay off early. Inflation is at least 3%/yr. Why would anyone pay that off aggressively? It makes absolutely 0 sense.

Pay Off Credit Card Debt Before Stock Investing

Don't invest your money in the stock market if you have credit card debt Unless to get the full employer match for your 401k (assuming good % matching and vesting rules) Get rid of that 25% interest asap Don’t work backwards

Big Gains Often Follow Market Crashes Within Weeks

7/10 BEST days in the stock market happened within 2 weeks of 10 WORST days. For example, worst day in 2020 (March 12) was immediately followed by best day of the year. This is also what we just saw in the current...

Know Your 401k Vesting Schedule Before You Quit

If you have a 401k, you need to understand vesting rules. It means how long you need to be employed to receive your employer’s match (your money is always yours) Common vesting schedule is ~33% per year for 3 years Check your vesting...

Tax Refunds Lose Value—Adjust Your W‑4

Zohran Mamdani released a copy of his tax return to reporters. His 2025 tax refund was $7,011... That means he earned 0% interest on it. He could've invested it throughout the year or earned ~$200 from HYSA. Tax refund isn’t free money. Adjust...

Don't Let Pre‑Approval Push You Into $50k Debt

Just because you're pre-approved for a $50k car loan doesn't mean you actually have to buy a $50k car. There are plenty of slightly used cars you can buy for $25k that will last for years with low mileage. Don't bury yourself...

Invest Your Salary, Retire Early with Passive Gains

Last year, my portfolio made me more money than my old job at Deloitte. I worked 55 billable hours during busy season vs just buying ETFs like $VTI and waiting for the same $$$ gain Turn your active income into investments so...

One in Four Workers Lose Free 401k Match

Shocking stat: 1 in 4 workers miss out on the full 401k match by not contributing enough. That’s literally free money lost forever. Sign up for the full match and figure out how to live on the rest

Higher Bracket only Taxes Income Within that Range

I know someone who declined a promo because he thought the increase would push him into a higher tax bracket and make all his income taxed at that rate. In reality, only the income within the new tax bracket is taxed...

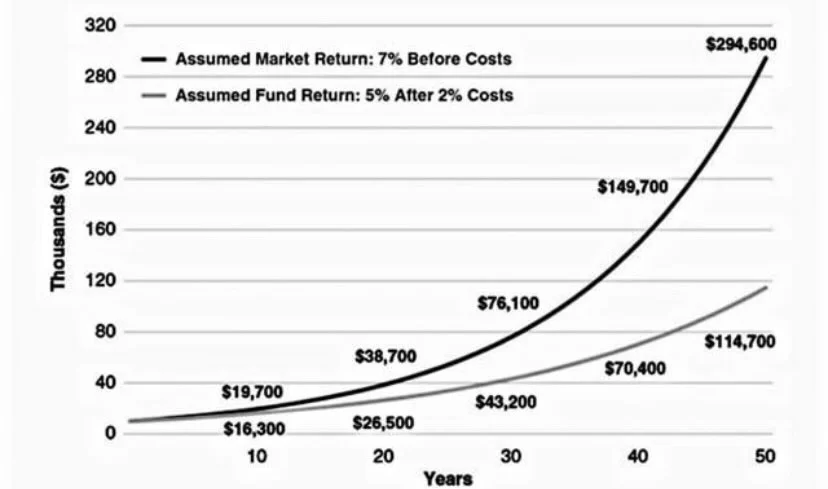

Small Fees Turn $10k Into $180k Difference

This chart shows the growth of $10k over 50 years with a 7% return vs a 7% return minus a 2% fee (high AUM, fees, etc) Difference is ~$180k on just $10k initial investment Please pay attention to fees

Withdraw Up to $65K Gains Tax‑Free

You can pay 0% in taxes on your investments: 0% long term capital gains rate applies if your taxable income is <= $49,450 (single) or $98,900 (mfj) After standard deduction, you can withdraw $65,550 (single) or $131,100 (mfj) of LT gains from...

Invest, Don't Just Save; Cash Loses to Markets

Growth of $10,000 since April 2016: High yield savings account: $12,534 $VGT (IT ETF): $74,973 $VOO (S&P 500): $39,064 Keeping cash long term is not a good strategy (aside from emergency funds) You can't save your way to wealth, you have to invest.

2026 Tax Bill Lets Charitable Donations Yield Deductions

Most people donate to charity and get $0 of tax benefit. In 2026, that finally changes because of the new tax bill. Here’s how to take advantage:

Maximize HSA Growth: Invest All, Reimburse Later

I have $500 in cash in my HSA (my plan’s minimum). The rest is invested in the S&P 500. I’m tracking all my medical expenses and plan to reimburse myself in 20 years. This is how you use HSA to its...

2026 Charitable Deductions Available With Standard Deduction

IMPORTANT: in 2026, you can deduct charitable donations even if you take a standard deduction (up to $1,000 for single, or $2,000 married) Please track all your cash donations in 2026. They could help save on taxes (whereas you had to...

Unlock Early 401k Access for Tax‑Free Retirement

Many finance influencers say "get your 401k match, then invest in a brokerage" Main argument is that you can retire early with brokerage I disagree because you can access your 401k early with 72t SoSEPP, or Rule of 55. If you're a high...

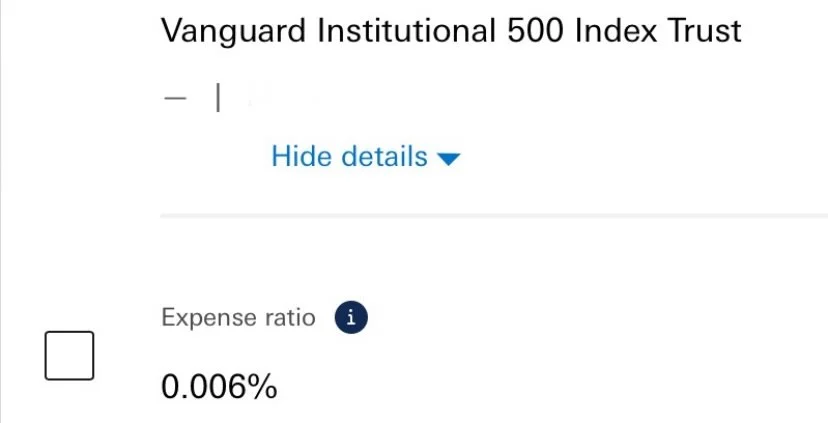

Ultra‑low‑fee Vanguard S&P 500 Proves 401k Value

My 401k plan has a Vanguard S&P 500 fund with a 0.006% expense ratio. It’s one of the lowest S&P 500 fee funds available in a 401k plans 401k is not a scam

Low Fees Drive Better Returns: Why I Choose Vanguard

Many people ask why I love Vanguard funds: It's because they are cheap. Vanguard reduced expense ratios more than 2,000 times for their funds. Terrible charts, outdated app, but I don't care about that. I care about performance (low fees = better returns)

Keep Mortgage, Let Investments Outperform Costs

"I have a $190k mortgage at 3.25%. I also have $25k in savings and $175k in stocks. Should I pay off my mortgage?" I wouldn't. You'd owe capital gains tax, lose protection against inflation, potential tax benefits, and the opportunity cost is...

Proper Asset Location Adds 0.30% After‑Tax Return

Vanguard's research showed that you could add 0.30% of annual after-tax returns simply by having a correct asset location strategy: - avoid bonds in brokerage. Keep them in retirement accounts - growth assets in Roth - efficient ETFs in brokerage - avoid REITs in...

Simple Steps to Build Strong Credit Quickly

Building your credit is not hard. Do this: - pay off your credit cards on time, every month - keep credit utilization low by requesting increased credit limits every 6-12 months - keep old accounts open, even if you don’t use the credit cards -...

Prioritize Savings: Emergency Fund, Match, Debt, Then Investing

"I don't know how to prioritize my money" Here’s a good rule of thumb: 1. Build emergency fund (3-6m) 2. Sign up for the 401k/403b match 3. Pay off high interest debt (7.25%+) 4. ESPP (if applies) 5. HSA (if eligible) 6. Roth IRA 7. Max out 401k/403b 8....

Markets Rebound Every Crash—Stay Focused Long Term

The stock market went down: • 49% in 2000 • 55% in 2008 • 35% in 2020 • 27% in 2022 • 23% in 2025 But it recovered every single time so far. There will always be short term volatility. That’s totally normal and healthy. Focus on...

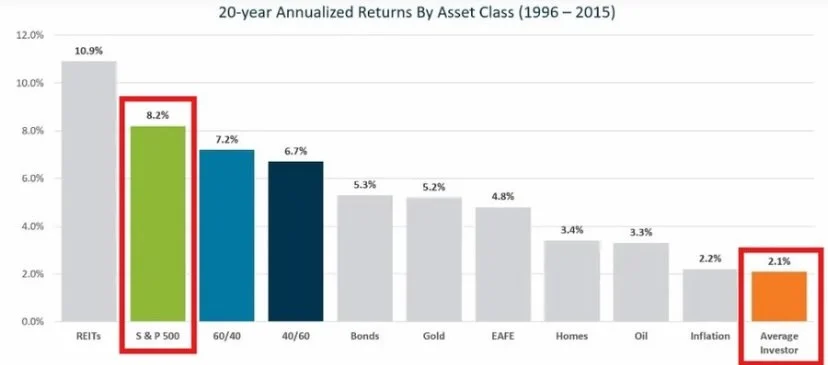

Average Investors Lag S&P; Index Funds Win

The average investor made 2.1%/yr in 1996-2015 vs 8.2%/yr for the S&P 500. This is exactly why many investors should just invest in index funds and chill. Stop gambling in individual stocks. Stop options trading. Start investing.

Double $1k in UTMA, Harvest Gains Tax-Free

Open a UTMA account for your child. Contribute $1k. Once that $1k turns into $2k, do tax gain harvesting (sell, rebuy). Kiddie tax will not apply since the gain is $1k (less than child's standard deduction) Good way to increase cost basis...

Choose the Right 401(k) Move After Leaving Job

If you quit your job, you have 3 choices for your 401k: 1. Leave as is. Good if you have low fees. 2. Rollover to IRA. Good if your 401k has high fees, but impacts Backdoor Roth. No ERISA protection. 3....

Use Credit Card, Reimburse Later: Maximize HSA Gains

I never activated my HSA debit card and you shouldn’t either Pay all medical expenses with a credit card, then reimburse yourself from HSA via direct transfer to your bank. Bonus strategy: reimburse yourself in 20+ years (keep documentation) and invest HSA...

Simple, Consistent Investing Beats Spending for Millionaire Goal

I will become a millionaire before 30 by doing basic things: - don’t spend money on stupid stuff - max 401k, put it in S&P 500 fund - max Roth IRA - max HSA, invest it - every 2 weeks put money in brokerage invested...

Stay Calm, Keep Buying: Long-Term Wins Over Volatility

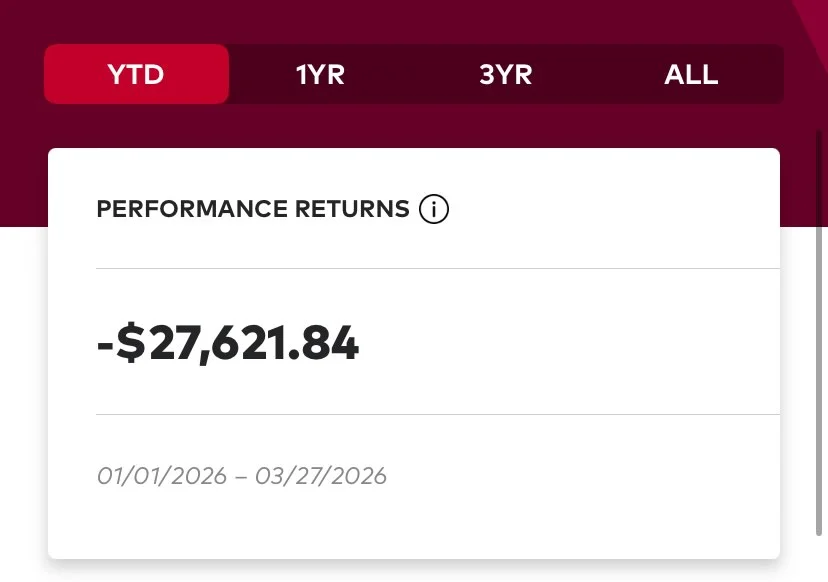

My brokerage account is down $27k YTD. More if you count 401k, HSA, etc But I’m not worried at all. I’ll continue buying as I always do. Thinking long term is how you win, despite short term volatility.

401(k) Isn’t a Scam—Early Withdrawals Are Possible

"401(k) is a scam because you can't retire early" People who say this don’t know about Rule of 55, Section 72(t) SoSEPP, or Roth Conversions. There are ways to access 401k before 59½. You also likely will live past 59 anyways.. Use tax...

Spend 10 Minutes Daily, Manage Money Like a Pro

It’s wild how most people spend 2,080 hours/yr working to earn money, but almost 0 hours managing that money… It takes 10-20 minutes per day to learn: - budgeting - investing - optimizing your finances The earlier you start, the better off you'll be in...

Stop Leaving Roth IRA Cash Idle—Invest for Growth

$70k of cash sitting in a Roth IRA… That’s 10 years of contributions getting only 2-4%/yr from MMF Instead of ~10%/yr from S&P 500 in that timeframe Just a reminder: your Roth IRA contributions need to actually be invested.

Consistently Beating the S&P? Just Buy the Market

Beating the S&P 500 isn't difficult. But beating the S&P 500 consistently, over the long term, is very very difficult. Many people overestimate their ability to pick good stocks over the long term. They eventually realize that it’s a losing game. That's why...

Save 15% Early, Secure Retirement by 65

If you want to retire at 65, you have to save at least 15% of your salary (including 401k match) starting at 25. Use that money to: 1. Get full employer's 401k match 2. ESPP (if applicable) 3. HSA (if eligible) 4. Roth IRA 5. Finish...

Tiny Fee Differences Compound Into Massive Portfolio Losses

1% investment fee per year will lower your portfolio by ~25.8% over 30 years. 0.10% investment fee per year will lower it by only ~3% over 30 years. That 22.8 percentage point difference could cost you $$$. Fees also compound. Pay attention.

Step‑up in Basis Can Erase Capital Gains Tax

If you bought a home for $500k and it is now worth $1M when you pass away, your children generally receive a “step up in basis.” If they sell it, they may owe no capital gains tax. But if you gift...

Invest Early, Retire Richer: 10 Years Beats 25

This is crazy: If you are 35 and start investing $5k/yr and stop at 60, you will have ~$431,754 (8%/yr assumption) But if you are 25, start investing $5k/yr and stop at 35, you will have ~$615,580 at 60 (8%/yr assumption) $75k less...

Markets Crash Hard; Stick to Strategy and Keep Cash

During Dot Com crash (2000-2002) the S&P 500 dropped ~49%. During Financial Crisis (2007-2009) market dropped ~57%. During 1973-1974 bear market, it dropped 48%. We don’t just go up all the time. During bad times, you have to stick to your job &...

Contribute Pre‑tax in High‑tax State, Retire Tax‑free Elsewhere

An easy tax arbitrage many people don't think about: Do a pre-tax 401(k) in a state with a high income tax vs withdrawing in a 0% tax state. Example - contribute pre-tax in CA/NY (say 10% marginal) but retire in 0% state,...

Step‑up Basis Wipes Out Taxes on Inherited Gains

Step up in basis is one of the most powerful tax provisions and can wipe out a lot of taxes. Say your dad bought $200k of stocks in a brokerage account that are now worth $2M. He passes them down to you...

Investing Made Simple: Open Roth IRA in Minutes

It’s never been easier to invest. You can literally open a Roth IRA in under 5 minutes, contribute $100, and buy fractional shares of ETFs with ZERO fees. Or sign up for your 401k and contribute 3% or 5% or 10% of...

Automate Small Paycheck Investments for Long-Term Growth

Every time you get paid, take a specific amount ($10, $20, $100, etc) and invest it. Don't know what to buy? Start with simple index funds, like VOO or VTI. Ideally, you should invest before your paycheck even hits (e.g 401k) Automate the...