Housing Scarcity Drove Rate Hikes in Early 2021

Dallas and the country, from 2020 to early 2022, didn't have enough housing listings, too many people chasing too few homes. Hence, the entire team higher rates concept in February of 2021 https://t.co/KU1fXBbATF

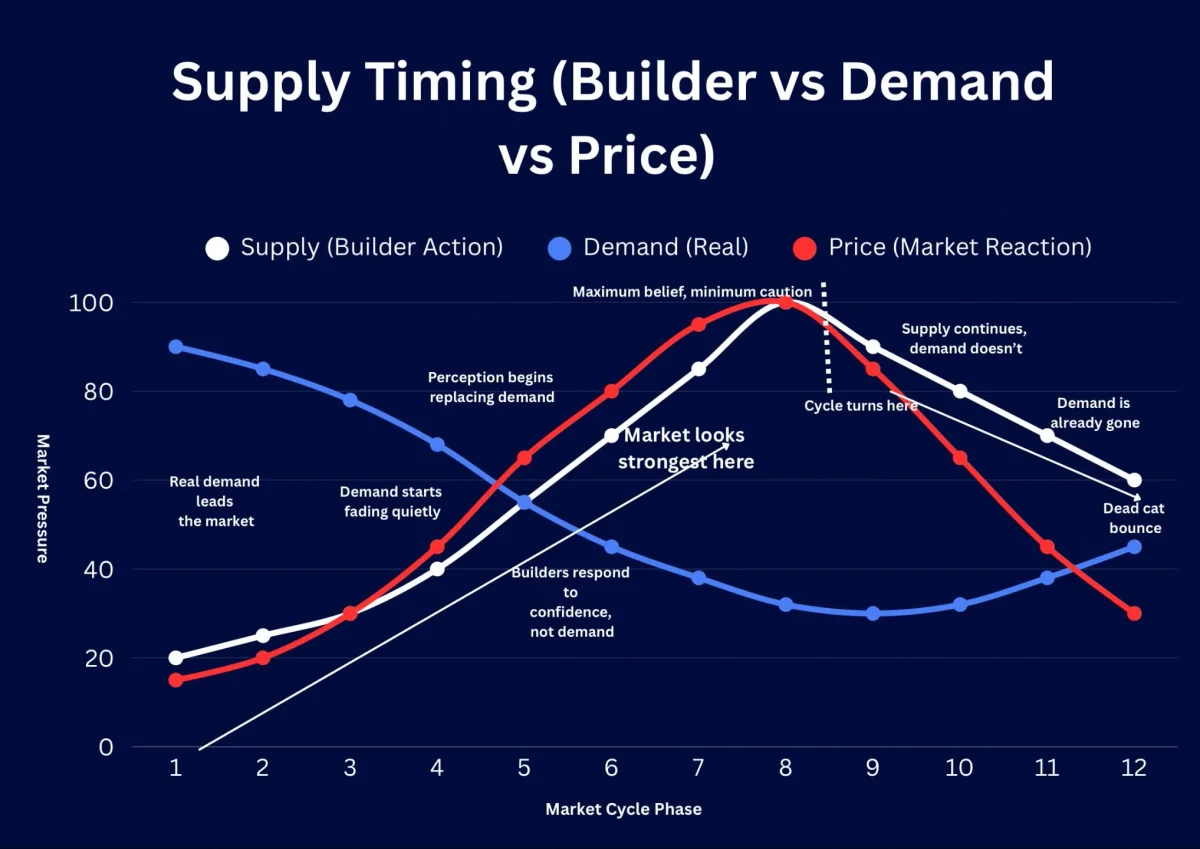

Supply Surges when Confidence Peaks, Not Real Demand

Supply enters when the market feels safest. That’s exactly when risk is highest. Most people think: Builders launch when demand is strong Reality? Builders launch when confidence is highest Not when demand is real. Let’s break this down 👇 Phase 1–3: Real demand leads the market At...

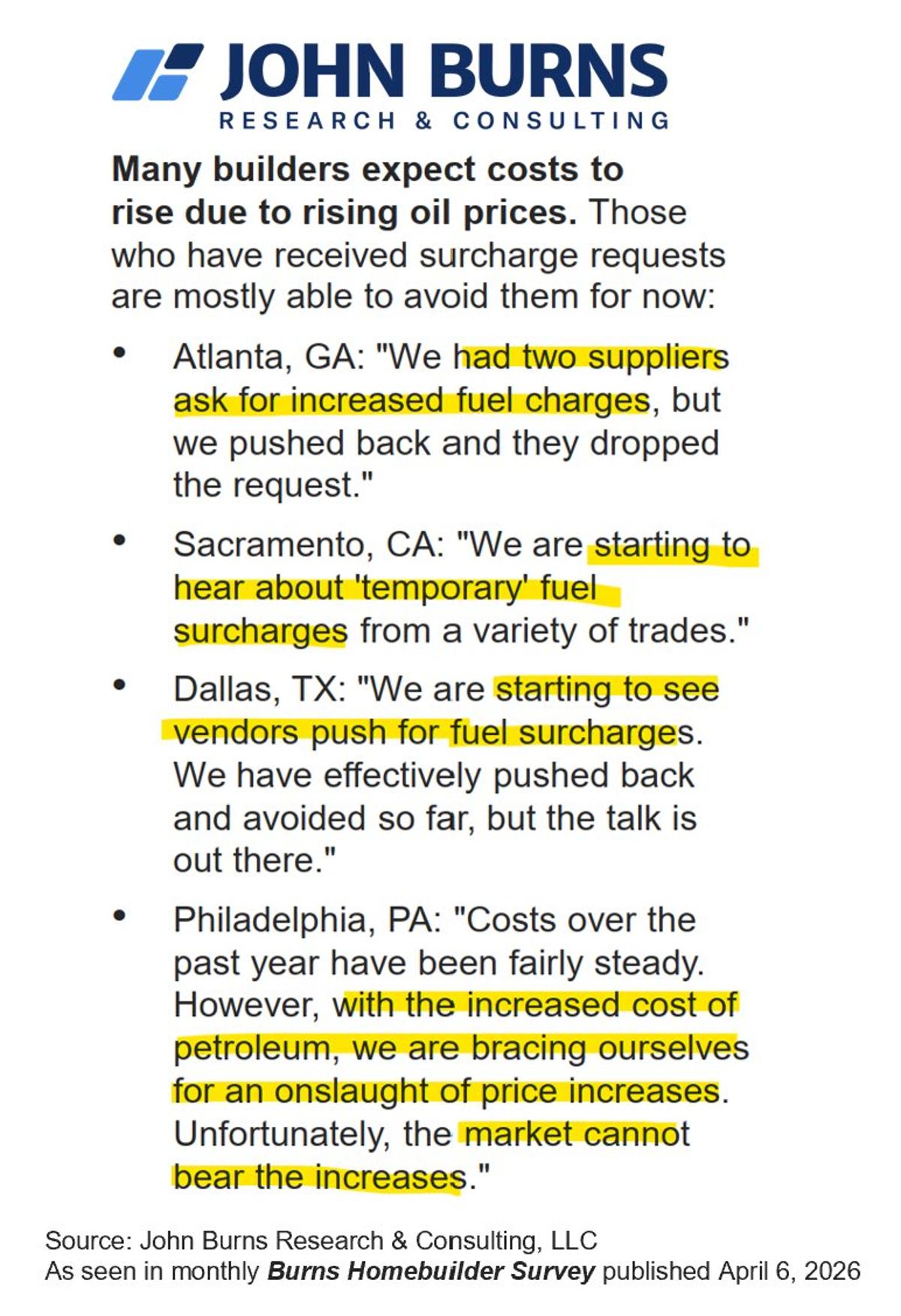

Construction Costs Surge After Energy Shock, Builders Confirm

Good read from @_willparker_ on construction cost increases happening post-energy shock. Homebuilders we surveyed in early April noted similar sentiment (several quotes below). https://t.co/QBhJxv5lrC https://t.co/9ICS9qHWaR

1970s Home Prices Outpaced 2020s Despite Higher Rates

Home prices rose faster from 1977 to 1979, with rates going from 8% to 13% than 2020 to 2022, when rates were sub 4% https://t.co/WlkyoI0JTr

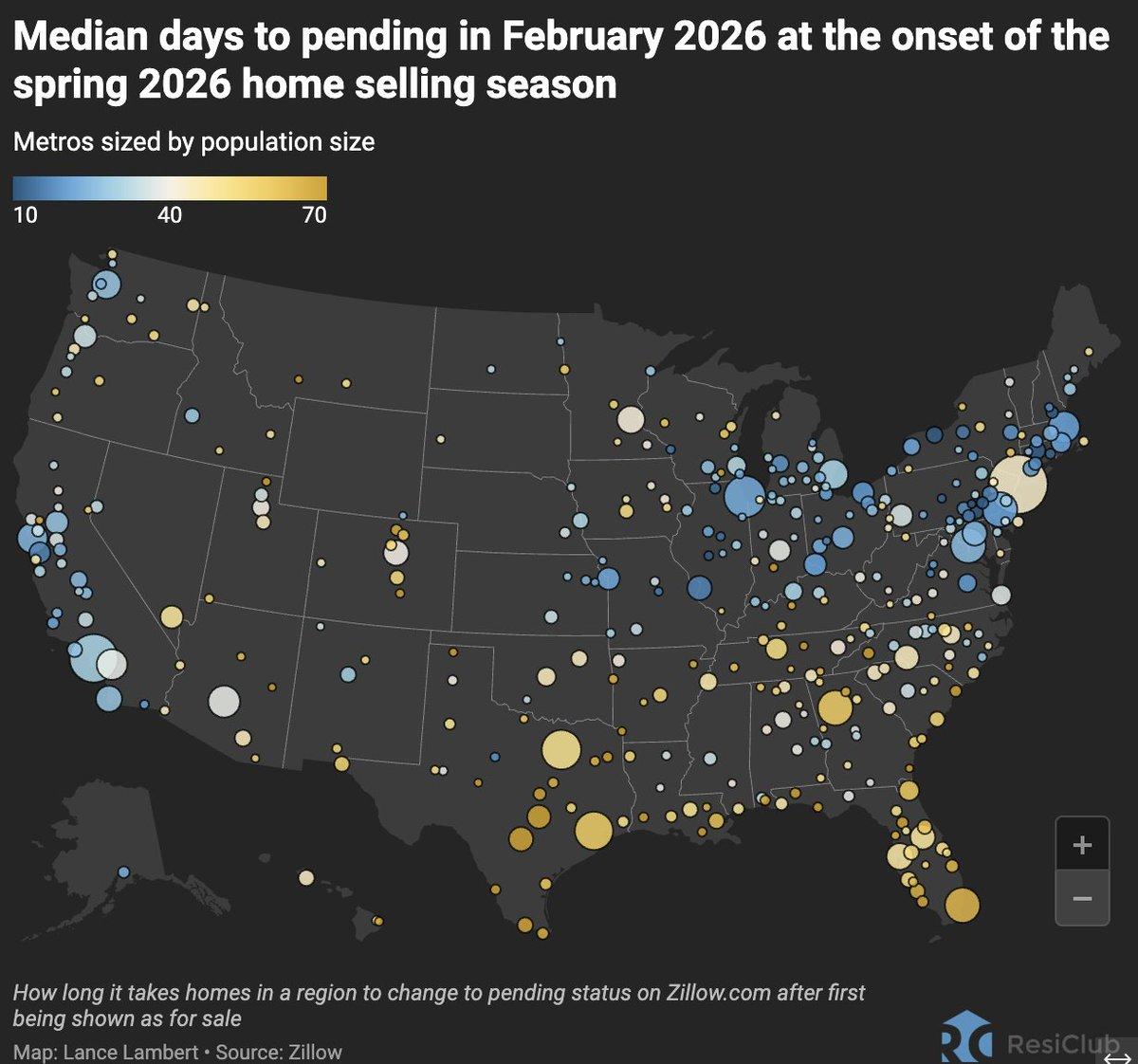

Housing Market Split: Hartford 11 Days, Austin 82

The current housing market bifurcation, as told by median days to pending The typical home listed for sale in the Hartford, CT metro area goes pending in 11 days, compared to 82 days in the Austin, TX metro area Our latest ResiClub...

70‑80% of New Sellers Are Mortgage‑Financed Buyers

New listings data ranged between 30K-80K per week seasonally, 70%-80% of these sellers are buyers, they don't sell and buy with cash. Most buy with mortgages. If you can't get this simple concept, I am no use to you both,...

Older Buyers Driving Mortgage Rate Lockdown, Data Shows

Again, if you analyze the buyer profile data, there’s no logical way we experienced a mortgage rate lockdown. The largest group of buyers tends to be older; the coupon data consistently showed this as they sold their homes with lower...

Data Shows Mortgage Rate Lock‑Down Theory Overstated

If the mortgage rate lock-down theory were a real thing, then existing home sales would be near 2 million because the 4 generational sellers that were buyers since late 2022 would not have sold and bought homes. As the data...

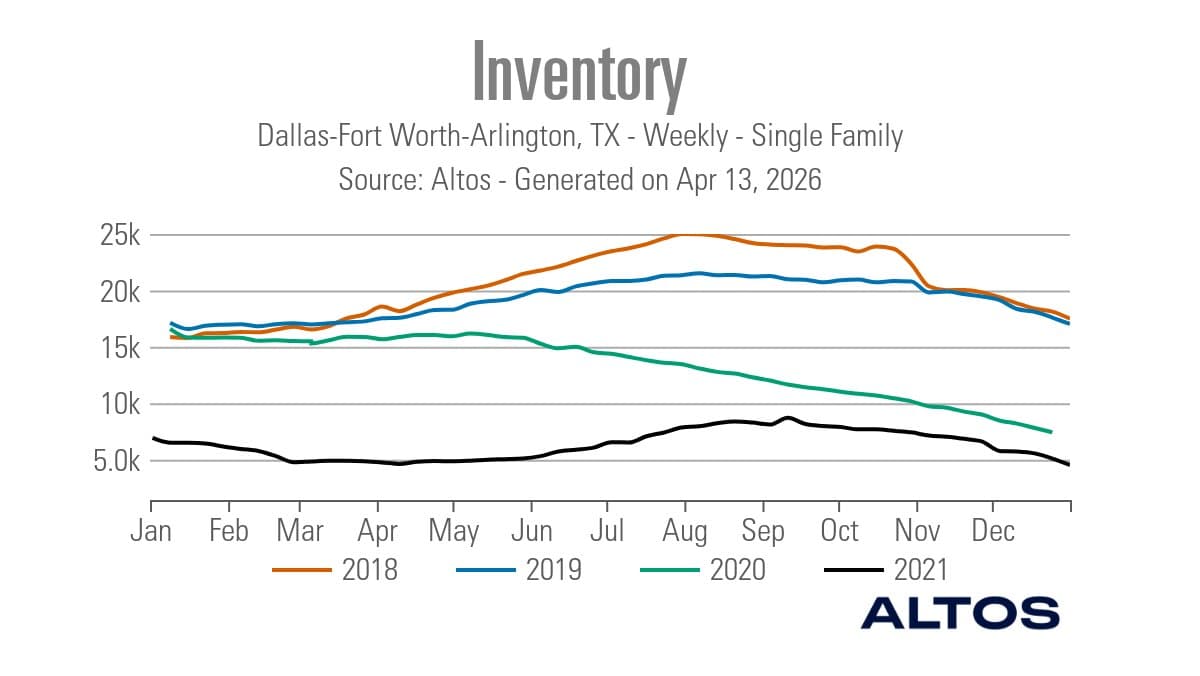

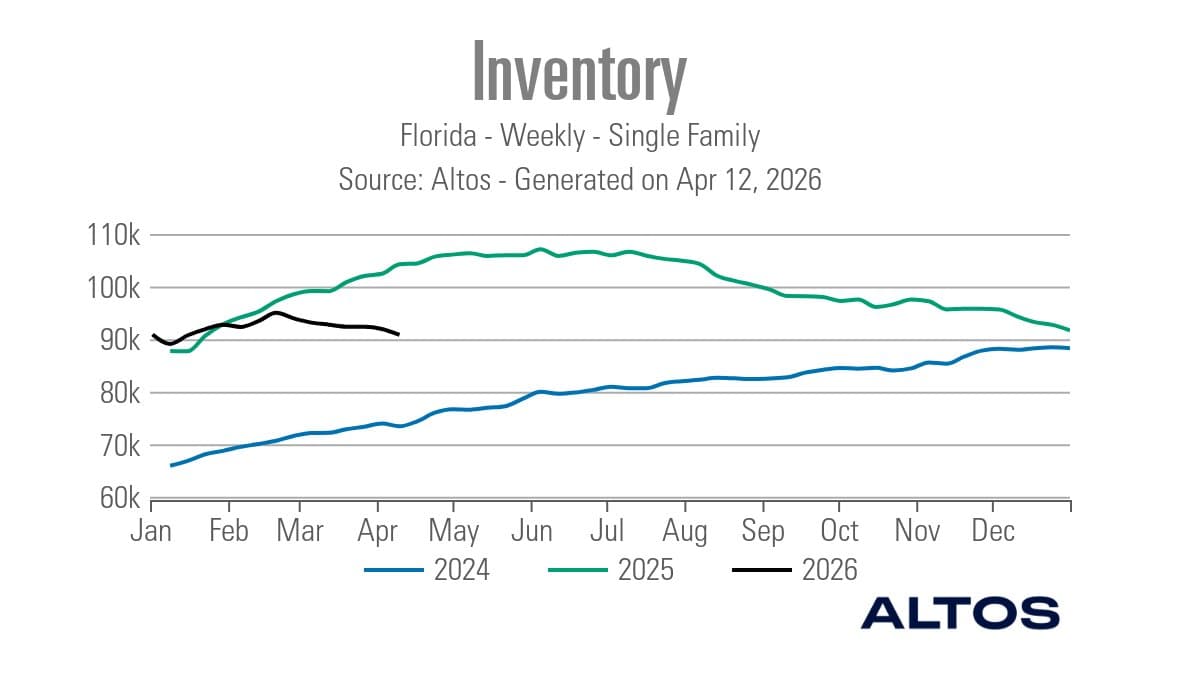

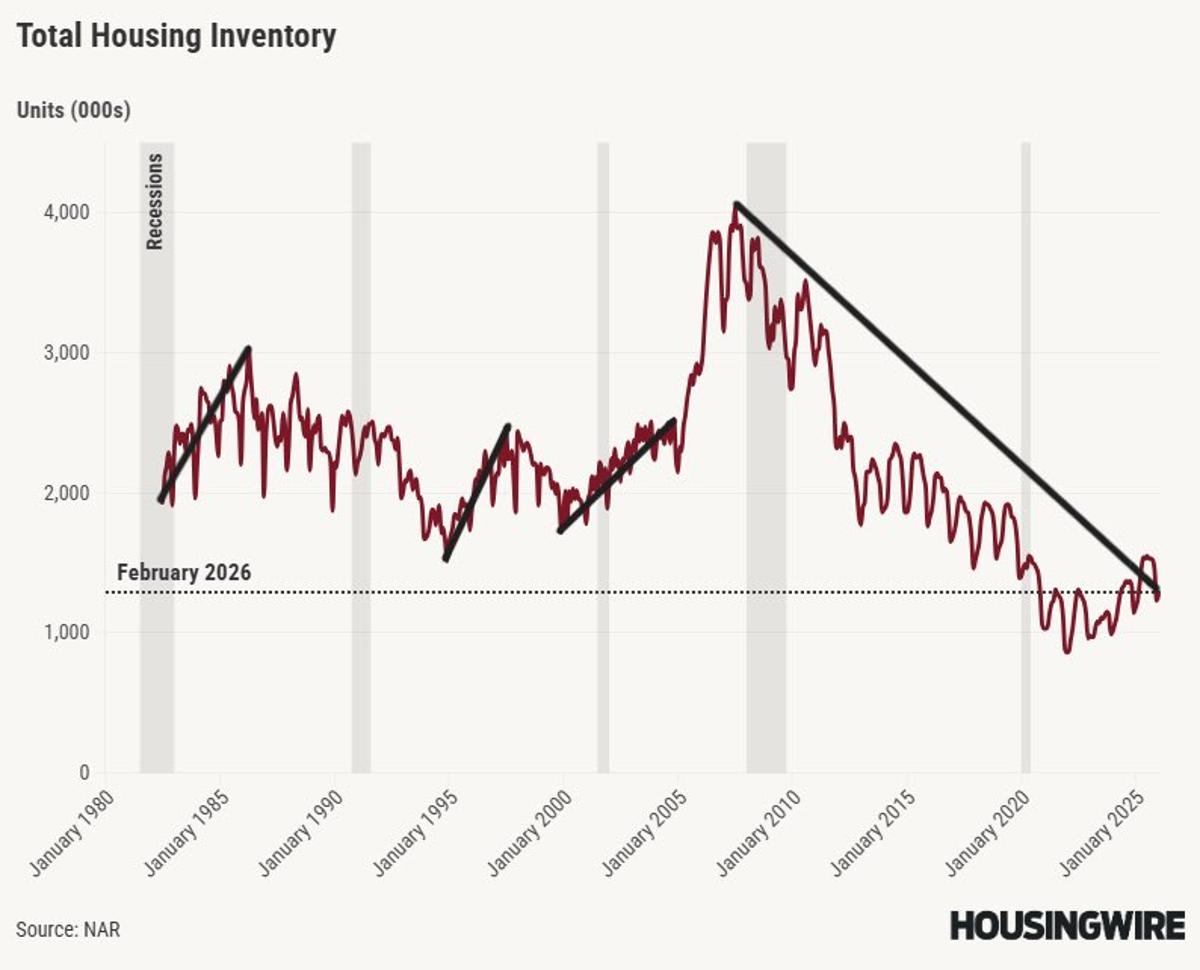

National Inventory Nears Negative YoY, but Not 2008 Levels

The national inventory is on the verge of going negative year over year. States like Florida that have seen a clear year-over-year decline were working from more elevated levels. Context is key, it's not worse than 2008, doom porn is...

Value‑Add Real Estate Profits Without Rent Growth

This seems to be one of the biggest misconceptions “Real estate investors need rent growth” No they don’t On a value-add deal, you make money even if rents decrease. You’re underwriting to *current* market rent $2.5MM profit if rents stay flat, $1.2MM profit if...

Adopt California ADU Model, Create National Market

Illinois should align their ADU framework with California's highly successful ADU framework. We need a national common market for manufactured ADUs in particular to really drive costs down. This is theoretically something the federal government might coordinate, but, well...

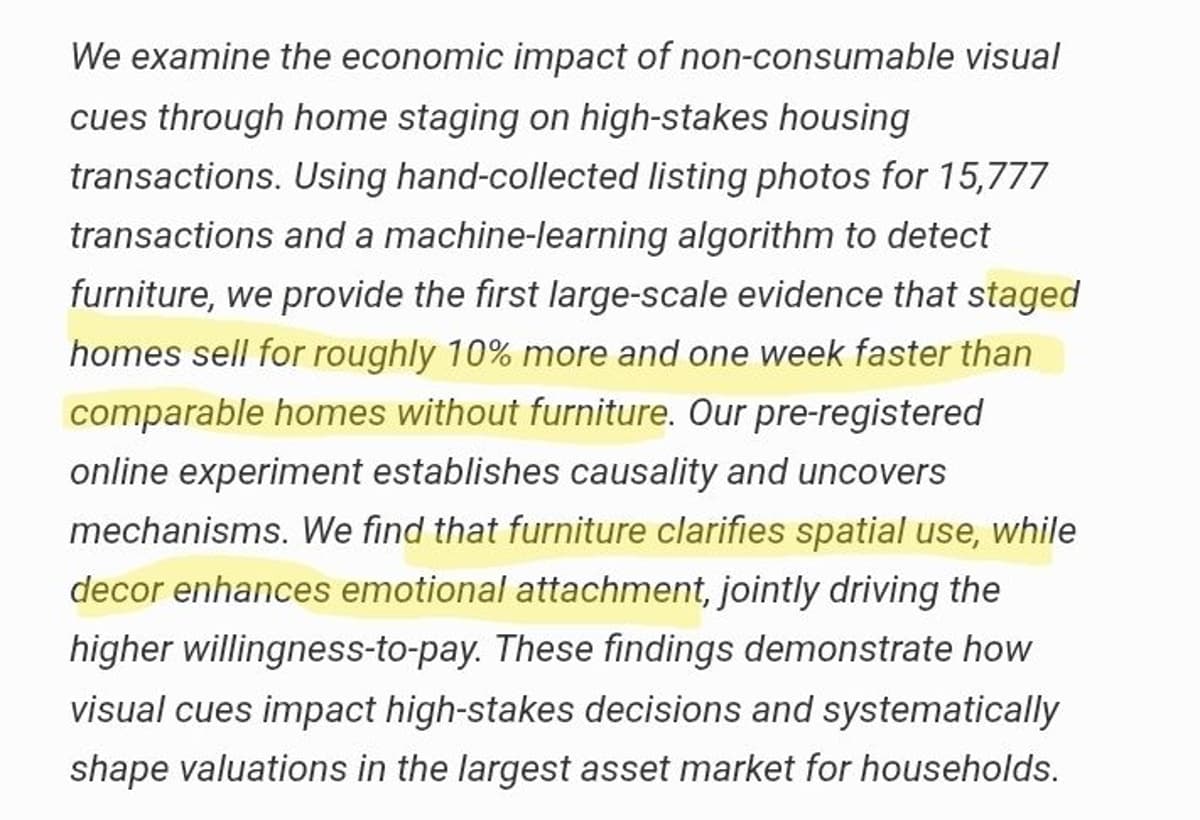

Staged Homes Fetch 10% More, Sell a Week Sooner

Fascinating: "staged homes sell for roughly 10% more and one week faster than comparable homes without furniture." https://t.co/5W7trDDx9w https://t.co/q0ff3oe93x

Existing Home Sales Data Arriving Tomorrow, Shows Inventory Trends

Existing home sales will be released tomorrow, providing a historical view of active inventory. https://t.co/Numo1lkNMr

Americans Trade Long Commutes for Larger New Homes

And this is why DR Horton is able to build and sell 100,000 homes per year Americans want a large new house … and they are willing to trade long commutes for them.

SUTL Enterprise Trades Cheap, Cash‑rich After Keppel

SUTL Enterprise (SUTL SP): The market leader in Singapore's luxury marina industry. Trades at 7.1x 2028e with a solid cash pile once the acquisition of Marina at Keppel Bay goes through. https://t.co/phzy16ip8T

Chinese City Land Sales Plunge 46% Year‑on‑year

Yicai: "300 cities auctioned 64.72 million square meters of land in the three months ended March 31, a 24 percent drop from a year ago. By value, sales plunged 46 percent to CNY215.4 billion. By floor area, they shrank 26...

Housing Inventory Drops Negative Year‑Over‑Year, Explained

#housing inventory going negative year over year? This weekend’s tracker we discuss what is really going on! @housingwire @sarahteresa6 #economics #mortgagerates #realestate #chartdaddy

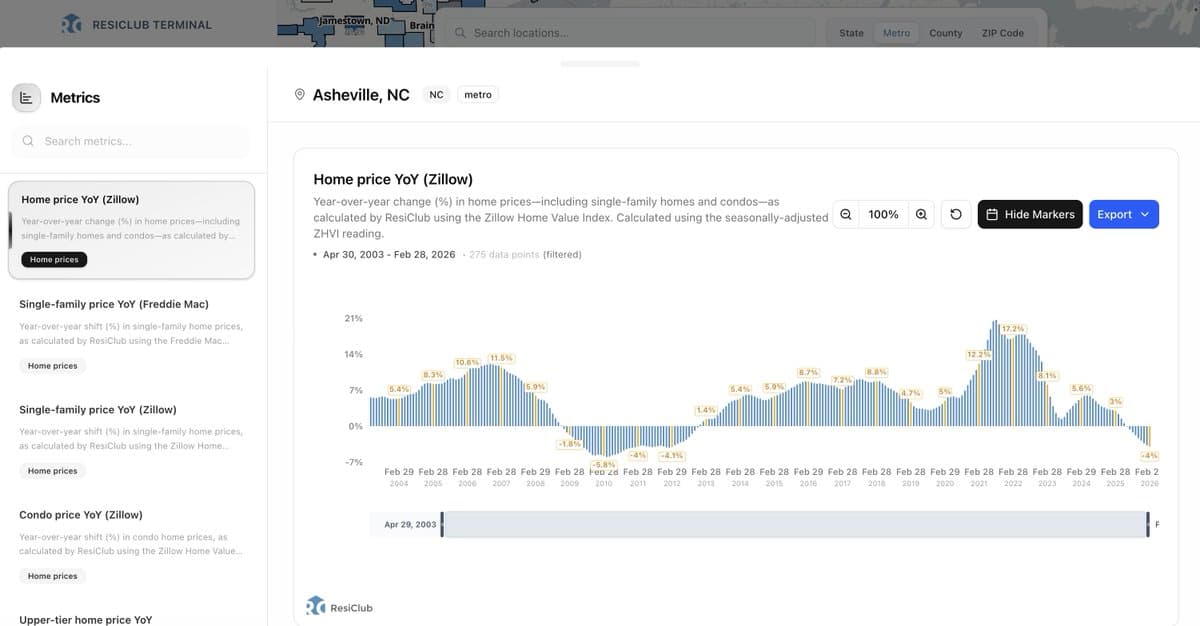

Asheville Housing Enters Rare Market Correction

The metro area Asheville, N.C. housing market remains in correction-mode Historically speaking, corrections are rare in the Asheville, N.C. market This is only Asheville's second correction since 1975. The other being 2008-2011 via ResiClub Terminal

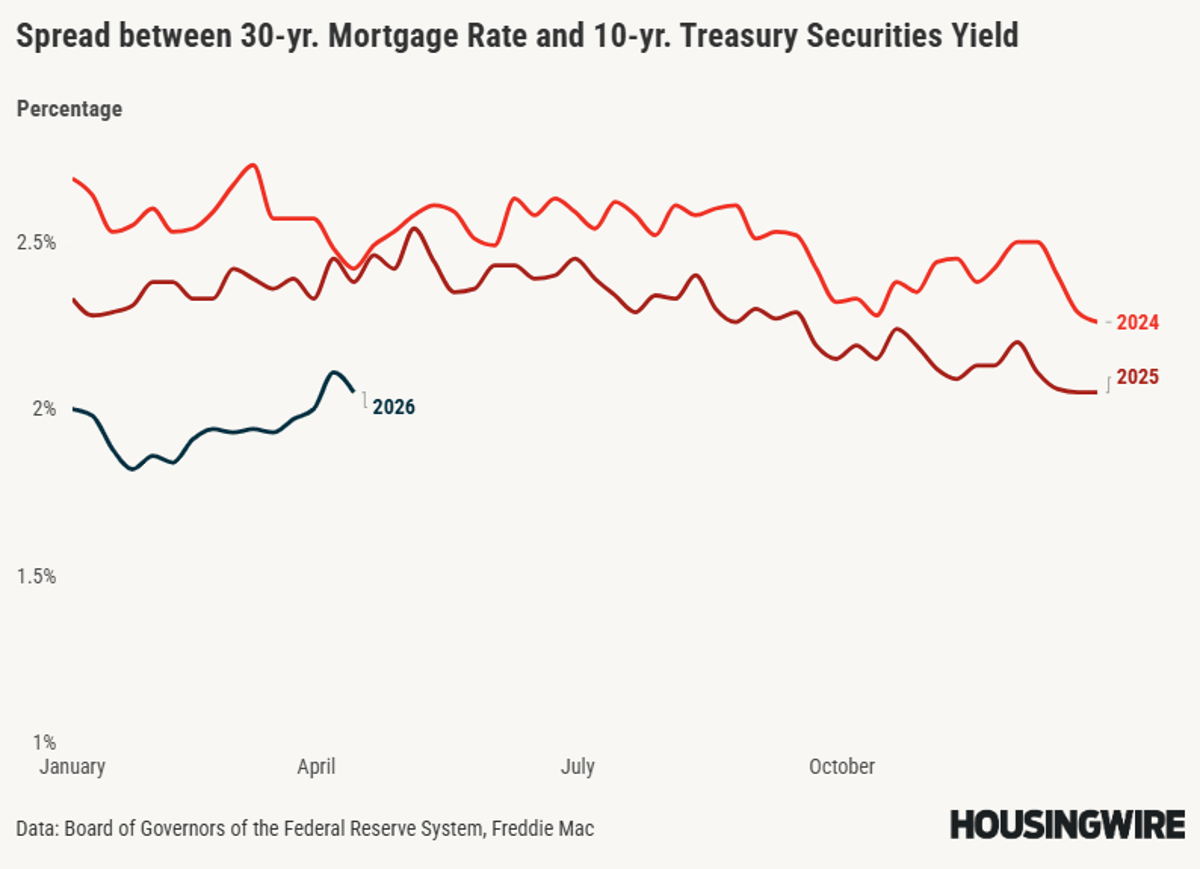

Better Mortgage Spreads Keep Rates About 1% Lower

If we had the worst mortgage spread levels in 2023, mortgage rates would be 7.45% today, not 6.39%. If we had the worst levels of 2024, mortgage rates would be 7.08% today. If we had the worst levels of 2025, mortgage rates...

Inventory Growth Stalls; New Listings Dip Sharply Year‑over‑year

Inventory growth really slowed this week, both active and new lisitngs, new listings is noticebly lower this year vs last year, but I do have a theory on that this week with the weekend tracker

Columbus Core Home Prices Surge Year‑over‑year

LEFT: Year-over-year home price change in the core of Columbus, OH in spring 2025 RIGHT: Year-over-year home price change in the core of Columbus, OH in spring 2026 via ResiClub Terminal https://t.co/Poj3BM9z1y

February Home Price Cuts Hit Record High Since 2012

I ask you this Saturday. WHO has been ahead of this surge? If you don’t follow @m3_melody you’re behind trends “34.2% of Feb home sellers lowered their list price. That’s up from 31.5% a year earlier & represents the highest Feb...

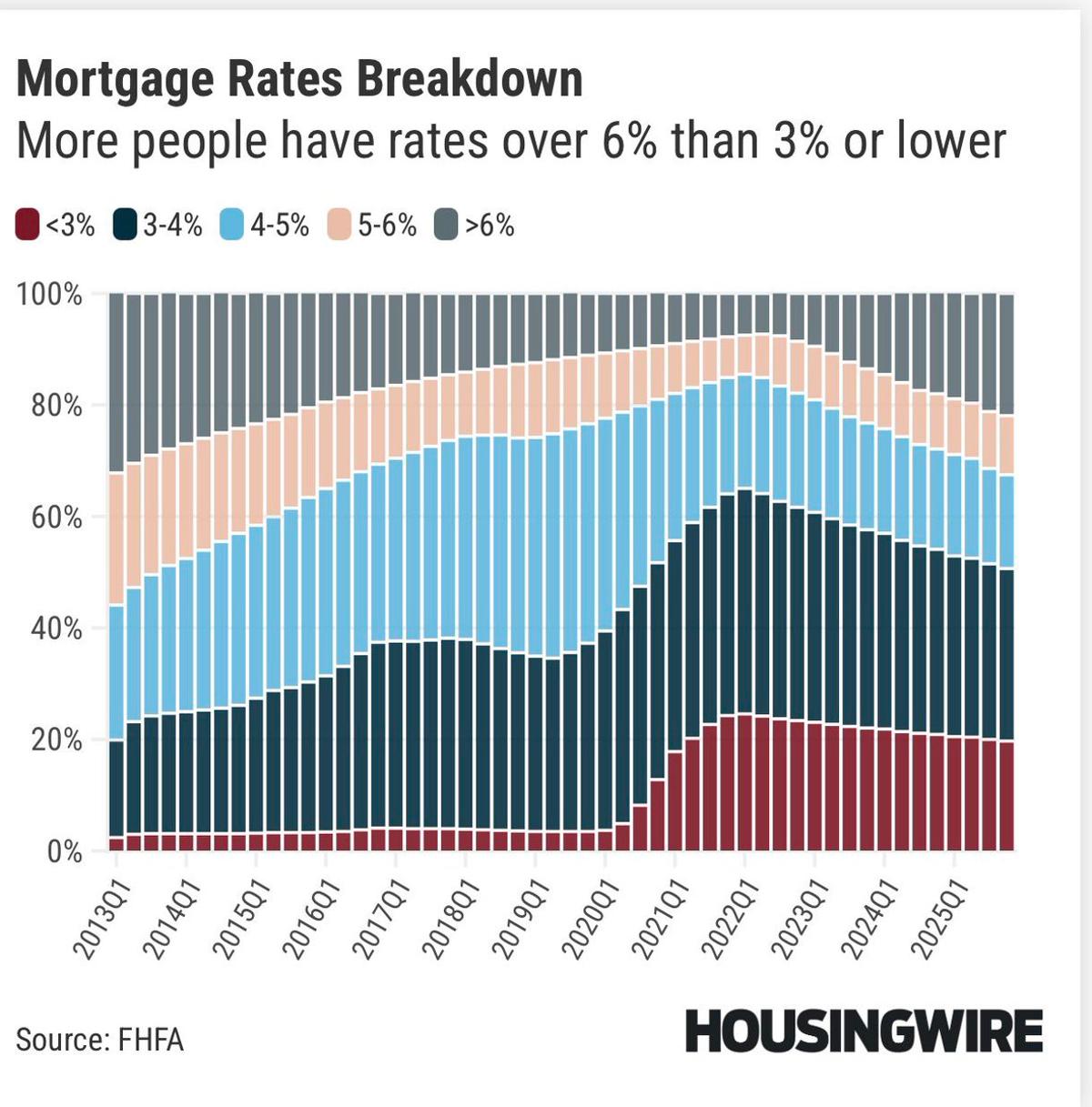

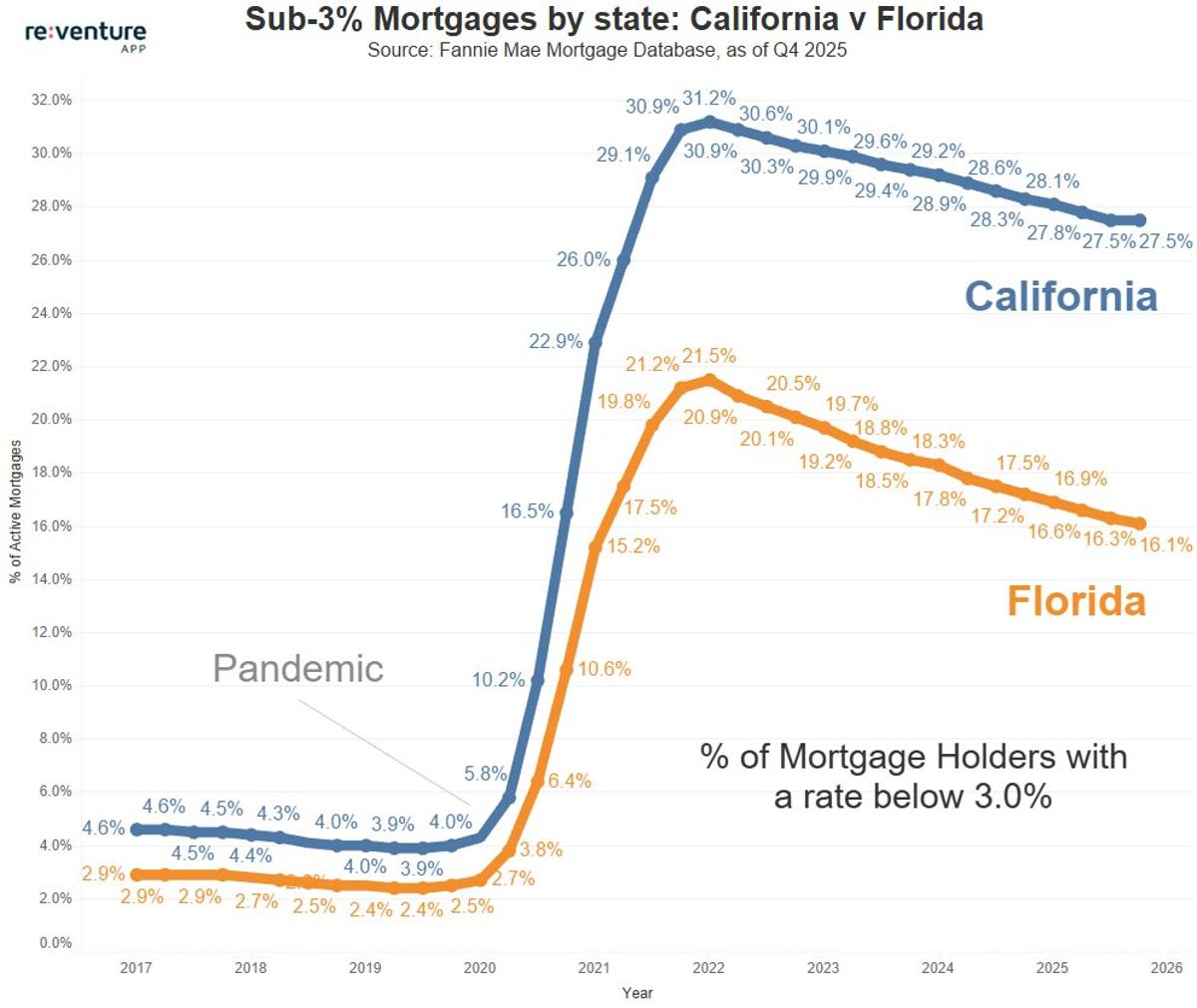

California's Low‑Rate Mortgages Keep Prices Firm, Florida Falls

Some interesting differences are showing up in mortgage rates by state. California: 28% of mortgaged houses are at sub-3% rate Florida: 16% only before pandemic, they both were similar. But now, there's a big gap. California's sub-3% mortgage rates are one of the reasons...

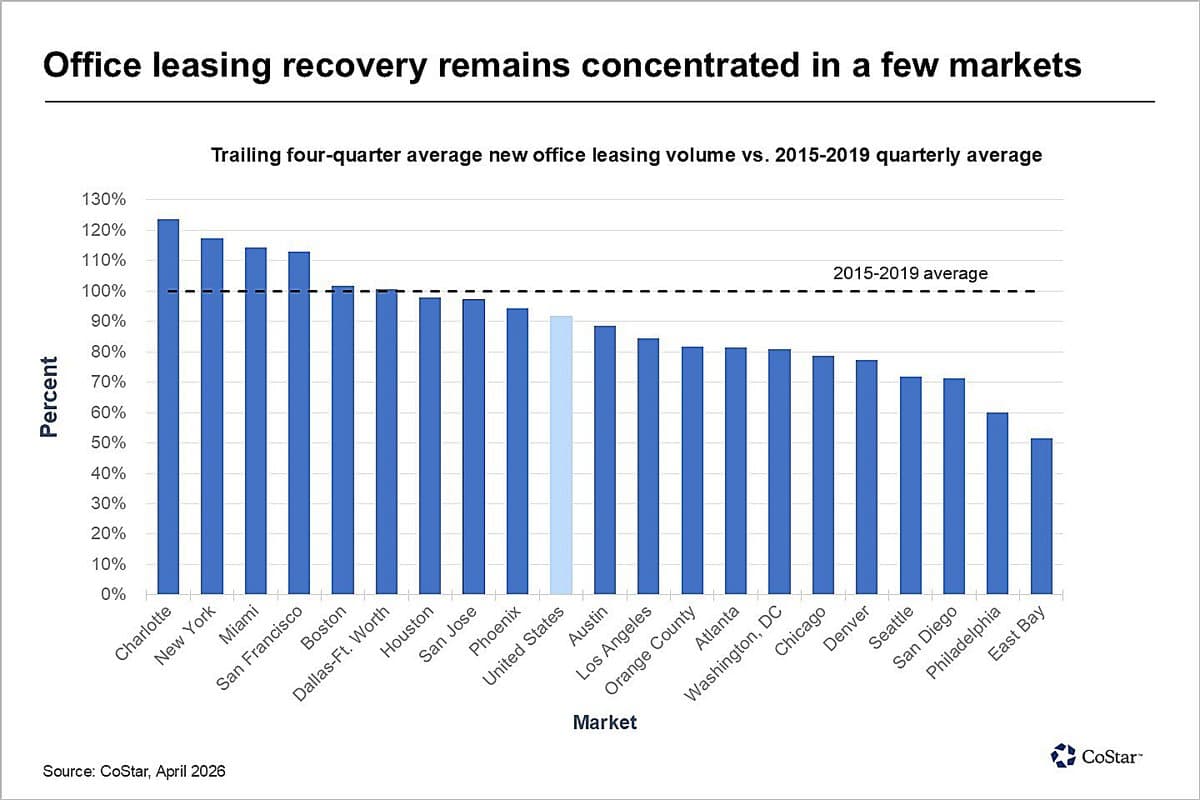

Office Leasing Nears Pre‑pandemic Levels in Half of Top Markets

Office leasing volumes have rebounded to within 10% of pre-pandemic averages in nearly half of the 20 largest office markets in the country. https://t.co/pNvbzWkrZl

Out‑of‑State Money Fuels Miami Office Boom

Out-of-state interest whips up the #Miami office market, as come-hither conditions attract the well off. 'It's OK to be rich here, it's OK to be poor here. It's not OK to be rich in #LA or #NY' #SoFla #realestate #CRE...

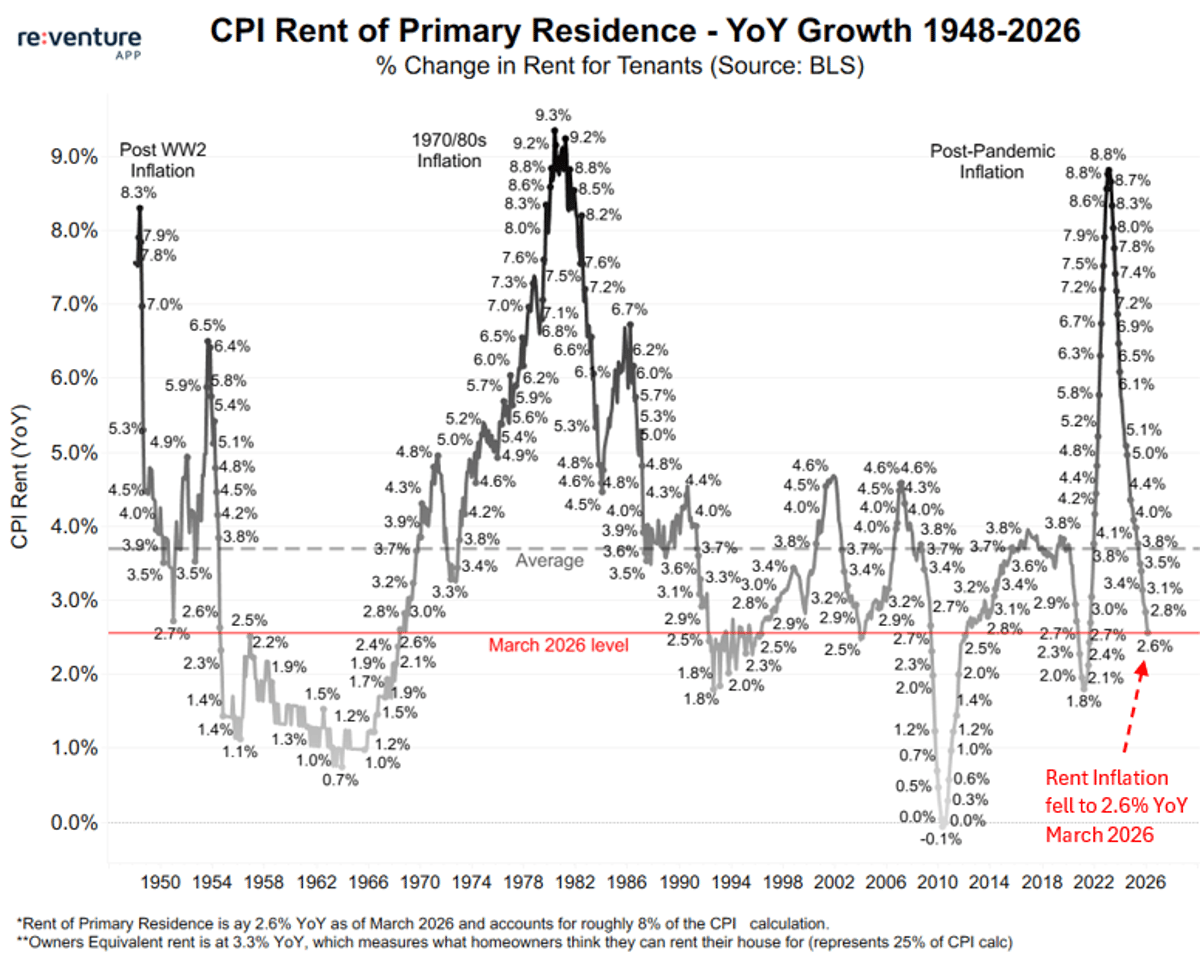

Rental Inflation Hits 60‑Year Low, Dampening CPI Outlook

The thing to pay attention to in this CPI report is rent. Rental inflation reported by tenants fell to 2.6% YoY in March 2026. This is a full percentage point below the long-term average, and near one of the lowest levels in...

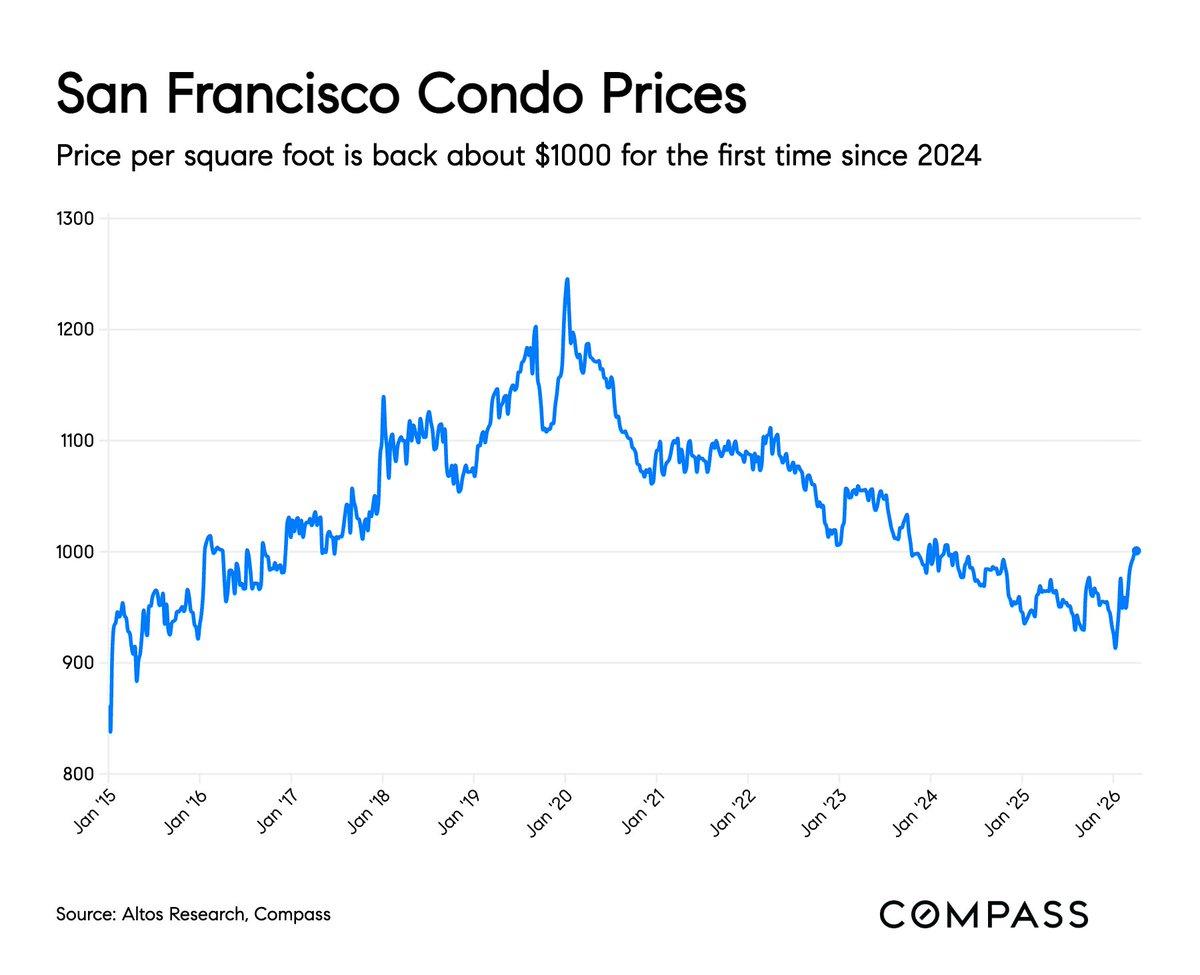

SF Condo Prices Surpass $1,000 per Sq Ft After Two Years

Welp, San Francisco condo prices are back above $1000/sft for the first time in two years. https://t.co/hRx2V9xESt

High Rent Targets Force Developers Toward Studios

Any new construction unit needs to be significantly higher Rent/SF than existing homes in the area, or else it won't get built at all The way developers keep Prices down is by building smaller units ... like Studio apartments And it's why...

Even Advisors Buy High‑Priced Property Amid 2026 Rates

I just heard a financial advisor bought a $1.5M condo. In 2026, with home prices sky-high and mortgage rates above 6%. Does this mean it's a good time to buy real estate?

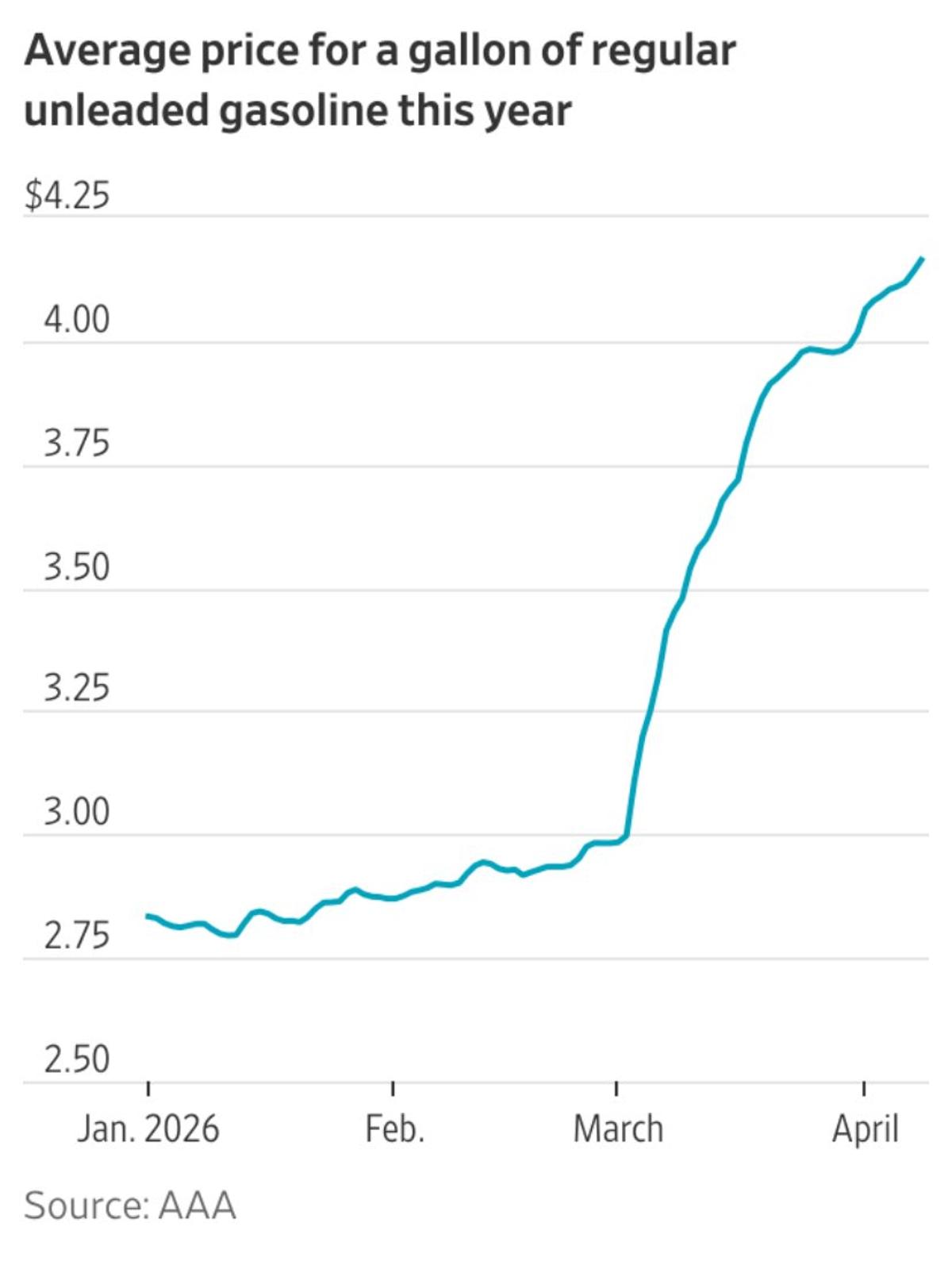

Rising Gas Prices Threaten Out‑skirt Home Sales

So many homebuilders ventured further out into ‘drive until you qualify’ submarkets this cycle as affordability got squeezed. This gas price chart is going to now weigh on those communities, adding incremental pressure to both new home sales and starts...

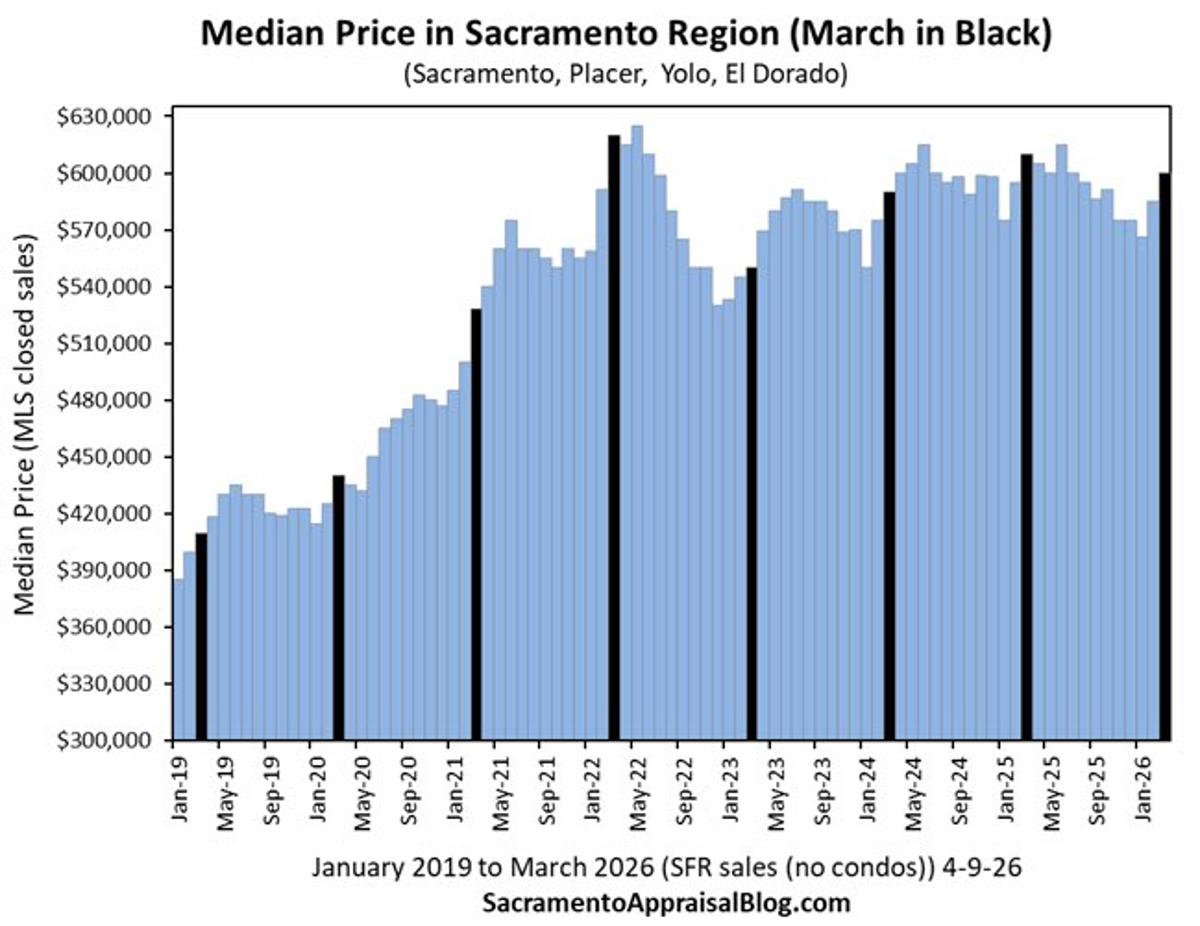

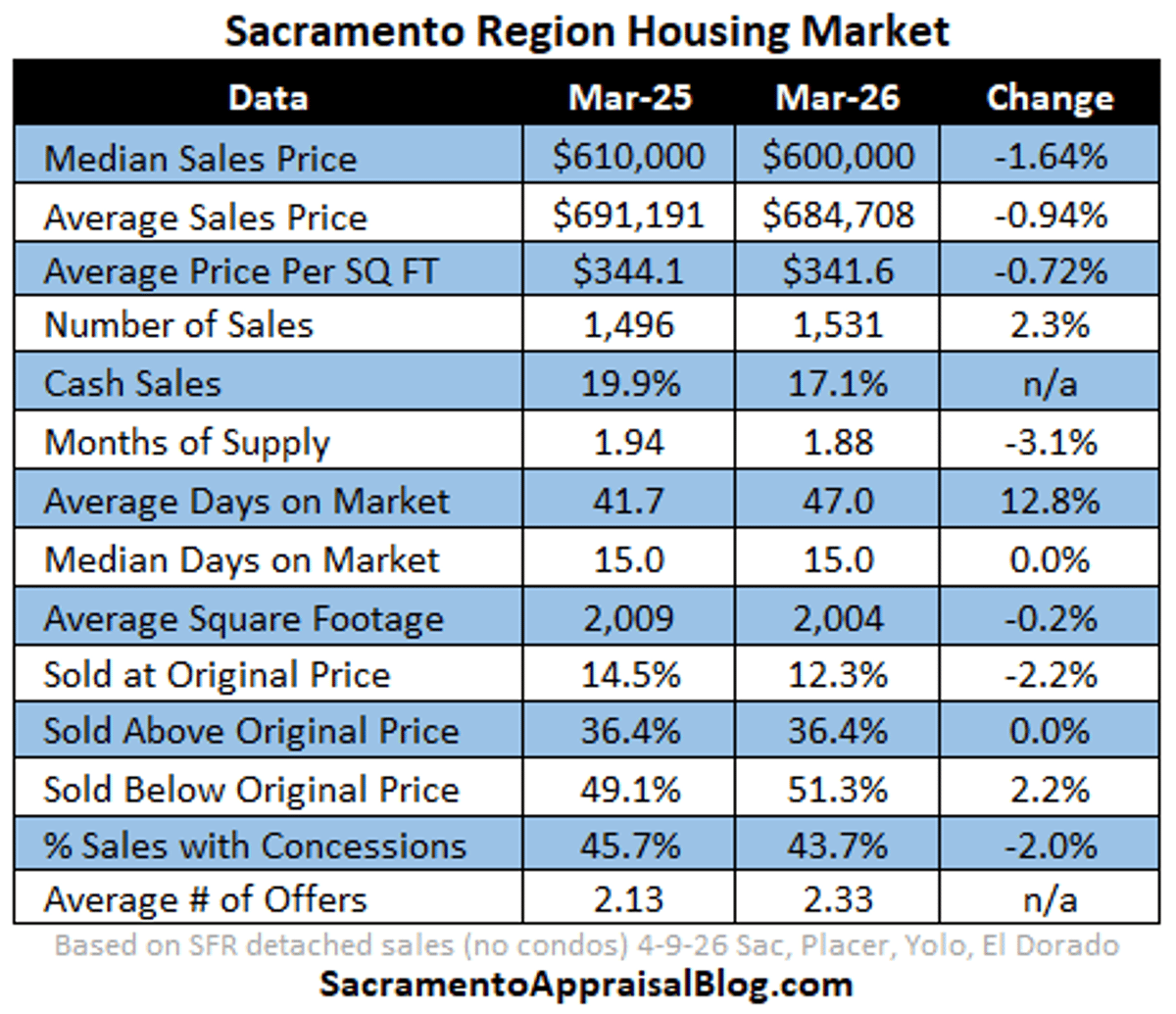

Slight Price Dip, Spring Surge Revives Sellers Across 12 Counties

Prices are down a little from last year, and we’re seeing a spring uptick in 2026. Both things are true. And sellers have been coming back to the market. Some perspective and stats for 12 counties on my blog today. https://t.co/mTNHN4Zkh3...

Chicago's Post‑COVID Boom: Housing Soars, Nightlife Thrives

I can't figure out why the switch flipped but Chicago is in boom times right now. Home values are skyrocketing (in the nice neighborhoods) and even on weeknights bars and restaurants are humming. I've lived here since 2009 and I...

Canadian Rents Plunge, Oversupply Threatens Landlords

Canadian Rents Have Gone Down 18 STRAIGHT MONTHS & More New Construction Rental Supply Is Coming Than Ever Before In History Yeah, Mom & Pop Landlords who bought units in the last 6 years knew things were bad But in some Canadian...

Why Top Flippers Skip Banks for Funding

Why would top fix & flippers like @abrahams.jonathan NOT go to a bank to fund their projects? Several reasons. #fixandflip #newconstruction #realestateinvesting #privatemoneylender

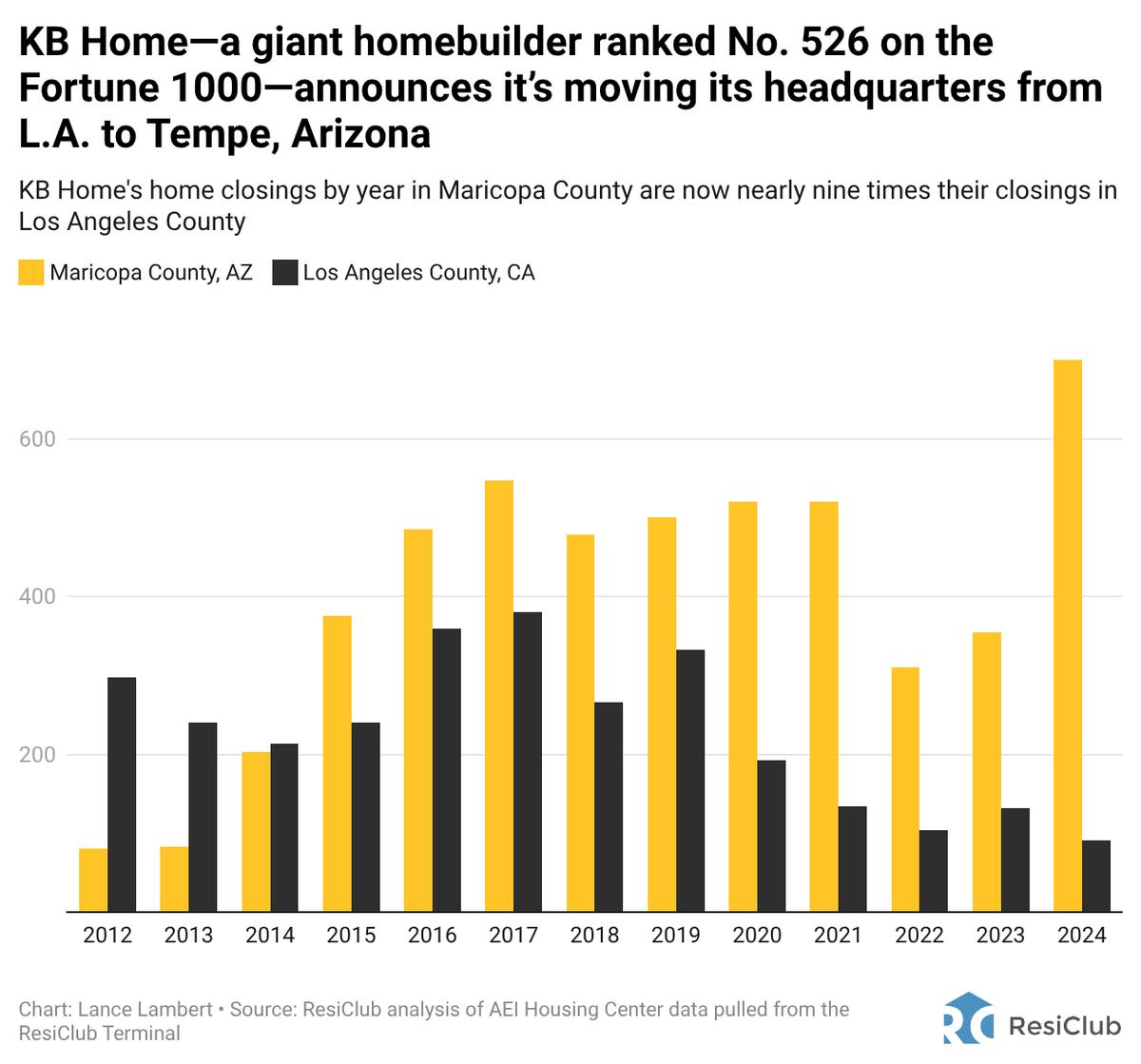

KB Home Flips Focus: Arizona Now Outpaces LA

KB Home—a giant homebuilder ranked No. 526 on the Fortune 1000—to move its headquarters from L.A. to Arizona Back in 2012, @kbhome did almost 4 times as much homebuilding in Los Angeles County as in Maricopa County Now, it does nearly 8...

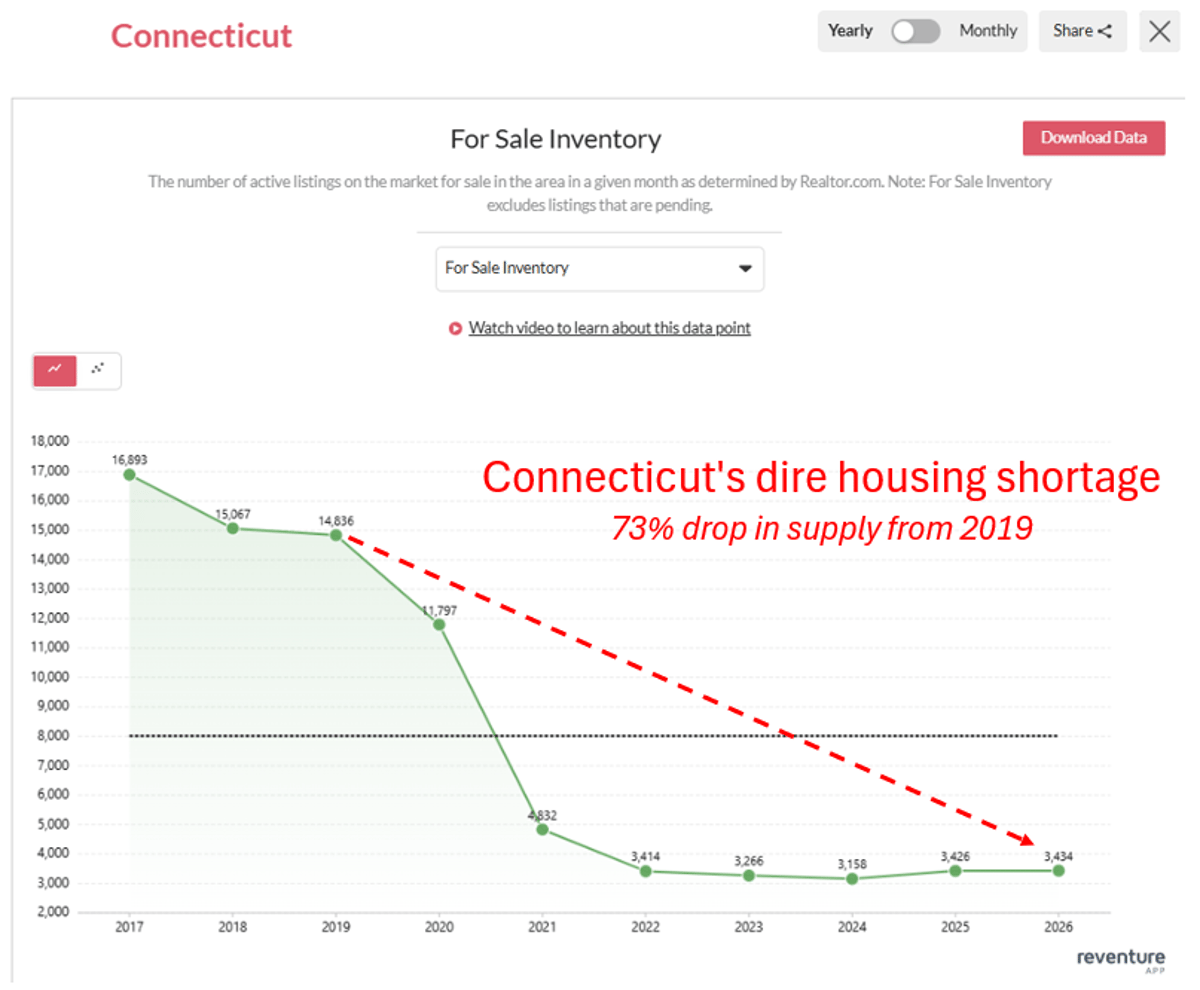

Connecticut’s Listings Plummet, Prices Surge

The Biggest Housing Shortage in the U.S. is in... Connecticut. Listings are down 73% from pre-pandemic levels, and by 50% from the 10-year average. As a result, prices are up nearly 25% in the last 3 years and there are still bidding...

Non‑residential Investment Barely up 2.4%

Non-residential investment increased at just a 2.4% rate in the 4th quarter. Good thing Trump keeps talking about that $18 trillion in foreign investment coming in, otherwise no one would know anything about it.

Gurgaon Real Estate Now Driven by Holding Power, Not Demand

Pricing in Gurgaon is not driven by demand anymore. It’s driven by who is willing to wait. Most people track buyers. Smart money tracks holding power. Because markets don’t move on transactions. They move on who refuses to sell. Here’s the shift no one is talking...

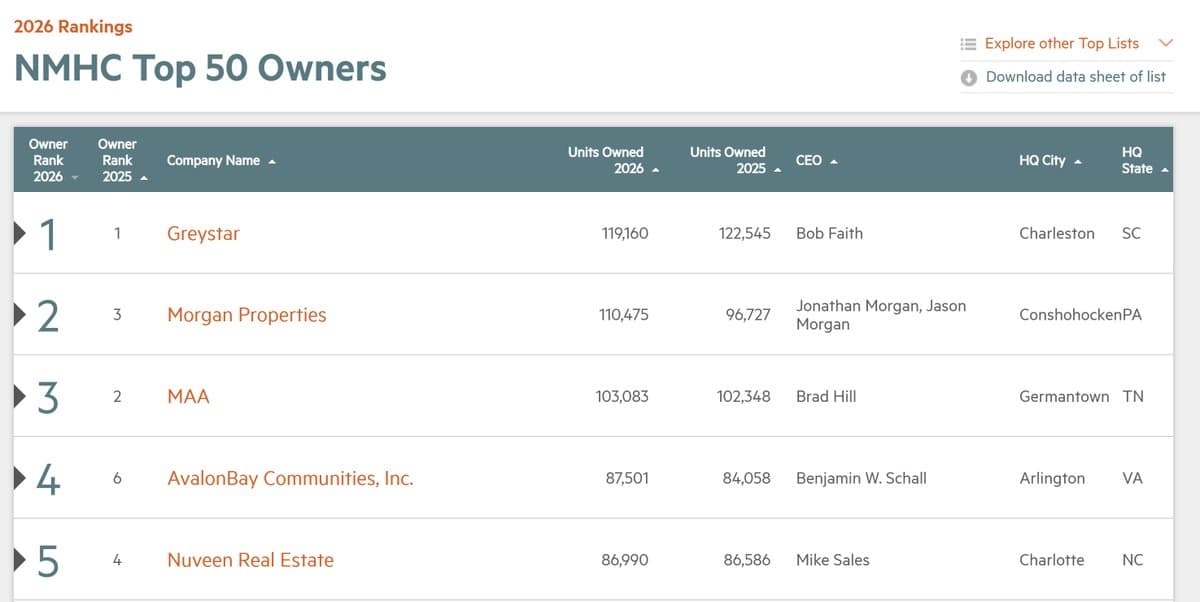

Morgan Properties Surges to #2, Greystar Holds Top Spot

The 2026 NMHC Top 50 rankings are out. Owners: Morgan Properties leapfrogs MAA into No. 2 spot, adding 14k units to reach 110k. Greystar remains No. 1, but was net seller last year. https://t.co/6UNTlK2tUF

Ares Backs $1.7B Sunbelt Retail REIT Push

Latest bet that #CRE especially in the #Sunbelt is undervalued belongs to #Ares, w/is teeing up #Whitestone #REIT for $1.7B+taking 5MSF of open-air #retail in places like #Phoenix #Austin #DFW #Houston #SanAntonio. #realestate #PE #BofA #WallSt https://t.co/iaUBXCrFQe

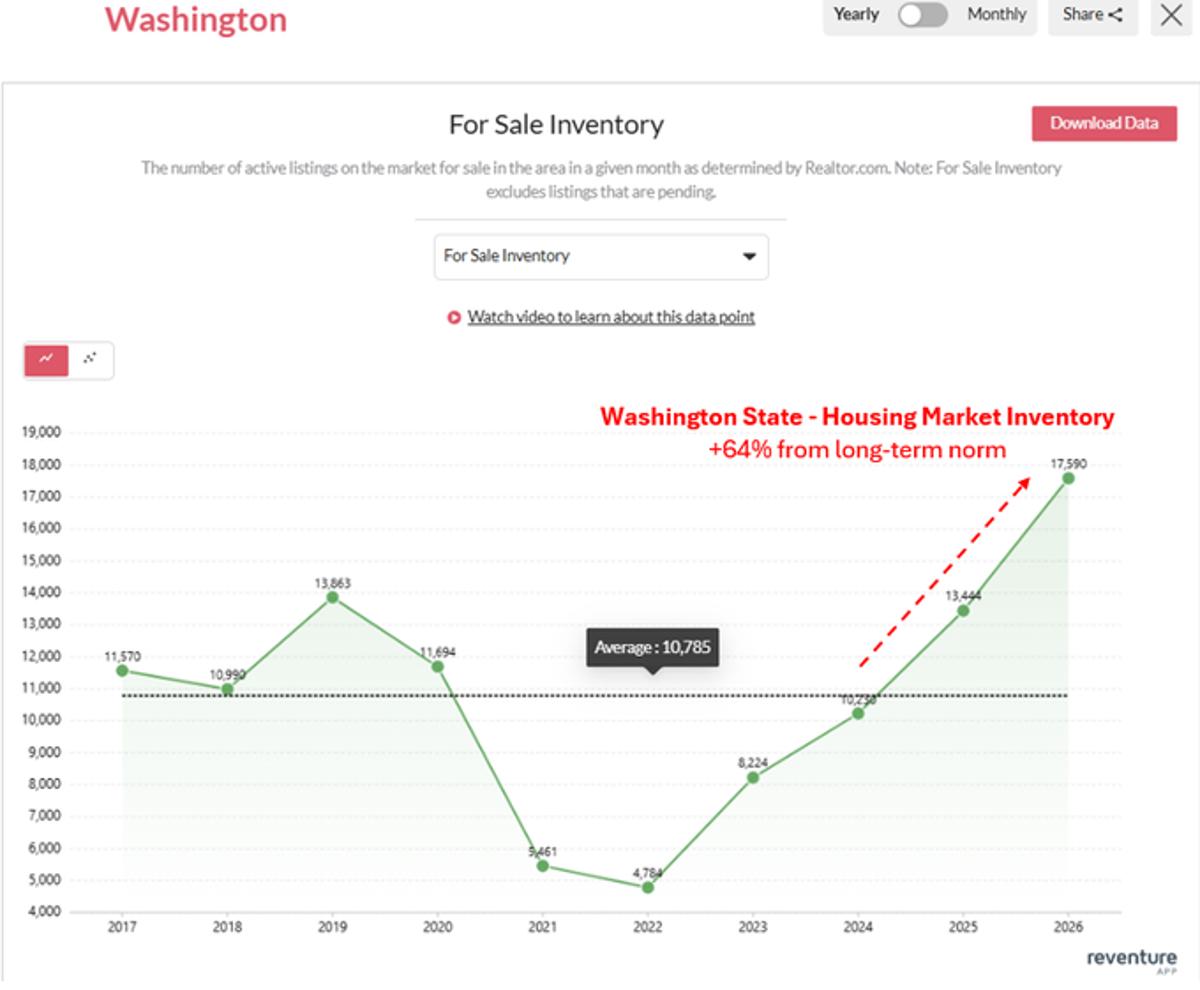

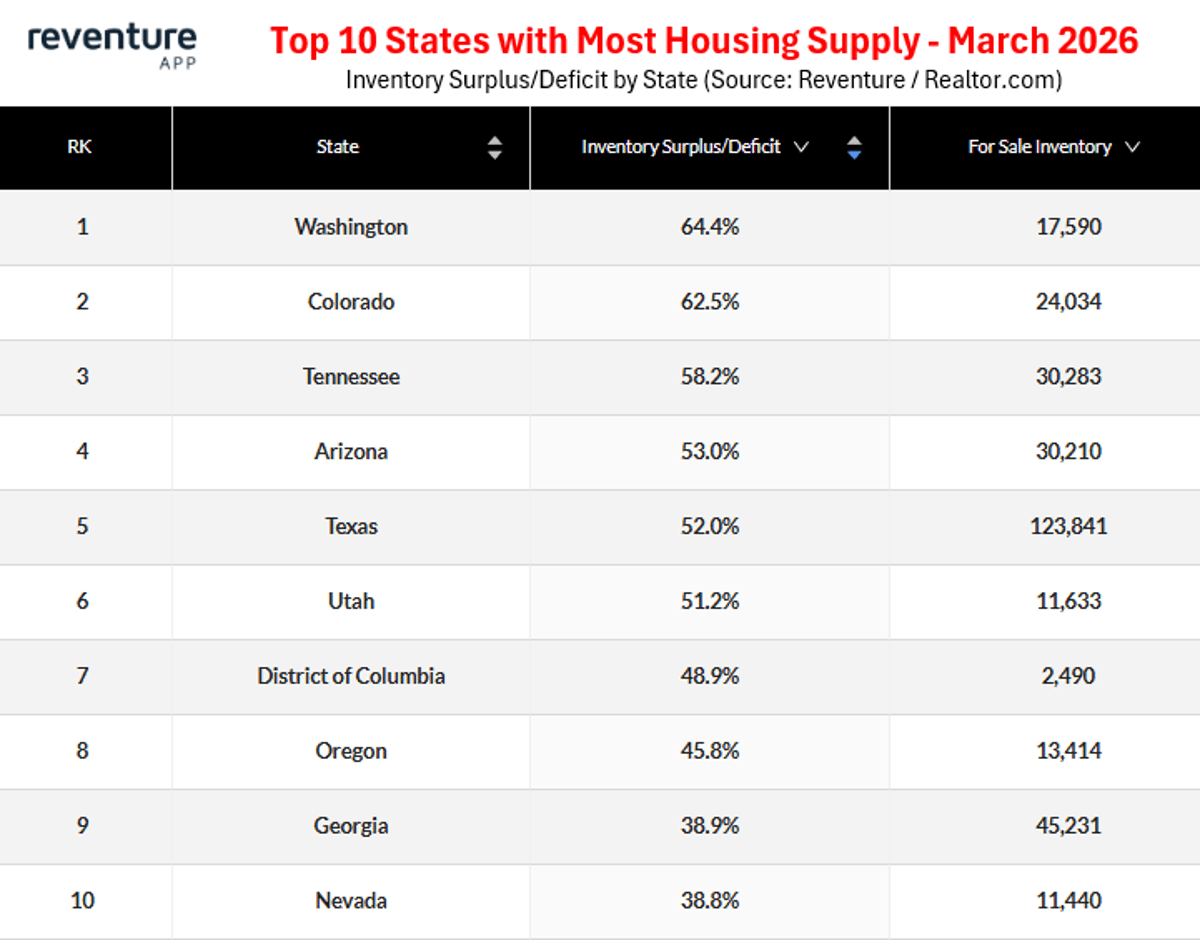

Washington Housing Supply Surges 64%, Prices Set to Tumble

What's going on in Washington State? housing supply is skyrocketing, now up to 17,580 listings. That's 64% above the long-term average for March. It seems like there's an exodus of sorts playing out, with metros like Seattle and Spokane spiking on supply. Home...

March Sales Volume up, Prices Slightly Down

March had slightly stronger sales volume this year and slightly weaker prices. I'll have over ten counties of data on my blog tomorrow. What stands out to you? https://t.co/1K0bqpjivW

FHA Delinquency Spike Mostly Reporting Artifact, Not Borrower Weakness

New paper argues that 92% of the increase in FHA mortgage delinquencies between Sept. 2025 and Jan. 2026 "is driven by how an FHA policy change is reported rather than increasing financial fragility among FHA borrowers" https://t.co/uRxP5BtOQO

NYC Simplifies Backyard ADUs for Affordable Housing

I love that NYC is making it easier to build housing with backyard ADUs that you can install for $200k and rent or use for family. A few here from the @nytimes: https://t.co/2TcTnKKRwm

February Sees Biggest Seller Price Cuts Since 2012

More sellers are cutting prices than any February since 2012, and they are having to adjust their expectations down by $40k on average. That's according to a new Redfin report (link in thread). https://t.co/uokLEo4VDR

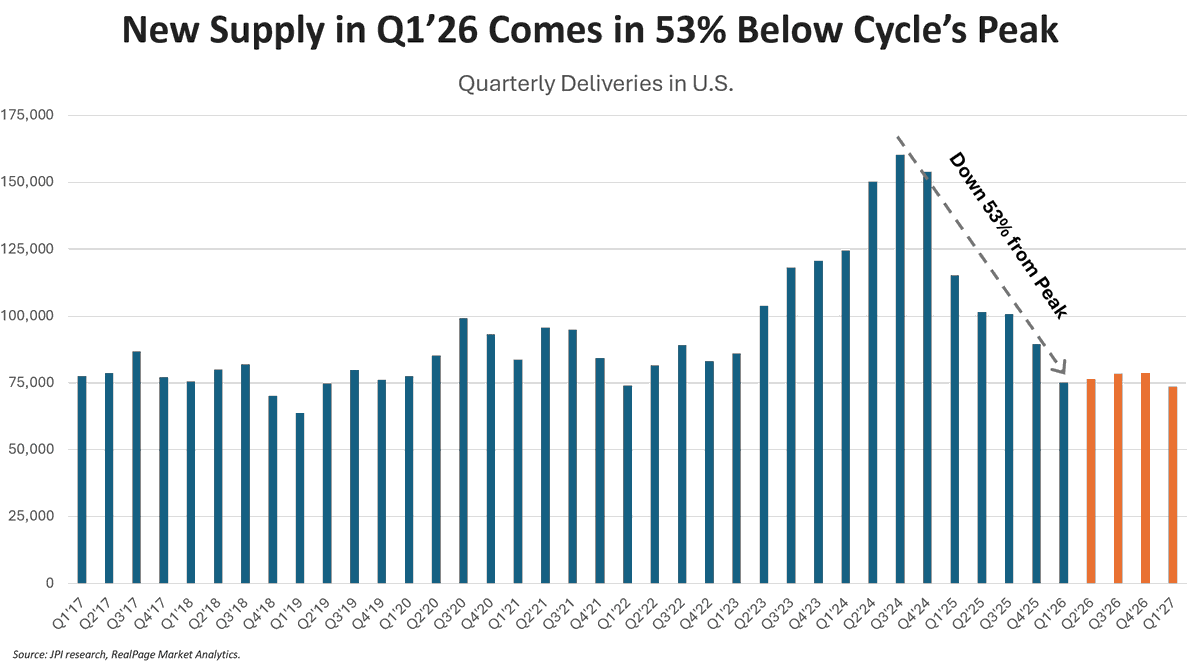

Apartment Supply Surge Ends, Rent Growth Stalls

It's official: The historic wave of new apartment supply is now in the rearview mirror. Completions in Q1'26 came in at one of the lowest levels in 7+ years, and will likely hover around these levels for a while --...

Office-to-Residential Success Demands Cost, Capital, City Alignment

First office-to-residential conversion in Old Town Alexandria just delivered 199 units — 40% leased out of the gate. The developer said it plainly: conversion isn’t right for every building. Cost basis, capital structure, city partnership. All three have to work....

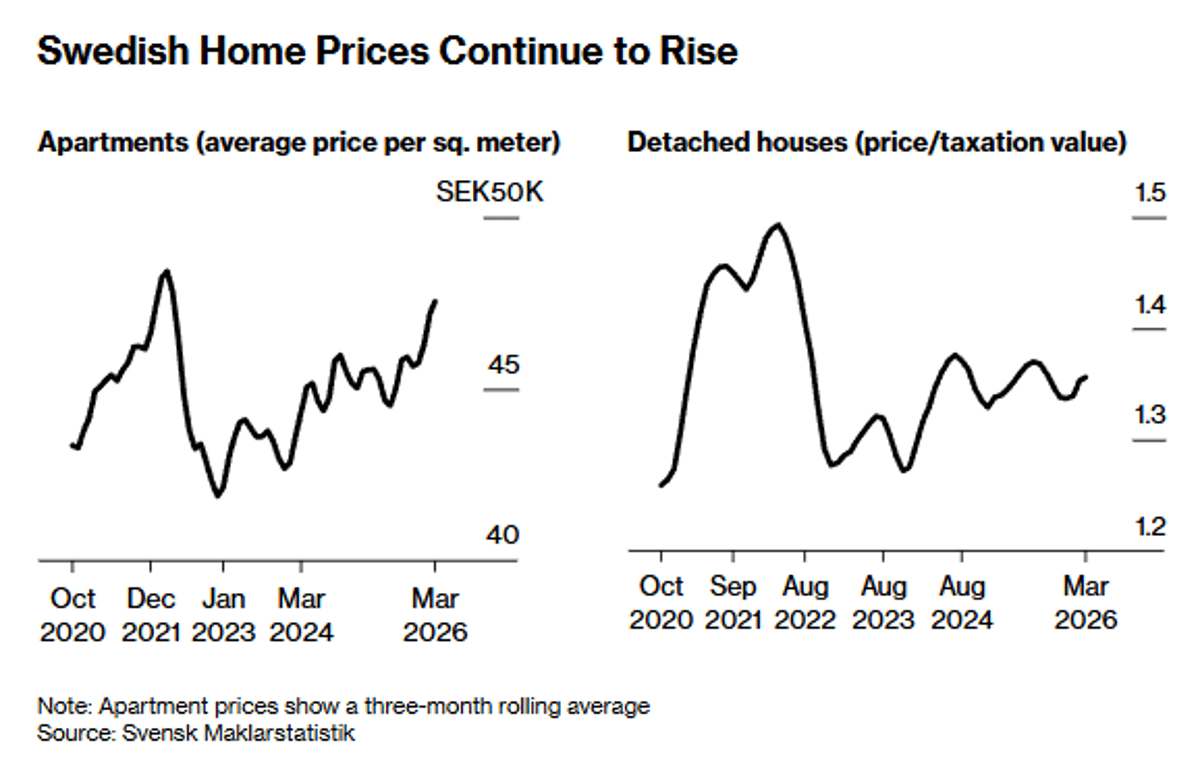

Swedish Apartment Prices Hit Four-Year High Amid Iran War Concerns

Swedish apartment prices rose to the highest in almost four years in a sign that a nascent recovery on the housing market continued despite new worries over the economic impact of the Iran war https://t.co/QGVdGR6q1k https://t.co/Pg9NlLqGgB

High‑Inventory States Face 2026‑27 Price Declines

We have some new leaders at the top of the housing inventory charts. 1. Washington: +64% inventory surplus 2. Colorado: +63% 3. Tennessee: +58% These markets have inventory levels more than 50% above the March long-term average. Interestingly enough, Florida has dropped out of the...

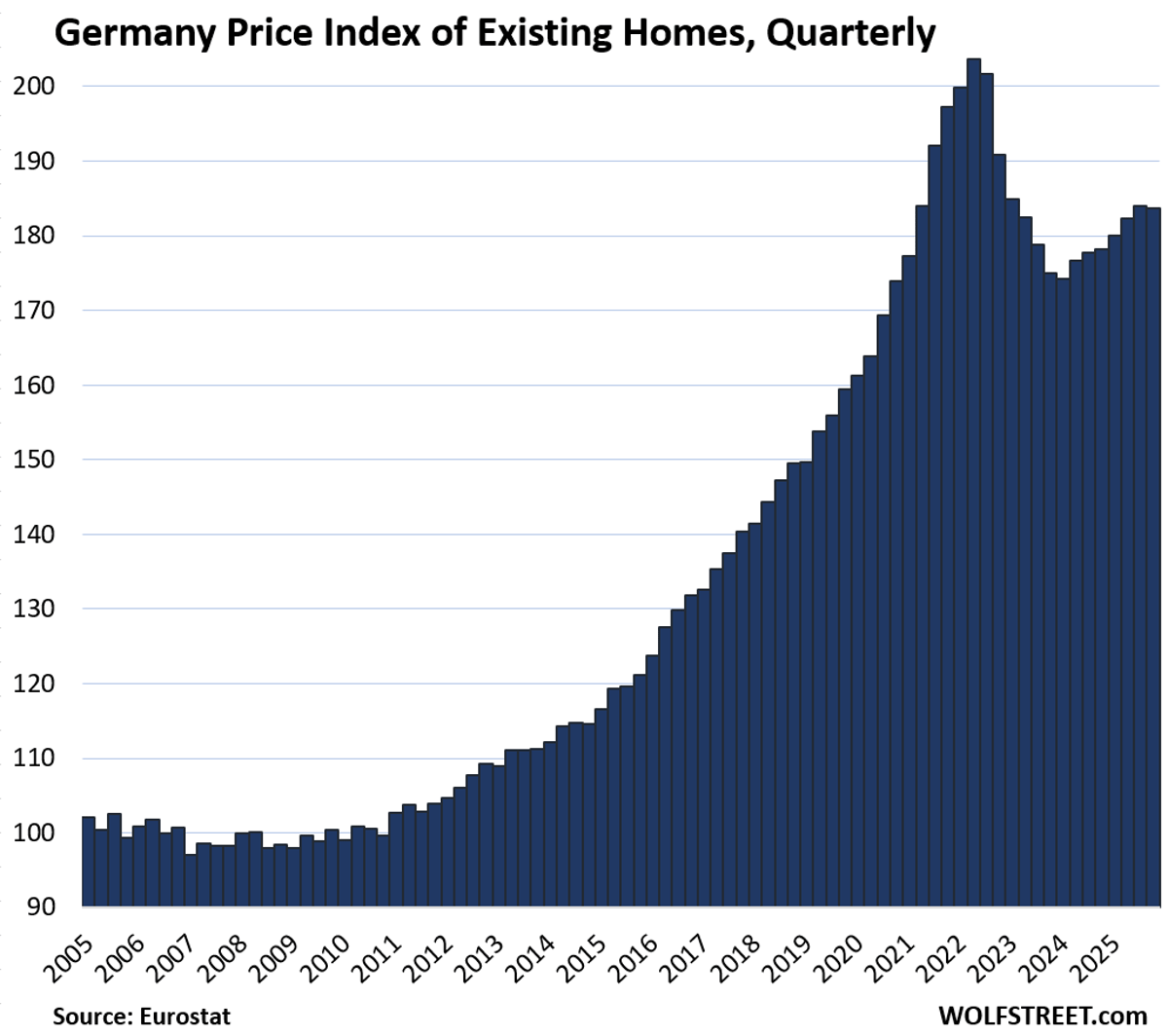

European Home Prices Span Bubbles to 2010 Lows

Home Prices in the 19 Largest European Countries Range from Housing Bubbles to a Market that Fell back to 2010. Here's Germany: https://t.co/aRKT01YIiS https://t.co/yIGmTLgpMC