US‑Iran Talks Spark US Equity Rally and Pull Brent Below $99

U.S. and Iranian negotiators signaled a possible cease‑fire extension, sending S&P 500 futures up 0.2% and Nasdaq 100 futures up 0.4% while Brent crude slipped below $99 a barrel. The rally marks the S&P's longest 10‑day winning streak since 2021, underscoring how geopolitics still drive market sentiment.

95% Options Surge: Smart Money Bets Big on a Super Micro Bounce

Super Micro Computer (SMCI) saw a 95% jump in call‑option volume, indicating strong bullish bets despite a recent price slump. The put‑call ratio sits at a bullish 0.46 and short interest remains high at 16.55% of float, creating a classic...

Bitcoin Poised for Short Squeeze, Eyeing $85‑88K

The markets are preparing for a short squeeze on #Bitcoin. The markets have rallied to $75,000 and rejected there. A 'shooting star' was made on the daily timeframe, and people freaked out. However, that's not the only indicator that we should be...

DERIVSOURCE: Credit Default Swaps See Record Trading Volumes, New Products

Credit default swaps (CDS) saw record activity in Q1, with global trading volume surging 69% to $4.5 trillion, eclipsing the previous peak. S&P Dow Jones introduced the CDX Financials index, linking CDS exposure to private‑credit funds such as Apollo Debt Solutions,...

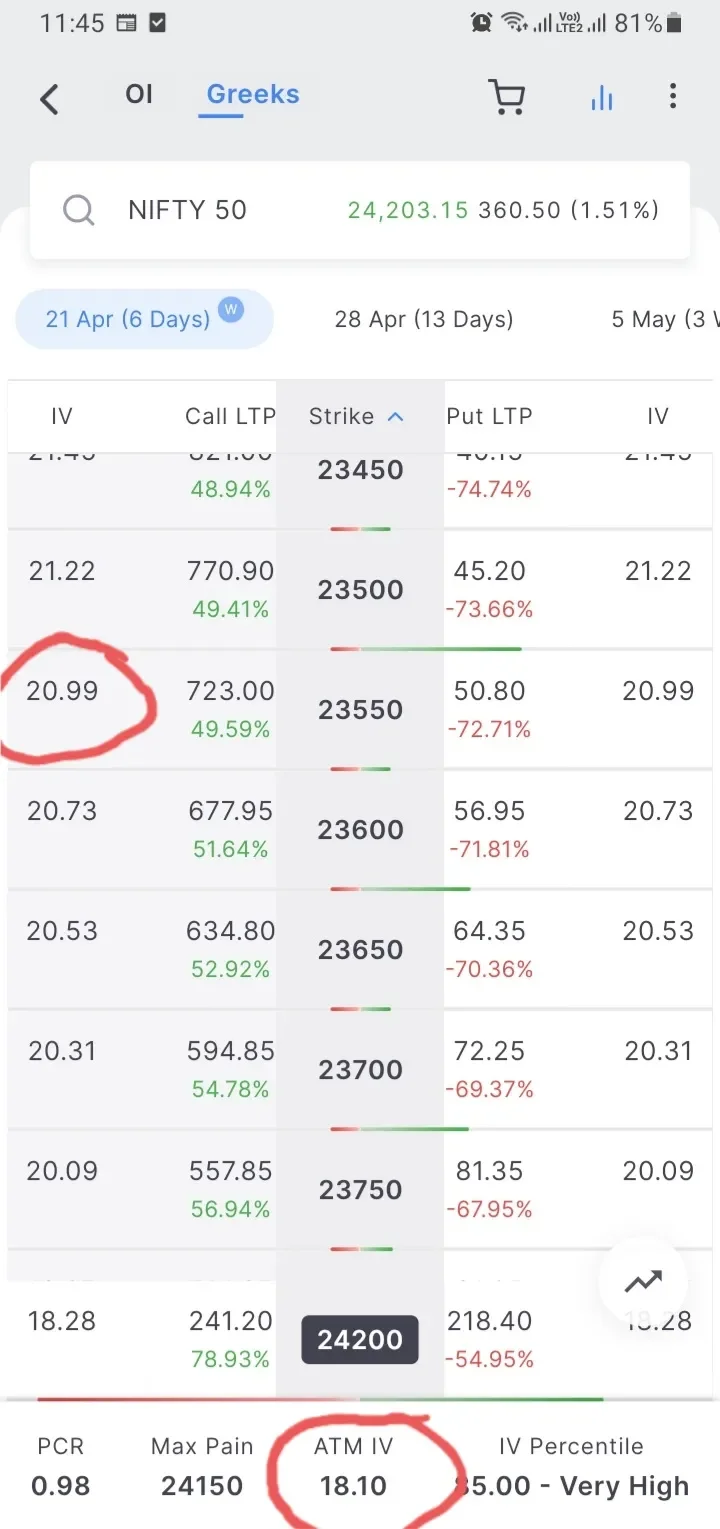

IV Collapse Threatens Nifty50 Call Upside Without Recovery

From Monday’s close, IV on this call has seen a sharp collapse....Despite the gap up, premiums aren’t expanding the way they should. That’s a concern. For this move to sustain, need to see IV on 23550 CE push back above ~25.5. Without...

Deutsche Bank Flags Brent Futures Dip Below $100, Hinting at Energy Stock Rally

Deutsche Bank analysts reported Brent crude slipping below $100 per barrel, with the 6‑month future at $83.55 and the 12‑month at $78.57. The downward‑sloping curve suggests markets view the Middle‑East flare‑up as temporary, a signal that could spark momentum trades...

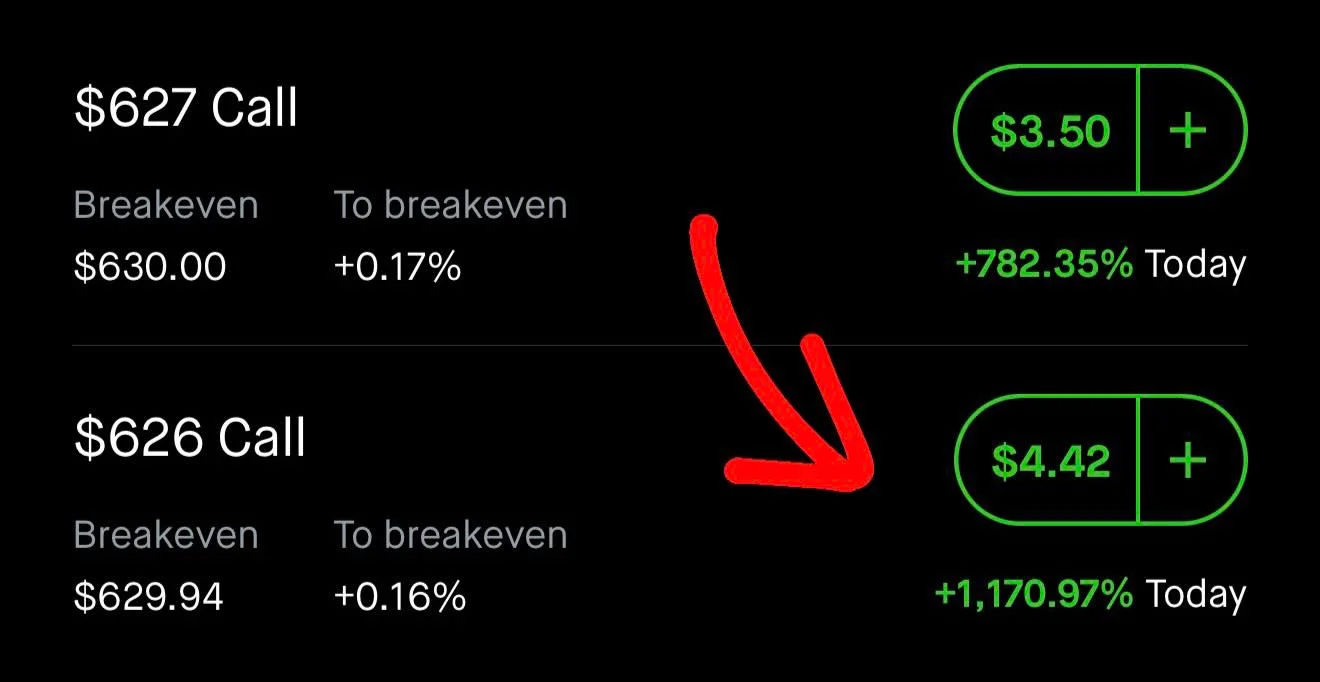

Timing, Not Luck, Drives 10x Options Gains

Is it luck or timing? How some traders make 10x on options in a single trade.

CFTC Weekly Swaps Report Triggers Debate Over Fintech Swap Platforms

The Commodity Futures Trading Commission’s weekly swaps report omitted event‑contract swaps, sparking criticism from market participants and former chairman J. Christopher Giancarlo. The gap highlights regulatory uncertainty as fintech firms roll out bank‑grade swap services, while the EU‑registered Abaxx Exchange...

Ruffer Investment Company Reports Sharp Volatility After US‑Israeli Attack on Iran

Ruffer Investment Company said its March 2026 performance was dominated by the US‑Israeli strike on Iran, which sent crude oil up more than 60% in the month and 94% for the quarter while equities, bonds and even gold fell sharply....

SPY Volatility Near Pre‑war Levels, Gamma Gains Focus

Implied vol on $SPY is practically back to pre-Iran war levels. As vol compresses, exogenous drivers become less dominant, and dealer hedging flows have a greater influence on price action, making gamma exposure increasingly important to monitor.

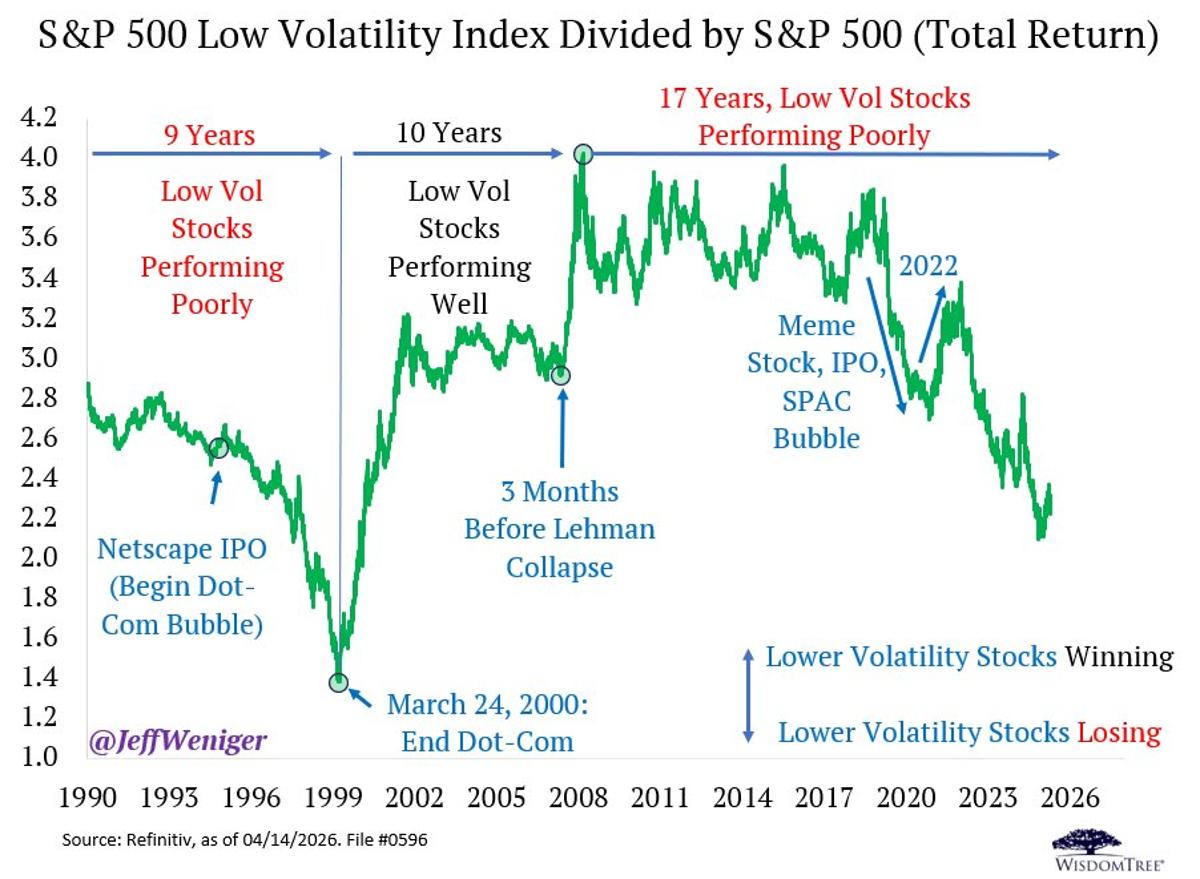

Low‑Volatility Index Underperforms 17 Years, Cycle Uncertain

The S&P 500 Low Volatility Index's underperformance commenced 17 years ago. Let me say it again: seventeen years ago. The previous cycles were 9 years one way, then 10 years the other way. How long this factor can remain washed...

TD and BMO Back New Montréal Exchange Credit Derivatives Product

TD Securities and BMO Capital Markets have been appointed liquidity providers for the Montréal Exchange’s newly launched FTSE Canada Bank Credit Index Futures (BCS). The contract, introduced on April 8, tracks a basket of Canadian bank bond spreads and offers a...

Netflix Trade Aims to Flip $2.50 Loss Into $6 Gain

$NFLX 1/20/26 Earnings Trade, short Aug. 80 puts, long Aug. 100/115 call spreads at $2.50 credit With it back to 200-MA and into next report, can take this off at $6 Turning -2.50 into +6 always nice

Gold & Silver Rally, As Market Digests Cryptic Trump 'Reset' Comment

Precious metals surged on Tuesday, with gold futures climbing $99 to $4,866 per ounce and silver up $3.92 to $79.59 per ounce. The rally coincided with a $7 drop in oil futures, which slipped to about $92 a barrel despite...

The European Market Brief 22: Throw Out The Old Conflict Playbook

In this episode of the European Market Brief, hosts Mark Longo, Murad Asgar (founder of EdgeClear), and Matt Corrin (Eurex V‑Stocks lead) dissect the market turbulence sparked by the U.S.–Iran conflict and the Strait of Hormuz blockade. They highlight unprecedented...

BUCK Offers A 7.55% Yield, But Don't Ignore The Competition

Simplify Treasury Option Income ETF (BUCK) delivers a 7.55% trailing yield by combining short‑term Treasuries with option spreads. Since its launch in October 2022, BUCK has outperformed the Treasury bill benchmark by 60 basis points on an annualized basis, though it...

Portfolio Shifts to Cash, Short US Equities, and Put Spreads

On the close. Raised cash in Beta by 10% of AUM trimming commodities, gold, and US and ROW Equities. Up to 30% Cash. In Alpha went max short US Equities. Two and Six Month Put Spreads totaling 4%...

May Rollover Anchors WTI Futures, Masking Underlying Supply Risks

The May WTI crude oil futures contract is entering a rollover with an $8 backwardation spread, temporarily anchoring front‑month prices and obscuring underlying supply concerns. Analysts warn that once the rollover clears, prices could snap back toward physical market fundamentals,...

Bitcoin's $76,000 Breakout Fails but a Rare Signal Is Hinting at Major Market Bottom

Bitcoin briefly breached the $76,000 resistance on April 14 but quickly retreated to around $74,000, extending a two‑month struggle to sustain a true breakout. Meanwhile, Binance’s Bitcoin perpetual funding rates have stayed negative for 46 consecutive days, a streak last...

Institutions Hedge Tail Risk as SKEW Near Resistance

SKEW is pinned just below 5-year resistance at 156. Institutions are quietly paying up for far out-of-the-money put protection. They're hedging a low-probability, high-impact tail event. That's not typically a buy-the-dip environment. Time will tell.

#58762

iShares Core High Dividend ETF (HDV) announced a 5‑for‑1 stock split effective April 29, 2026. The split will increase the share count fivefold while proportionally reducing the price per share. OCC will adjust all HDV options on the ex‑date, changing the contract...

Goldman Sachs to Use Options Strategy for Planned Bitcoin Income ETF

Goldman Sachs has filed with the SEC to launch a Bitcoin Premium Income ETF that will generate yield by selling call options on Bitcoin‑linked exchange‑traded products while keeping at least 80% exposure to the crypto asset. The fund’s “overwrite” strategy...

Profit Spikes Aren't the Lesson—Focus on Strategy

From $400 to $1,300 in 2 Days… But That’s Not the Point #optionstrader #tradingstrategy #stocks #tradebreakdown

GMX Rolls Out 24/7 Gold and Silver Trading

GMX has introduced synthetic gold (XAU/USD) and silver (XAG/USD) perpetual contracts on Arbitrum, pulling more than $10 million in trading volume on day one. The contracts settle on‑chain using WETH‑USDC liquidity and rely on Chainlink Data Streams for price accuracy. GMX...

Gold Stock Flashes An 87% Annualized Return Opportunity With This Put Option Strategy

Orla Mining (ORLA), a low‑cost gold producer in Mexico, is trading above its 50‑day moving average with strong accumulation. A cash‑secured put at a $17.50 strike generates roughly $125 premium, delivering a 7.69% return on capital, which annualizes to about...

🎯Take Profit Alert HOOD. HUT, OKLO Cash Secured Puts

A trader announced the closure of three cash‑secured put positions on Robinhood (HOOD), Hut 8 Corp (HUT) and Oklo (OKLO) after capturing 76.67%, 94.19% and 78.24% of the premiums respectively. Each option moved deep in‑the‑money, making further upside limited while...

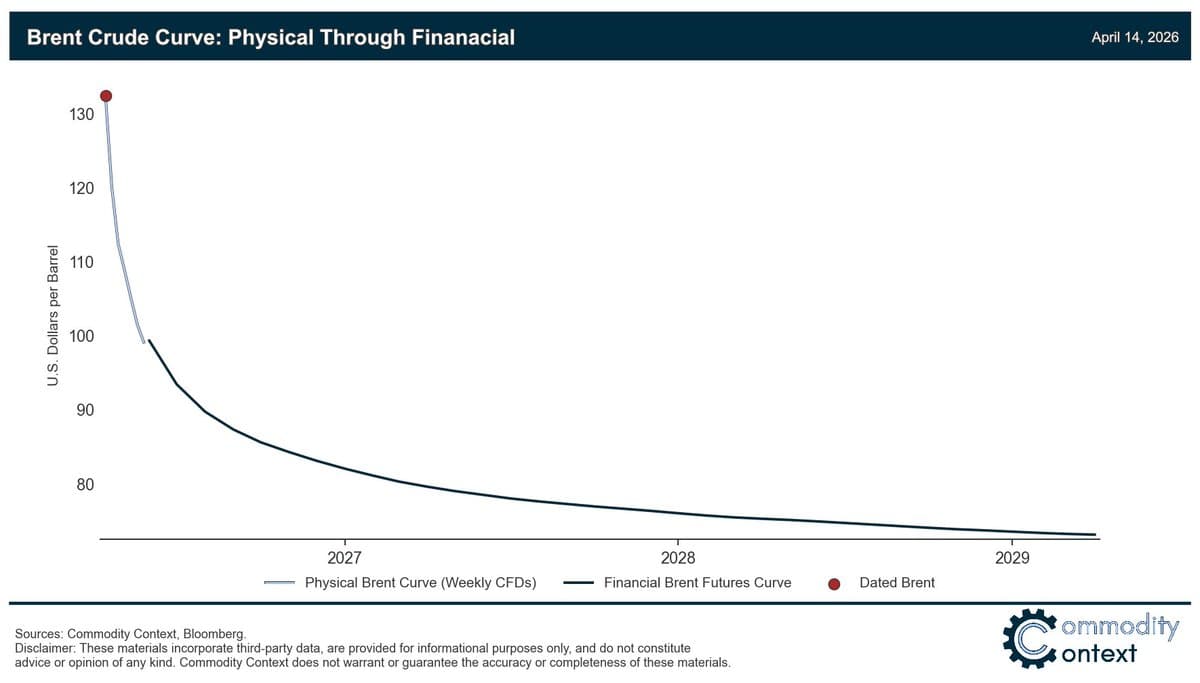

Extreme Brent Backwardation Pushes Physical Prices $20 Above Dated Brent

Charting the Brent complex today to add some context to the numbers bouncing around. Pretty well everything weird in the current oil market can be explained via *extreme* backwardation (i.e., near-term delivery premia), and as you can see the intense futures...

#58761

The Options Clearing Corporation (OCC) announced that BBBY2 options will now settle with a deliverable of 19 Bed Bath & Beyond (BBBY) shares plus a cash‑in‑lieu amount of $4.33 per contract. The cash portion, based on a $4.66 per‑share price,...

Earn $2/Hour via Funding Fee on Leveraged Positions

Just look at this funding fee, if you know how to make money from funding fee, this is one of your biggest opportunities. Right now, the funding fee is about $2 per hour. What this means is: if you open a...

Low Implied Correlation Reveals High Single‑stock Volatility

From 3M implied correlation of .14 to avg single stock vol: √(15.6²/.14) Moontower V2 is Agent forward yo https://t.co/HLau7SGzXo

The Hidden Chain Connecting VIX to Your SPX Puts

The article explains how VIX futures are mechanically linked to SPX options through a chain of dealers, replicators, and carry traders. Five distinct counterparty types absorb VIX futures pressure, with variance dealers playing the pivotal role by replicating the VIX...

SPY 8‑MA at 676, Trim Positions

SPY 8-MA way back at 676 now, quite extended near-term along with that NYMO, not a bad time to trim, take profits, write covered calls imo, annual outlook to start the year put out SPX 6350 as the BTFD level...

Huge FX Options Set to Expire Tomorrow Across Major Pairs

Interesting FX options that expire tomorrow 1.64 bln euros $1.18 2 bln euros at $1.1750 $1.5 bln at JPY158.85 A$2.1 bln $0.7125-30. https://t.co/SuL5KID8ce

Options Remain Red-Hot on AI Favorite META

Meta Platforms expanded its CoreWeave partnership to a $21 billion commitment, up from $14.2 billion, bolstering its AI compute capabilities. The move follows multi‑year deals with AMD and Nebius and comes as the stock climbs roughly 10% this month despite a jury...

Netflix Earnings Spark Surge in July Call Buys

Netflix (NFLX) earnings week sees 135,000 July 120/140 call spreads buy as 90K August call spreads adjust higher that nailed the lows

FIG Plunge Redirects Put Buyers to Anthropic News

$FIG smashed lower, big put buyers yesterday into Anthropic news today (though other providers thought they were sold) https://t.co/IuNwoKYfvh

CME Group to Debut Eris SOFR Swap Options on June 16, Expanding Interest‑Rate Toolkit

CME Group announced that it will launch Eris SOFR Swap options on June 16, 2026, pending regulatory approval. The new options sit on a futures series that has already seen over 10 million contracts traded and a March‑2026 open‑interest peak of...

SPX Straddle Cheap Despite Recent

Tomorrows SPX straddle is $41/58bps SPX last 2 days: +111bps +100bps also VIX EXP tomorrow

XBI Dec $135 Calls Added After 120% Surge

Biotech (XBI) 10,000 December $135 calls bought adjusting the $120 calls from Oct. 8th that are up over 120%, a top Q1 group with M&A and approval upside

Wall Street Futures Slip as Middle East Tensions and Oil Prices Weigh on Markets

U.S. stock futures fell sharply on Tuesday, with Dow futures off 484 points, the S&P 500 down 48.25 points and the Nasdaq 100 sliding 182.25 points. Traders cited renewed Middle East tensions, Brent crude hovering around $102 a barrel, and...

Buy Deep OTM SPX Puts on Potential Tanker Attack

a pretty good asymmetric trade would be buying some WAY OTM SPX puts for May on the off chance Hegsweth decides to torpedo a Chinese oil tanker... thoughts?

Ethereum 10% Swing Threatens $4.3B in Positions

🚨UPDATE $1,550,000,000 in shorts will get liquidated if $ETH spikes 10%. $3,800,000,000 in longs will be wiped out if Ethereum drops 10%. https://t.co/CYw0mYMcTp

Financial Risk Management Platform Pillar Raises $20M Seed in Round Led by A16z

Pillar, a financial risk‑management platform for commodity‑driven firms, announced a $20 million seed round led by Andreessen Horowitz, bringing its total funding to $23 million. The AI‑powered solution automates hedging by ingesting contracts, ERP data, spreadsheets and even WhatsApp messages to continuously...

Amazon Call Spread Positioned for Earnings Swing

AMZN earlier a buy of 37,500 May 9th (W) $260/$290 call spreads targeting earnings adjusting June 225/265 spreads

Strategy Equals Wide Butterfly Plus Eight Strangles

i won't comment except to point out that this is algebraically equivalent to buying 1 really wide butterfly and 8 strangles (the butterfly is technically an "iron fly") Also, they used the word "deep" when traders say "far", so the target audience...

#58759

Monroe Capital Corporation (MRCC) announced that its listed options will be adjusted following the anticipated merger with Horizon Technology Finance Corporation (HRZN). Effective the first business day after the merger, the option symbol changes to HRZN1 and the contract multiplier...

Falling VIX Masks Ongoing Geopolitical Risks

$VIX spiked to 29.3 in late March. It's now at 18.75. The market is telling you the fear is gone. But is it? VIX dropping while geopolitical risk stays elevated and Q1 earnings loom is either a relief rally — or dangerous...

SynFutures Entropy – The Gas Problem That Kept Orderbooks Offchain

SynFutures, a permissionless perpetual DEX backed by Pantera, Polychain and Dragonfly, launched Entropy on Base to make on‑chain order‑book gas costs flat regardless of depth. The contract‑level algorithm processes order‑book data off‑chain, aiming to eliminate the gas‑limit barrier that pushed...

BingX Launches Zero-Fee TradFi Futures While Maintaining Full Partner Commissions

BingX announced a zero‑fee trading campaign for its TradFi Futures platform that runs from April 13 to July 31, covering more than 100 traditional assets such as commodities, forex, stocks and indices. While users trade without fees, the exchange subsidizes the cost...

Adobe Continues to Struggle. This Options Trade Doubles Down on a Potential Rebound

Adobe's shares have slipped further amid market volatility, prompting trader Nishant Pant to propose a second bull call spread at lower strikes. The 235/240 May‑8 spread can be entered for about $2.50, offering a potential $2.50 profit if the stock...