Powell’s Last Meeting

Key Takeaways

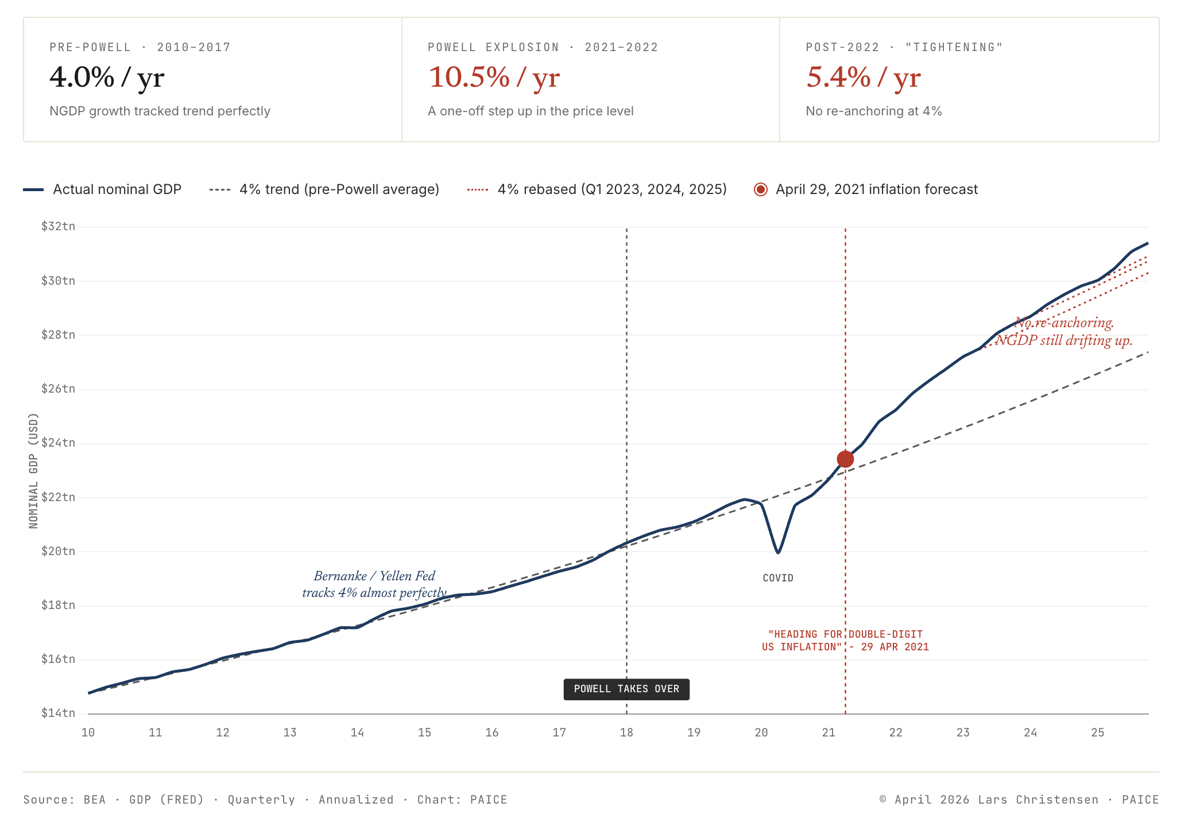

- •Powell's Fed ran easiest policy in modern history, NGDP >4% trend

- •Inflation peaked 9.1% in 2022 after delayed response to money surge

- •Warsh nominated; lacks clear monetary rule, faces fiscal‑dominance pressures

- •Credibility gap gives Trump political leverage to demand lower rates

- •Future regime shift hinges on Warsh's approach to independence and macroprudential scope

Pulse Analysis

The final Powell meeting marks more than a routine rate decision; it closes a chapter where the Federal Reserve tolerated an unprecedented expansion of nominal GDP. By keeping the policy rate near zero through 2021‑22, the Fed allowed NGDP to run at 10‑11% annually, far above the long‑run 4% target. This accommodative stance generated a sharp inflation surge, peaking at 9.1% in mid‑2022, and forced a later, aggressive tightening that succeeded in lowering headline prices but failed to restore the pre‑crisis growth regime. The credibility gap left by that episode now fuels political narratives that the Fed is too tight, even though objective data shows the opposite.

The political dimension intensifies as President Trump and congressional Republicans leverage the Fed’s weakened standing to press for lower rates, citing fiscal concerns. Federal debt now exceeds 100% of GDP, and net interest payments have risen from roughly $350 billion in 2020 to over $1 trillion in 2025. In a fiscal‑dominance scenario, the Treasury’s budgetary pressures can constrain monetary independence, prompting a cycle where lower rates are demanded to ease debt servicing costs, potentially reigniting inflationary pressures. Understanding this dynamic is crucial for investors and policymakers who must assess the risk of policy being shaped by fiscal imperatives rather than macroeconomic fundamentals.

Kevin Warsh’s nomination introduces uncertainty about the next monetary regime. While he is known for criticizing the Fed’s balance‑sheet expansion and macro‑prudential overreach, he has offered no concrete rule‑based framework—whether NGDP, price‑level, or inflation targeting—to anchor policy. Without a clear strategy, the Fed could either revert to a more disciplined stance or succumb further to fiscal pressures, reshaping the U.S. monetary landscape for years to come. Stakeholders should watch Warsh’s early statements and the June FOMC meeting for signals on whether the Fed will regain its credibility or continue operating under a compromised, politically influenced regime.

Powell’s last meeting

Comments

Want to join the conversation?