Kazakh Manufacturing Hit by Marked Fall and Elevated Inflationary Pressures in February, PMI Shows

•March 3, 2026

0

Companies Mentioned

Why It Matters

The contraction signals slowing activity in a key economic driver, potentially dampening GDP growth, while rising confidence hints at forthcoming investment and recovery.

Key Takeaways

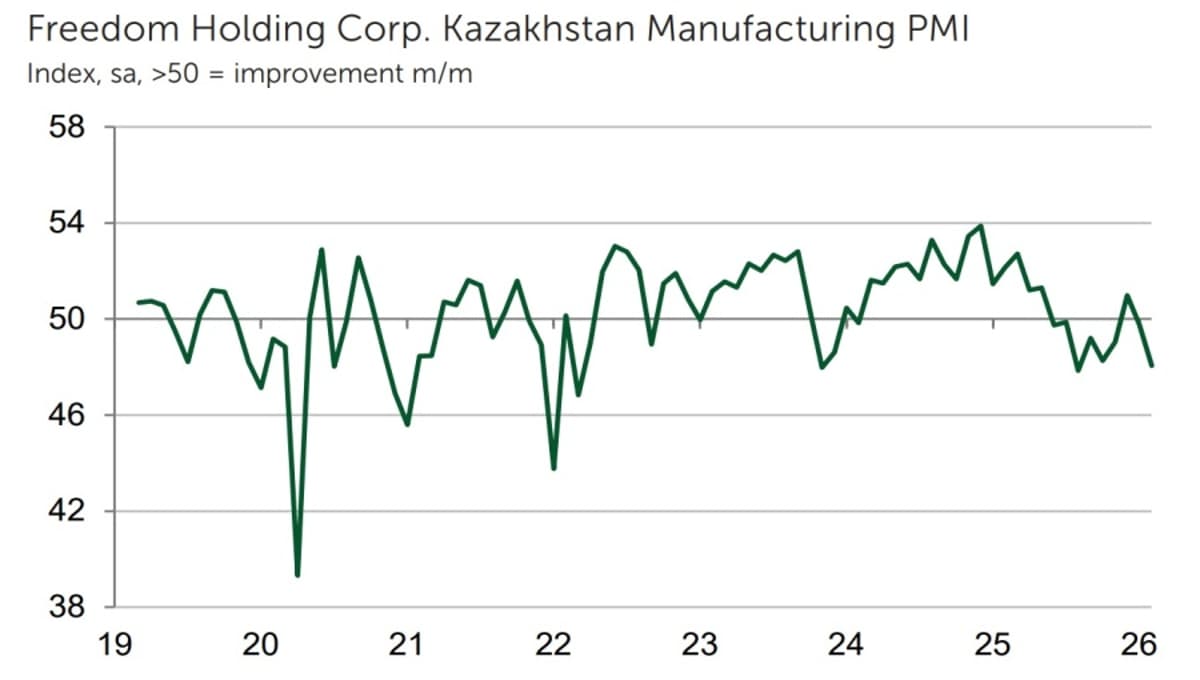

- •PMI fell to 48.1, confirming manufacturing contraction.

- •New orders and output prices rose after VAT hike.

- •Firms cut employment, purchases, and inventory levels.

- •Business confidence reached highest level since October.

- •Optimism hinges on planned investments and advertising campaigns.

Pulse Analysis

The February PMI reading of 48.1 places Kazakhstan’s manufacturing sector firmly in contraction territory, underscoring a slowdown that follows a modest decline in January. The drop is tied to weaker domestic demand and the fiscal impact of a 1 % VAT increase implemented in January, which pushed input costs and output prices higher. While inflationary pressure remains elevated, the rate of price growth has softened compared with early‑year spikes, suggesting that firms are beginning to absorb the tax shock rather than pass it fully onto customers.

Manufacturers responded to the tightening environment by trimming headcount, scaling back purchases, and reducing inventory buffers. These cost‑containment measures are typical of firms bracing for prolonged uncertainty, and they help preserve operating margins amid lingering price volatility. However, the simultaneous decline in staffing and stock levels can strain supply chain resilience, especially for export‑oriented producers that rely on steady output. Compared with peers in the CIS region, Kazakhstan’s contraction is deeper, reflecting both the tax burden and a slower rebound in consumer confidence.

Despite the downturn, business confidence rose to its highest level since October, driven by expectations of upcoming investment projects and aggressive advertising campaigns slated for the second half of the year. Analysts see this optimism as a signal that firms view the current dip as a temporary correction rather than a structural shift. Policy makers may need to balance further tax adjustments with incentives that encourage capital spending to sustain the manufacturing revival. If demand picks up and price pressures ease, the sector could return to growth by late 2026.

Kazakh manufacturing hit by marked fall and elevated inflationary pressures in February, PMI shows

0

Comments

Want to join the conversation?

Loading comments...