Emerging-Market Stocks Eye Correction, Currencies Erase YTD Gain

•March 9, 2026

0

Why It Matters

The correction signals heightened risk for investors exposed to emerging economies, while the currency reversal underscores how geopolitical shocks can quickly erode recent market advances.

Key Takeaways

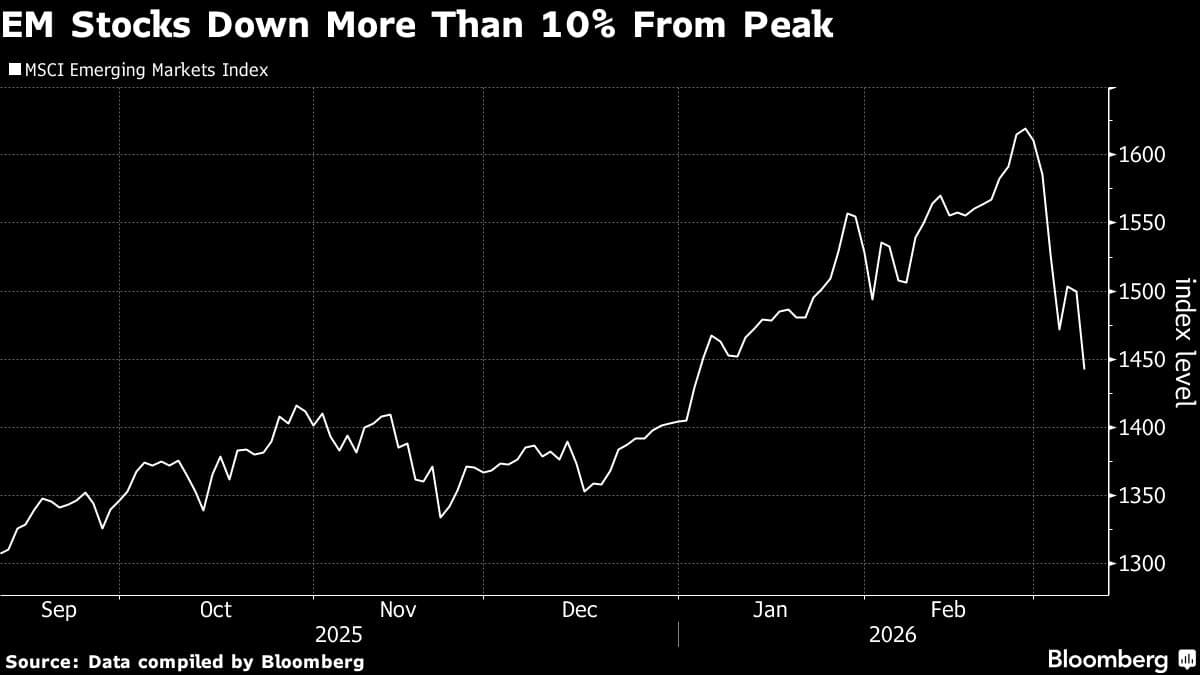

- •MSCI EM down 3.4%, nearing 10% correction

- •Two‑thirds of constituents posting losses today

- •Largest monthly decline since September 2022

- •YTD gain fell from 15% to just over 3%

- •Emerging‑market currencies erased all year‑to‑date gains

Pulse Analysis

The recent plunge in the MSCI Emerging Markets Index reflects a classic technical correction, where a 10% pullback from recent peaks triggers algorithmic sell‑offs and risk‑averse repositioning. With the index down 3.4% in early London trading, the breadth of weakness is evident—about 66% of the stocks are in the red, a pattern that historically precedes broader market consolidation. This correction is the steepest monthly loss since the post‑pandemic sell‑off of September 2022, highlighting the fragility of the rally that had propelled the index to a 15% year‑to‑date gain just weeks earlier.

Compounding the market’s technical stress is the escalating conflict involving Iran, which has reignited fears of supply‑chain disruptions, energy price spikes, and capital flight from vulnerable economies. Emerging‑market currencies, which had previously benefited from a weaker dollar and robust commodity demand, have now erased all of their YTD gains as investors scramble for safe‑haven assets. The war’s ripple effects threaten debt‑servicing capacities in countries heavily reliant on external financing, potentially prompting sovereign defaults or currency devaluations.

For investors, the twin pressures of a technical equity correction and geopolitical volatility call for a reassessment of exposure. Diversification into higher‑quality emerging‑market issuers, hedging currency risk, and tightening stop‑loss thresholds can mitigate downside. Meanwhile, selective opportunities may arise in sectors insulated from geopolitical shocks, such as technology firms with strong balance sheets or consumer staples in stable jurisdictions. Navigating this environment demands disciplined risk management and a keen eye on evolving geopolitical developments.

Emerging-Market Stocks Eye Correction, Currencies Erase YTD Gain

0

Comments

Want to join the conversation?

Loading comments...