Mike the Value Investor

Professional investor focused on fundamentals and intrinsic value; shares valuation concepts (e.g., ROIC, FCF, scenario analysis) and long‑term equity strategy.

Graham Prioritized Tangible Book Value Over Accounting Goodwill

Most investors think a high book value means a cheap stock. Graham didn't. He wanted tangible book value, assets you can actually touch, sell, or liquidate. Goodwill-heavy book value is an accountant's opinion. Tangible equity is a margin of safety.

Berkshire Gives Acquisitions Freedom, Not Just Capital

The most underrated thing Berkshire offers its acquisitions isn't capital. It's freedom. 1️⃣ No committee theatrics eating up your calendar 2️⃣ No quarterly PowerPoint ritual nobody believes in 3️⃣ No second-guessing where your excess cash goes Just: run the business. We'll handle the rest. Most investors...

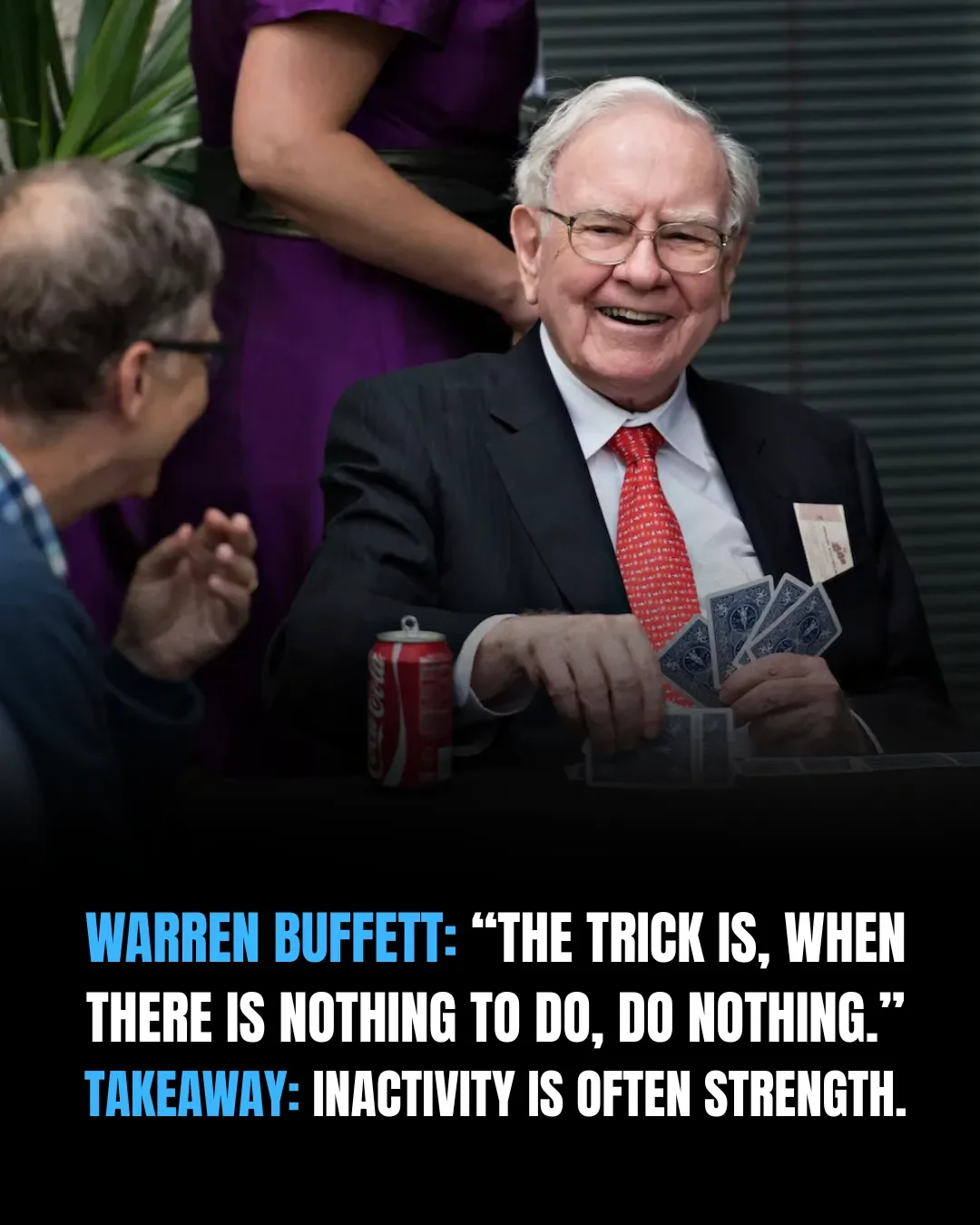

Patience Beats Panic: Buffett’s Secret Skill

Buffett's most underrated skill isn't stock-picking. It's sitting on his hands while everyone else panics. Most people confuse activity with progress — in life and in portfolios. Do the math. Then wait.

Holding Cash Early Beats Desk Decisions Later

Seth Klarman proves that the best investing decisions aren't made at a desk, they're made years earlier, when you decided to hold cash while everyone else was fully invested. Preparation isn't passive. It's the most aggressive thing a value investor can...

Discounts Mean Nothing when Assets Are Overstated

Most investors blow up not because they overpaid. Because the thing they bought at a "discount" was worth less than the paper it was reported on. Overstated assets don't offer margin of safety. They offer margin of false comfort. Mr. Market doesn't care...

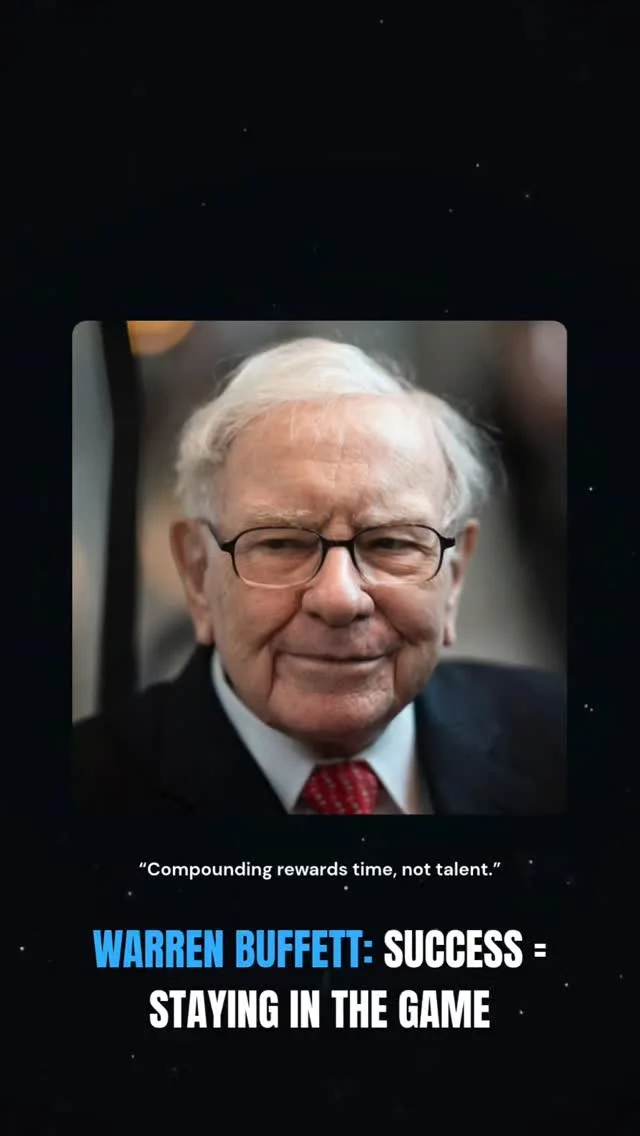

Compounding Rewards Persistence, Not Brilliance, over Time

Buffett admits it plainly: if he'd died at 60 like his father, you'd never have heard of him. He wasn't smarter at 60 than at 30. He just kept showing up. Compounding doesn't reward genius. It rewards whoever stays in the game longest.

Graham's Edge: Process Over Story, Let Statistics Win

Graham's edge wasn't genius. It was a process: 1️⃣ Find broadly undervalued securities, not one "perfect" pick 2️⃣ Let margin of safety do the work, not your story 3️⃣ Repeat until the math wins Most investors want a great story. Graham wanted great odds. Stories...

Stress‑test Your Model Before Investing, Not Just During Booms

Mr. Market is generous in expansions and brutal in recessions. Your valuation assumptions should already know that. If your model only survives the good times, it isn't a model — it's a mood. Stress test first. Invest second.

Investors Should Judge CEOs by Their Future Reputation

Buffett met Gianni Agnelli once. One line changed how he thought about people: "When you get old, you've got the reputation you deserve." Here's what that means for investors: 1️⃣ The market is short-term forgiving, long-term honest. 2️⃣ Management track records are lagging indicators...

Timeless Value Investing Beats Every Market Shift

The market changes every decade. The principles don't. New asset classes. New technologies. New narratives. But buying below intrinsic value? Still works. Margin of safety? Still works. Patience? Still works. Ben Graham figured this out in the 1930s. Mr. Market still hasn't gotten...

Three‑question Checklist Decides Conviction vs Caution

Three questions before I buy anything: Would I pay this price for the assets alone? Do the earnings justify it if growth flatlines? Does the dividend signal management believes the story? One "no" = caution. Three "yeses" = conviction.

Buy Great Businesses Only at Suitable Prices

Graham didn't say "buy great businesses." He said buy them at suitable prices. There's a word missing from most investor vocabularies. That word is "suitable."

Focus on Big Winners, Not Just Avoiding Mistakes

Most investors obsess over not making mistakes. Peter Lynch obsessed over making sure the winners were big enough to cover them. That's the whole game.

Safety Lies in Capital Structure, Not Just Stock Price

A bad year tests a business. High leverage ends one. Earnings recover. Dilution doesn't. Bankruptcy doesn't. The equity you owned before the rescue round doesn't. Margin of safety isn't just about price. It's about capital structure.

Focus, Not Timing: Concentrate on Few, Win Big

Buffett doesn't time the market. He times his attention. The best capital allocators I've studied don't work harder — they work on fewer things, longer. Concentration isn't just a portfolio strategy. It's a life strategy.

Buy When Pessimism Drives Prices Below Liquidation Value

Ben Graham waited for bad news. That's not a typo, it's the whole strategy. A true bargain only exists when pessimism has priced the business below what its parts are worth in a liquidation. No pessimism = no bargain. The crowd hates the...

Ignore Debt Seniority, Destroy Acquisition Value

Buffett's hierarchy before making any acquisition: 1️⃣ Can the business pay its own way? 2️⃣ If we borrow, who now sits above the shareholder? 3️⃣ Is the upside worth that demotion? Most acquirers never ask #2. That's why most acquisitions destroy value.

Intelligence Is a Habit, Not a Gift—Read Daily

Most people think intelligence is a gift. Munger thinks it's a habit. He surveyed every wise person he'd ever met across his entire life — and found zero who didn't read constantly. Not some. Not most. Zero. The sample size is 99 years. That's...

Consistent Dividends Reveal Management Integrity Over EPS

Most analysts study earnings per share. The smart ones study dividend history. One can be massaged. The other has to be paid, in cash, every quarter, for decades. Show me 20 years of uninterrupted dividends and I'll show you management that can't...

Buffett Profits From Cards Yet Warns Against Debt

Buffett owns one of the most profitable credit card businesses on earth. And he still tells young people: don't use credit cards to fund a lifestyle you haven't earned yet. The guy selling you the rope is warning you not to buy...

Patience Is the Market’s Most Aggressive Advantage

Most investors think patience is passive. It's not. It's the most aggressive advantage in the market. Nine women can't produce a baby in one month. A great business can't compound in a quarter. Stop mistaking urgency for strategy.

Wealth Comes From Normalized Earnings, Not Quarterly Spikes

Most investors obsess over next quarter's earnings. The ones who actually build wealth ignore them entirely. Intrinsic value runs on normalized earnings, what the business earns in a normal year, not its best year. Peak profits are a trap dressed up as a...

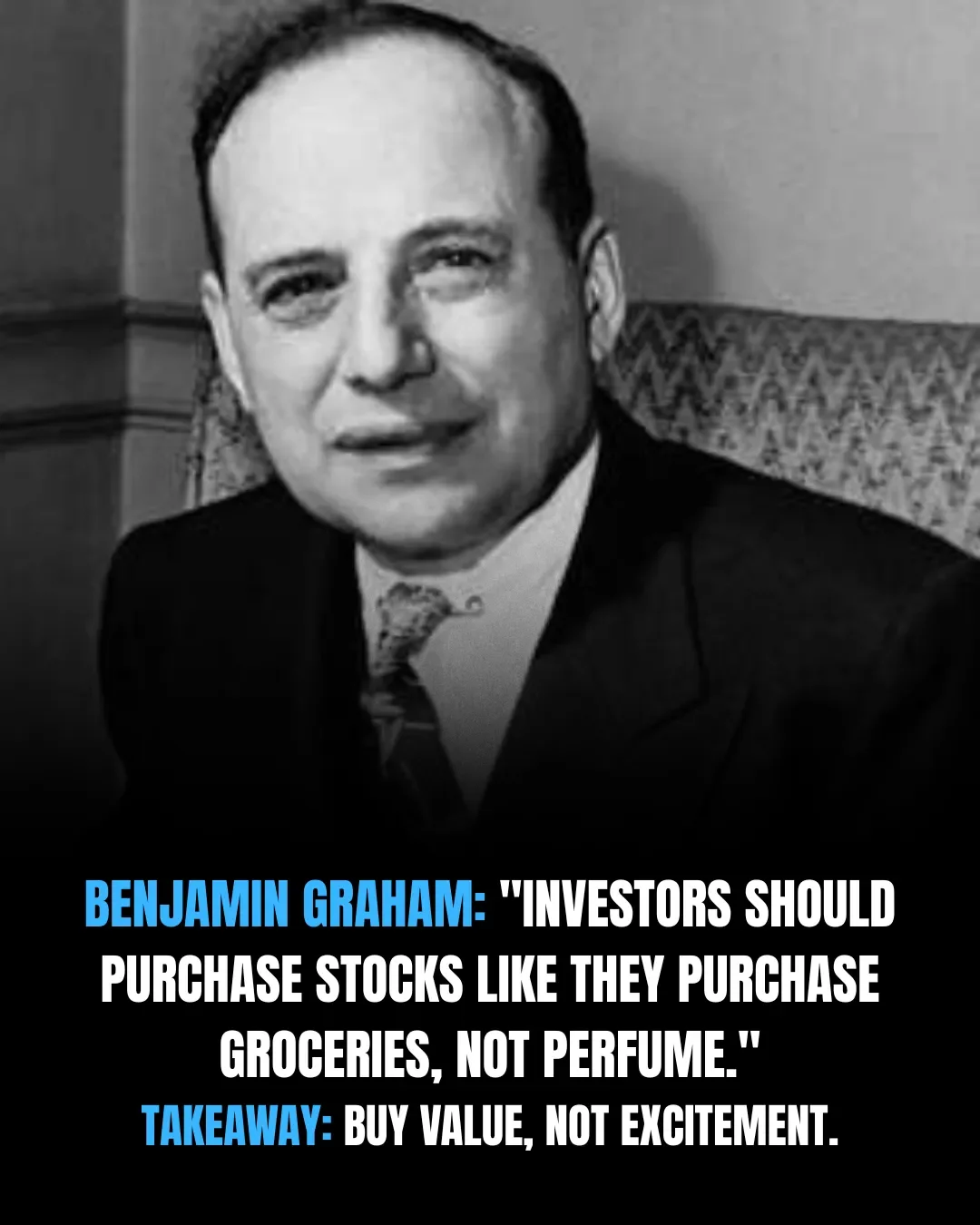

Buy Stocks Like Groceries: Pay Price, Not Hype

Graham's grocery store rule is the most underrated idea in investing. Here's what it actually means: 1️⃣ Groceries have a price you compare. Perfume has a price you feel. 2️⃣ You never overpay for milk because it's "trending." Why do it with stocks? 3️⃣...

Discipline Means Valuing Fundamentals Over Market Noise

Ben Graham didn't chase stocks flying up. He didn't panic-sell stocks falling down. While everyone else was reacting to price, he was focused on value. One never changed without reason. The other changed every second. Discipline isn't missing out. It's knowing the difference...

Margin of Safety Means Earnings, Low Debt, Not Price

Ben Graham didn't just want cheap stocks. He wanted cheap stocks that could survive being wrong. That's the part most value investors skip — two conditions, not one: earnings must cover the downside, and debt must stay low enough to survive it. Margin...

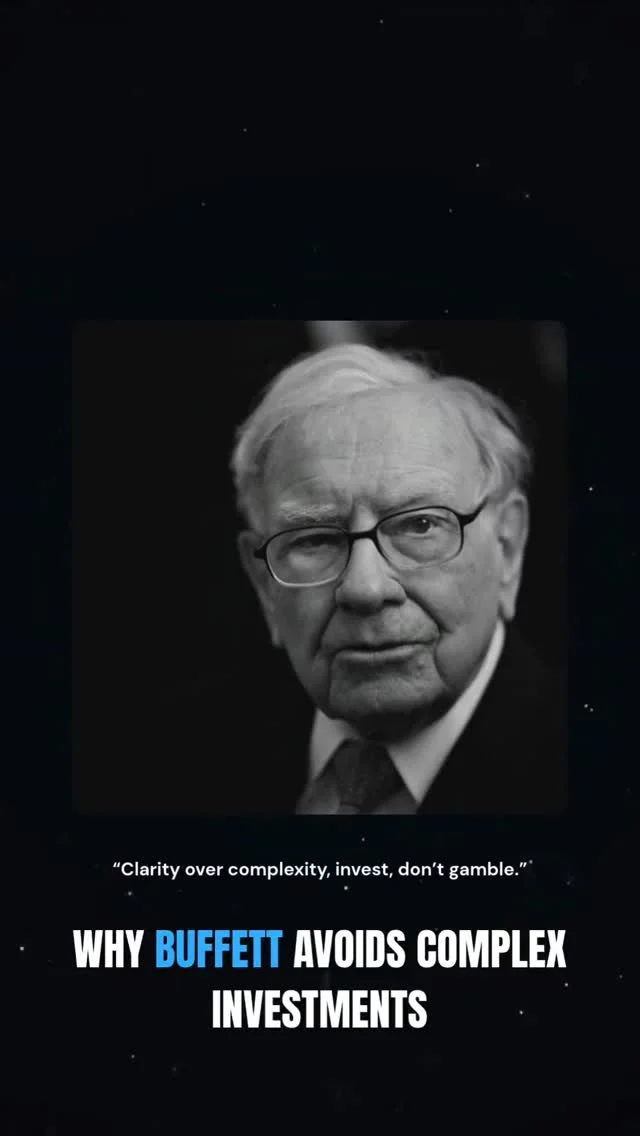

Buffett Chooses Simple Clarity Over Complex Sophistication

Buffett understands hamburgers better than semiconductors. That's not a weakness. That's a strategy. Most investors chase complexity because it feels sophisticated. He chases clarity because it actually works. If you can't explain why the business makes money, you don't own an investment. You...

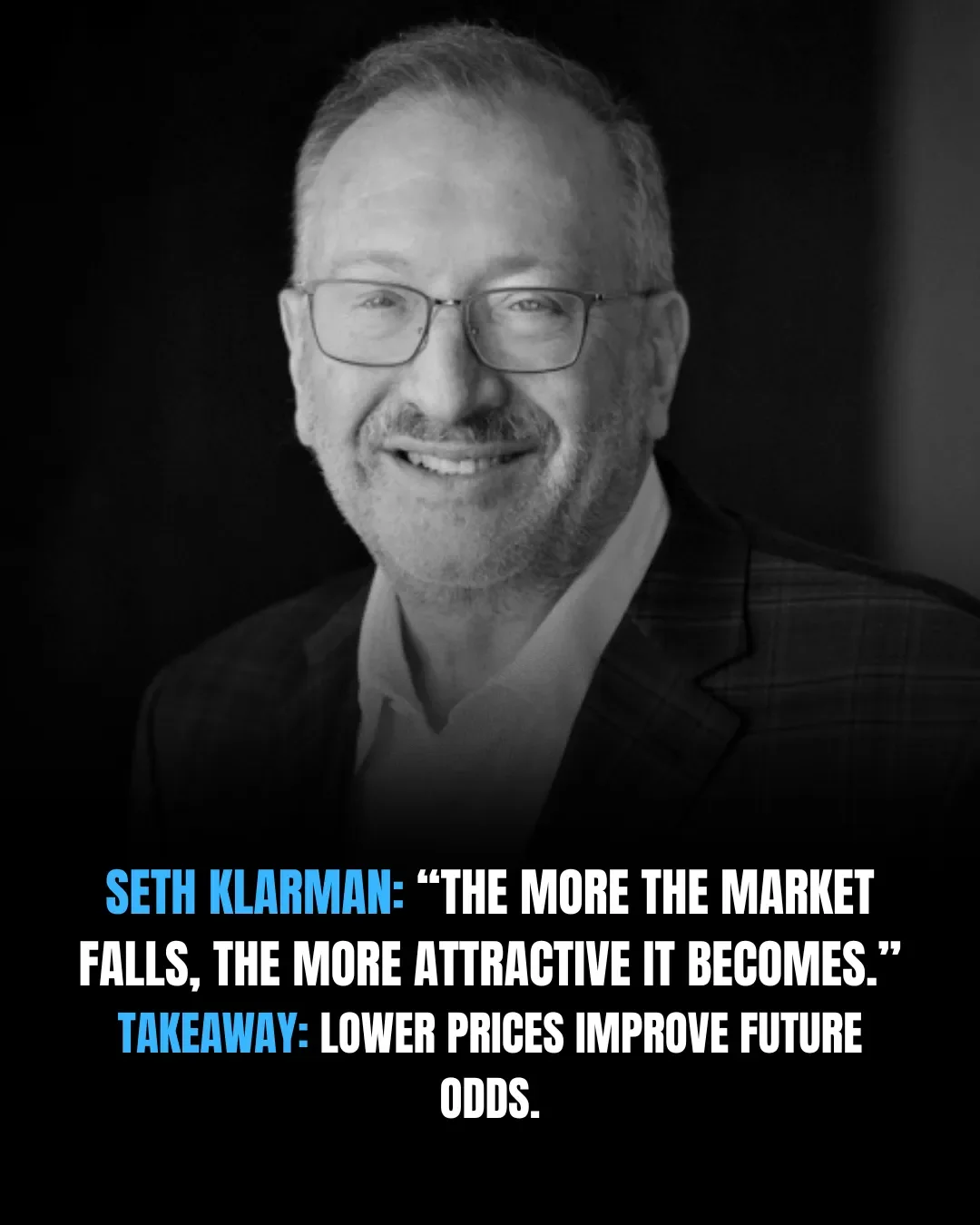

Klarman Sees Market Dip as Discount, Not Panic

Seth Klarman doesn't panic when markets fall. He gets interested. The crowd sees danger. He sees the price of future returns just dropped. Mr. Market is having another episode, and writing you a discount.

Book Value Only Matters With Liquid Assets and Clear Liabilities

"Book value matters most when assets are liquid and liabilities are transparent." Most investors get book value wrong, and it can cost them. Book value really only matters when a company’s assets can be easily turned into cash and its liabilities are...

Invert Your Strategy: Avoid Mistakes, Grow Wealth

Want to improve your investing results? Learn Charlie Munger’s inversion thinking, focus on what to avoid, not just what to chase. This simple mental model can sharpen decision-making, reduce risk, and boost long-term wealth in the stock market.

Pick Great Companies Over Favorable Industries Every Time

"If it's a choice between investing in a good company in a great industry, or a great company in a lousy industry, I'll take the great company in the lousy industry any day." ~ Peter Lynch

Start Valuation with Balance Sheet, Not Earnings

"Graham valuation starts with balance sheet reality, then adjusts for earning power." Most investors focus on earnings, but overlook what’s actually real.

Low Prices Aren’t Guarantees: Avoid Cheap Stock Traps

Learn why a low stock price doesn’t automatically mean a good investment in this engaging topic inspired by Peter Lynch. This idea focuses on the dangers of “cheap stocks” and how they can still fall to zero, making it essential...

Cash: Unlimited Call Option, Pure Financial Flexibility

Warren Buffett: “Cash is a call option with no expiration date.” Takeaway: Liquidity equals flexibility.

Buy Cash‑flow Assets Cheap, Ignore Market Hype

"The intelligent investor buys discounted cash-producing assets, not market excitement." Stop chasing hype, start owning real value.

Patience Beats Tickers: Invest in Quality, Not Daily Swings

Warren Buffett shows us that patient, long-term investing beats watching the stock ticker every day. Using See’s Candy as an example, once you buy a high-quality business, fundamentals matter more than daily price swings.

Choose Better, Not More: Long-Term Investing Wins

The secret to stock market success isn’t trading more, it’s choosing better. Learn how long-term investing and patient decision-making can help you outperform and grow your wealth over time.

Credibility Beats Hype: Buffett’s Long‑Term Value Investing

Warren Buffett proves that trust and credibility often matter more than fancy strategies. Learn why genuine, long-term value investing beats hype and how staying disciplined can help you build wealth over time.

Control What You Can, Build Real Investment Wealth

Charlie Munger’s mindset is a game-changer for investing. Stop thinking like a victim and start focusing on what you can control. The best investors stay rational, adapt quickly, and learn from every setback. That’s how real wealth is built in...

Low P/E Misleads When Earnings Are Leveraged or Cyclical

"A low P/E is irrelevant if earnings are inflated by leverage or cyclicality." A “cheap” stock isn’t always a bargain. A low P/E ratio can be misleading. Sometimes earnings look strong only because the company is heavily in debt. Other times, especially...

Stay Calm: Long-Term Value Beats Short-Term Panic

Warren Buffett reminds us that stocks might feel risky in the short term, but over the long run, they create real wealth. Even Berkshire Hathaway went through 50% drops, and Buffett stayed confident. Think like an owner, focus on value,...

Buy a Dollar for Fifty Cents with NCAV Investing

"Net current asset value (NCAV) investing is valuation by liquidation logic." What if you could buy $1 for 50 cents? That’s the logic behind NCAV investing, valuing a company as if it were liquidated today.

Liquidity and Solvency Ratios: Core Valuation Metrics

"Liquidity and solvency ratios are valuation inputs, not accounting trivia." Liquidity and solvency ratios aren’t just numbers, they show the real health of a company.

Patience Over Action: Buffett’s Key to Long-Term Wealth

Patience beats action in the stock market. Inspired by Warren Buffett, this investing mindset shows why waiting for the right opportunity is key to long-term wealth building. Stop chasing every trade, focus on value investing, smart decisions, and strong portfolio...

True Value Requires Assets or Earnings, Not Low Price

"A stock is not undervalued unless intrinsic value is supported by hard assets or earning power." Most “cheap” stocks aren’t actually cheap.

Avoid Stocks with Confusing Accounting, Buffett Advises

Warren Buffett’s investing rule is simple: if the accounting is confusing, walk away. Smart investing starts with transparency. If you can’t understand the numbers, you shouldn’t own the stock.

Wealth Grows Through Daily, Long‑Term Rational Investing

Building wealth isn’t about getting rich overnight, it’s about staying in the game. Charlie Munger’s mindset: show up daily, think long-term, and make rational moves in the stock market. That’s how portfolios grow.

Quality Businesses Create Value Even without Market Hype

"A high-quality business compounds intrinsic value even when the stock is ignored." Most investors chase attention, smart investors build value.

Agency Costs Silently Erode Your Investment Returns

Agency costs can quietly drain your portfolio. As Charlie Munger explains, both self-serving executives and poor decision-makers can hurt long-term returns. Learn smarter stock analysis and build wealth with better investing strategies. Most investors ignore this silent portfolio killer—and it’s costing...

Patience Beats Data: Markets Reward Long-Term Discipline

"Patience captures the value that spreadsheets underestimate." Spreadsheets don’t reward patience—but markets do. Most investors overestimate short-term signals and underestimate long-term compounding. The real edge isn’t in more data, it’s in discipline.

Excitement Costs Returns; Prioritize Value and Patience

In stock market investing, chasing excitement often destroys returns. Charlie Munger reminds us that smart investors focus on what truly adds value, compounding, patience, and clarity, rather than unnecessary risks or short-term wins. Excitement is expensive in the stock market.