Today's Personal Finance Pulse

New student loan repayment options debut on July 1

Starting July 1, borrowers will be offered two new repayment plans and must choose the option that best fits their financial situation. The change aims to give borrowers more flexibility in managing loan payments.

Starting to Invest in Your 40s? Here’s What It Could Take to Catch Up

Investing in your 40s may feel late, but time remains a powerful ally when contributions are consistent. Most employers (over 80%) offer a 401(k) match averaging just under 5%, essentially free money that can boost early savings. A modest $50 weekly for ten years can grow to roughly $42,600, outpacing a $100‑weekly five‑year plan by more than $10,000 thanks to compounding. Automating contributions and using low‑fee index funds can lock in these gains without complex strategies.

89,720 PSLF Buyback Applications Are Pending — But Many Borrowers Won’t Need Them

The episode explains that 89,720 Public Service Loan Forgiveness (PSLF) buyback applications are pending, but many borrowers won’t need the buyback because they’ll reach the 120‑payment threshold through regular payments before their applications are processed. The Department of Education is...

Trump Signs Order Creating TrumpIRA.gov, Offering $1,000 Annual Match

President Donald Trump signed an executive order on April 30 to launch TrumpIRA.gov, a government‑backed website that will let workers without employer‑sponsored plans open low‑cost IRAs. The platform will deliver a Saver’s Match of up to $1,000 per year for...

Huge Savings, Tiny Emergency Fund

You’re 33, Senior SWE, $250k TC. Renting in Austin. No kids yet. You have $280k in your 401k + brokerage. Your emergency fund is $400. **Here’s the trap**:

Diversify to Avoid Losing Everything when One Investment Crashes

When you concentrate a large portion of your money into one asset, you don’t have much to fall back on if that investment plummets. https://t.co/ZmzFL1fdHb

I’m a Retirement Expert Who Just Turned 65. Here’s the Advice I’m Actually Following

The author, a longtime retirement writer, turned 65 and shifted from theorizing to living retirement. He distills five durable lessons: keep portfolios simple with low‑cost ETFs and a trusted adviser, build risk capacity rather than just confidence, resist reacting to...

Best Money Market Account Rates Today, May 2, 2026 (Best Account Provides 4.01% APY)

Money market account (MMA) rates have rebounded, with the national average at 0.57% APY—up from 0.07% four years ago—while several banks now offer over 4% APY. TotalBank leads with a 4.01% APY, requiring a $2,500 balance, and Brilliant Bank follows...

4 Ways to Become Wealthy That No One Taught You In School, According to Charlie Munger

Charlie Munger outlines four wealth‑building principles that run counter to textbook finance. He urges investors to concentrate capital on a few high‑conviction ideas rather than diversifying indiscriminately. He stresses buying businesses with durable, high return on invested capital (ROIC) and...

To Love, Honor and to Pay: 4 Ways to Keep Wedding Costs From Ruining Wedded Bliss

Wedding expenses in the United States average roughly $36,000 and have been climbing as inflation pushes up vendor prices for flowers, food, and staffing. About 30‑40% of couples count on parental contributions, yet many now shoulder the full cost themselves....

New Free Financial Advice Plan Aims to Help Britons Build Savings

The UK Financial Conduct Authority has launched a regulated "targeted support" service that lets banks, building societies and platforms provide free, commission‑free investment suggestions to customers with cash savings. The scheme, aimed at the estimated 7 million adults holding £10,000 (≈ $12,500)...

Saving for Grandchildren

The article outlines four tax‑advantaged ways to save for a grandchild—529 plans, UGMA custodial accounts, Coverdell ESAs, and the newly introduced Trump accounts. It details each option’s contribution limits, tax benefits, and withdrawal rules, highlighting the Trump account’s $1,000 government...

Wall Street Trap

May 1, 1975 marked the SEC’s deregulation of brokerage commissions, sparking the rise of discount brokers and lower trading costs for investors. Decades of research, from Alfred Cowles to Barber and Odean, show that individual stock‑picking and active fund management consistently underperform...

Your Initial Savings of ₹20 per Day Can Help in Getting a ₹6 Lakh Monthly Pension. Here's How

A 30‑year‑old investor who saves roughly ₹20 a day and starts a ₹6,000 monthly equity SIP can amass about ₹9 crore (≈ $1.1 million) over 30 years by applying a 10% annual step‑up and assuming a 15% return. The corpus, invested in a systematic...

Kevin O'Leary Unveils 60/20/20 Asset Allocation Blueprint for Retail Investors

Kevin O'Leary disclosed his personal investing formula on The Iced Coffee Hour podcast, outlining a three‑bucket portfolio of 60% equities, 20% fixed income and 20% alternatives. He tied the mix to dividend‑focused stocks, a 4.5% 10‑year Treasury yield and disciplined...

High‑Yield Savings Reach 4.21% APY as Fed Eases, Ten‑Fold National Avg

Axos Bank now offers a 4.21% APY on its high‑yield savings account, the highest rate available in May 2026. The rate is more than ten times the FDIC‑reported national average of 0.38%, reflecting a brief window of elevated yields as...

‘I’m Very Late to the Game’: I’m 48, Earn $65,000, Have $48,000 in Debt and No Retirement. Am I Doomed?

A 48‑year‑old wine director earning $65,000 annually faces $48,000 of mixed debt and no employer‑provided retirement plan. The writer lives rent‑free in a family‑owned home, giving a low cost of living but no savings or investments. Financial advice emphasizes eliminating...

![T-Mobile Money Review – Earn 4% APY On Balances Up To $3,000 [New Negative Changes From June 1]](/cdn-cgi/image/width=1200,quality=75,format=auto,fit=cover/https://www.doctorofcredit.com/wp-content/uploads/2018/11/t-mobile-money.png)

T-Mobile Money Review – Earn 4% APY On Balances Up To $3,000 [New Negative Changes From June 1]

T‑Mobile Money, the telecom‑backed digital checking account, will slash its Annual Percentage Yield on most balances to 1% starting June 1, 2026. The 4% APY on the first $3,000 of a checking balance remains only for customers who deposit at least $200...

How (and when) to Dispute a Credit Card Charge

The Fair Credit Billing Act (FCBA) gives consumers the right to dispute unauthorized, incorrect, or undelivered credit‑card charges. Cardholders should first contact the merchant, but if the issue isn’t resolved they can file a dispute with the issuer, typically online,...

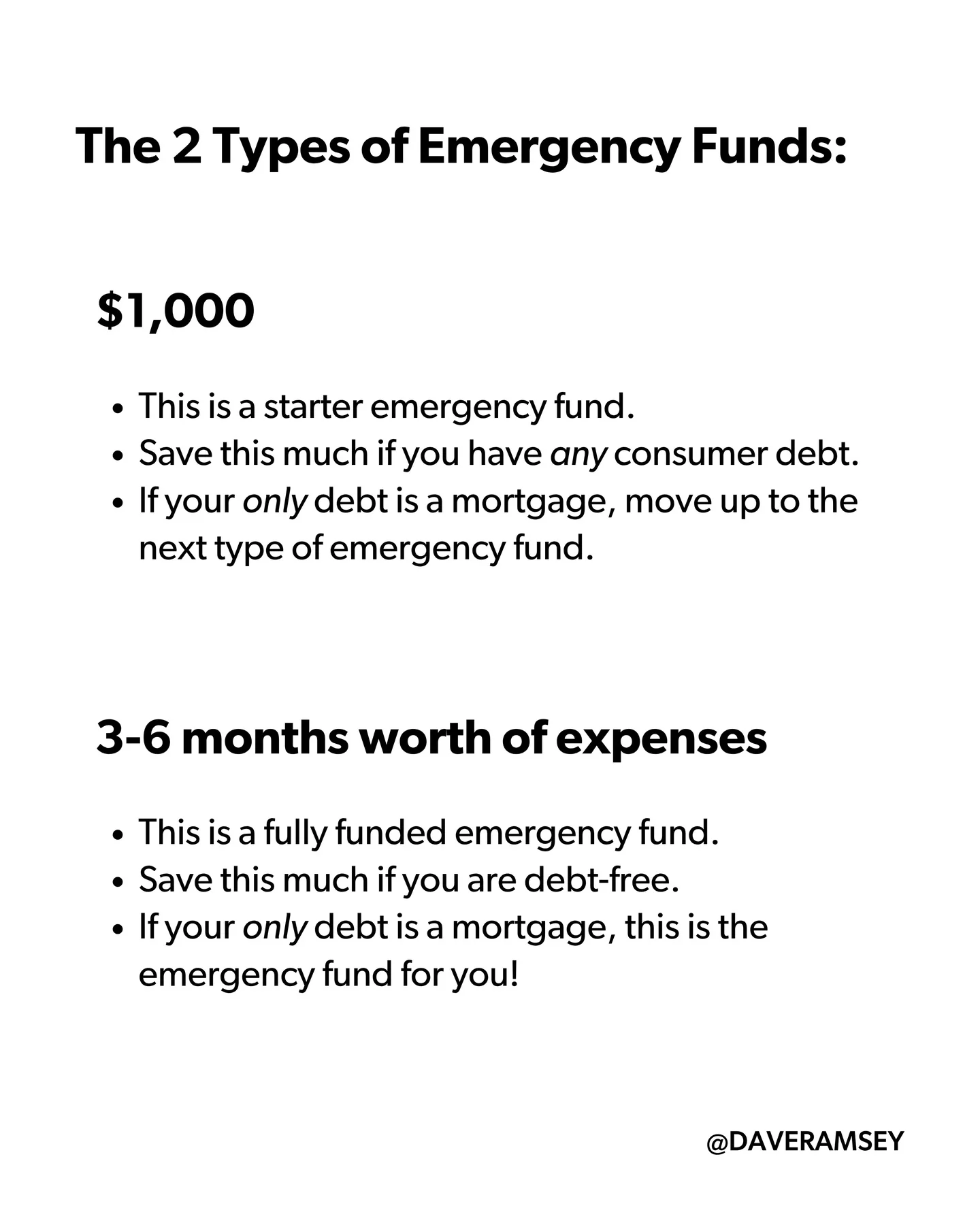

Emergency Fund: Your Safety Net for Life’s What‑Ifs

An emergency fund is insurance between you and the "what ifs" in life. It's important to have one while you're walking the 7 Baby Steps.

1977: Ask Farnoosh: How Much Should We Pay for College? Plus: Her Investments Went Missing

In this episode Farnoosh Torabi tackles the looming decision of college costs, urging listeners to treat college choice as their first major financial decision and to weigh return on investment. She shares a cautionary story about a woman whose investment...

SCHD Edges Out HDV on Yield and Returns, But HDV Leads Recent Performance

Schwab U.S. Dividend Equity ETF (SCHD) delivers a 3.3% yield, a lower expense ratio and more than 3 percentage points of annual outperformance over the past decade versus iShares Core High Dividend ETF (HDV). Yet HDV has outpaced SCHD by...

Affluent Shoppers Trim Daily Costs to Fund Luxury Travel and Experiences

Erin O’Connor‑Bell of Aprio Wealth Management says high‑income consumers are deliberately skimping on groceries and household goods to keep money for premium travel and experiences. The trend highlights a shift in how affluent families balance cost‑of‑living pressures with discretionary spending.

Vanguard Total Stock Market ETF Tops Picks Under $500 Amid Earnings Surge

Analysts recommend Vanguard Total Stock Market ETF (VTI) as the best sub‑$500 ETF, citing 15% Q1 earnings growth for the S&P 500, forward P/E near historical norms, and a 0.03% expense ratio. The pick balances geopolitical headwinds and rising oil...

Skip Dynamic Currency Conversion, Save on Every Purchase

Europe’s most expensive button 👆 It’s called Dynamic Currency Conversion, and pressing USD costs you way more. ❌ A worse exchange rate ❌ A ~3% markup fee The fix: ✅ Pay in local currency abroad ✅ Use a card with no foreign transaction fees Save this for...

Why Tax-Efficient Retirement Income Is About Structure

The article argues that tax‑efficient retirement income hinges on the overall structure—risk allocation, account placement, and withdrawal sequencing—rather than isolated tax tricks. It stresses that a proper asset‑allocation mix is the foundation, then recommends holding growth‑oriented funds in taxable accounts...

Who Pays Property Taxes on a Land Contract? Rules and Examples

Land contracts let buyers gain equitable ownership while the seller retains legal title, but property tax responsibilities usually fall on the buyer. The contract may dictate direct tax payments, seller‑collected payments, or an escrow arrangement, making precise language essential. Failure...

Treasury Hikes I Bond Rate to 4.26%, Fixed Portion Stays Same. What It Means for Savers

The U.S. Treasury lifted the Series I savings‑bond composite rate to 4.26%, up from 4.03%. The fixed‑rate component, however, remains unchanged at 0.9% for bonds issued through October 2026. I Bonds continue to offer inflation‑linked returns, tax‑free state and local treatment,...

Prioritize Time Horizon Over Rate Forecasts in Bonds

When It Comes To Bonds, Don't Be A Hero: Why taking a strategic approach to bond investments based on an investor's time horizon and cash needs could be superior to a tactical approach focused on anticipating future interest rate moves....

#711: Is a Computer Science Degree Still Worth the Debt?, With Ron Lieber

In this episode, host Paula Pant talks with New York Times financial journalist Ron Lieber about whether a computer science degree—and college education more broadly—is still worth the debt in today’s volatile labor market. Lieber emphasizes that while a bachelor’s...

Markets Have Felt Shaky for Months, but the Returns Tell a Very Different Story

Despite months of headline volatility, federal Thrift Savings Plan (TSP) funds have posted solid gains this year. The C Fund swung from a 4.3% loss at the end of Q1 to a 4.5% gain by mid‑April, while the S Fund...

Big‑Tech Employees Use Simple Playbook to Earn Extra Income

To anybody at Apple, Amazon, Meta, Google, Microsoft/LinkedIn, Broadcom, Salesforce, and a handful of other big tech companies Here's the general playbook that people I work with are running (w/o going into Airbnbs/short-term rentals or starting a business):

The Crash Cart that Taught Me Physician-Led Investing

Physician‑led investor Harsha Moole describes how a network of 200+ doctors identified a startup that automates hospital crash‑cart inventory, raising compliance from the national 70‑75% average to near‑100%. The team validated the product with 17 frontline clinicians before investing, then...

10 Best Low-Risk Investments in May 2026

Tom Lee told CNBC that easing geopolitical tensions, a softer private‑credit market and clearer Federal Reserve leadership are reducing risk, allowing the S&P 500 to target above 7,700. He highlighted AI‑driven productivity as a new engine for earnings growth in...

Open-Source AI Portfolio Advisor Runs on $1/Month

I built a system called Sheet Advisor and I'm open-sourcing it today. The idea: you bring an investment thesis, Claude helps you turn it into an actual strategy with specific positions and rationale for each. Then it watches your portfolio every...

23 Habits That Built My $1M Net Worth

I built a $1M net worth in 7 years. I didn't come from money. I didn't time the market. I didn't get lucky. Here are the 23 financial habits that made my family wealthy:

Generative AI Cuts Home Renovation Regret, Saving Users $371 Annually

Adobe's latest research shows that generative AI tools are now used by 49% of American homeowners for renovation projects, trimming average annual expenses by $371. The technology also stopped 62% of users from making purchases they later regretted, signaling a...

Michigan Treasury Sends 27,000 Wrong Tax Refund Checks, Triggers Consumer Alerts

The Michigan Department of Treasury accidentally mailed about 27,000 incorrect tax‑refund checks and 27,000 mistaken “Notice of Adjustment” letters. The blunder has sparked consumer‑protection warnings as taxpayers risk cashing fraudulent checks or paying unnecessary penalties.

We Can Return to 20-Year Mortgages

John Wake argues that the U.S. housing market could revive 20‑year mortgages, a shift that would cut total interest without raising monthly payments. Between 2018 and 2021, falling rates made a 20‑year loan financially equivalent to a 30‑year loan. By...

Why Saving The First $10,000 Is Critical

Saving the first $10,000 is presented as the cornerstone of financial security, especially for high‑income professionals who often overlook basic cash reserves. The article highlights that an emergency fund covering three to six months of expenses protects against income volatility...

Biking Saves Money—Fiscal Conservatives Misread the Math

“If you care about the bottom line, budgets & taxes, then you should care about urban biking, because it’s a money saver. It’s ironic when so-called fiscal conservatives attack biking, when their efforts just show a lack of understanding of...

Baby Steps

A Canadian parent wants to help her 16‑year‑old daughter start investing before she can open a TFSA. The article explains that minors can contribute to a RRSP if they have earned income and file a tax return, and that parents...

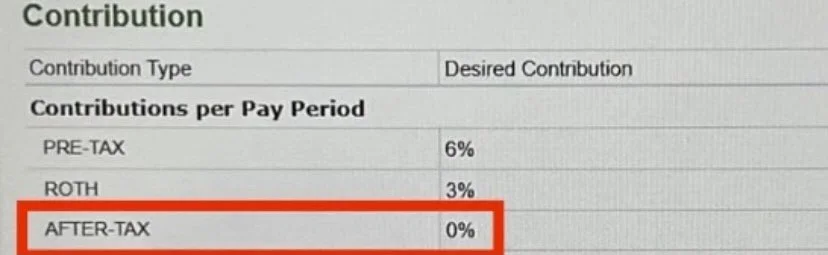

Mega Backdoor Roth: Boost Roth Savings via After‑Tax 401k

Does your 401k have an "after-tax" account? If so, you can use the Mega Backdoor Roth strategy to invest $40,000+ to a Roth account in addition to your regular contributions. It's an amazing strategy to minimize future taxes on growth for high...

Good Financial Reads: The Business Owner’s Financial Operating System

The article guides small business owners through three critical financial pillars: selecting the optimal retirement plan—SEP IRA, Solo 401(k), or SIMPLE IRA—based on income, employee count, and growth goals; avoiding costly bookkeeping errors, especially the failure to reconcile bank accounts;...

Old-Fashioned Frugal Living Tips

The piece revisits classic frugal‑living habits—using items fully, cooking at home, repairing instead of replacing, reusing, careful spending, home gardening, buying only necessities, DIY creation, regular small savings, avoiding debt, choosing durable goods, and sharing. Each tip is framed as...

Use an LLC for Crypto to Protect Privacy and Taxes

Personal name XRP sales get you a standard deduction and full exposure to creditors and scrutiny. The LLC gives you anonymity, creditor protection, and actual tax strategy. Borrow against the position, generate income through DWP products, or set a limit...

Monthly Check‑Ins Keep Your Finances on Track

Doing a quick assessment one or two times a month can help you stay on top of your finances and address any weaknesses in your savings and spending strategies. https://t.co/9cnFCvqWhZ

Bitcoin for Everyday Investors: How to Think About Risk, Timing, and Size

The article frames Bitcoin as a high‑risk, high‑volatility satellite asset rather than a core holding. It advises investors to assess personal risk tolerance, use structured entry such as dollar‑cost averaging, and size the position so a steep drawdown won’t jeopardize...

Maine Launches Paid Family Leave, Offering Up to 12 Weeks of Wage Replacement

Maine’s paid family‑leave program went live on May 1, allowing employees to take up to 12 weeks of partially paid leave for childbirth, illness or caregiving. The state expects 22,000 workers to use the benefit this year, with projected payouts of...

SOXX vs IYW: Cost, Concentration and AI Exposure Shape ETF Choice

Fool.com analysts released a side‑by‑side analysis of the iShares Semiconductor ETF (SOXX) and the iShares U.S. Technology ETF (IYW), showing SOXX’s 0.34% expense ratio and near‑150% one‑year return versus IYW’s broader 0.38% fee and lower volatility. The report underscores how...

Utility Bills Are Likely to Be Higher This Summer. Here’s What You Can Do.

The National Energy Assistance Directors Association forecasts an 8.5% rise in average U.S. electricity bills this summer, reaching $778 for the June‑September period. Southern states face steeper hikes, with Florida, Georgia and the Carolinas projected at $860 (13.5% increase) and...