Your Loan Fails because of the Opening Paragraph

Your bank rejected your financing request. But it wasn’t your business that failed the test. It was your first paragraph. Loan Marketing Officers at RHB, Affin, MBSB, Maybank, CIMB — they process dozens of SME inquiries a week. Most get deleted before the second sentence. Not because the business is weak. Because the message reads like a distress call, not a credit conversation.

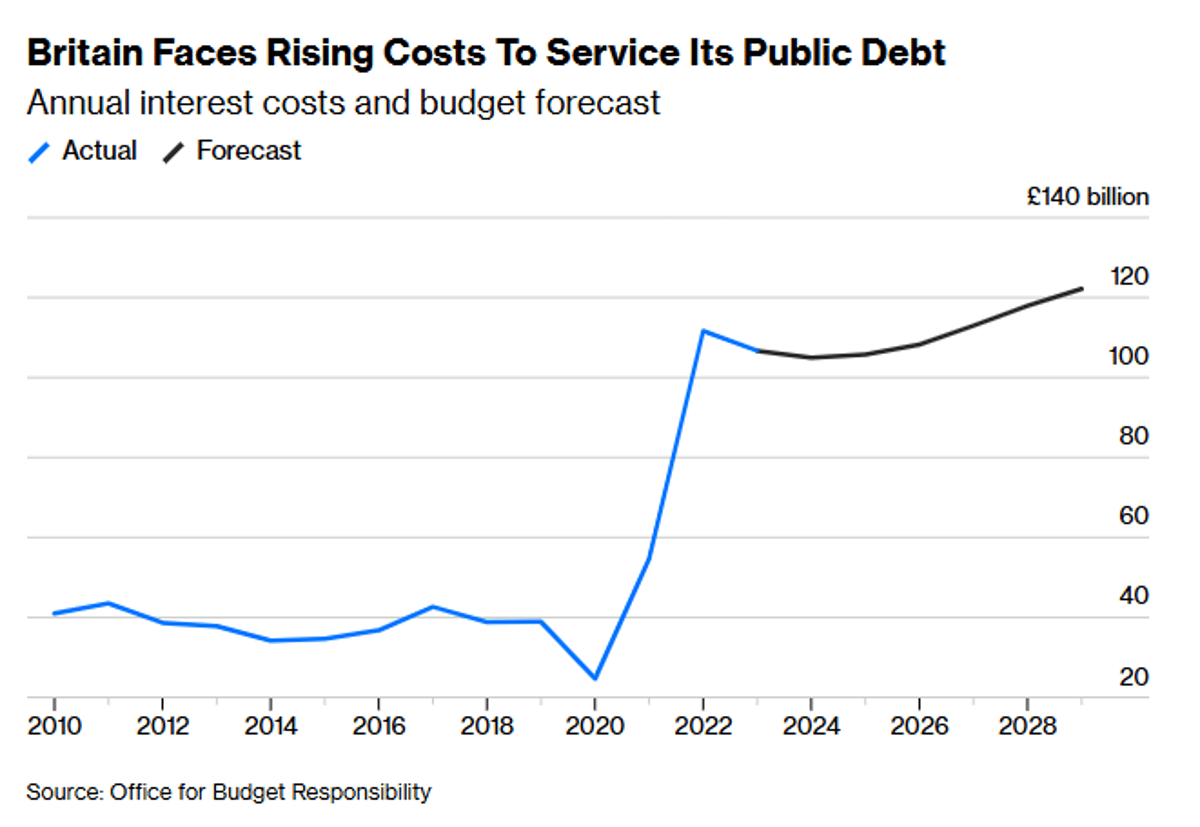

Barclays Proposes Banking Rule Changes to Ease UK Fiscal Strain

Barclays has come up with a plan to adjust banking rules to help ease the UK’s fiscal woes. It’s worth considering, argues @PaulJDavies https://t.co/OQDvfacRPH via @opinion https://t.co/fD5uHJYMXM

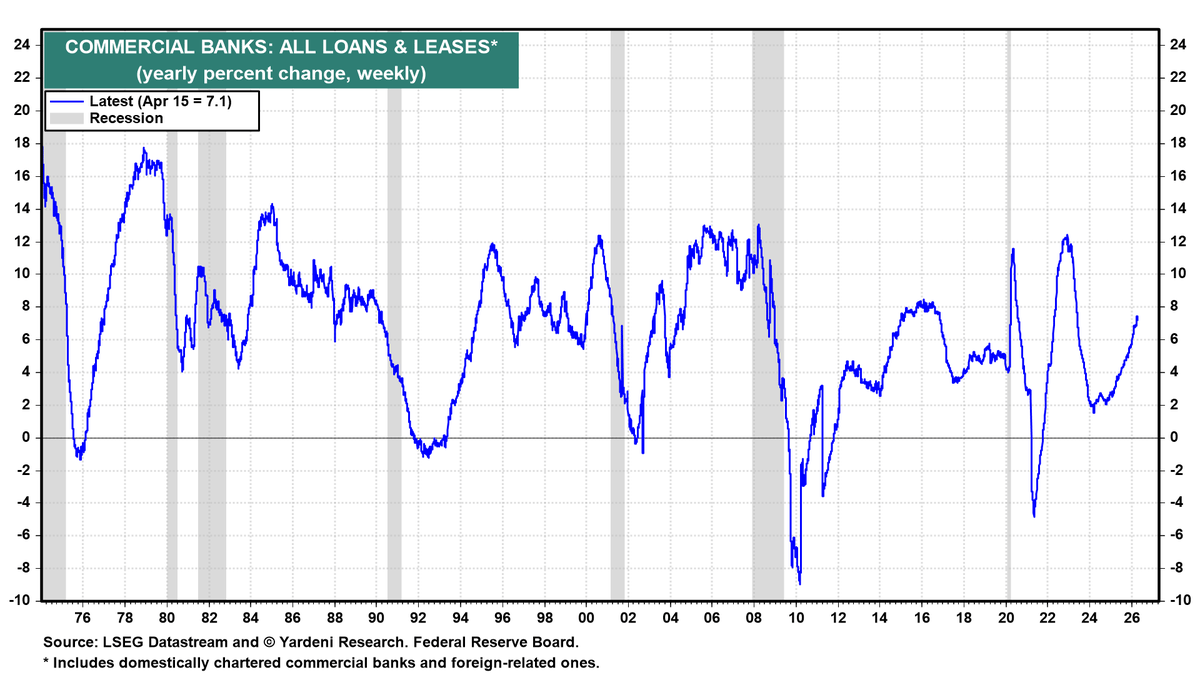

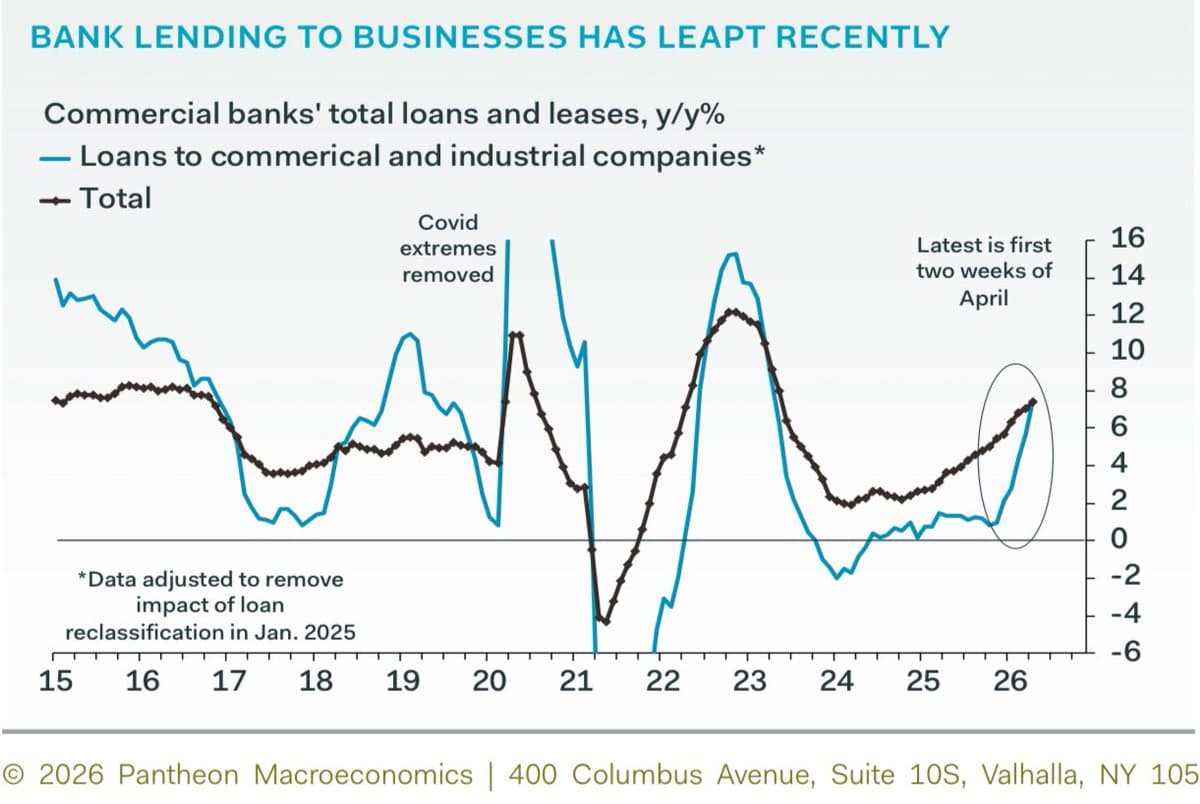

Bank Loans Surge 7.1% YoY, Easing Private Credit Risks

Yardeni Research Chart of the Day (April 26, 2026) Bank loans and leases are growing 7.1% y/y, the fastest pace in ~3 years. Traditional lenders are picking up the slack, which is why private credit stress is unlikely to spill into...

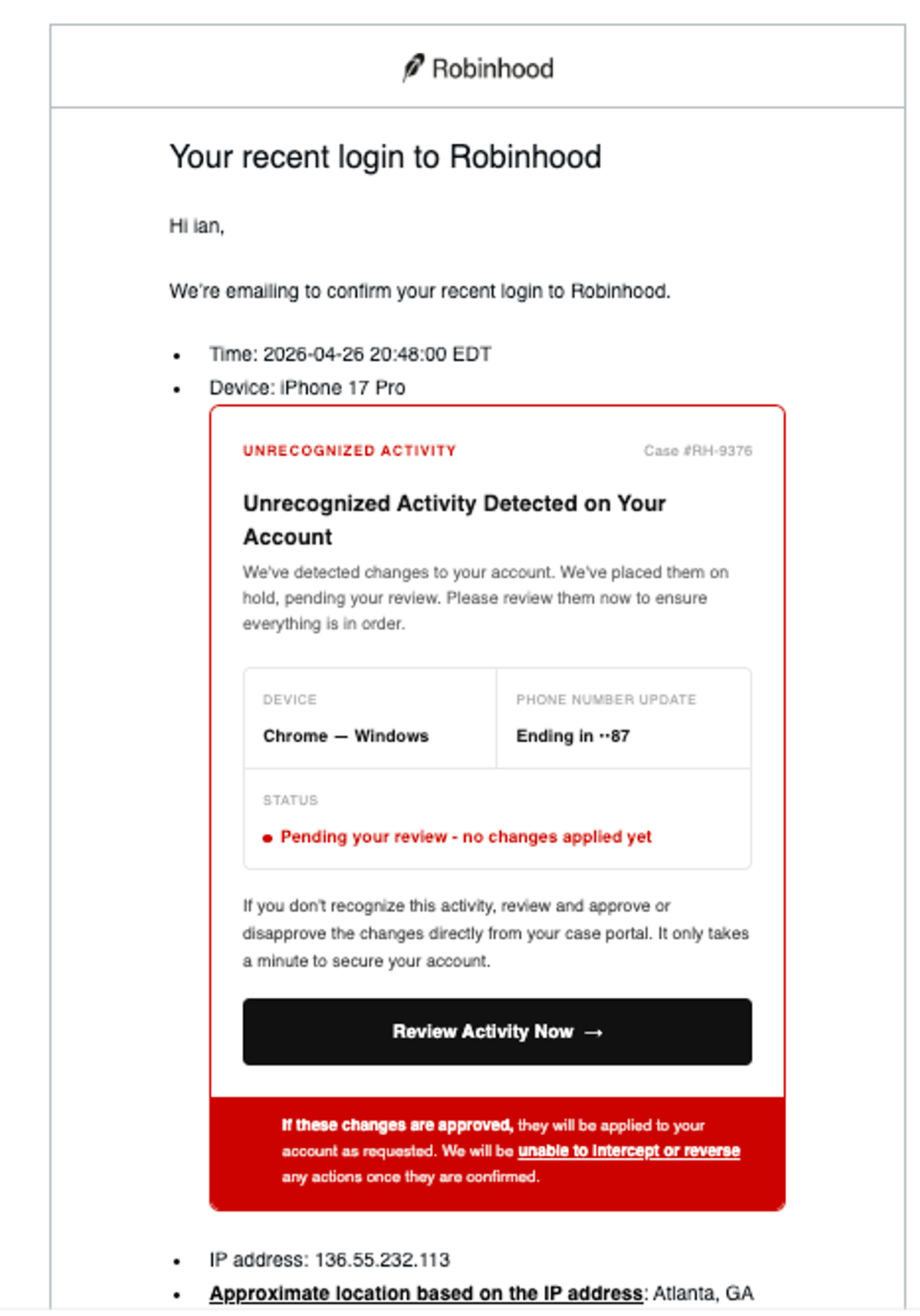

Sophisticated Robinhood Email Spoofing Threats Rise, Stay Vigilant

this looks like an extremely real @RobinhoodApp email but its fake. the email it was sent to was slightly off. most of the links except the big one to reset my account link to RH websites. email comes from noreply@robinhood.com....

Alipay Launches AI Voice Payments for Cars

🇨🇳 Alipay brings mobile #payments to the car: Chinese tech firm Banma Intelligence and #fintech giant @Alipay unveiled a new AI-powered in-car system that allows drivers to make purchases using only their voice at the Beijing International Automotive Exhibition 2026. @finews_asia. https://t.co/S3ihuRsaq4

Anchorage Guarantees Crypto Safety with Federal Charter

Anchorage is a federally chartered bank regulated by the OCC, the first ever chartered to work with crypto. Accounts are segregated, bankruptcy remote, and insured. FTX, Voyager, and Celsius failed because they were not. With Anchorage, you are never a...

Private Credit Turns Shadow Banking Into Retail Product

Private credit now wants retail money: because apparently the lesson from finance was, 'What if we made shadow banking available in family size?' https://t.co/iSwqZWtej1

Banking Is Now Fully Scriptable via Command Line

All banks are now in the command line Think about that for a second Your grandmother's checking account Your mortgage Your savings All accessible via terminal commands We went from marble lobbies to APIs in one generation The friction is gone The gatekeepers are code The future is scriptable Finance...

Deploy AI, Not Just Pilot, to Transform Banking

Pilot programs don’t create value. Deployment does. The banks that operationalize AI will turn investment into impact while others fall behind. Download your free copy of Agentic AI: Powering the Self-Driving Bank: https://t.co/BkPDkgVWre https://t.co/JvZFvOF49a

AI‑Native Banking OS Powers Autonomous Agent Infrastructure

AI-Native Banking OS: What Does That Actually Mean? @backbase April 28 global reveal - Jouk Pleiter + Tim Rutten unveil the architecture for Agentic Banking. Not "digital transformation". Infrastructure purpose-built for autonomous agents, real-time decisioning, and composable services. Register. EMEA/APAC (1:00...

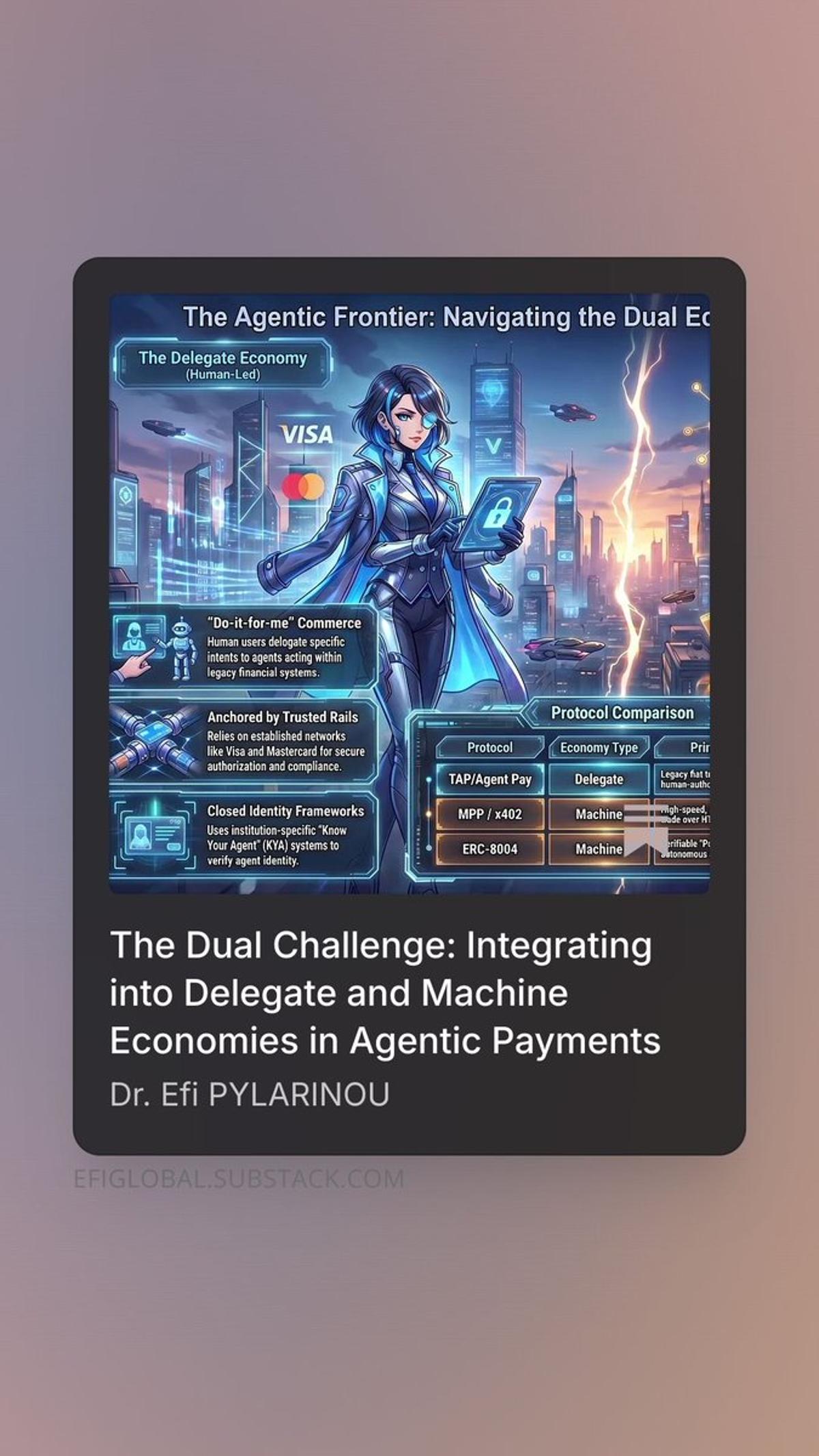

Financial Giants Hedge as Agentic Rails Transform Commerce

Visa, Stripe, Coinbase, JP Morgan - everyone’s hedging their bets as agentic rails reshape commerce. Discover how to integrate into both legacy and machine-to-machine economies in my new article. https://t.co/fWAC0ztm61 https://t.co/JV9vEpMdN6

Revolut's Unified AI Model Boosts Banking Performance

Revolut just moved the IP of banking into a model. Trained on 24 billion banking events in 111 countries. One foundation model replacing six separate ML systems. Credit scoring: +130% Fraud recall: +65% Marketing engagement: +79% The model is the new moat.

Germany Seeks White‑knight Bidders to Block UniCredit Takeover

Germany sounded out potential white knights for Commerzbank earlier this year, underlining its efforts to fend off UniCredit https://t.co/SFoDdMQcTL via @KowalczeKamil https://t.co/jmbx69DPzh

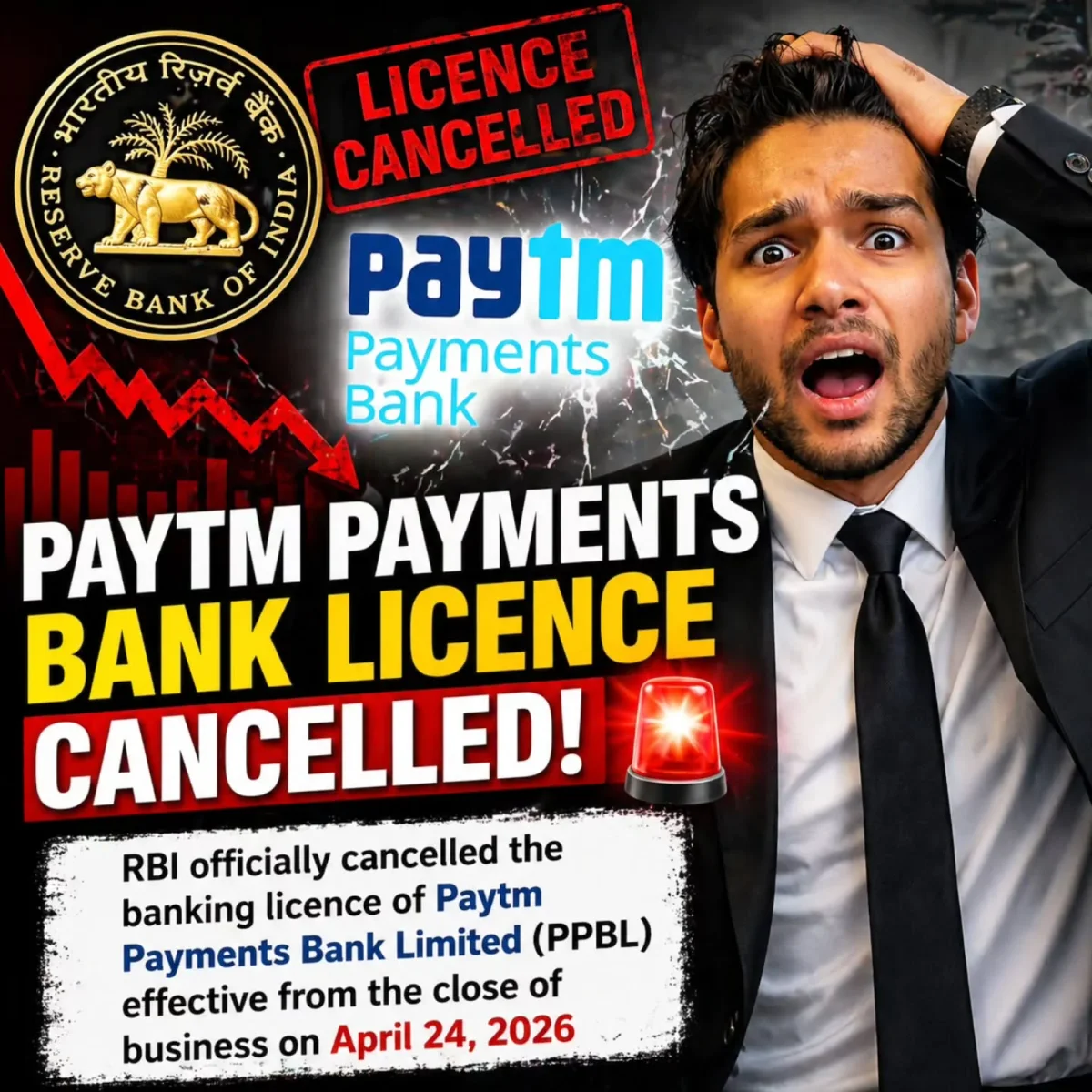

RBI Revokes Paytm Payments Bank Licence Effective April 24

The Reserve Bank of India (RBI) officially cancelled the banking licence of Paytm Payments Bank Limited (PPBL) effective from the close of business on April 24, 2026.

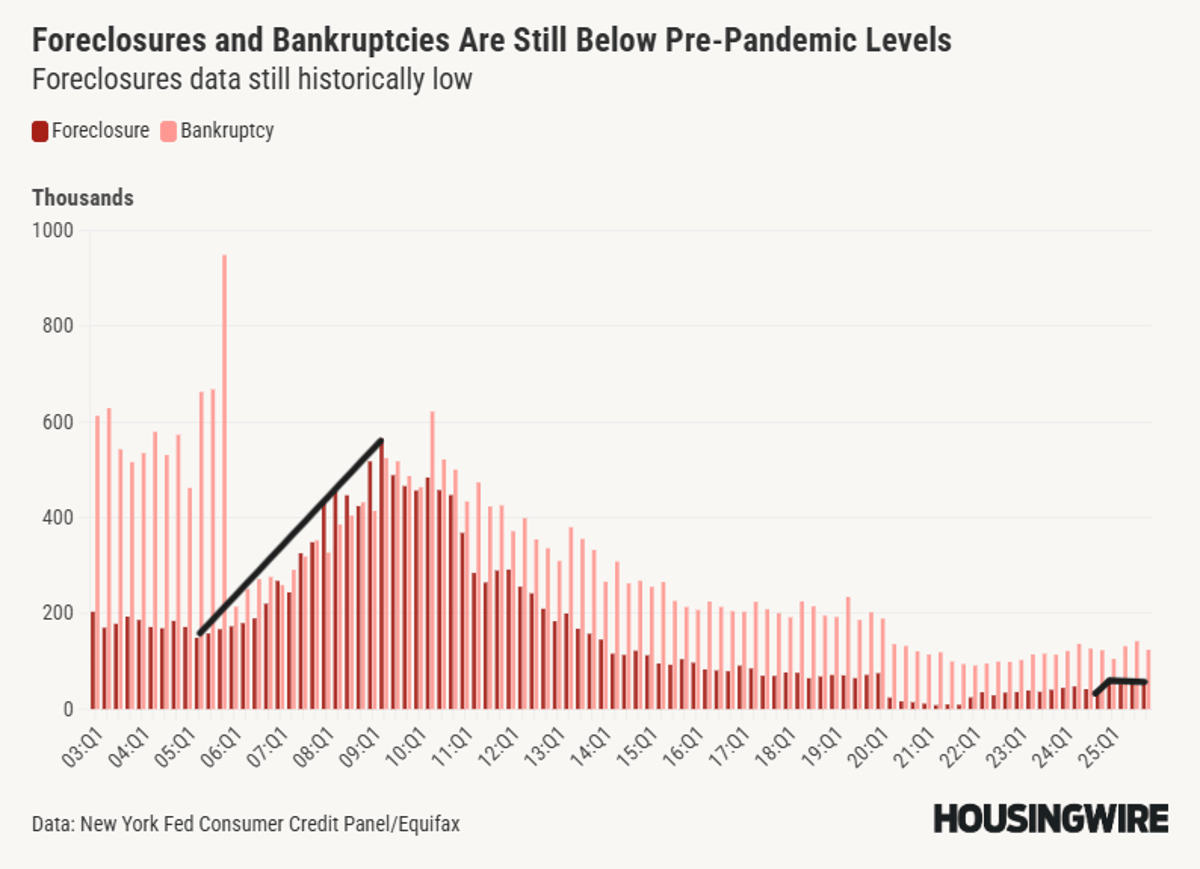

2005 Bankruptcy Reform and 2010 Qualified Mortgage Laws Revolutionized Lending

2005 BK reform law, notice all the BK filings before the law went into effect. Then add the 2010 Qualified Mortgage Law on top. Those two laws changed everything forever https://t.co/2gnt1ETE2e

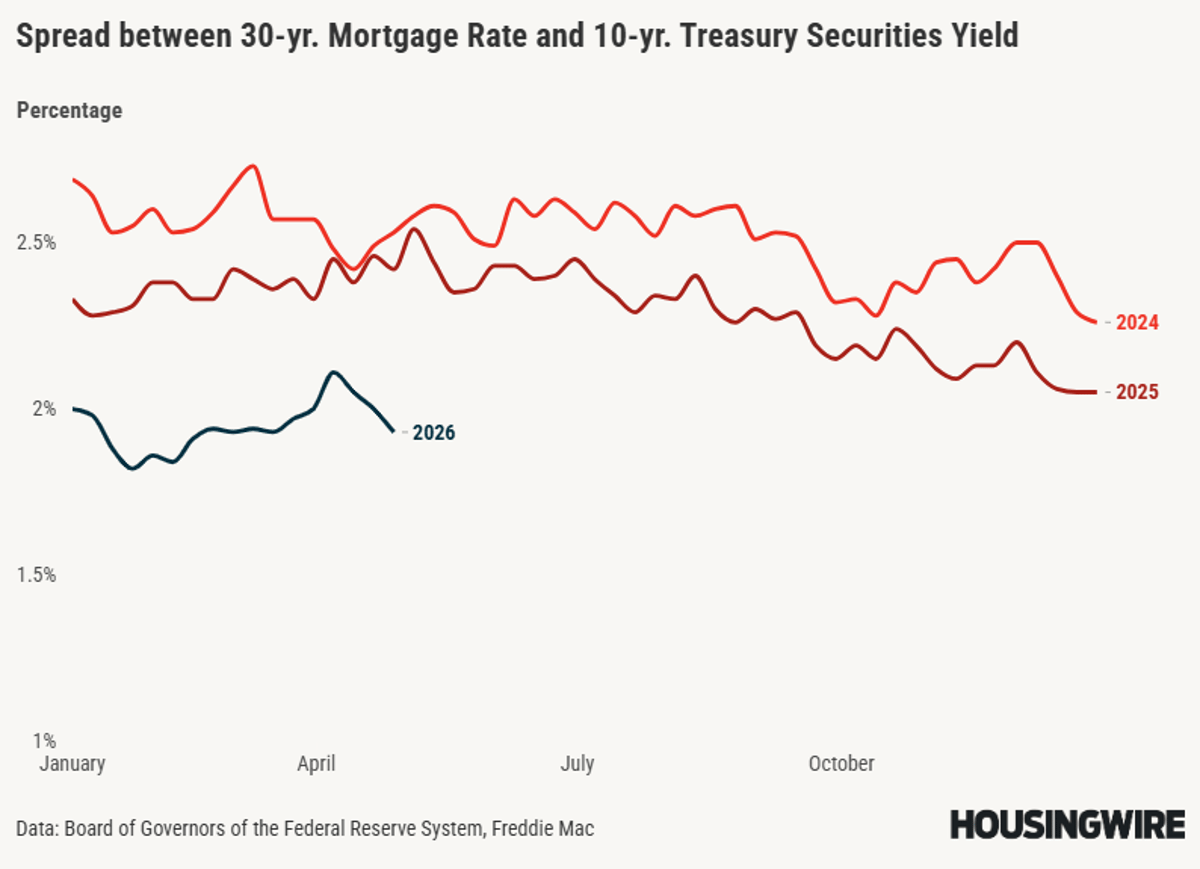

Improved Spread Levels Shave a Percentage Point

If we had the worst mortgage spread levels of 2023, mortgage rates would be 7.50% today, not 6.32%. If we had the worst levels of 2024, mortgage rates would be 7.12% today. If we had the worst levels of 2025, mortgage rates...

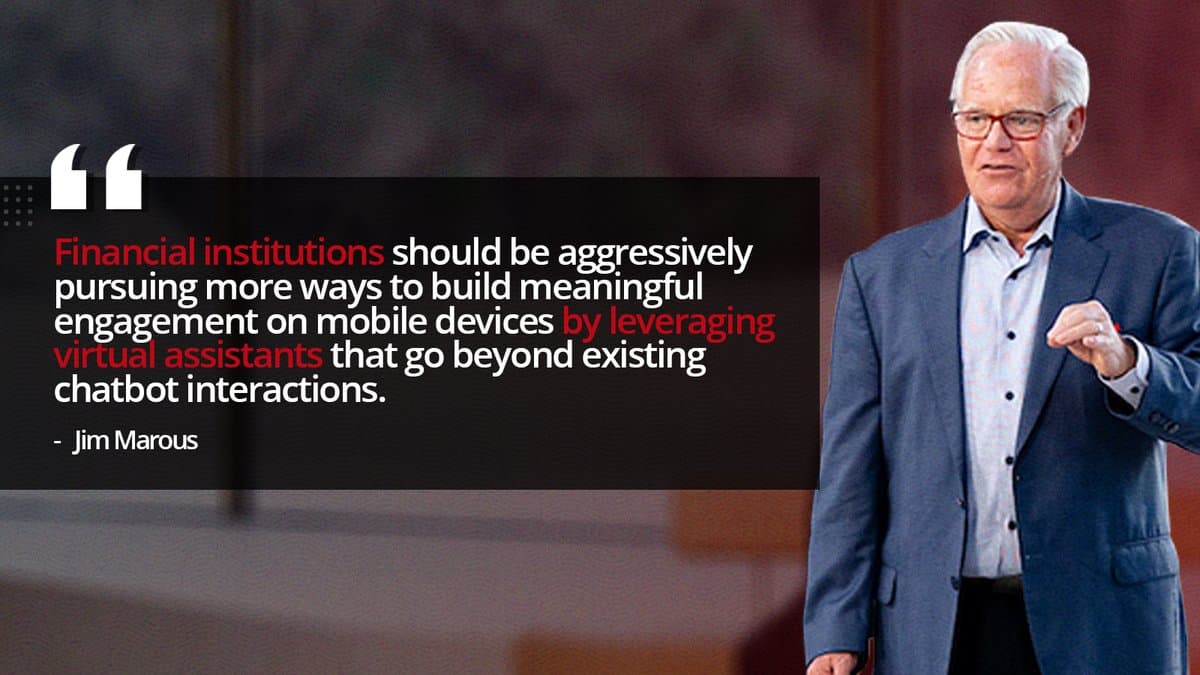

Virtual Assistants Enable Deeper Financial Engagement, Not Just Automation

The opportunity is not just automation. It’s deeper engagement. Virtual assistants can help customers manage money, not just answer questions. https://t.co/dcRagBD5q7

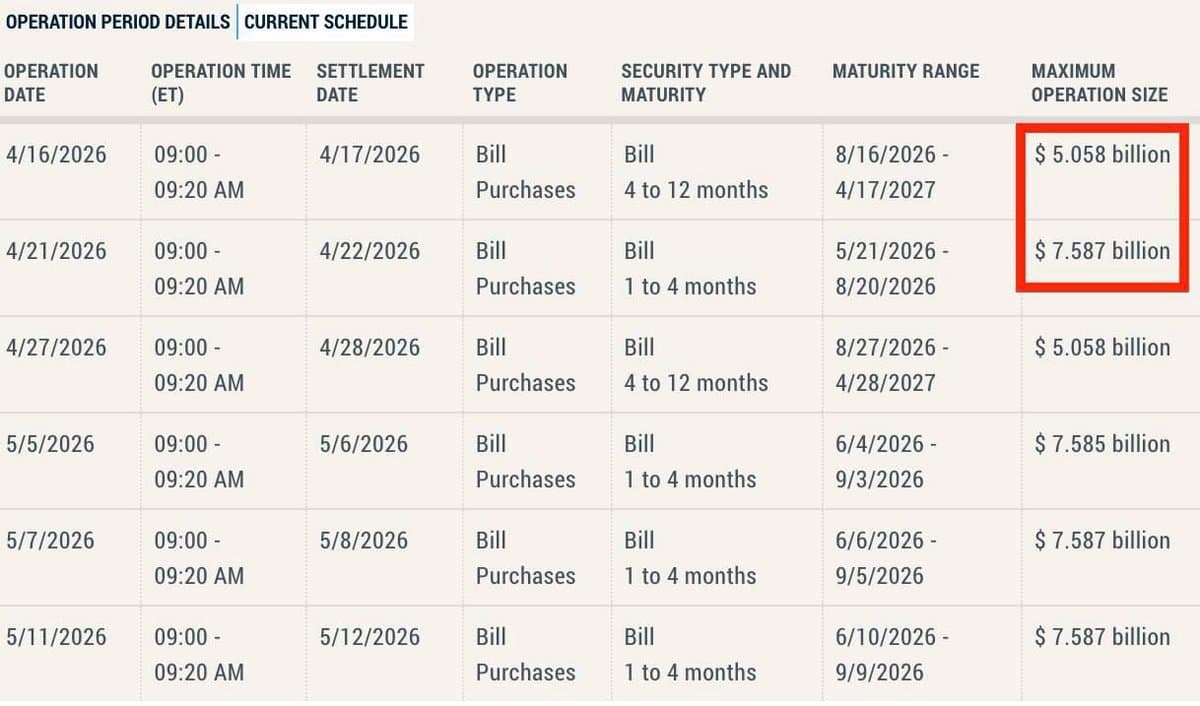

Fed Pumps $17.7 B Liquidity Into Markets This April

MASSIVE The Fed has already injected a total of $12.645 BILLION this month, and another $5 billion is expected to flow in within the next few days. That brings total liquidity injections in April alone to $17.703 billion. https://t.co/d8xIZjDvj4

Alternative Data Powers Digital Lending for the Unbanked

Digital lending platforms have brought millions of previously unbanked people into the formal financial system. To reach these borrowers, many platforms rely on alternative data such as call records, mobile usage patterns, and social network information. https://t.co/QEz3AWRmB6

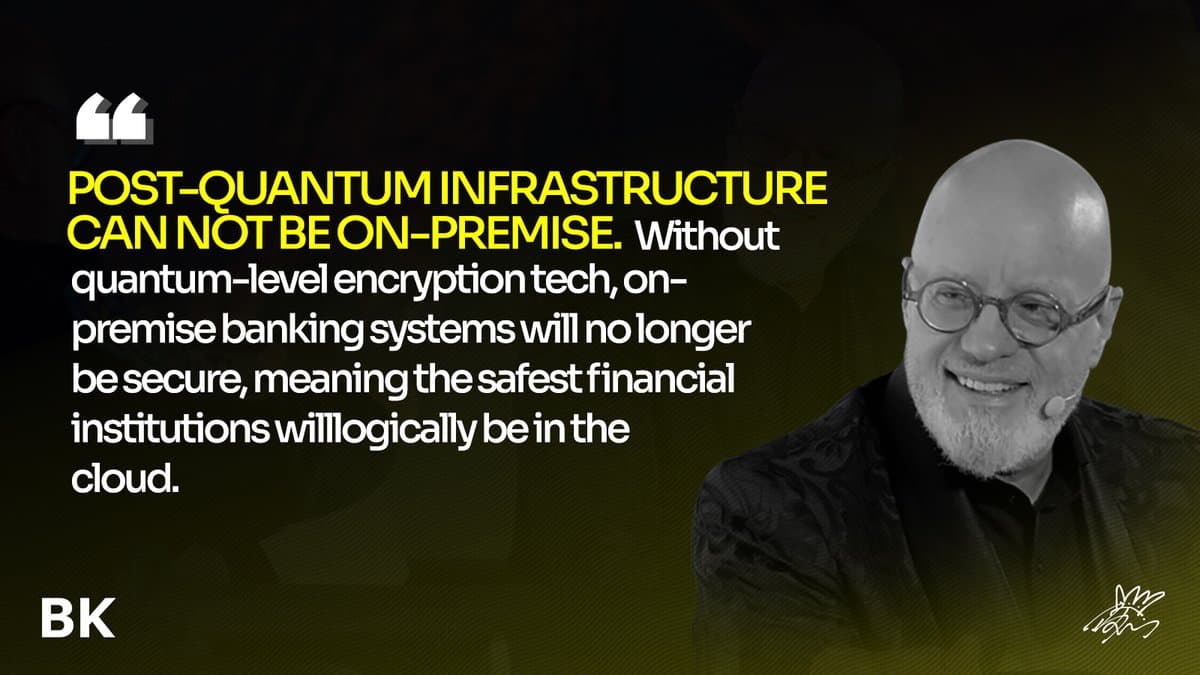

Banking Must Adopt Post‑Quantum Standards, Embrace Cloud

If banking systems cannot evolve to post-quantum standards, they risk becoming structurally insecure. The cloud becomes the logical foundation. https://t.co/4ZvlgernJn

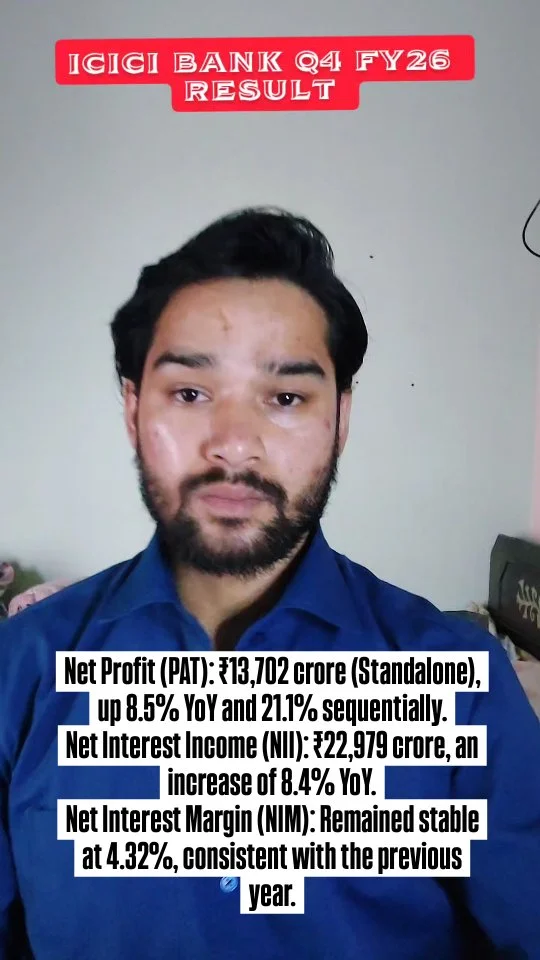

ICICI Bank Q4 Profit Jumps 8.

Icici bank q4 fy26 result. Net Profit (PAT): ₹13,702 crore (Standalone), up 8.5% YoY and 21.1% sequentially. Net Interest Income (NII): ₹22,979 crore, an increase of 8.4% YoY.

Senate Banking Committee Schedules Warsh Fed Chair Vote

The Senate Banking Committee has set a committee vote for Kevin Warsh’s Fed chair nomination on Wednesday https://t.co/l3pMHESk0G

Banks Embrace AI, Yet Execution Stalls Production

96% of banks say they are engaged with agentic AI. Only 19% have anything in production. That gap is not about regulation. It is about execution. In this episode, I break down what is holding the industry back. 👉 Watch the...

Swap Lines Are Loans, Not Gifts, Fueling Dollar Demand

For those new to swap lines due to recent headlines, swap lines are not USD “gifts”, they are USD “loans”. The difference? Loans need to be paid back. And as such create dollar demand. Swap lines...

Five Banking Tech Trends Transforming Financial Services

Five #Banking #Tech Trends Reshaping #FinancialServices https://t.co/21VGN9n6WZ #fintech #AI @SpirosMargaris @ahier @Khulood_Almani @AkwyZ @FinMKTG @efipm @FrRonconi @Hana_ElSayyed

Powell Already Ordered Fed IG Probe, Piro Not Starting New

Also, Powell asked for the Inspector General at the Fed to investigate last July, so Piro is not starting a new investigation there https://t.co/69DrLkUpjT

April 25 Q4 Earnings Radar: Top Indian Stocks

🚨 𝗤𝟰 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗥𝗮𝗱𝗮𝗿: 𝗔𝗽𝗿𝗶𝗹 𝟮𝟱 🔹 𝗔𝘅𝗶𝘀 𝗕𝗮𝗻𝗸 🔹 𝗜𝗗𝗙𝗖 𝗙𝗶𝗿𝘀𝘁 𝗕𝗮𝗻𝗸 🔹 𝗥𝗕𝗟 𝗕𝗮𝗻𝗸 🔹 𝗨𝗖𝗢 𝗕𝗮𝗻𝗸 🔹 𝗦𝗕𝗙𝗖 𝗙𝗶𝗻𝗮𝗻𝗰𝗲 🔹 𝗜𝗻𝗱𝗶𝗮 𝗖𝗲𝗺𝗲𝗻𝘁𝘀 🔹 𝗔𝘂𝘁𝗼𝗺𝗼𝘁𝗶𝘃𝗲 𝗦𝘁𝗮𝗺𝗽𝗶𝗻𝗴𝘀 𝗮𝗻𝗱 𝗔𝘀𝘀𝗲𝗺𝗯𝗹𝗶𝗲𝘀 🔹 𝗠𝗜𝗖 𝗘𝗹𝗲𝗰𝘁𝗿𝗼𝗻𝗶𝗰𝘀 🔹 𝗦𝗲𝗷𝗮𝗹 𝗚𝗹𝗮𝘀𝘀 🔹 𝗦𝗮𝗻𝗴𝗶𝗻𝗶𝘁𝗮 𝗖𝗵𝗲𝗺𝗶𝗰𝗮𝗹𝘀

GOP Banking Chiefs Praise Pirro; White House Warns Case Persists

Both GOP leaders of the banking committees, which oversee the Fed, have issued statements welcoming Pirro's decision. But so far, we have heard nothing from Tillis. Meanwhile, the White House says the case "is not necessarily dropped."

UAE USD Swap Lines May Fund China Investments

So…will the USD swap lines Bessent is going to give UAE going to finance the UAE’s newly-signed investments in China? Or are the USD swap lines so UAE doesn’t have to sell USTs to make these investments in China? Or do the...

South Africa to Mandate Crypto Disclosures, Private Key Access

South Africa’s National Treasury has proposed draft rules that would require crypto holders to declare assets above a certain threshold and, if requested, provide private keys to authorities. Failure to comply could result in fines and prison sentences of up...

Amex Hikes Platinum Fee, Customers Stay; Broader Fee Surge Ahead

Amex Raised Platinum’s Fee, Customers Didn’t Cancel — Higher Annual Charges Coming Across Cards - View from the Wing https://t.co/znitJsCq1M

Wealth Firms Lag Culture, Talent Despite AI Push

#PrivateBanking tech struggles with traditional attitudes and talent shortage: Although wealth managers have moved fast to introduce #AI and data analysis, many can struggle to build an appropriate #culture to foster high-level #innovation. @YuriBender, @FT_PWM: https://t.co/ocChsW4E3q #WealthManagement #WealthTech #AItransformation

Financial AI Must Predict Crises, Not Just Automate

Look Financial institutions are sitting on mountains of data But they're using AI like a calculator This is the problem: • AI reads reports humans already wrote • AI summarizes data humans already know • AI automates tasks humans already perfected We're not harnessing AI We're domesticating it Real...

Instant Account Opening Drives Deposit Growth

Before you invest in a new branch, invest in your back office. Make account opening instant. Then layer in digital marketing. That’s how you accelerate deposit growth. https://t.co/l6qOxJxVWO

DOJ Ends Fed Probe, Citing No Viable Options

DOJ is dropping its probe into the Fed and Chair Jerome Powell because there was really no other winning scenario here, as I laid out last week: https://t.co/K1glC171IN

Mortgage Health Holds, but Late‑stage Delinquencies Rise

https://mortgagetech.ice.com/resources/data-reports/first-look-at-march-2026-mortgage-data "While overall mortgage performance remains healthy for most borrowers, the continued buildup in late-stage delinquencies and foreclosure pipelines remains worth watching.”

Record Mortgage Renewals Spur Higher Rates, Dampening Spring Market

Will Higher Fixed Mortgage Rates Slow Down An Already Slow Spring Real Estate Market? PROBABLY Thing is when you're coming off ridiculously low 2025 Home Sales numbers in BC & Ontario: a very small increase in resales is inevitable But very bad...

TradFi and DeFi Converge via Blockchain Tokenization Alliance

Ondo Finance, Clearstream, 360X Form Alliance To Merge TradFi with Blockchain-Based Tokenization The line between DeFi and TradFi is getting more blurred. Public, permissionless blockchains for execution AND settlement within regulated systems https://t.co/j6jUqwrSWn

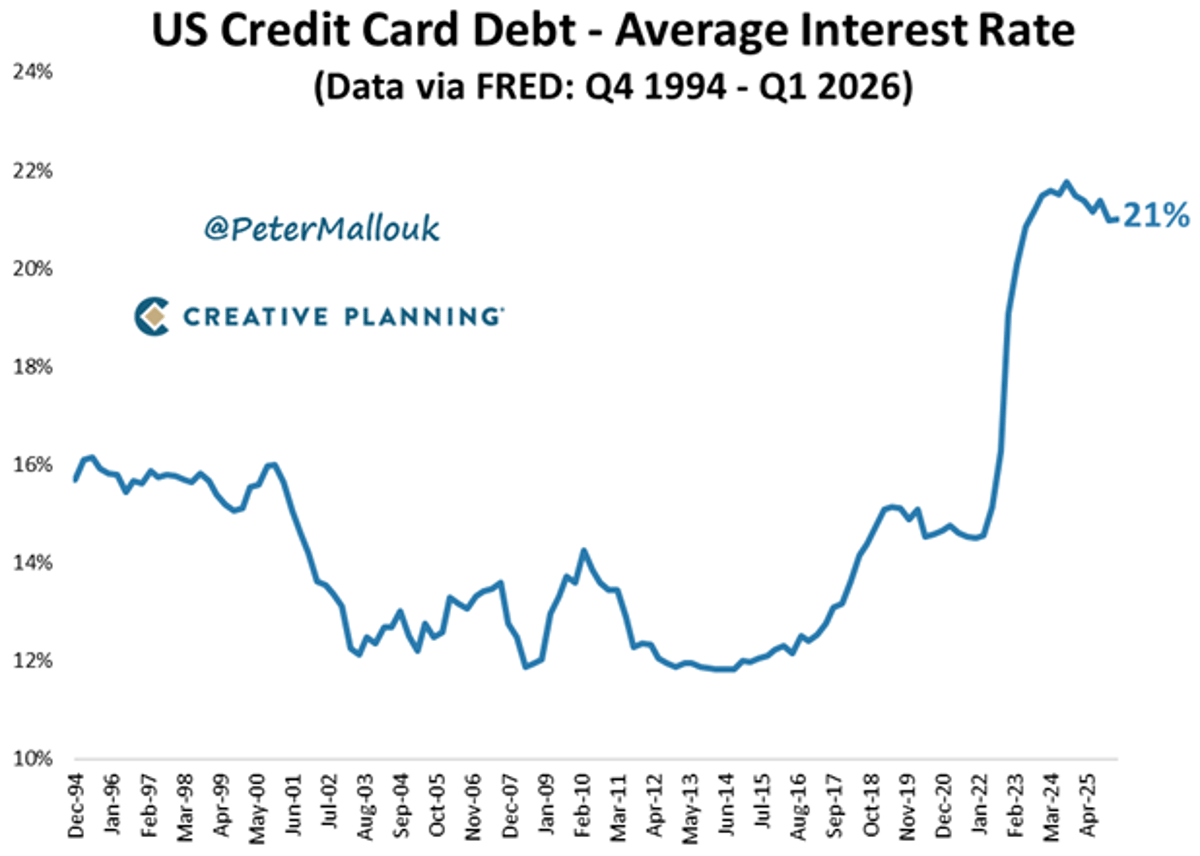

US Credit Card Debt Hits $1.3T, 21% Interest

There is now a record $1.3 trillion in total credit card debt in the US - at an average interest rate of 21%. This is the #1 wealth killer in America by a landslide. https://t.co/WIIhT0vYRO

AI Moves From Pilot to Core in Asian Finance

From Bangkok to the Boardroom: AI in Finance Has Left the Lab – At @Money2020 Asia 2026 in #Bangkok, the shift from experimentation to execution was evident. Leading institutions are no longer piloting AI – they are scaling it across operations,...

Three Mandates to Accelerate Your Bank's AI Transformation

If your AI strategy is still on the innovation roadmap, you are already behind. In this episode, I share 3 leadership mandates to move toward a self driving bank. 👉 Watch the latest episode: https://t.co/P54LuzdywH https://t.co/KaTfkodOPt

Morgan Stanley Unveils Regulated Stablecoin Reserves Fund

NEW: Morgan Stanley launches "Stablecoin Reserves Portfolio," a government money market fund offering stablecoin issuers a regulated, low-risk place to hold reserves https://t.co/kx3yYKDt3X

Russia's Central Bank Lowers Rate To

MOSCOW, April 24 (Reuters) - The Russian central bank reduced its key rate by 50 basis points to 14.5% on Friday, as expected by analysts, despite pressure from businesses to cut faster in order to boost the economy, which contracted...

SNB Free to Adjust Rates and Intervene, Says Schlegel

Schlegel says a vigilant SNB is unrestricted on interest rates and interventions https://t.co/T29eQBLJeq via @bbenrath https://t.co/d7Ln9mGd5W

Fed's Crypto Master Account Sparks Bank Opposition, Benefits Competition

New on the not-a-newsletter... Skinny is Good https://t.co/bujchlQubN The Fed has given a master account to a crypto exchange. The banks are mad. I understand why - but they are wrong. It is better for everyone if banks face real competition....

MUFG Appoints Saumitra Shrivastava as Asia Project Finance Head

MUFG has hired Saumitra Shrivastava as head of Asia project finance based in Singapore, according to sources https://t.co/gA6CQ3OaxK

Citi Wealth Launches AI Advisor Powered by Google Gemini

.@Citigroup's wealth unit launches Citi Sky, a Google-powered wealth advisor https://t.co/IwwDU1eovF @GoogleCloud's partnership with Citigroup is starting to pay off as Citi Wealth, a unit of Citibank, launched an AI agent that utilized the Gemini Enterprise Agent Platform and…

AI Boom Stalls as Capital and Power Limits Surface

Oracle is running into the financial limits of the AI boom. Massive data center projects tied to AI are becoming harder to finance, as banks reach exposure limits and infrastructure costs surge. It reveals a deeper constraint. AI growth is not just...

Banks Fill Private Credit Gap as Loans Surge 7.4%

Commercial and industrial loans made by banks are up 7.4% year-over-year, the biggest jump in three years: @PantheonMacro While this can indicate a pickup in capex spending, this time it shows how banks are taking the place of private credit...

Regulator Confused About Polymarket’s International Scope

Remarkable that the country's top derivatives regulator either doesn't know (or is deliberately obfuscating) the difference between the two Polymarkets....