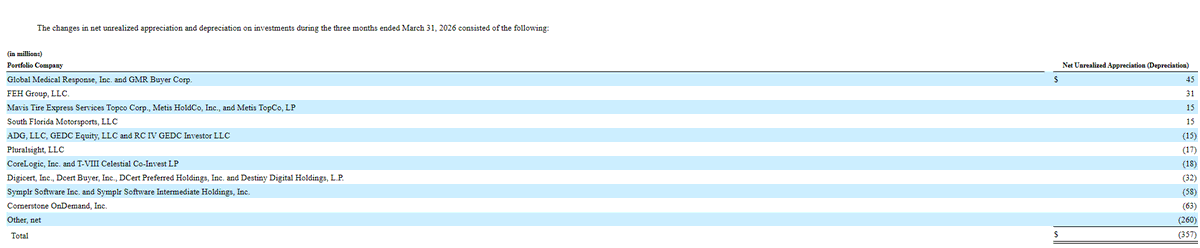

Ares Capital Logs $357M Unrealized Losses, Market‑Driven Write‑

Ares Capital $ARCC is the first private credit fund to report Q1 results. Net unrealized losses were $357 million. The top 3 writedowns were loans to Cornerstone OnDemand, Symplr and DigiCert, which are all software companies owned by Clearlake Capital. None of these loans are on non-accrual, and the reduced marks were presumably market related and not credit related.

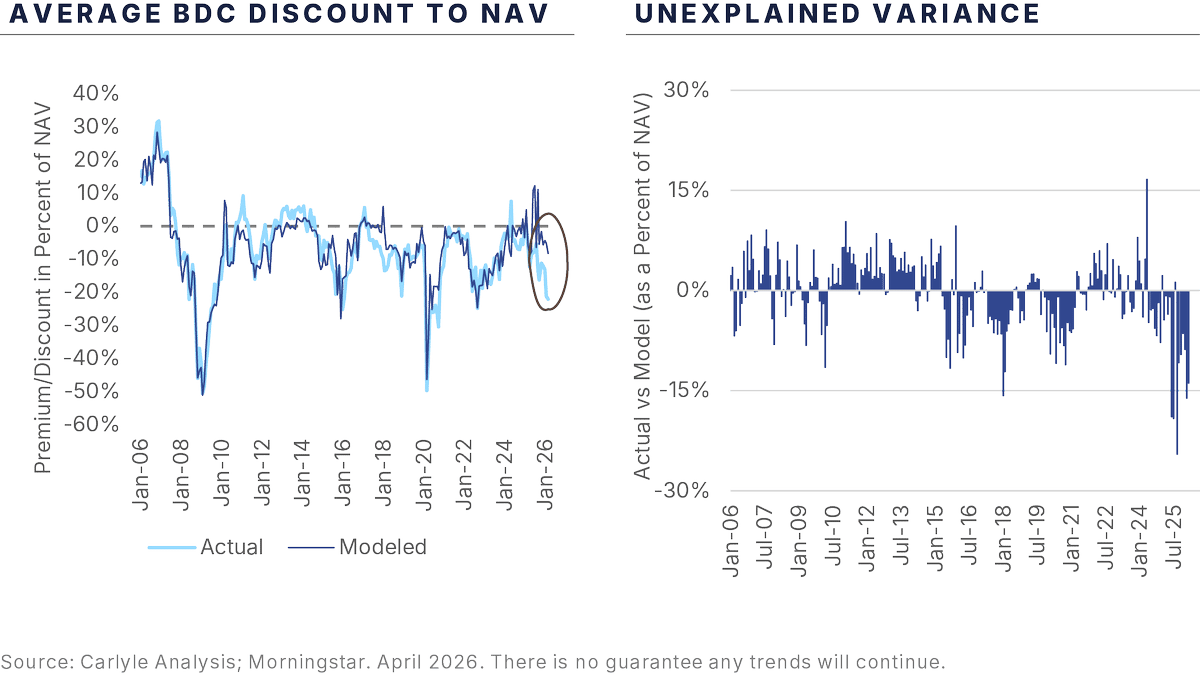

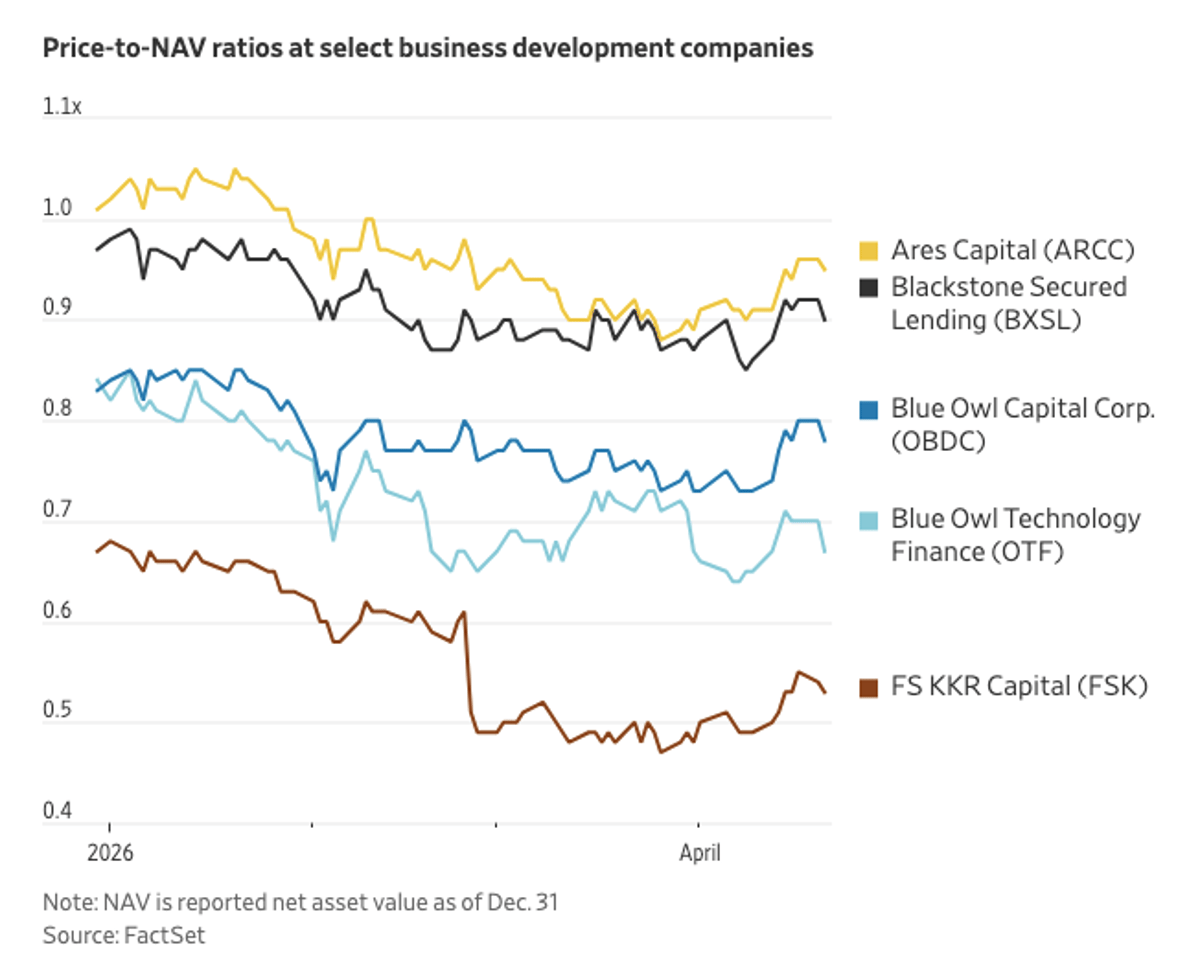

Carlyle's BDC Discount Model Vastly Underestimates Market Reality

Carlyle's modeled average BDC discount of approximately -5% (based on current credit conditions) is far greater than the average actual BDC discounts of more than -20%, leading to a record "historical variance" in which NAV discounts are far wider...

Blue Owl BDC Tender Attracts Under 1% Participation

*BOAZ WEINSTEIN'S BLUE OWL BDC TENDER DRAWS UNDER 1% OF SHARES It was a valiant effort and an interesting campaign, but ultimately Blue Owl nontraded BDC holders will HODL

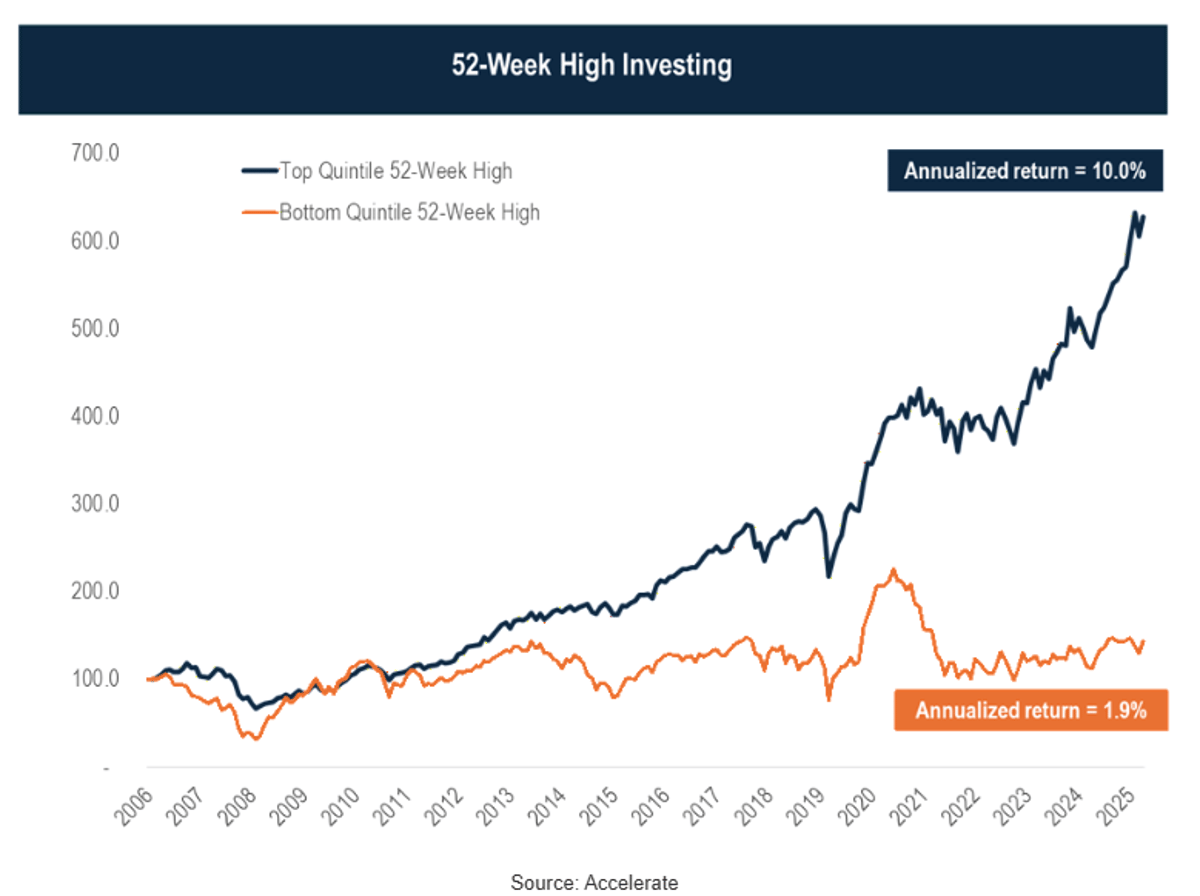

Ignore 52‑Week Highs: Best Buys Often Appear Strong

"The hardest stocks to buy are often the ones the market is telling you are working." My latest memo: Don’t Fear the 52-Week High https://t.co/maO0NjM84P https://t.co/uSecDvzaVW

Four Pharma Deals Showcase Hefty Premiums, Billions at Stake

Today's M&A notes $ARX.to to be acquired by $SHEL.LN for $8.20 cash per share + 0.40247x shares, 26.6% premium, $22.0 billion $OGN to be acquired by Sun Pharmaceutical for $14.00 cash per share, 138.9% premium, $11.75 billion $RMAX to be acquired by $REAX...

Stocks Near 52‑Week High Outperform by 8% Annually

Over the past twenty years, the top quintile of stocks closest to their 52-week high have returned 10.0% annualized. In contrast, the bottom quintile (or those trading furthest from their 52-week high) returned just 1.9% per annum. Don’t fear the 52-week...

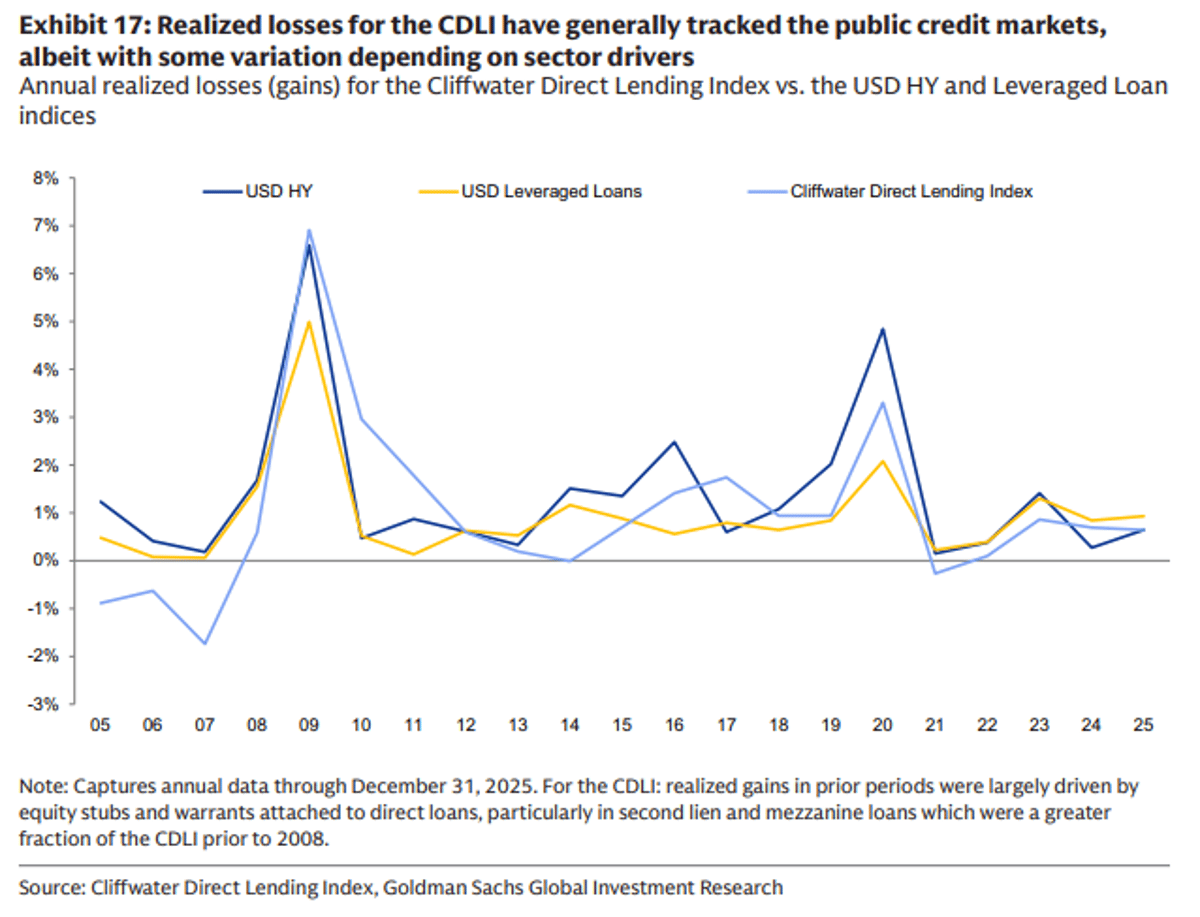

Private Credit Losses Remain Mild, Historically Sub‑1%

Interesting historical private credit metrics: - Private credit losses were -0.64% in 2025 - Long term historical annual average is -1.0% - Worst period was 2008-2010 in which the cumulative realized loss was -10.2% https://t.co/fnCeDwk655

High‑volatility, Uncorrelated Assets Boost Capital Efficiency

Most allocators miss this, because it’s counterintuitive, but a high volatility uncorrelated asset is more useful than a low vol one because it is more capital efficient (assuming expected returns are positive). So yes, this return stream could be useful in...

BDC Buybacks Validate NAV Amid Deep Discount

WSJ: "When a BDC trades at a deep discount to its official NAV, the most direct way to signal that the official marks are reliable is for the fund to repurchase its own stock on the open market." It really is...

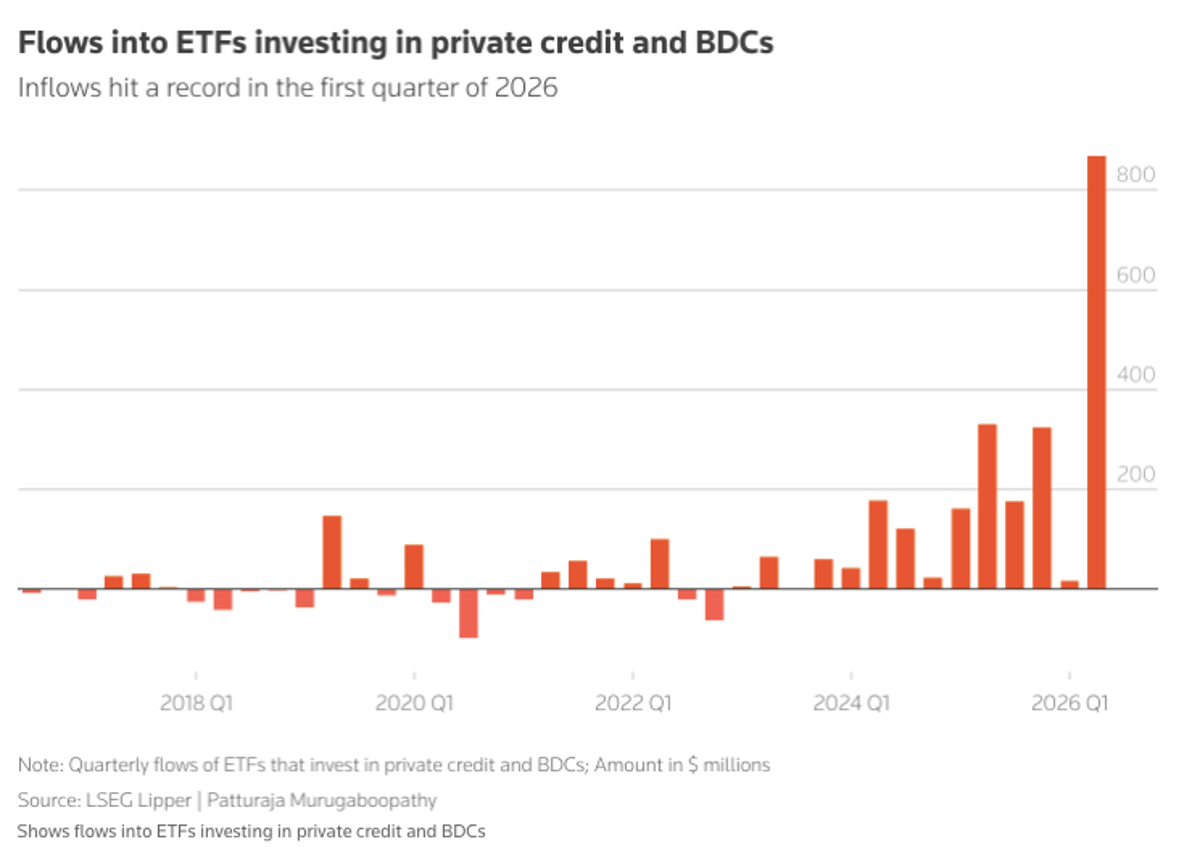

Investors Flood Private Credit ETFs Amid Doom Headlines

Despite the negative headlines, private credit and BDC ETFs have drawn record inflows. “Doomsday headlines may be overstating the actual level of risk. Our flows are telling us a different story: that investors view this as an opportunity to invest at...

War and Inflation Redefine the Market Regime

Absolute Return Podcast #272 Inflation, War, and the New Market Regime with arcMacro Founder Dylan Smith https://t.co/YruLKBcxdr

Medallia Loan Collapses, Blackstone Marks 60% Value

Blackstone has marked the Medallia loan down another 9 points to 60.3 as of Q1’26. It appears that Thoma Bravo has declined to recapitalize the company and it may be owned by its lenders soon. https://t.co/Duuu08riB1

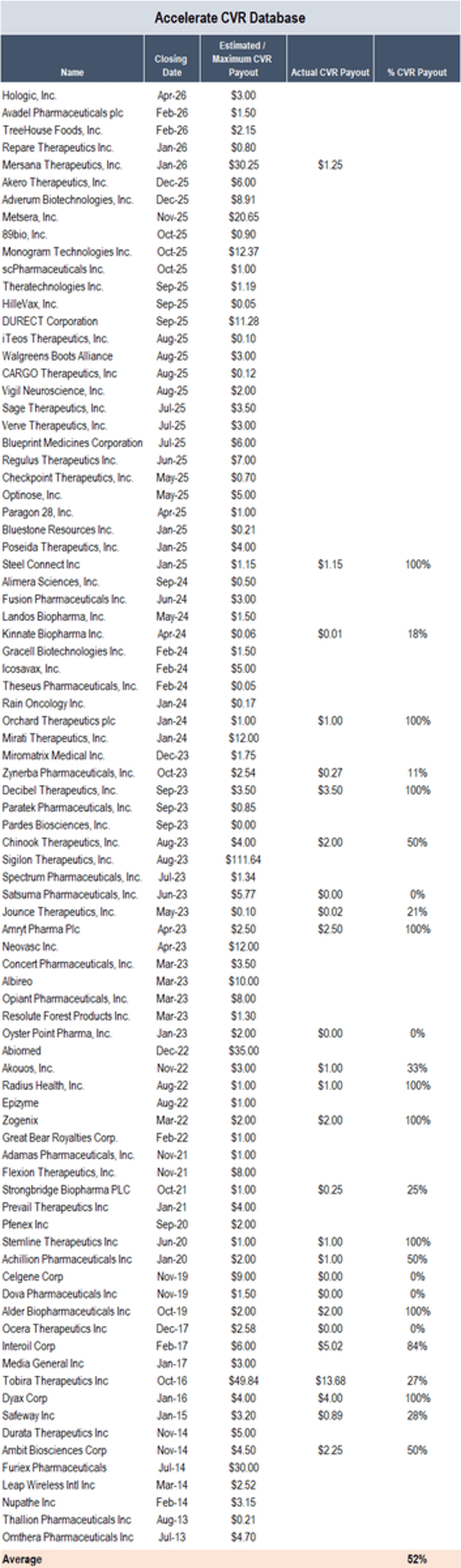

April Sees Record 29% of Deals Using CVRs

An unprecedented 29% of public M&A deals in the U.S. and Canada announced in April feature a contingent value right as part of the deal consideration. The use of CVRs has never been so high. Below is the database of closed deals...

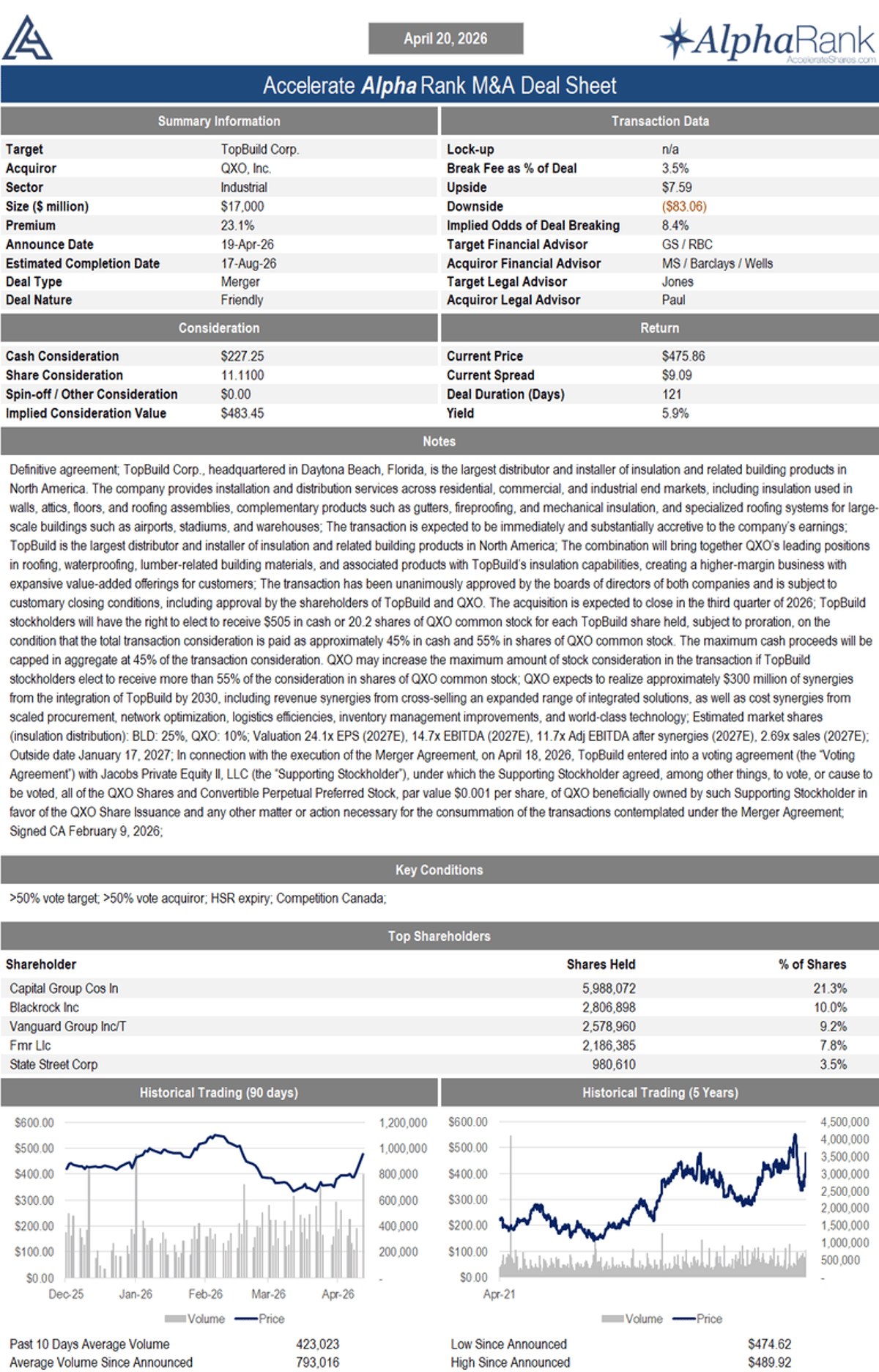

QXO's $17B TopBuild Deal Offers 5.9% Arbitrage Yield

➡️ M&A Deal Sheet ⬅️ TopBuild Corp. $BLD to be acquired by QXO, Inc. $QXO for $227.25 cash per share + 11.11x shares, 23.1% premium, $17.0 billion, 14.7x EBITDA (2027E) Trading at a 5.9% arbitrage yield and an implied 92% odds of...

Four Major Deals Showcase Hefty Premiums Across Sectors

Today's M&A notes $BLD to be acquired by $QXO for $227.25 cash per share + 11.11x shares, 23.1% premium, $17.0 billion $SILA to be acquired by $OWL for $30.38 cash per share, 19.0% premium, $2.4 billion $RUP.to to be acquired by $AEM for...

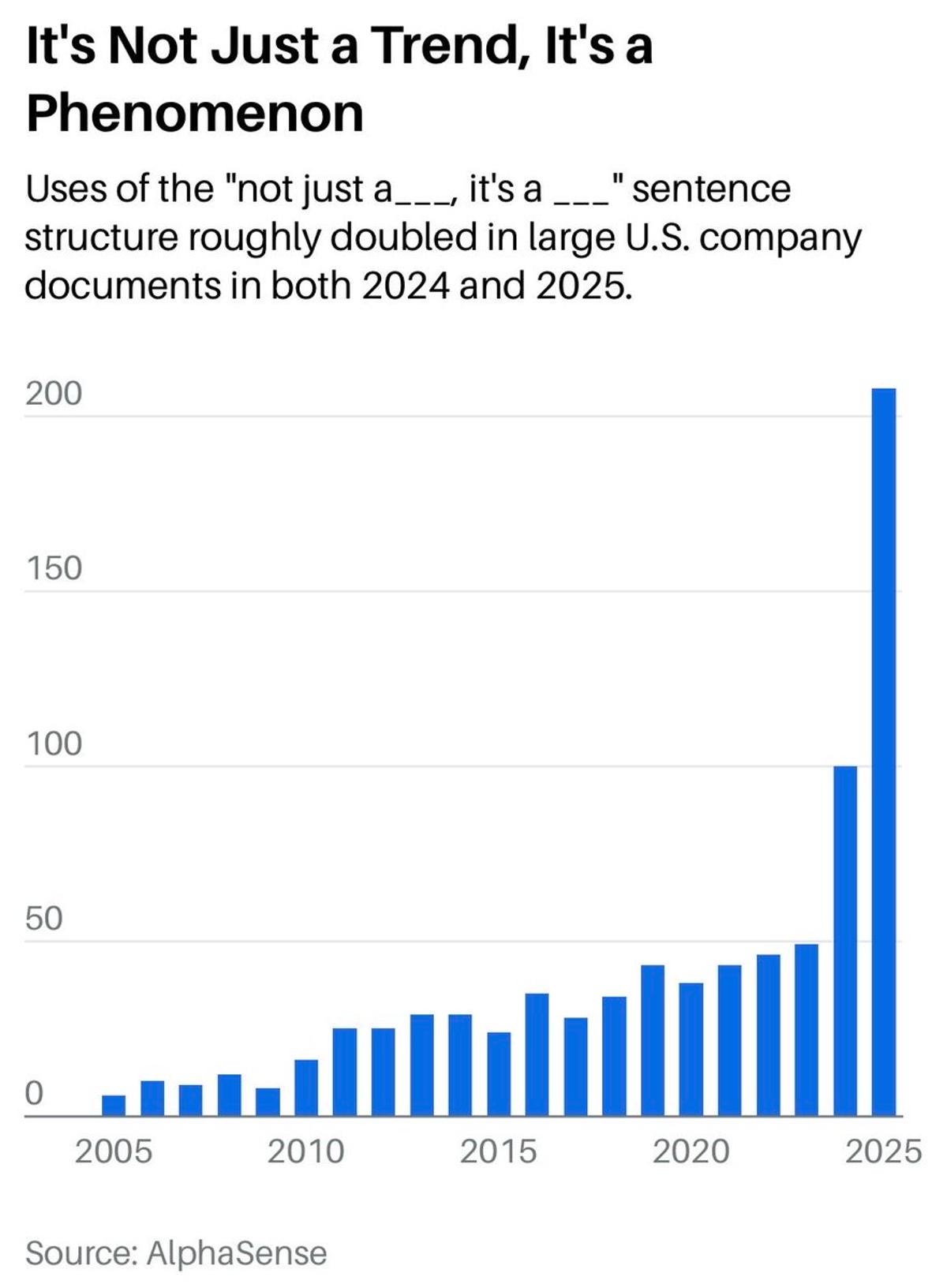

AI Fuels Surge of “Not X, It’s Y” Press Releases

AI has created a bull market in ‘it’s not X, it’s Y’ appearing in corporate press releases. https://t.co/uB4nF1Eeff

Trudeau Era Sparks $1 Trillion Capital Exodus

The "Trudeau Tragedy": “Between 2015 and 2024, more than $1 trillion of investment exited Canada — the largest capital exodus in Canadian history”

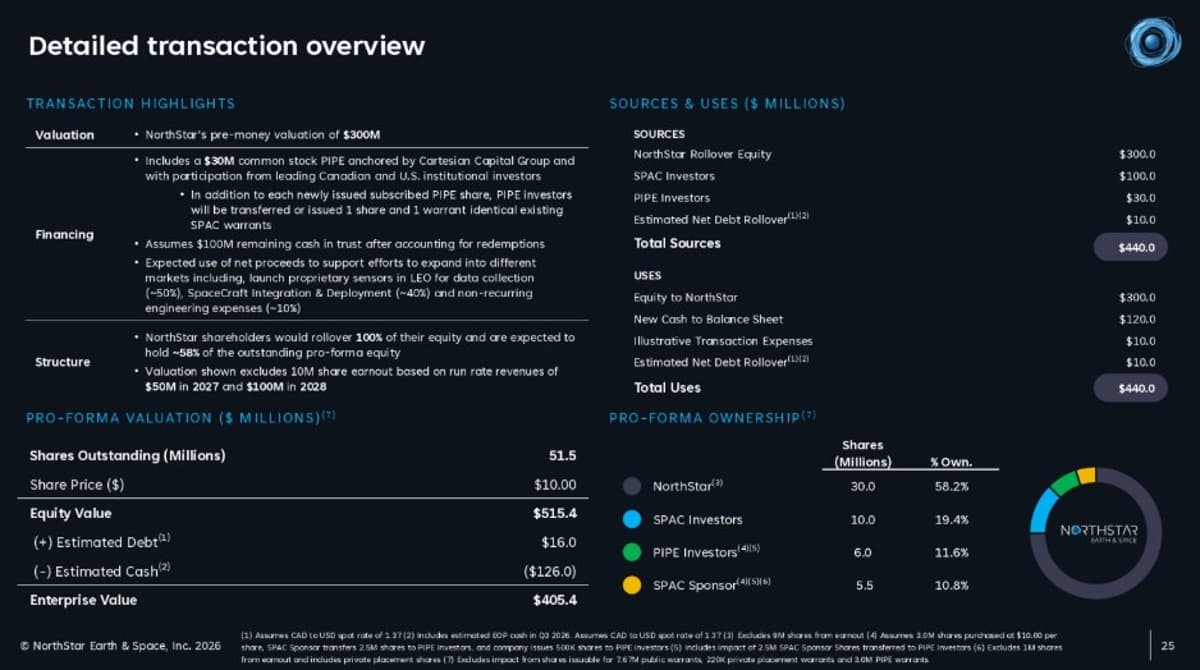

NorthStar Satellite Analytics Secures $30M PIPE, $405M Valuation

NorthStar / Viking Acquisition I deal overview Space and satellite data analytics company $405 million enterprise value $30 million PIPE Closing Q3 Symbol $NSTR PR: https://t.co/v61y0ElAJP IR deck: https://t.co/mosqCqKlMZ Disclosure: Long $VACI shares + warrants in $ARB.to https://t.co/CTqRus69vb

Cut Antitrust Red Tape, Build Canadian Champions

First, the Trump administration took the positive step to dramatically reduce the U.S.'s stifling antitrust regulatory regime. Now, the EU is rightfully following suit. Dear PM @MarkJCarney, let's cut regulatory red tape at the Competition Bureau and create Canadian Champions. https://t.co/FrxajvGasb

Private Credit Shows Unexpected Strength, Cycle Likely Turning

Interesting to note the relative strength of private credit over the past several weeks. Here's Barrons: "Private credit has been notably quiet in recent months, with far less visible stress than many expected... the lack of volatility could suggest that...

Skipped BIRD Liquidation; Stock Surged 467%

I took a look at $BIRD upon announcement of their asset sale as a liquidation play, but figured we may get screwed on the liquidation proceeds, so I passed. Turns out my thesis was right, but the result was very, very...

M&A Surge: AVNS, GSAT Deals Lead $13B Activity

Today's M&A and SPAC notes $AVNS to be acquired by American Industrial Partners for $25.00 cash per share, 72.1% premium, $1.3 billion $GSAT to be acquired by $AMZN for $90.00 in cash + stock, 23.5% premium, $11.7 billion $SZZL announced a business combination...

Private Credit Defaults Far Lower than Market Fears

Goldman's David Solomon providing some much needed rational thought around private credit: - GFC saw defaults peak at 10% - recoveries were 50% - trough cumulative loss of 5%-6% vs coupons of 9%-10% For context, listed BDCs are currently pricing in defaults of more...

Private Credit May Calm, Not Amplify, Corporate Cycles

How dare these academics posit such a narrative violation: "Contrary to the concern that private credit could amplify credit supply shocks, our results indicate that private credit may dampen the corporate credit cycle"

All Factors Down, Hedge Fund Proxy Plummets, Shorts Rise

Value, quality, and momentum factors all down today. Long short hedge fund proxy declined -188bps. The only thing that was up was high short interest. Not healthy. https://t.co/nCK12nnBAU

Two Major Acquisitions Announced, Two SPAC Deals Terminated

Today's M&A and SPAC notes $SES.to to be acquired by $GFL.to for $4.95 cash + 0.3356x shares, 16.8% premium, $6.4 billion $LEG to be acquired by $SGI for 0.1455x shares, 13.7% premium, $2.5 billion $ETHM / The Ether Machine deal terminated $SPAC.to / Cube...

Covered Calls Aren’t Income, They’re Position Reductions

Selling a covered call does not "generate income". It represents cash proceeds from reducing your position (the functional equivalent to selling), and paying a massive bid-ask spread to do so. https://t.co/evuVehJaQT

Second Inflation Wave Revives Commodity Prices

My latest monthly client memo: The Second Wave of Inflation and the Commodity Comeback https://t.co/4L7dEvdDn4 https://t.co/eRCYHTHapt

Commodities Futures Add Value to Balanced Portfolios

If you look at the data, investing in commodities futures makes sense within the context of a total portfolio approach. https://t.co/KYqknJKQ54

Lowest‑P/E Stocks Explode: Micron Up 520% Year‑to‑Date

The cheapest stock in America is up 520% in a year. The 10 lowest-P/E stocks are up 70% YoY. Micron has the lowest P/E in the S&P 500 at just 4.4x. Disclosure: long $MU https://t.co/W2gEcOm2By

SPAC DAT Merger Ends, PIPE Investors Breathe Relief

PIPE investors breathe a sigh of relief as we get the first big SPAC DAT merger termination. Dynamix $ETHM terminates its business combination with The Ether Machine, which is awkward after already changing its ticker. Also, who gets the $50 million break...

Private Equity: The Kid Who Hides Trouble Until Inevitable

Remember when you were a kid and got in trouble at school but held off telling your mom for as long as possible, delaying the inevitable? That's private equity today.

Massive WBD, KVUE Block Trades Signal Merger Arb Alert

$198mm $WBD and $200.4mm $KVUE block trades today at the close Merger arb PM got a tap on the shoulder today? https://t.co/tx0WOC2arI

M&A Spree Sees Premiums up to 80%

Today's M&A and SPAC notes $GTWO.to to be acquired by $GMIN.to for 0.212x shares + CVR + Spinco, 79.7% premium, $3.0 billion $WSR to be acquired by $ARES for $19.00 cash per share, 26.5% premium, $1.7 billion $ASRT to be acquired by Garda...

Discounted BDC Seeks Dilution, Vote Likely to Fail

A BDC can only issue shares below NAV if it has prior shareholder authorization. This shareholder approval for dilutive share issuance is required annually. In the current market environment, most BDCs with good corporate governance are aggressively buying back shares at...

Institutions Flood Private Credit as Retail Walks Away

Investors can be prorated on the way in too. “COF V is Blackstone’s largest opportunistic credit fund raised to date, reflecting continued strong institutional demand for private credit." Institutional investors piling in to private credit as retail flees. https://t.co/gjHIJ7Kg2B

M&A Surge: Blackstone Deal, SCII LOI, Two $200M IPOs

Today's M&A and SPAC notes $HOLX / Blackstone / TPG deal closed $SCII entered LOI with a payments technology company $ACGCU $200 million IPO $AACPU $150 million IPO https://t.co/094cl5qlvH

FTC Shifts to Divestiture‑First, Settlement‑Driven M&A Policy

On Friday, the Federal Trade Commission published its 5-year strategic plan under Chair Andrew Ferguson The most notable change is the FTC's strategy to reasonably regulate M&A from an antitrust perspective, highlighting their new policy to "prioritize divestitures" and "engage in...

Now Is Prime Time for Fresh Private Credit Capital

Quite the opportune time to be putting fresh capital to work in private credit. https://t.co/JSc6jmY0Rb

HOLX at Buyout Price, CVR Lottery Offers Tiny Upside

The Hologic buyout by Blackstone / TPG at $76.00+CVR is expected to close tomorrow With the stock trading at $76.01, you can get a lottery ticket that'll pay as much as $3.00 for $0.01 (CVR payout based on Breast Health division...

Rising Private Credit Redemptions Signal Potential Trouble

My latest memo on the private credit market: Redemptions Are Climbing — Is That a Problem? https://t.co/QbeBHZNKir https://t.co/0CaMneVvAU

Closed Markets Make Today Ideal for Bad News Filings

While North American stock exchanges are closed, EDGAR is open. - and it is probably the best day of the year for a public company to file a bad news 8-K. So yes, all analysts working today.

Coke Now Outprices Microsoft, Defying Gates' Logic

Bill Gates once argued that tech stocks should trade at lower multiples than consumer staples, due to disruption risk. Nearly 30 years later, $KO is trading at a premium to $MSFT https://t.co/kvxe5UxICA

OCIC Redemption Spike Covered by Quarterly Tender Liquidity

Blue Owl's non traded BDC, OCIC, received redemption requests for 21.9% of the fund. Is it cooked? No, it'll be fine. Here's why: 1) Portfolio turnover and 5% quarterly tender - OCIC tenders for 5% of its fund each quarter (20% per annum),...

Medallia Loan Collapse Erases $5.1B Equity, Media Silent

Medallia loan value continues to decline, with latest marks at 69. With the term loan in distress, the $5.1 billion of equity has certainly been vaporized. This -100% private equity loss surpasses any private credit loss by an order of magnitude. Where's...

Deep Discounts Drive High Redemption Tenders in Blue Owl Funds

Blue Owl Credit Income (OCIC) with 21.9% tendering for redemption and Blue Owl Technology Income (OTIC) with 40.7% tendering for redemption makes sense as both have publicly-traded "sister" funds that trade at large discounts to NAV: Blue Owl Capital $OBDC trades...

March Hurts Long‑short Equity; April Rebounds Sharply

March was a challenging month for long short equity hedge funds as junk stock shorts materially outperformed (+7bps on the month). The GS VIP Long vs GS Most Shorted basket fell -7.6%, dropping its YTD performance to -14.4%. That said, April is...

Denies Air Canada CEO Rumors, No Acceptance Plans

PERSONAL UPDATE: I want to address the rumors and media speculation that I recently interviewed for the position of CEO at Air Canada, and the below picture of my response when they asked about my french skills. As it currently stands,...

Private Credit Wins: Sixth Street Secures Prepayment Fee

Looks like some private credit is good. With Apellis $APLS set to be acquired by Biogen $BIIB, Sixth Street $TSLX is likely to earn a prepayment fee on its term loan (which is at SOFR + 575). https://t.co/AS5W0OFzUn

Strong SaaS Growth Offsets Multiple Contraction

While SaaS multiples have contracted meaningfully, 20-30% revenue CAGR since 2021 means that revenue has increased 150-250%, counteracting much of the multiple contraction from an LTV perspective (assuming no dividend recaps). Growth solves a lot of problems over time.