Mortgage Applications Retreats Further in April

Why It Matters

The slowdown signals reduced refinancing demand as higher rates curb borrower incentives, potentially tightening mortgage‑backed securities pipelines. Lenders and investors must adjust pricing and inventory strategies amid shifting borrower behavior.

Key Takeaways

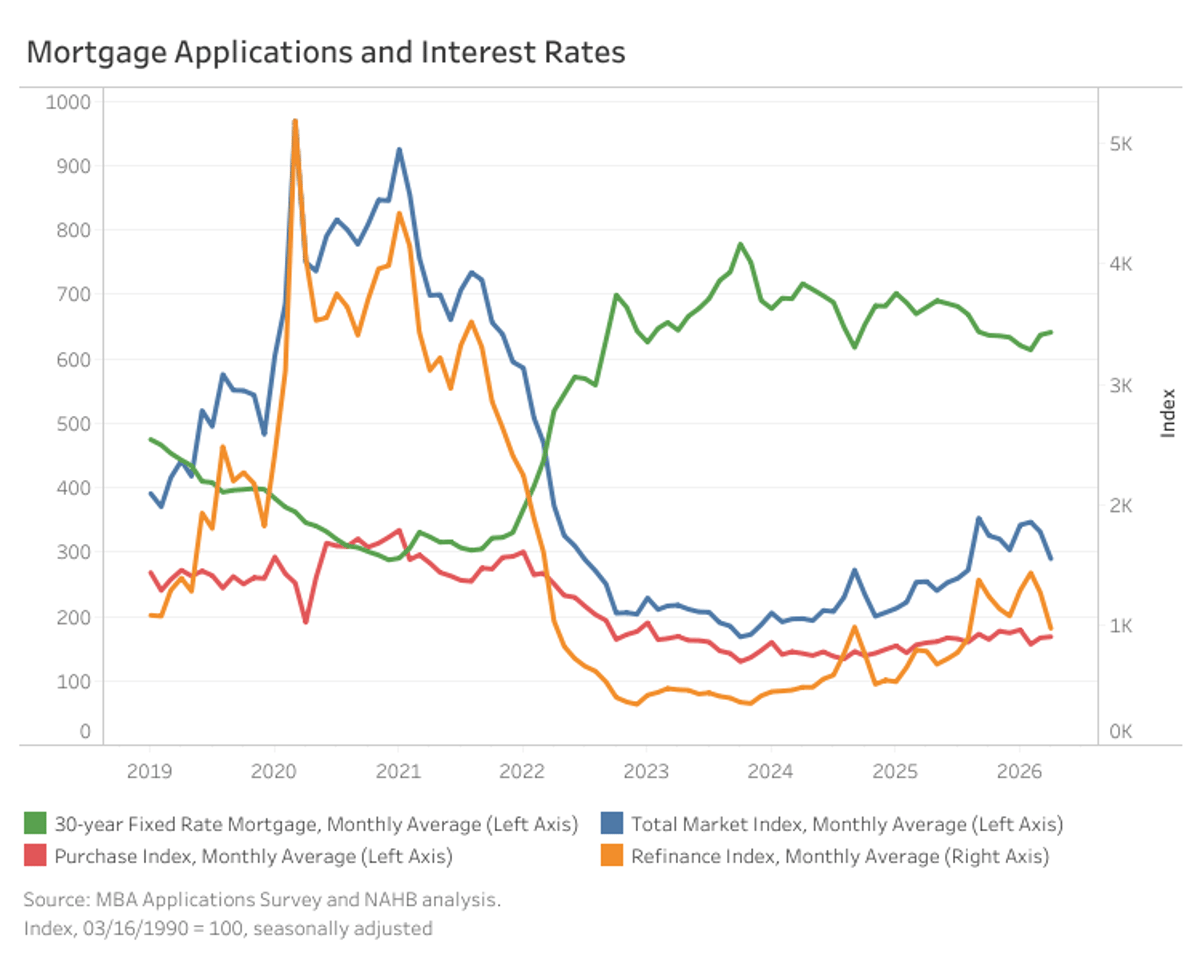

- •MBA index fell 12.4% MoM, but up 14.2% YoY.

- •30‑year fixed rate rose to 6.41%, still 0.39% below last year.

- •Refinance applications dropped 23.5% MoM, purchase apps unchanged.

- •Average loan size slipped to $397,800, refinance loans fell 7.1%.

- •ARM share held steady at 8.3% of total applications.

Pulse Analysis

April’s dip in mortgage applications underscores the sensitivity of borrower behavior to rate movements. The 30‑year fixed‑rate benchmark nudged higher to 6.41% after a modest four‑basis‑point increase, yet it remains well below the peak levels seen a year ago. This environment dampened refinance activity, which fell 23.5% from March, while purchase demand stayed flat. The overall loan‑size average slipped to $397,800, reflecting tighter borrowing capacity, especially among refinancers whose average loan size dropped 7.1%.

For lenders and mortgage‑backed securities (MBS) investors, the shift signals a tightening pipeline. Reduced refinance volume curtails the flow of high‑quality, low‑risk loans that traditionally underpin MBS performance, prompting issuers to reassess pricing models and hedging strategies. At the same time, the steady share of adjustable‑rate mortgages (8.3%) suggests that borrowers are still exploring rate‑risk mitigation, albeit without a significant shift in product mix. Lenders may need to recalibrate underwriting standards and inventory allocations to balance the lower refinance inflow with stable purchase demand.

Looking ahead, the trajectory of mortgage rates will be shaped by geopolitical tensions, such as the conflict in Iran, and domestic monetary policy. If rates continue to inch upward, refinance demand could erode further, pressuring loan‑origination volumes and potentially slowing home‑price appreciation. Conversely, any easing of rate pressures could revive refinancing activity, bolstering MBS issuance and supporting broader housing market liquidity. Stakeholders should monitor rate trends and macro‑economic indicators closely to anticipate shifts in borrower sentiment and adjust strategies accordingly.

Mortgage Applications Retreats Further in April

Comments

Want to join the conversation?

Loading comments...