Simply Unaffordable! FHA Lower Credit Score Borrowers (0-619) Suffer Escalating Mortgage Delinquency Rates

Key Takeaways

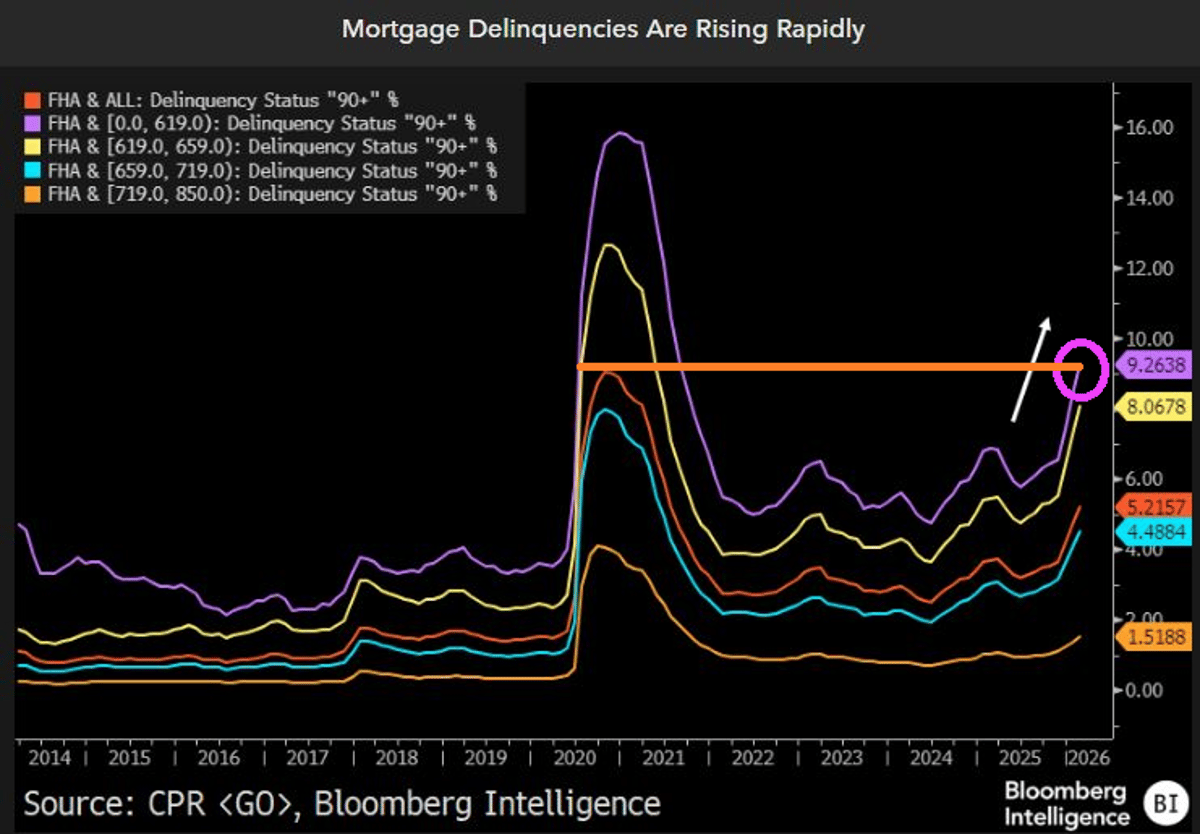

- •Delinquency rates for 0‑619 credit scores surged 2023‑2025.

- •FHA portfolio now exceeds historic delinquency benchmarks.

- •Home price inflation outpaces wage growth, tightening affordability.

- •Federal stimulus amplified demand, inflating mortgage balances.

- •Policy risk: tighter underwriting may curb future defaults.

Pulse Analysis

The recent uptick in 90‑plus‑day delinquencies among FHA borrowers with sub‑620 credit scores reflects a broader affordability crisis that began with the pandemic‑era fiscal response. Massive government spending injected liquidity into the housing market, driving home prices up faster than wages. As a result, many low‑income families stretched beyond their means to secure mortgages, often relying on the FHA’s more lenient credit standards. This mismatch between debt service capacity and loan balances is now manifesting as higher default rates.

From a systemic perspective, the FHA’s insurance fund faces heightened exposure. Historically, the program has absorbed higher risk to promote homeownership, but the current delinquency trajectory exceeds previous peaks, signaling potential strain on the fund’s reserves. If unchecked, increased claim payouts could necessitate higher premiums for lenders or direct federal subsidies, both of which would ripple through mortgage pricing and lender profitability. Moreover, the concentration of risk among the lowest‑credit segment amplifies vulnerability to macroeconomic shocks, such as rising interest rates or a slowdown in employment.

Policymakers and mortgage insurers are thus at a crossroads. Tightening underwriting criteria could mitigate future losses but may also restrict access for first‑time buyers who depend on FHA financing. Alternative solutions include targeted assistance programs that address income gaps, or revisiting the loan‑to‑value ratios for high‑risk borrowers. Understanding the interplay between fiscal stimulus, housing price dynamics, and credit risk is essential for crafting balanced interventions that preserve both market stability and the FHA’s mission of expanding affordable homeownership.

Simply Unaffordable! FHA Lower Credit Score Borrowers (0-619) Suffer Escalating Mortgage Delinquency Rates

Comments

Want to join the conversation?