🎯 Today's Venture Capital Pulse

Anthropic files confidential IPO paperwork as it expands Claude Partner Network

Anthropic has confidentially filed for an initial public offering, marking a concrete step toward a public market debut. The filing follows a recent $100 million investment to grow its Claude Partner Network, positioning the AI startup alongside other high‑profile IPO candidates. The move underscores a broader wave of AI‑centric listings.

Also developing:

By the numbers: Runway raises $315M Series E

🚀 Top Venture Capital Headlines

Tripo AI Raises Nearly $200M in Financing for AI 3D and World Model Tech

Tripo AI, a global artificial intelligence company building AI 3D foundation models and world models, today announced the completion of its Series A+ and... The post Tripo AI raises nearly $200M in financing for AI 3D and world model tech appeared first on GamesBeat.

GamesBeat

Sam Altman Is Quietly Backing a Stealth Startup That's Building Software for Robots and Cars

Sam Altman. Anna Moneymaker/Getty Images Sam Altman and Khosla Ventures are backing a stealth startup called Alfred, documents show. The startup was founded by a former Tesla designer and an ex-Meta Reality Labs engineer. Alfred is raising at a $40 million valuation to turbocharge manufacturing, its founder said. OpenAI CEO Sam Altman is backing a stealthy physical AI startup run by former Tesla and Meta employees, in the latest sign that investors are rushing into robotics. The startup, called Alfred, is also being funded by Khosla Ventures, SV Angel, Chapter One, and others, according to internal documents reviewed by Business Insider. The startup is aiming to raise at a $40 million valuation, co-founder Ankit Ukil told Business Insider. Aflred is run by Ukil, a former Tesla designer, and Dömötör Gulyas, a former engineer at Meta Reality Labs. Alfred is emerging as investors pour money into physical AI, a category built around bringing AI to machines that move through the real world — like robots. In April alone, physical AI startups raised around $5.3 billion in VC funding, according to Crunchbase data. Big Tech companies are also flocking to place their bets in the robotics arms race. On Sunday at Nvidia GTC Taipei, the company announced a standard humanoid robot blueprint for academic researchers, expected to be available in late 2026. Over the weekend, Altman took to X to declare that robotics is OpenAI's next frontier. "In the short term, we are focused on robots to support skilled workers to build our future infrastructure; in the long term, we imagine everyone having a personal robot doing anything they need," Altman wrote on X. Altman is also backing startups in the space alongside OpenAI's bet. He invested in Alfred through his venture capital firm, Hydrazine Capital. Ukil said he and Altman initially bonded over their love of cars. "He's a big car guy," he said. "I met Sam a while ago, and he largely believed in me before the company existed." Altman was filmed driving an ultra-rare $5 million Koenigsegg Rivera in Napa in 2024, Business Insider previously reported. Altman and OpenAI did not respond to requests for comment. The rest of Alfred's team includes designers and engineers from Tesla, Ford, and Honda, according to the documents. The startup was founded 9 months ago, according to Ukil's LinkedIn profile, and is based in Hawthorne, California, opposite the SpaceX factory where the Falcon rockets are made. The founders are pitching investors on a software platform that helps engineers build machines faster. The ultimate goal of Alfred is for their product to turbocharge the manufacturing process by shrinking research and development timelines. That way, engineers can skip gruntwork and focus on doing things like adding cool new features to cars, such as those often seen in the latest Chinese electric vehicles, Ankit said. Ukit told Business Insider that Alfred's flagship platform is under development, and that the startup is in "active conversations" with unspecified automakers, defense, and robotics companies. Over the past 15 years, Altman has made more than 170 investments, according to PitchBook data. These include venture fund Hydrazine Capital, through which he invested in Alfred. Altman has no equity in OpenAI, but his venture investments, including stakes in Stripe, Reddit, and Helion Energy, have helped make him a billionaire. Read the original article on Business Insider

Business Insider — Markets

Swiss Dental Startup vVardis Is Preparing for US IPO

vVardis Holding AG, a Swiss dental startup, is working with banks for a US initial public offering that could come this year, according to people familiar with the matter.

Bloomberg – Markets

Venture Capital’s Most Underrated Skill: Knowing when NOT to Invest

An article by Husameddin AlMadani, angel investor and aviator There is a moment before every flight that matters more than takeoff itself. It is not dramatic or cinematic. From the outside, it often looks like nothing at all. A pilot reviews the conditions, studies the route, checks the aircraft, evaluates the weather, considers alternatives, and then makes a decision: go or no-go. That decision is deceptively simple to underestimate because nothing visibly happens. If the answer is “go”, the flight proceeds. If the answer is “no-go”, the aircraft stays on the ground, the plan changes, and life moves on. Over time, I have come to believe that this moment — the disciplined willingness to decide whether conditions truly justify action — is one of the most important lessons that flying can offer. For me, it has also become one of the most useful mental models in investing. At 2Pi Ventures, we spend a great deal of time evaluating opportunities that appear promising on the surface: capable founders, large markets, compelling narratives, exciting technologies, and the kind of momentum that naturally attracts conviction. In venture capital, as in aviation, there is always pressure to move. Opportunities appear time-sensitive. Markets reward decisiveness. Others may already be in motion. Often, the greatest temptation is not fear, but momentum itself. But momentum is not judgement. The conditions do not care what you want That is where the idea of go/no-go becomes powerful. In flying, a sound decision is not defined by optimism. It is defined by readiness. You may want the flight to happen. The destination may matter. The aircraft may be technically capable. But if the conditions are wrong — if the weather is deteriorating, visibility is poor, reserves are too tight, or your own readiness is compromised — the right decision may simply be not to depart. What makes this difficult is that “no-go” can feel like a loss in the moment. It can feel overly cautious or like a lost opportunity. In reality, it is often a sign of maturity. A pilot who cannot say no should not be impressed by his willingness to say yes. The same is true in investing. One of the most underrated disciplines in venture capital is the ability to decline an opportunity not because it lacks promise, but because the conditions for participation are not right. A company can be exciting and still not be investable for us. A founder can be talented and still not be ready. A market can be large and still be premature. A trend can be real and still be overheated. The venture world celebrates conviction, and rightly so. But conviction without discipline is not a strength — it is a liability. The hardest investment decisions are not always about identifying what could work. More often, they are about recognising whether the timing, structure, execution risk, and underlying fundamentals truly justify action now. That is a go/no-go decision. The easiest lie is the one you tell yourself In both aviation and investing, there is a subtle but dangerous habit of rationalisation. Once we become attached to a desired outcome, almost any warning sign can be reframed as manageable. In venture capital, customer concentration is called “focus.” Weak defensibility becomes “speed”. Poor unit economics become “temporary”. Execution risk becomes “ambition”. This phase is where discipline matters most — not after the decision, but before it. Flying teaches you to respect conditions that aren't concerned about your preferences. Weather does not respond to enthusiasm. A headwind does not weaken because the destination matters. Visibility does not improve because you are in a hurry. Reality remains reality. The question is whether you are willing to see it clearly before committing yourself to it. Interest is not the same as readiness That mindset has shaped the way I think about investing. At 2Pi Ventures, one of the most important distinctions we make is between interest and readiness. We can be interested in a business and still decide not to invest. We can admire a founder and still conclude that the timing is not right. We can believe in a category and still decide that the current setup does not justify deployment. That is not hesitation or lack of vision. It is a refusal to confuse possibility with preparedness. This matters even more in today’s venture environment. Across global and regional markets, capital has become more selective, growth assumptions are being tested, and investors are under greater pressure to separate durable businesses from momentum-driven narratives. In markets such as MENA, where cycles can shift quickly and capital conditions can tighten without warning, judgment matters even more. The ability to distinguish between genuine readiness and excitement disguised as readiness is becoming a defining advantage. Every “go” comes with consequences In the cockpit, a go/no-go decision is not about fear. It is about responsibility. Investing should be no different. Once an aircraft is airborne, the nature of responsibility changes. You are no longer evaluating possibilities — you are managing consequences. The same is true once capital is deployed. At that point, investors are no longer observing a narrative from a distance. They become part of the reality of execution, governance, support, and outcomes. That is why the threshold for “go” matters so much. The quality of the decision shapes everything that follows. None of this means waiting for perfect conditions. Neither flying nor investing allows for certainty. If we demanded complete visibility before acting, we would be grounded and unable to build anything meaningful. The goal is not to eliminate uncertainty. It is to understand which risks are acceptable, which are manageable, and which are simply being ignored. That distinction is where judgement lives. Strong decision-makers are not seduced by motion Over time, I have come to believe that strong investors, strong operators, and strong pilots share one important trait: they do not let themselves be seduced by motion. They understand that activity is not the same as progress. They know that saying “not yet” can be just as wise as saying “let’s go.” And they recognise that walking away from a marginal decision often preserves their ability to make a better one later. There is also humility in this approach. A no-go decision requires accepting that desire does not override conditions. It demands resistance to ego, urgency, and social pressure. In that sense, no-go decisions are often less about caution than about self-command. Some of the best decisions in both flying and investing leave little visible trace: a flight avoided, a term sheet withheld, a story dismissed. These moments rarely make headlines. But they shape outcomes. Sometimes restraint is the real conviction Flying has reinforced for me that we do not prove our judgement when conditions are easy. It is proven in the moments when action is possible, attractive, and defensible — and restraint remains the better choice. That is as true in the air as it is in venture capital. At 2Pi Ventures, we are in the business of backing ambitious founders and bold ideas. That requires optimism. But real optimism is not blind. It is informed, structured, and grounded in reality. And occasionally, the most disciplined way to protect long-term conviction is to make the hardest short-term decision of all: no-go.

Wamda

Northzone Brings on Firstminute Investor to Support AI Ventures

Investment group Northzone has appointed Sam Endacott as its latest London-based partner who will focus on applied and physical AI. Endacott joins the firm from Mistral and Wayve backer Firstminute Capital and will focus on early-stage investments from seed to Series B. “I am thrilled to join Northzone as a Partner and continue supporting the […] The post Northzone brings on Firstminute investor to support AI ventures appeared first on UKTN.

UKTN â People

💰 Venture Capital Fundraising

Ryan Secures $400M Funding to Challenge Big Four in Europe

US tax adviser Ryan has secured a $400 million investment to expand its European operations and compete with the Big Four accounting firms. The deal, announced on June 1, 2026, marks a significant capital raise for the firm as it seeks to broaden its tax advisory services across the continent.

Runway Raises $315M in Series E Round Led by General Atlantic, AMD Ventures and Nvidia

Runway, the Nvidia‑backed AI startup, closed a $315 million Series E financing round with investors General Atlantic, AMD Ventures and Nvidia, lifting its valuation to $5.3 billion. The new capital will fund the company’s expansion, including a planned $200 million investment in a London hub by 2028.

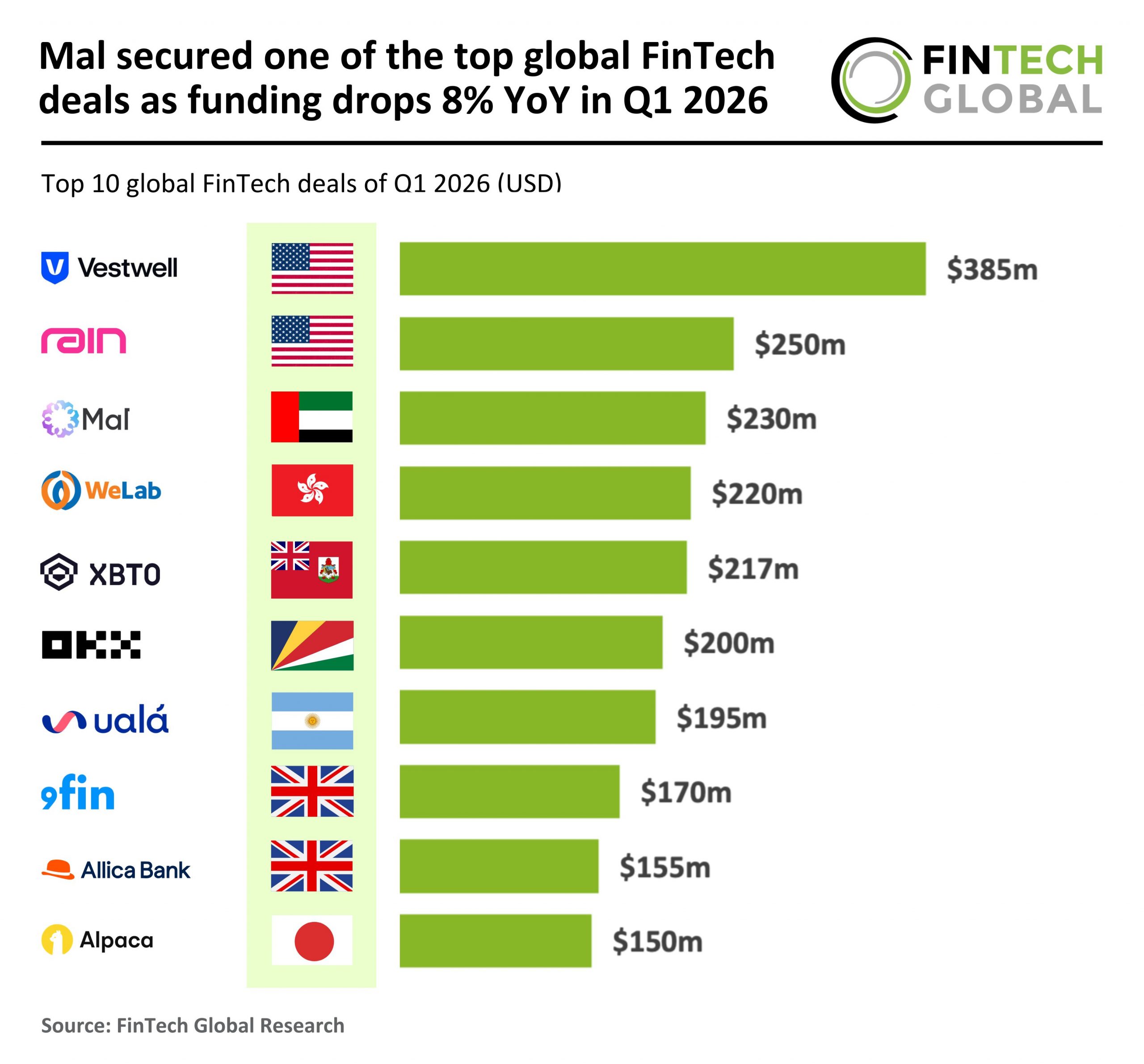

Mal Raises $230M Seed Round Led by BlueFive Capital

Abu Dhabi‑based AI‑native Islamic digital finance platform Mal announced a $230 million seed funding round, led by asset manager BlueFive Capital. The capital will be used to accelerate product development, licensing and go‑to‑market expansion across the Middle East and Asia. The round marks one of the top global FinTech deals in Q1 2026.

💬 Top Venture Capital Social Posts

Tweet by @Greg_ip

Or Bernie Sanders could become president and then just demand the companies hand over a share of their equity. Seems to work.

Thread by @Schrep

Today we're announcing Gigascale Capital's $250M first institutional fund to back early-stage founders rebuilding the physical economy. When we started, the thesis sounded non-obvious: hardware and infrastructure could produce venture-scale companies again. 3 years later, we're seeing it work. There's a revolution in hardware and infrastructure at the same time demand is rising from data centers, onshoring, electrification, and industrial growth.

The Best Founders I've Backed over the Years Didn't Wait for the Right Moment to Start Building. They Were Already Moving. I Discussed with Jen Holmstrom on What We Can Do About that as a Partnership… | Hans Tung

The best founders I've backed over the years didn't wait for the right moment to start building. They were already moving. I discussed with Jen Holmstrom on what we can do about that as a partnership back in 2020. The 2026 Notable Capital NextGen Fellowship class reflects that (and more). These are undergraduate and graduate students spending the summer interning at companies like OpenAI, Vercel, Databricks, and Handshake, or building their own companies while still in school. The fellowship gives all of them a shared structure: weekly sessions with founders and investors diving deep into company-building, and a Demo Day where they pitch an original company idea to early-stage investors — I’m excited to see what they’ve built as one of the judges. This summer's esteemed NextGen Fellowship speakers include: Paul Klein IV of Browserbase , Sahaj Garg of Wispr Flow , Alfred Wahlforss of Listen Labs , Phoebe Gates of Phia , and Tom Occhino of Vercel . NextGen alumni have gone on to raise from leading VCs, join Y Combinator, and land in Forbes 30 Under 30. What stands out about this cohort is how many fellows are already building. That shift is something I've noticed accelerating over the last few years. AI has lowered the cost of starting, and the students coming up now know it. Congratulations to the 2026 class. Meet the fellows: notablecap.com/next-gen