I'm a Financial Planner: This Is How the Tax Torpedo Targets Wealthy Retirees (and How You Can Step Out of...

The column warns that retirees with roughly $3 million in assets face a series of hidden taxes dubbed the “tax torpedo.” Using a case study of a couple with two‑thirds of their wealth in tax‑deferred accounts, it shows how required minimum distributions, the net investment income tax, and Medicare IRMAA surcharges can quickly elevate marginal rates. The author recommends proactive Roth conversions and modern planning tools to lock in today’s lower brackets. Ignoring these triggers can turn a seemingly comfortable cash flow into a costly tax burden.

Television Academy Endorses Post-Production Tax Credit Bill as Assemblyman Nick Schultz Rallies Support in Burbank: ‘We Should Have Done This...

The Television Academy has officially endorsed Assemblyman Nick Schultz’s AB 2319, a bill that would create a 35%‑50% tax credit for post‑production work done in California, even when the principal shoot occurs elsewhere. The legislation aims to reverse a loss of...

Top-Earning Australians Make Money Very Differently From Typical Workers

The Australian government is set to amend capital gains tax, negative gearing and family‑trust rules in next week’s budget. Analysis shows the nation’s highest earners—those with over AUD 1 million (≈ US $660 k) in total income—derive a large share of earnings from capital gains,...

Already Have Life Insurance? Why an ILIT May Be Worth It

Estate planning now faces state-level estate taxes, especially in New York where the exemption is $7.35 million and a 5% overage triggers tax on the entire estate. Life‑insurance death benefits are generally includable in the decedent’s gross estate under IRC 2042, potentially...

Republican-Led Plan Aims to Preserve 179D Building Energy Deductions, Extend Other Energy Credits

A bipartisan House bill, H.R. 8477 – the American Energy Dominance Act – was introduced on April 23, 2026 to make the Section 179D commercial building energy‑efficiency deduction permanent and to roll back select changes from the 2023 One, Big,...

What Happens to an RESP when a Family Moves to the U.S.?

A Canadian family moved from Vancouver to California, leaving their child Rhodes as the RESP beneficiary. Because Rhodes is now a U.S. resident, any new contributions to the RESP no longer qualify for the Canada Education Savings Grant (CESG). Existing...

An Income Tax Play for Professional Athletes

The article examines how state "jock taxes" hit professional athletes when they change teams via free agency or trades. It outlines the historical rise of these taxes, from California’s 1991 lawsuit to Washington’s 9.9% millionaire levy on a single duty...

India’s New Safe Harbour Rules Create Fresh Tax Dilemma for Multinationals, GCCs

India’s 2026 Union Budget introduced a 15.5% safe harbour margin for IT and ITeS services, undercutting the 16.5%‑18.5% margins typically set in advance pricing agreements (APAs). Multinationals with existing APAs now face a choice: stay locked into higher margins or...

IRS Establishes Program for Rulings on Significant Issues

The IRS issued Rev. Proc. 2026‑21 on May 7, 2026, creating a program that lets taxpayers request rulings on specific, significant legal issues tied to transactions under sections 332, 351, 355, 368, or 1036. The initiative reinstates the practice of issuing letter rulings on parts of integrated transactions, aiming...

Pensions IHT Shake-Up Is ‘Not a Tweak, but a Reset’

Financial advisers have just 11 months to prepare for a sweeping overhaul of how inheritance tax (IHT) applies to pensions, set to take effect in April 2027. Industry leaders at MMI Leeds 2026 highlighted that HMRC will soon release detailed...

Why the R&D Tax Credit Could Bring Back Made in the USA

The Section 41 research and development tax credit, recently streamlined by new legislation, is emerging as a catalyst for reshoring U.S. manufacturing. By delivering six‑figure cash refunds, the credit helps firms offset higher domestic labor costs, upgrade equipment, and buffer against...

Inheritance Taxes, Sweden and Family Businesses

Sweden is debating a reduction of its inheritance tax amid widening budget deficits and soaring welfare spending. The current rate of 20% on estates above roughly €1.5 million (about $1.6 million) has drawn criticism from family‑owned firms that argue it hampers succession...

I'm a Financial Planner: Trump Accounts Are a No-Brainer if You're Eligible (How to Apply)

The Treasury is rolling out a new federally backed savings vehicle called a Trump Account, slated to debut this summer for children born between 2025 and 2028. Each eligible minor receives a $1,000 government seed contribution and can make up‑to‑$5,000...

IRS Plans Settlements in Conservation Easement Cases

The IRS announced a time‑limited settlement program for taxpayers involved in syndicated conservation‑easement transactions that the agency deems abusive. The new website details recent court decisions, highlights inflated valuations, and warns of disallowed deductions, penalties, and back‑dated approvals. Eligible individuals...

Instructions for S Corporation Election Timing- File Form 2553 Correctly

A timely Form 2553 election is essential for businesses seeking S corporation status and the associated pass‑through tax benefits. The IRS requires filing within 2 months and 15 days of the intended effective date, with proper signatures and shareholder consent;...

:max_bytes(150000):strip_icc():format(jpeg)/GettyImages-1426185837-ad8ec5d9806c44bea5b3b107a91a375d.jpg)

Should You Use a Mega Backdoor Roth Conversion for Your Tens of Thousands in Savings?

A mega backdoor Roth lets high‑income earners funnel after‑tax 401(k) contributions into a Roth account, unlocking $30,000‑$35,000 of tax‑free growth each year—far beyond the $7,500 Roth IRA cap. The tactic hinges on a 401(k) plan that permits after‑tax contributions and...

Brazil Tax Reform Regulations: What You Need to Know About April 30, 2026

On April 30, 2026 Brazil issued three comprehensive regulations—Decree 12,955/2026 (CBS), Resolution CGIBS 6/2026 (IBS), and Joint Ordinance MF/CGIBS 7/2026—collectively codifying over 1,200 articles that replace the legacy PIS/COFINS, ICMS and ISS taxes. The new rules introduce a "tax on...

Skadden Explores Cross-Border Tax Complexity for REITs

Skadden tax partner Sarah Beth Rizzo discussed the growing complexity of cross‑border REIT taxation at Nareit’s REITwise 2026 conference. She explained that U.S. REIT qualification rules, built for domestic assets, must be re‑engineered for global portfolios, often requiring private letter...

NPR Went Looking for Polymarket's Panama Headquarters. It's Elusive

Polymarket, a $15 billion‑valued prediction‑market platform, lists its corporate headquarters on the 21st floor of the Oceania Business Plaza in Panama City, an address it shares with more than a dozen other crypto firms. NPR’s investigation found the listed office is...

The R&D Tax Credit Window Is Closing: What CPAs Must Do Before July 6—And What Comes Next

CPAs have until July 6 to amend 2022‑2024 returns under the restored Section 174 rules, enabling both the R&D tax credit and immediate expensing of qualifying costs. The change can generate cash refunds for firms with average gross receipts up to $31 million...

Two Fast-Moving Transfer Pricing Shifts in Canada and India that Can Reshape Pricing Policies

Canada is tightening transfer‑pricing audits by requiring a “delineation‑first” approach that aligns contracts, actual conduct, and value creation, rendering pure benchmark studies insufficient. India’s 2026‑27 budget introduces a 15% cost‑plus safe harbor for routine data‑center services, offering pricing certainty but...

Burlington in the Court of Appeal: New Guidance on Purpose Tests and Access to Treaty Benefits

The UK Court of Appeal in Burlington Loan Management DAC v HMRC clarified that merely obtaining a tax‑treaty benefit does not constitute treaty abuse. The judgment distinguishes between a taxpayer’s motive and the purpose of a transaction, holding that anti‑abuse...

Why some CFOs Stay Far Away From the R&D Credit

The article argues that many CFOs deliberately forgo the U.S. research and development (R&D) tax credit because of high consulting fees, onerous documentation, and lingering audit fears. Structural factors—such as the credit’s design favoring large firms and frequent legislative tweaks—make...

Give More But Pay Less: An Essential Guide to Tax-Smart Charitable Giving in 2026

The 2026 tax year introduces the One Big Beautiful Bill Act (OBBBA), which limits deductible charitable contributions to amounts exceeding 0.5 % of adjusted gross income and caps overall itemized deductions at 35 % for taxpayers in the top 37 % bracket. Cash...

How Landmark Ruling in Orsted Tax Dispute Will Affect Future UK Offshore Wind Projects

The UK Supreme Court ruled that pre‑construction surveys and studies for offshore wind farms do not qualify for capital allowances under the Capital Allowances Act 2001. The decision, arising from Ørsted’s dispute with HMRC, narrows the definition of expenditure “on”...

QSBS Stacking: Leveraging Gifts and Trusts for Additional Section 1202 Exclusions

Section 1202 lets each taxpayer exclude up to $10 million (or $15 million for post‑July 4 2025 issuances) of QSBS gains. Because the exclusion is per‑taxpayer per‑issuer, shareholders can “stack” exclusions by gifting shares to other individuals or placing them in separate trusts. Outright...

Ohio’s Proposed R&D Credit Expansion Could Unlock State Income Tax Savings

Ohio’s House Bill 756, introduced in March 2026, proposes extending the state’s nonrefundable research and development (R&D) tax credit from the Commercial Activity Tax (CAT) to the Ohio state income tax. The change would let firms with little or no...

Bipartisan Bill Would Use Tax Credits to Build US Plant-Based Materials Sector

Two bipartisan congresswomen introduced the Biobased Materials Investment and Production Act, offering a 30% investment tax credit for new or retrofitted biomanufacturing facilities and a production credit of $0.10 per pound of renewable material, capped at $10 million annually. The legislation...

Tax-Managed Long-Short Strategies Gain Traction. Are They Worth the Risk?

Tax‑managed long‑short equity strategies are gaining traction as advisors look for ways to harvest losses and offset large capital‑gain events. Natixis' Gateway Long/Short Extension Strategy posted an 18.69% total return through 2025, edging out the S&P 500’s 17.82% gain. However, fees...

The Contents of Highlights & Insights on European Taxation, Issue 4, 2026

The EU Court of Justice ruled on 12 March 2026 that Spain’s Article 96 exclusions on client entertainment and recreational expenses fall within the stand‑still clause of Article 176 of the VAT Directive. The judgment confirms a functional interpretation of the clause, allowing later‑acceding...

The California Wealth Tax Has a Loophole—Here’s How Much Billionaires Could Save

California’s proposed billionaire tax would levy a one‑time 5% charge on the total global assets of residents with net worths above $1.1 billion. The legislation excludes real property held directly or in revocable trusts, but assets owned through limited liability companies...

The £1m Inheritance Tax-Free Allowance Illusion – Why Many Couples Don’t Get It

The UK’s headline‑grabbing £1 million inheritance‑tax‑free allowance actually comprises two £413,000 personal nil‑rate bands and two £222,000 residence nil‑rate bands, totalling about $1.27 million. The residence component only applies when a couple has direct descendants and when the estate stays below the...

We've All Heard the Buzz About Roth Conversions, But Not Everyone Will Like the Reality

Roth conversions, moving money from traditional IRAs or 401(k)s into a Roth IRA, have surged in popularity as investors seek tax‑free retirement income. The strategy requires paying income tax on the converted amount now, making it attractive only when future...

Wealthy Raid Their Pensions to Avoid UK Inheritance Tax Shake-Up, Advisers Warn

Wealthy UK retirees are accelerating pension withdrawals ahead of a planned inheritance‑tax overhaul, according to financial advisers. The Treasury is expected to tighten rules that currently allow pension funds to pass tax‑free to heirs, prompting a rush to move assets...

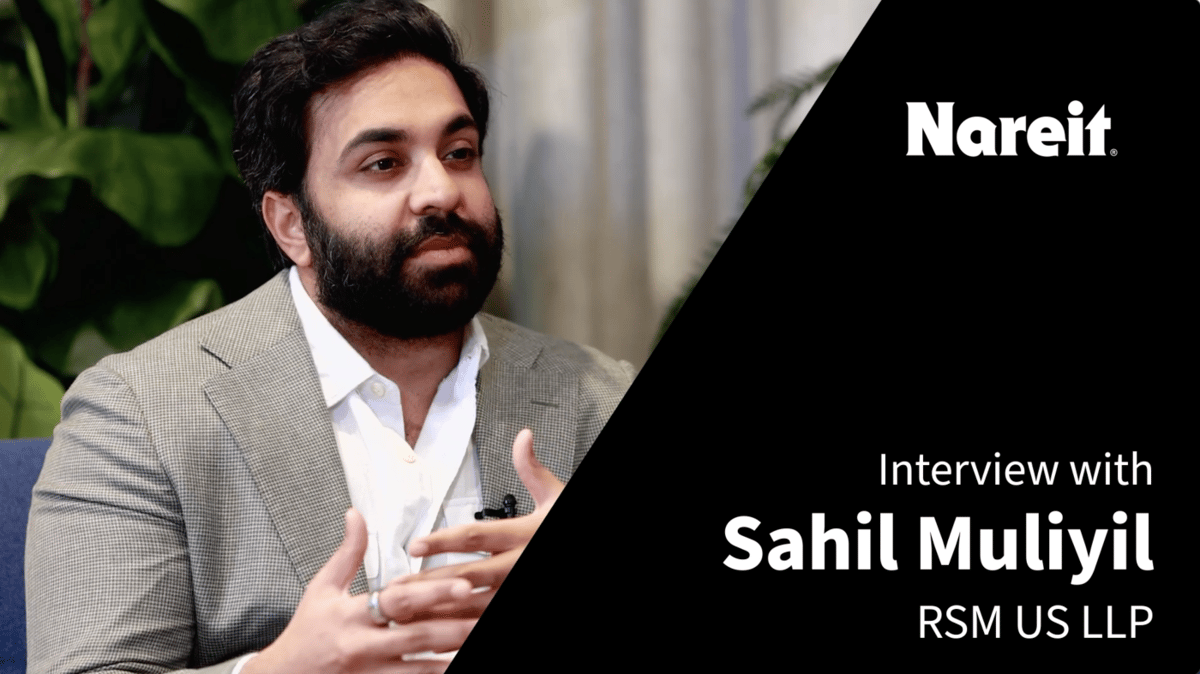

RSM Highlights Hidden Impact of State and Local Taxes on REIT Performance

Saham Muliyil, senior manager of state and local real estate tax at RSM US LLP, warned that state and local taxes (SALT) can materially affect REIT performance across development, operation, and disposition phases. Many investors mistakenly believe REITs are insulated...

Federal Court Shuts Down BVI Tax Escape for Canadian Holding Company

The Federal Court of Appeal overturned a Tax Court decision, holding that DAC Investment Holdings Inc. remained a Canadian‑resident corporation after its continuance to the British Virgin Islands. The court applied the general anti‑avoidance rule (GAAR) to a C$2.36 million (≈US$1.75 million)...

Good Financial Reads: The Business Owner’s Financial Operating System

The article guides small business owners through three critical financial pillars: selecting the optimal retirement plan—SEP IRA, Solo 401(k), or SIMPLE IRA—based on income, employee count, and growth goals; avoiding costly bookkeeping errors, especially the failure to reconcile bank accounts;...

Ask the Tax Editor, May 1: 10-Year Rule for Inherited IRAs

The 2019 SECURE Act eliminated the lifetime stretch for most non‑spousal inherited IRAs, imposing a 10‑year distribution window. Beneficiaries must fully withdraw the account by the end of the tenth year, with annual required minimum distributions (RMDs) only if the...

IRS Provides Way to Extend ERC Disallowance Deadline

The IRS has introduced a new mechanism for taxpayers whose Employee Retention Credit (ERC) claims were disallowed to extend the two‑year deadline for filing a refund lawsuit. Eligible taxpayers can submit Form 907, “Agreement to Extend the Time to Bring...

How Boast Helped Companies Secure $900 Million in R&D Tax Credits Since 2018

Boast’s 2026 R&D Benchmark Report reveals the firm helped North American companies secure close to $900 million USD in research‑and‑development tax credits from 2018 to 2024, with Canada accounting for 45 % of the total. Annual claim values have risen 245 % since...

Billions in Battery Tax Credits Hinge on FEOC Compliance

The Treasury’s new N‑26‑15 guidance turns Foreign Entity of Concern (FEOC) compliance into a project‑level calculation that determines eligibility for the Section 48E investment tax credit and the Section 45X advanced manufacturing credit. Developers must now compute a material assistance cost ratio...

ZigZag Partners Trade Duty Refund for EU Duty Drawback Service

ZigZag has partnered with Trade Duty Refund to launch an integrated EU duty drawback service for UK retailers selling into the EU. The solution blends ZigZag’s returns platform with Trade Duty Refund’s digital claims engine, automating evidence capture and customs...

Mamdani Tax Break Proposal: Could NYC Businesses Leave as Economy Turns Fragile?

New York City Mayor Zohran Mamdani proposes scaling back the pass‑through entity tax (PTET) credit to narrow a growing budget gap. The credit currently offsets New York’s high tax burden for thousands of S‑corporations and LLCs, especially owners earning $300,000‑$500,000....

How GPs Can Use Carried Interest Derivatives for Estate Planning

Venture‑capital general partners are turning to carried‑interest derivatives as a tool for estate planning. By gifting these synthetic contracts, GPs can lock in future profit participation while transferring value to heirs at a reduced tax cost. The strategy leverages the...

IRS Increases Foreign Earned Income Tax Breaks

The IRS issued Notice 2026‑25, raising the foreign earned income exclusion to $132,900 for 2026, up from $130,000. Taxpayers must meet the bona‑fide residence or 330‑day physical presence test and file Form 2555 to claim the benefit. The foreign housing deduction base...

Safehold Discusses Tax Complexity in REIT Joint Ventures and Opportunity Zones

Safehold’s senior tax executive Adam Cohen told Nareit’s REITwise conference that operating partnership (OP) unit transactions have shifted from pure tax‑deferral tools to acquisition‑driven structures, creating new negotiation friction. Sellers increasingly seek to defer taxes, but mismatched depreciation schedules or...

Last-Minute Pension Investing Could Cost Brits £24,000 – What’s a Better Way to Save?

Penfold’s analysis shows that roughly one‑fifth of UK pension contributions are rushed into in March, the final month of the tax year, with single‑payment amounts 4.4 times higher than the monthly average. This last‑minute behavior can erode long‑term returns because it...

House Passes Panetta’s Bipartisan ‘Supporting Early-Childhood Educators’ Deductions Act’

The bipartisan Supporting Early‑Childhood Educators’ Deductions (SEED) Act, championed by Rep. Jimmy Panetta, cleared the House unanimously and now moves to the Senate. The bill expands the existing $300 above‑the‑line educator expense deduction to include pre‑K and early‑childhood teachers, allowing...

IRS Clarifies Tax-Free Educational Assistance Cap to Adjust With Inflation Beginning in 2027

The IRS issued Fact Sheet 2026‑10 clarifying that the $5,250 tax‑free educational assistance limit stays flat for 2026 but will be indexed to the cost‑of‑living adjustment (COLA) starting in 2027. The guidance also makes employer‑paid qualified education‑loan payments a permanent benefit...

Ottawa Cracking Down on 21-Year Deemed Disposition Rule for Trusts: Lavery Lawyer

Canada’s federal government is tightening the 21‑year deemed disposition rule for trusts that hold private‑company shares. New reporting requirements force most express trusts to file T3 returns and disclose key parties, ending the secrecy that enabled last‑minute restructuring. The 2025...