Ooh Media Drops as Bidder Backs Off

Ooh Media’s shares dropped 8.2% after The Australian reported that I Squared Capital, one of two bidders, is losing interest in the outdoor‑advertising firm. ARN Media fell 9.5%, pushing its market capitalisation below AU$70 million (about US$46 million). The declines came amid broader weakness in Australian media stocks, with Southern Cross Austereo and Nine also slipping. The Unmade Index fell 2.6% to 376.1 points, marking one of its steepest daily drops.

Lumine Buys Synamedia Video Net Business

Lumine Group announced the acquisition of Synamedia’s video network business, which will continue operating under the Quortex brand. The deal represents Lumine’s sixteenth carve‑out transaction and deepens its media ecosystem across video processing, broadcast delivery and live streaming. Financial terms...

Boroo’s Bid to Buy Former Eagle Gold Site Raises Questions Among Miners

Private investment firm Boroo has signed an exclusivity agreement with PwC to evaluate buying the former Eagle Mine in Yukon, a site devastated by a 2024 heap‑leach pad landslide. The Yukon government has earmarked US$220 million for remediation, while a 2024...

PE Firm Open Road Ventures Acquires Intermodal 3PL Double-Stack

Open Road Ventures, a middle‑market private‑equity firm, announced its first acquisition—intermodal freight broker Double‑Stack Logistics. Double‑Stack distinguishes itself by owning more than 150 intermodal containers and maintaining direct relationships with Class I railroads. The deal, whose financial terms were not...

Stratasys and Markforged: ‘The Perfect Match’

Stratasys announced an all‑cash acquisition of Markforged for $42.5 million, gaining the latter’s composite‑printing technology and its global reseller network. The deal excludes Markforged’s metal binder‑jet line, which remains with Nano Dimension, allowing Stratasys to focus on FDM‑based metal and high‑performance...

FNBO to Buy Another Kansas City Bank

First National Bank of Omaha (FNBO) announced it will acquire Independence‑based Blue Ridge Bancshares, adding eight Missouri branches to its Kansas City footprint. Blue Ridge holds roughly $850 million in assets, and the deal follows FNBO’s Country Club Bank purchase nine months earlier,...

Vermont Packinghouse Acquisition Forms New Operating Company

Galt Foods' acquisition of Vermont Packinghouse has been finalized, creating the new operating company Vermont Packing & Trading. The 50,000‑square‑foot USDA‑inspected plant in North Springfield will now be overseen by Louis Helbling, who plans to broaden market access for New...

Robinhood Closes $180M WonderFi Deal, Crossing 1M International Customers as It Enters Canada

Robinhood Markets closed its all‑cash acquisition of Toronto‑listed WonderFi Technologies for roughly $180 million, adding about 300,000 funded crypto customers and pushing its international user base past the 1 million mark. The deal gives Robinhood direct control of Canada’s longest‑running regulated crypto...

Hortispeed Acquisition Announced by Van Der Ende Group

Van der Ende Group announced the acquisition of Hortispeed’s activities, adding the Ecofilter belt filters, O₂ Solutions’ nanobubble oxygenation technology, and Trumma Filter’s filtration systems to its portfolio. The move broadens Van der Ende’s water‑treatment capabilities for Controlled Environment Agriculture...

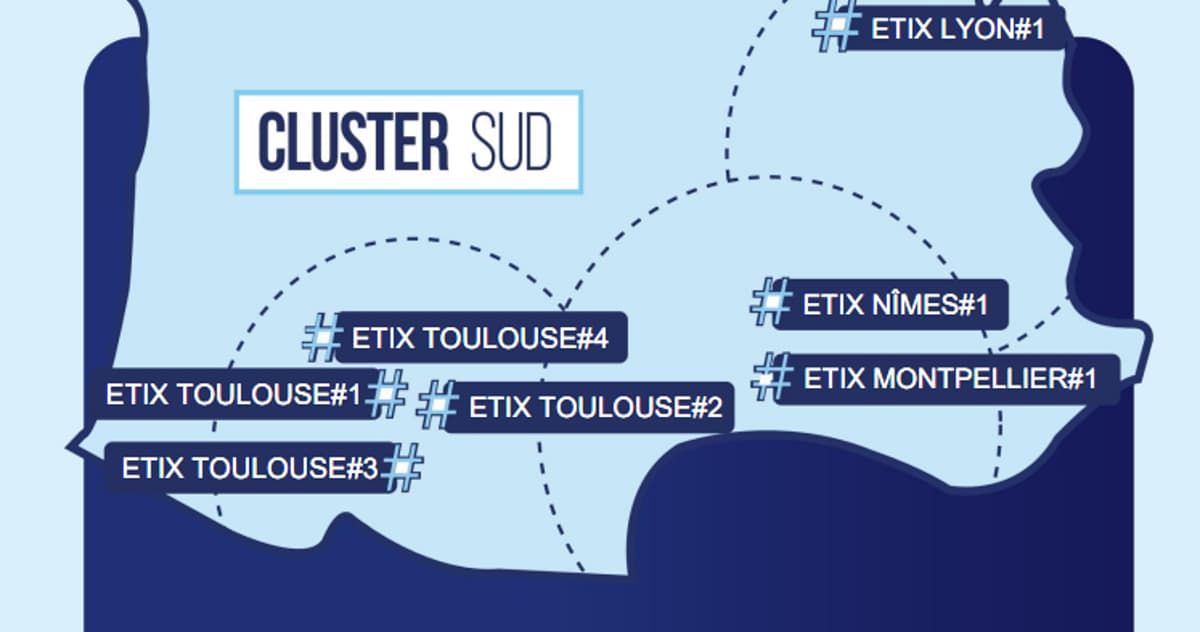

Etix to Acquire Eurofiber's French Data Centers

Etix Everywhere announced exclusive negotiations to acquire Eurofiber’s French colocation portfolio, comprising four data centers in Toulouse, Auch, Nîmes and Labège. The transaction, expected to close by June 2026, will expand Etix’s footprint to 19 data centers worldwide, adding to its...

JMI Equity Leads the Acqusition of SewerAI

JMI Equity is leading the acquisition of SewerAI, a connected platform that enables organizations to capture, analyze, collaborate on, and act upon infrastructure data. The terms of the deal were not disclosed, but the transaction adds an AI‑driven data solution...

Teneo Flies to easyJet's Rescue

Castlelake, which holds a 2.1% stake in easyJet, is weighing a $4.1 billion offer for the British low‑cost carrier that operates 355 aircraft across 38 countries. The potential bid must be formalized by June 26 under UK takeover rules. easyJet dismissed the...

General Mills to Sell Haagen-Dazs Ice-Cream Shops in Mainland China

General Mills announced it will sell its Haagen‑Dazs ice‑cream shop network in mainland China to an investor group that includes local tea chain Ningji. The buyer will receive an exclusive licence to operate Haagen‑Dazs retail and gifting businesses on the...

Blackstone Raises $13bn Asia PE Fund in World's 'Fastest-Growing' Region

Blackstone announced the final close of its third Asia private‑equity vehicle, Blackstone Capital Partners Asia III, at $13.1 billion, surpassing its $10 billion target. The fund is the firm’s largest private‑equity raise in the region and underscores Asia’s status as the fastest‑growing...

Lights, Camera, Due Diligence: What International Investors Miss When Buying US Entertainment Assets

The U.S. entertainment market generated $11.5 bn in recorded‑music revenue and $62.2 bn in home‑entertainment spending in 2025, highlighting its scale and cash‑flow potential. International investors are drawn to recurring royalties and valuable IP, yet often underestimate the layered U.S. tax, state‑law,...

Cegedim Santé Acquires Médoucine, the “Doctolib of Alternative Medicine”

Cegedim Santé has acquired Médoucine, the French platform likened to the “Doctolib of alternative medicine,” while keeping it as a separate legal entity. Médoucine generated roughly €2 million in annual revenue—about $2.2 million—and serves an estimated 80,000 complementary‑care practitioners. The deal gives Cegedim...

Barry Diller’s $12.4 Billion Offer for MGM Is a Big Bet that Vegas Is Bac...

Media mogul Barry Diller’s People Inc. has submitted a cash offer of roughly $12.4 billion to take MGM Resorts private at $48.30 per share, a 24.1% premium to the stock’s recent average price. The proposal sparked a 16% jump in MGM’s...

#59078

Destination XL Group (DXLG) announced an extended tender offer to purchase all outstanding common shares at $0.82 per share in cash. The offer, made by Zodiac Partners II, LLC—a subsidiary of Camac Fund—now expires at 5:00 p.m. ET on June 22, 2026, three...

6 Newly Formed Health Systems

Six new health systems debuted across the U.S. after mergers, bankruptcy exits, and nonprofit turnarounds. The entities range from Memorial Health System of Southwest Oklahoma’s 464‑bed merger to Hudson Regional Health’s $120 million‑backed restructuring of four New Jersey hospitals. Centralus Health...

Christie’s Parent Dumps Tri-State Affiliate

Christie’s International has terminated its franchise agreement with Christie’s International Real Estate Group LLC, the exclusive affiliate covering New York, New Jersey and Connecticut. The affiliate, acquired by Compass in a $450 million deal that also included @properties, operates roughly 30 offices and...

WWEX Group and Auctane Complete Merger, Creating Leading Logistics Provider ShipStation Global

WWEX Group and Auctane have completed a merger that creates ShipStation Global, a logistics platform backed by Thoma Bravo with CVC retaining a minority stake. The new entity combines WWEX’s freight brokerage network of over 2,300 sales professionals with Auctane’s AI‑powered...

Applied Nutrition Snaps up US Manufacturer for $16M

Applied Nutrition announced a $16 million acquisition of US supplement maker Nutrablend, adding a New York‑state manufacturing and R&D hub. The Buffalo facility will take over all U.S. production, freeing capacity at the UK plant and is projected to contribute an extra...

Bessemer-Backed MRG Sells 44 Houston-Based Taco Bell Locations to Ghai Restaurant Group

Bessemer-backed MRG, a Houston‑based Taco Bell franchisee, has sold 44 of its Texas locations to Ghai Restaurant Group. The transaction, whose financial terms were not disclosed, transfers both the restaurant assets and lease agreements. MRG plans to redeploy the proceeds...

IFF to Sell Food Ingredients Unit for $4.3 Billion

International Flavors & Fragrances (IFF) agreed to sell its Food Ingredients unit to private‑equity firm CVC Capital Partners for $4.3 billion. IFF will keep a roughly 10% equity stake and a board seat, allowing continued collaboration and upside participation. The divestiture,...

Paramount's Delrahim Slams 'Fear-Mongering' And Partisan Politics Clouding Warner Bros. Deal

Paramount Pictures, led by CEO David Ellison, is pursuing a $111 billion acquisition of Warner Bros. Discovery, a deal that would unite CBS News and CNN under one owner. The company’s chief legal officer, former DOJ antitrust chief Makan Delrahim, is...

EasyJet Says No Takeover Talks yet as Castlelake Weighs Bid

European private‑equity markets stayed active this week, with easyJet confirming no takeover talks while Castlelake weighs a potential bid, and KKR opening a new Milan office to cement its Italian footprint. Oaktree and Pantheon announced a €1bn (~$1.08bn) push into...

Leonard Green Commits to Mister Car Wash

Leonard Green & Partners completed a cash takeover of Mister Car Wash, valuing the Tucson‑based chain at $3.1 billion. The private‑equity firm, which owned about two‑thirds of the company since 2014, bought the remaining shares at $7 per share, delisting the...

Simpson Thacher & Bartlett on How Buyside Expansion Fuels Dealflow

Simpson Thacher & Bartlett partners Drew Harmon and Lauren King note that surging retail capital and expanding assets under management (AUM) among secondary‑market buyers are enabling private‑equity firms to write larger checks. The increased liquidity diminishes the traditional reliance on...

Download Buyouts’ Secondaries Report 2026

Buyouts Insider released its 2026 Secondaries Report, offering fresh insight into how limited partners (LPs) are recalibrating secondary market strategies. The report highlights emerging trends such as rising transaction volumes, shifting liquidity preferences, and heightened regulatory focus. It also examines...

Are CVs the Answer to GP Stakes Exit Challenges?

GP-led secondaries have become a popular liquidity tool for investors in GP stakes, yet they often fall short on price discovery and timing. Continuation vehicles (CVs) are emerging as an alternative, allowing sponsors to extend ownership while offering partial exits...

Yatra Founders Explore Stake Sale as Consolidation Buzz Swirls in Online Travel

Yatra Online’s founders have opened talks to sell a controlling stake, reaching out to rivals such as MakeMyTrip, Paytm Travel, Rapido, Ixigo and a private‑equity fund. The company posted FY 2026 revenue of about $12.4 billion and a record net profit of...

Chinese Rivals Push GoPro From Pioneer to Takeover Target

GoPro, the U.S. action‑camera pioneer, is weighing a sale after reporting a $93.5 million net loss for the year ended December and a 19% revenue decline to $652 million. The company has trimmed about 20% of its workforce and received multiple acquisition...

Paramount Is Pulling Every Lever to Sell LBO Debt

Paramount Skydance is mobilizing a $50 billion debt package to fund its $110 billion bid for Warner Bros. Discovery. The financing mix is expected to include roughly $30 billion of investment‑grade bonds, $12 billion of high‑yield notes and $7.5 billion of loans, with a $15 billion bridge loan...

Easyjet Attracts Takeover Interest From US Private Credit Firm

Easyjet, the UK‑based low‑cost carrier valued at roughly $3.8 billion, has attracted takeover interest from US private‑credit firm Castlelake, which manages about $36 billion in assets. Castlelake disclosed it is in the early stages of evaluating a possible offer but has not...

Cyient to Buy US' TAO Digital for $218 Mn to Boost AI, Data Engineering Capabilities

Cyient announced the acquisition of U.S.-based TAO Digital Solutions for an enterprise value of about $218 million (₹2,071 crore). The deal, slated to close by Q2 FY27 pending regulatory clearance, aims to strengthen Cyient’s artificial‑intelligence, data‑engineering and product‑engineering services. TAO Digital, founded...

Yum Is in Exclusive Talks to Sell Pizza Hut to LongRange

Yum! Brands has entered exclusive talks to sell its Pizza Hut chain to private‑equity firm LongRange Capital, outpacing rival bidder Sycamore Partners. Pizza Hut’s contribution to Yum’s revenue has fallen to roughly 12% in 2025, with annual sales just above $1 billion, while...

Universal Rejects Billionaire Bill Ackman's Takeover Bid

Universal Music Group rejected Bill Ackman's Pershing Square £48 bn ($64.3 bn) takeover offer, labeling it fundamentally undervalued. The board defended CEO Sir Lucian Grainge’s strategy and promised enhanced financial disclosures to better assess value. Ackman’s bid, aimed at moving Universal to...

Changes at CBS Put Pressure on California AG to Challenge Paramount-Warner Bros. Deal

The Department of Justice is poised to approve a $110 billion merger between Paramount Skydance and Warner Bros. Discovery, creating the biggest Hollywood consolidation in decades. At the same time, Paramount’s CBS unit is undergoing a major news‑division overhaul, including changes to the flagship...

Trump Floated the Idea of a 15% Government Stake in a Massive Railroad Merger

President Donald Trump floated a 15% federal equity stake in the $71.5 billion Union Pacific‑Norfolk Southern merger, a deal that would create the largest U.S. freight railroad. The Surface Transportation Board paused the transaction for a deeper public‑interest review, citing unclear...

Tilman Fertitta, Del Taco, Clover Food Lab

Tilman Fertitta’s Fertitta Entertainment is set to acquire Caesars Entertainment in a $17.6 billion deal that includes $11.9 billion of debt, adding more than 50 casino‑hotel resorts to his portfolio of restaurants. Del Taco announced a new $1 value menu featuring ten...

Kinderhook’s Matt Bubis Reveals Enhabit Consolidation Plans; AEA, Bridgepoint, Kohlberg Eye Oncology

Kinderhook Industries’ managing partner Matt Bubis outlined a plan to consolidate Enhabit, a leading hospice provider, with additional operators to create a national platform. The firm sees scale as a way to improve payer contracts and service quality in a...

How Consolidation, New Sweeteners and Retail Pressure Are Redefining Food

Ingredion has announced a $3.7 billion bid to acquire Tate & Lyle, a move that could forge a $10 billion global ingredient leader focused on texture, fortification and sugar‑reduction solutions. At the same time, biotech firm Amai Proteins secured Singapore regulatory clearance for its high‑intensity...

Portman Fund Acquires The Westin Peachtree Plaza, Atlanta

Portman Hospitality Fund I LP has purchased the 1,073‑room Westin Peachtree Plaza in downtown Atlanta from Marriott International, while retaining Marriott as the long‑term operator. The acquisition aligns with Portman’s strategy to target large, branded full‑service hotels in prime U.S....

MidOcean to Sell Zonda to CoStar Group

MidOcean Partners announced it will divest its portfolio company Zonda to real‑estate data giant CoStar Group. The transaction, terms undisclosed, follows CoStar's recent spree of acquisitions aimed at expanding its SaaS offerings for commercial property professionals. Zonda, founded by Jeff...

IFF Enters Into Agreement to Sell Its Food Ingredients Business to CVC

International Flavors & Fragrances (IFF) agreed to sell its Food Ingredients business to funds advised by CVC Capital Partners for an enterprise value of about $4.3 billion, retaining a 10 percent minority stake worth roughly $200 million. The divestiture, part of a broader...

PE Seeks Assets in Oncology: 6 Deals

Private equity firms are intensifying their focus on oncology, with six deals announced in the latest quarter. AEA Investors, Bridgepoint and Kohlberg are among the active buyers, targeting a mix of drug development, diagnostics and radiotherapy assets. The wave of...

Apollo and Blackstone Plan $36bn Private Credit Package to Fund Anthropic’s Google TPU Deal

Apollo Global Management and Blackstone are arranging a roughly $36 billion private‑credit facility to finance Anthropic's acquisition of Google tensor processing units (TPUs). The SPV will buy the chips and lease them back to Anthropic, with lease payments forming the primary...

DEEP DIVES | Q1 2025 AM Financials & Business Deals in Review

Nano Dimension completed its April 2025 acquisition of MarkForged for $116 million, a deal that followed a brief, costly stint with Desktop Metal. MarkForged generated roughly $70 million of Nano’s $102.4 million revenue this year, but the company still faces a $15 million annual...

TrueLayer Acquires Dutch Fintech In3 to Offer Credit at Checkout

UK‑based payments fintech TrueLayer has acquired Dutch credit‑specialist In3 to add buy‑now‑pay‑later and other credit options to its open‑banking platform. The deal, terms undisclosed, expands TrueLayer’s pay‑by‑bank network—currently focused on debit—to become Europe’s only provider offering both debit and credit...

Eurazeo Snaps up Majority Stake in T1A Group

Eurazeo has acquired a majority stake in T1A Group, a French firm that refurbishes and redeploys end‑of‑use IT equipment. T1A’s circular‑economy model extends device lifespans, cutting carbon emissions, water use and electronic waste. The deal deepens Eurazeo’s exposure to sustainable...