Saving for Grandchildren

The article outlines four tax‑advantaged ways to save for a grandchild—529 plans, UGMA custodial accounts, Coverdell ESAs, and the newly introduced Trump accounts. It details each option’s contribution limits, tax benefits, and withdrawal rules, highlighting the Trump account’s $1,000 government seed, $5,000 annual limit, and Roth‑conversion flexibility without earned‑income requirements. The author’s family plan prioritizes the Trump account, modest 529 funding, and later UGMA contributions, projecting a $2‑3 million tax‑free nest egg by age 60. The piece also notes potential shifts in education costs due to technology and policy changes.

Why Tax-Efficient Retirement Income Is About Structure

The article argues that tax‑efficient retirement income hinges on the overall structure—risk allocation, account placement, and withdrawal sequencing—rather than isolated tax tricks. It stresses that a proper asset‑allocation mix is the foundation, then recommends holding growth‑oriented funds in taxable accounts...

What Happens When a Taxpayer Dies with Passive Losses?

When a taxpayer dies holding a passive activity with suspended passive activity losses (PALs), the losses are not fully deductible. Under IRC §469(g)(2), only the portion of PALs that exceeds the step‑up in basis allowed by §1014 can be claimed...

The Nevada Advantage: Strategic Trust and Tax Planning for the Modern Family Business

The article outlines why Nevada has become a premier trust jurisdiction for high‑net‑worth family businesses. It highlights Nevada’s tax neutrality—no state income, capital gains, estate or GST taxes—combined with flexible statutes such as decanting and directed trusts. Dynasty trusts can...

Is 831(b) Ruling One of the US Captive Industry’s Biggest Wins?

The U.S. District Court in Texas partially struck down IRS regulations governing 831(b) captive insurance elections, marking a notable judicial pushback. While the decision may embolden more businesses to explore 831(b) structures, the IRS retains broad audit authority and has...

Kustoff Bill Would Boost Section 199A Deduction to 23%, Expand QBI Eligibility

Rep. David Kustoff introduced the Small Business Tax Cut Act, proposing to raise the Section 199A qualified business income deduction from 20% to 23% and broaden eligibility. The bill rewrites wage and property limits, allowing service‑trade businesses to retain the...

Using Exchange Funds To Diversify Concentrated Securities (And When It’s Better To Sell Instead)

Advisors facing clients with highly concentrated, appreciated stock holdings can use exchange funds to swap those positions for a diversified basket while deferring capital‑gain taxes. The fund operates as a partnership, requiring a seven‑year lock‑up and a minimum 20% allocation...

IRS Sets Larger 2026 Tax Allowances for Expensive Housing Abroad

The IRS released Notice 2026-25, raising foreign housing tax allowances for high‑cost overseas locations in 2026. The maximum housing exclusion climbs to $39,870, with city‑specific caps that reflect local cost differentials. London now qualifies for a $68,600 allowance, while Hong Kong,...

Understanding the PPLI Opportunity: The Basics and Beyond

Private Placement Life Insurance (PPLI) is rapidly gaining traction among affluent families seeking tax‑efficient wealth growth. Winged Keel Group, a sponsor of Family Enterprise USA, is hosting a free webcast on May 28 at 1:00 PM PDT to demystify PPLI’s structure and...

Do You Have to Replace Debt in a 1031 Exchange?

Many investors mistakenly think a 1031 exchange requires taking on a new loan equal to the debt paid off on the relinquished property. In reality, the IRS only demands that the replacement property’s total value match or exceed the sold...

Start Thinking Now About Crop Insurance Deferral for the 2026 Harvest

Farmers planting for the 2026 harvest should start planning how a crop‑insurance payout will affect their 2026 tax return. Under IRS Section 451(f), cash‑basis producers can defer part of a 2026 insurance check to 2027, but only if three specific...

Three Deferral Likely Applies Starting in 2026

The IRS has introduced a Section 1062 four‑installment, three‑year deferral for gains on qualifying farmland sales, but it only applies to transactions occurring after July 4, 2025 and to taxable years that begin after that date. Consequently, taxpayers filing a calendar year 2025...

The 2026 EBL Limit Is Much Lower Than the 2025 Limit

The Tax Cuts and Jobs Act of 2017 created Excess Business Loss (EBL) limits to curb large agricultural loss deductions, originally set at $250,000 for single filers and $500,000 for married couples. Those caps were indexed to inflation, reaching $313,000...

QSBS Eligibility Checklist: Does Your Stock Qualify Under Section 1202?

The article provides a step‑by‑step checklist to determine whether a stock qualifies as Qualified Small Business Stock (QSBS) under IRC Section 1202. It outlines eight eligibility criteria—including C‑corporation status, a $75 million gross‑asset ceiling at issuance, direct original issuance, an active‑business...

Oregon QSBS Decoupling Is Law: What Kotek's Signing Letter — and the Referendum — Mean for Founders

Governor Tina Kotek signed Senate Bill 1507 on April 9, 2026, officially decoupling Oregon from the federal qualified small‑business stock (QSBS) exclusion and applying the change retroactively to Jan 1, 2026. The move means Oregon residents must pay state tax on gains that remain...

US Court Strikes Down IRS 831(b) Listed Transactions Designation

A U.S. district court in Texas partially struck down IRS regulations governing 831(b) micro‑captive transactions. While the court affirmed the IRS’s designation of these captives as “transactions of interest,” it ruled the agency did not substantiate a presumption that they...

The 183-Day Rule and Safe-Harbor Day-Counting for Washington Taxpayers

The article explains Washington’s emerging 183‑day statutory residency rule and how it interacts with domicile analysis for founders leaving the state. It details how states define a “day,” the pitfalls of permanent places of abode, and why merely staying under...

Trust Planning for Washington High Earners: ING, NING, and DING Trusts Under ESSB 6346

Washington will launch a state income tax on residents whose AGI exceeds $1 million in 2028. High‑earning Washingtoners can use non‑grantor trusts—often called ING, NING, or DING—sited in Nevada, South Dakota, or Delaware to shift portfolio and passive investment income out...

QSBS and Washington Residency: Timing Section 1202, the Sale, and the Move

Washington founders face a narrow 20‑month window before ESSB 6346 takes effect, during which federal Section 1202 qualified small business stock (QSBS) treatment, Washington’s 7% capital gains tax, and the new 9.9% income tax intersect. The article outlines four levers—QSBS...

The Marriage Penalty in ESSB 6346: Why Two Unmarried Washington Earners Can Save $40,000 a Year

Washington's ESSB 6346 imposes a 9.9% tax on household income exceeding $1 million, creating a built‑in marriage penalty for dual‑high‑earner couples. A pair earning $700,000 each would pay roughly $39,600 annually, or nearly $600,000 over a 15‑year career, solely because they...

Marrying A Non-U.S. Citizen? Your S Corp May Be At Risk

U.S. citizens who marry nonresident aliens risk losing S‑corporation status because foreign community‑property rules can automatically attribute ownership of the business to the spouse. Under the immutability principle, the community‑property regime may continue to apply, making the foreign spouse a...

Marrying A Non-U.S. Citizen? Your S Corp May Be At Risk

U.S. citizens who marry non‑resident aliens risk losing their S‑corporation election because community‑property regimes can deem the foreign spouse a shareholder. Under the immutability principle, ownership rules from the couple’s first habitual residence may persist, automatically invalidating the S status...

Investing More Than The Gift Tax Exclusion Limit Shouldn’t Be A Problem

The author contributed roughly $35,000 per child to custodial accounts in 2026, exceeding the $19,000 annual gift‑tax exclusion. The $16,000 overage per child is deducted from the $15 million lifetime exemption, meaning no immediate tax is due. He will file IRS...

The Great Wealth Transfer: Strategies to Transfer ‘Superfluous’ Assets Without Taking an Estate Tax Hit

The article defines “superfluous” assets as holdings—second homes, artwork, concentrated stock—that exceed a family’s income needs and can be earmarked for tax‑efficient transfer. It outlines several estate‑planning tools, including Grantor Retained Annuity Trusts, Qualified Personal Residence Trusts, charitable remainder trusts,...

What Counts as Washington Taxable Income Under ESSB 6346?

Washington’s new income tax under ESSB 6346 uses federal adjusted gross income as its starting point, then applies state‑specific additions, subtractions, and structural adjustments. After these modifications, a $1 million household standard deduction is allowed and the remaining amount is taxed at...

TinyLog: You Should Consider Moving Your Business to the US

The author is leaving Germany for Thailand and restructuring his online business as a U.S. LLC to escape Germany’s 45 % top income‑tax rate. Thailand’s territorial tax regime only taxes money physically remitted into the country, allowing profits to stay in...

Washington’s Capital Gains Tax Charitable Deduction Has a Hidden Catch

Washington’s capital gains tax offers a charitable deduction, but it only applies when the donation is made to a “qualified organization” that is principally directed and managed within the state. The rule diverges from federal law, which merely requires 501(c)(3)...

The Alternative Minimum Tax and Stock Options: A Complete Guide for Washington Startup Employees

The guide explains how the federal Alternative Minimum Tax (AMT) hits incentive stock options (ISOs) and how Washington’s new tax regime reshapes planning. The 2026 One Big Beautiful Bill Act raises the AMT exemption to $90,100 for singles and $140,200...

RSUs and Washington State's New Taxes: What Seattle Tech Employees Need to Know

Washington’s new tax regime adds a 7‑9.9% capital‑gains levy (effective 2025) and a 9.9% broad‑based income tax (effective 2028) that together reshape the cost of restricted stock units for Seattle tech workers. RSU vesting is ordinary income, so any vesting...

Robbing Peter to Pay Paul: A(nother) Look at Long/Short Direct Index Tax-Loss Harvesting

Leveraged long/short direct‑index tax‑loss harvesting (LSDI) lets investors swap a concentrated, high‑cost‑basis stock for a diversified basket without paying capital‑gains tax up front. The authors model a $10 million Shopify holding and find that manager fees—0.5% on the long side and...

Section 1045 Rollovers: How to Defer QSBS Gains When You Sell Too Early

Section 1045 permits owners of Qualified Small Business Stock (QSBS) to defer capital gains by reinvesting sale proceeds into new QSBS within 60 days. The rollover treats the original gain as unrecognized, reducing the basis of the replacement shares, while...

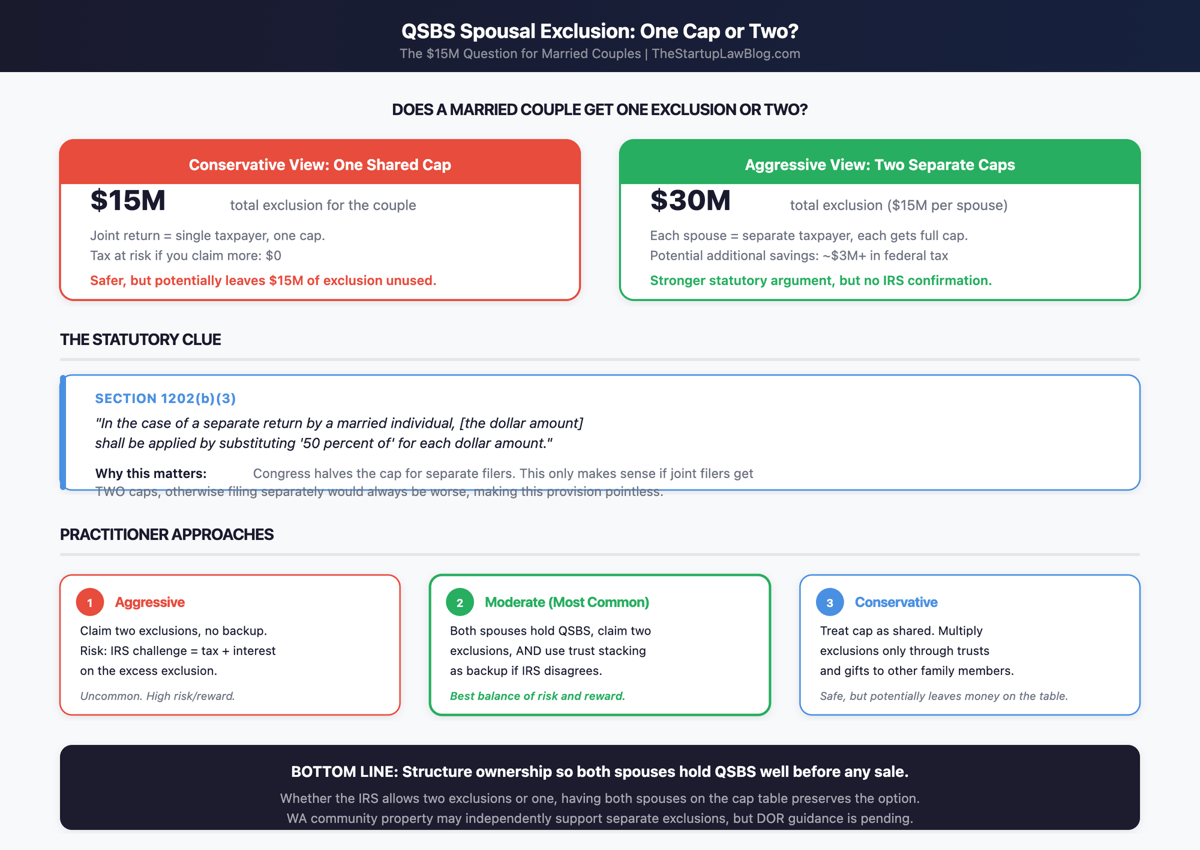

Can Both Spouses Claim the QSBS Exclusion? What Section 1202 Does and Doesn't Say About Married Couples

Section 1202 lets a taxpayer exclude up to $15 million of qualified small‑business stock (QSBS) gains, but the law is silent on whether a married couple filing jointly receives one $15 million cap or two. The statute only specifies that married filing separately...

Restricted Stock Vs. Stock Options: Which Is Better for Startup Equity?

Startup equity compensation typically comes in two forms: restricted stock awards and stock options. Restricted stock grants actual shares at grant and, with an 83(b) election, locks in tax on the low initial value, turning future gains into capital gains....

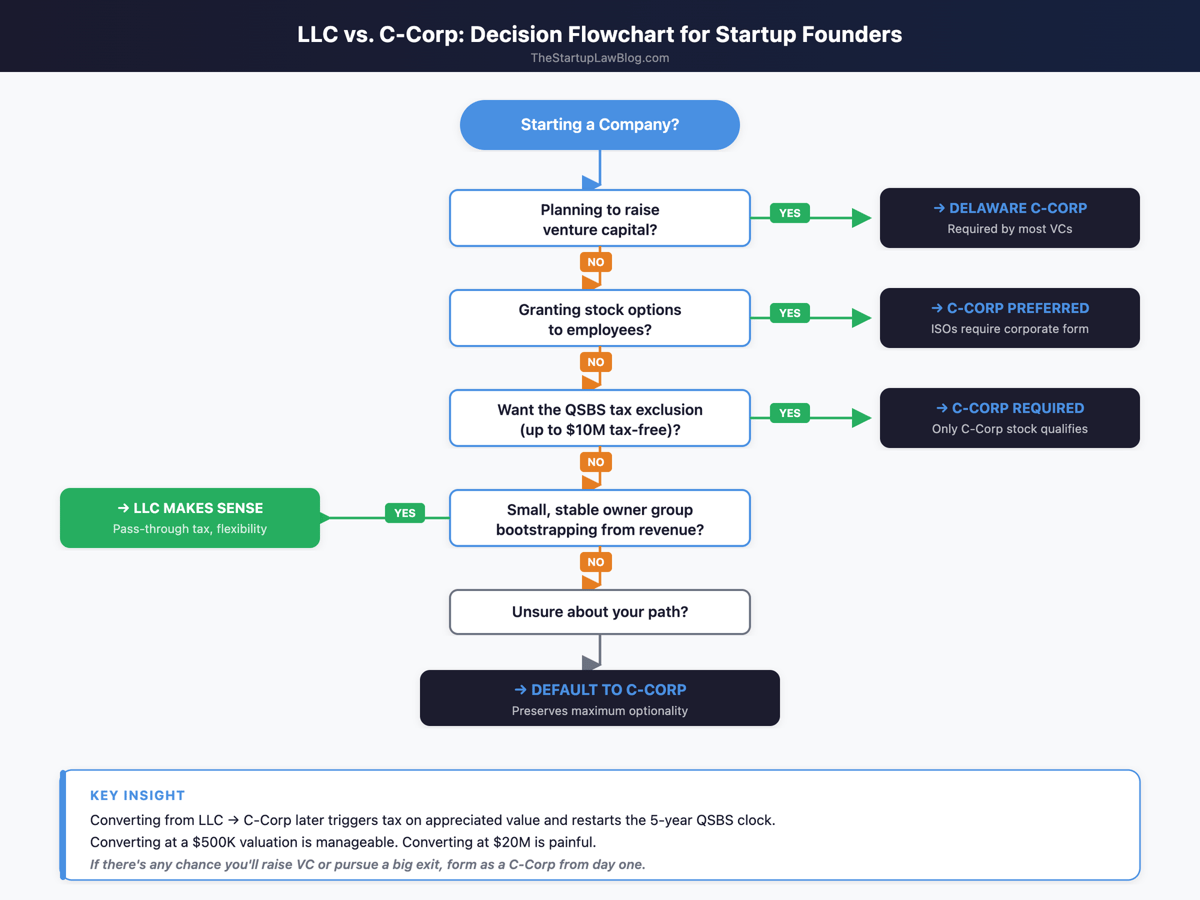

LLC Vs. C-Corp for Startups: How to Choose the Right Entity

The guide breaks down the practical trade‑offs between forming an LLC and a Delaware C‑Corporation for startups. It explains how entity choice affects fundraising mechanics, equity compensation, tax treatment, and long‑term exit strategies such as the QSBS exclusion. Real‑world examples...

An Overview of the Enhanced Senior Deduction

The OB3 Act added §151(d)(5)(C), creating a senior deduction of up to $6,000 per individual 65 or older (or $12,000 for married couples) for tax years 2025‑2028. The deduction lowers taxable income, does not affect AGI, and can be claimed...

State Tax Comparison for Startup Founders: Where to Incorporate and Where to Live

The guide breaks down how incorporation state and personal residence state affect a founder’s tax bill, emphasizing that residence decisions can swing after‑tax proceeds by millions. It compares Delaware’s standard corporate framework with personal tax regimes in high‑tax states like...

Washington's New Income Tax: The Complete Guide for Founders, Investors, and High Earners

Governor Ferguson signed ESSB 6346 on March 30, 2026, establishing Washington’s first broad‑based income tax—a 9.9% levy on adjusted gross income exceeding $1 million, effective January 1, 2028. The law reshapes tax planning for founders, investors, executives, and high‑earning residents, introducing residency rules, a marriage...

The Complete Guide to Qualified Small Business Stock (QSBS): Section 1202 Explained

Section 1202 of the Internal Revenue Code lets founders and early investors exclude up to $15 million of capital gains when they sell qualified small business stock (QSBS) after a five‑year hold. The One Big Beautiful Bill Act (OBBBA) enacted in July 2025 raised the...

![Why Physicians Pay More in Taxes and How to Reclaim Your Income [PODCAST]](/cdn-cgi/image/width=1200,quality=75,format=auto,fit=cover/https://kevinmd.com/wp-content/uploads/65a06f47-06d1-44f6-b074-deb9a2d19a25.jpeg)

Why Physicians Pay More in Taxes and How to Reclaim Your Income [PODCAST]

Physician earnings surge after residency, but many doctors face unexpectedly high tax bills due to progressive rates, payroll taxes, and under‑withholding. Tax specialist Logan Foltz explains that most physicians lack basic tax literacy, especially when transitioning from W‑2 resident salaries...

Estate Planning Before 2028: How Washington's Income Tax Changes the Calculus

Washington will impose a 9.9% income tax on earnings above $1 million starting Jan 1 2028, adding a second layer to its already aggressive estate tax regime. The combined effect creates a double‑tax problem for high‑net‑worth residents, making the pre‑2028 window the most...

Washington Income Tax: What Happens If You Move Mid-Year?

Washington’s new income tax includes a part‑year residency provision that prorates both the tax base and the $1 million standard deduction based on days of residency. Under §406, taxpayers only owe tax on income earned while a Washington resident, with the...

Charitable Giving Strategies to Reduce Your Washington Income Tax

Washington’s new 9.9% income tax introduces a charitable deduction under §309, limited to $100,000 per year, which can shave up to $9,900 off a taxpayer’s liability. The deduction mirrors federal IRC §170 gifts, but its cap means high‑income earners must look...

Washington Vs. California: A Tax Comparison for Founders and Investors

Washington’s new ESSB 6346 law, effective 2028, imposes a 9.9% income tax on household income above $1 million, ending its zero‑tax reputation for high earners. California still taxes all income at a progressive rate topping 13.3%, including wages, capital gains and...

Washington's New Income Tax and Pass-Through Business Income: S-Corps, LLCs, and Partnerships

Washington enacted a 9.9% state income tax (ESSB 6346) that applies to individuals, including income passed through from S‑corporations, LLCs, and partnerships. The law permits pass‑through entities to elect to pay the tax at the entity level, converting the state...

Washington's New Income Tax: The Marriage Penalty Explained

Washington’s new 9.9% state income tax provides a $1 million standard deduction per household, not per individual. Consequently, married or domestic‑partner couples share a single deduction, creating a marriage penalty that can reach $99,000 annually for comparable earners. The penalty also...

Washington's New Income Tax and Remote Workers: Who Owes What?

Washington will launch a 9.9% personal income tax on Jan. 1, 2028, using a dual‑track residency test that hinges on domicile and physical presence. Residents—defined by domicile or a 183‑day presence test—must allocate all income to the state, subject to a...

How Washington's New 9.9% Income Tax Applies to Stock Options and RSUs

Washington’s ESSB 6346 imposes a 9.9% income tax on household earnings above $1 million starting January 1, 2028. The tax is calculated from federal adjusted gross income, meaning equity compensation can push employees over the threshold in a single year. Incentive Stock Options...

Your Accountant Is Right. Stop Investing in Residential. Buy Your Building.

Small business owners are urged to replace rental expenses with ownership of commercial real estate. By leveraging SBA 504 or 7(a) financing, they can acquire a building with as little as 10% down and benefit from long‑term fixed rates. Owner‑occupied...

Perplexity Launches Computer for Taxes to Draft, Review, and Optimize U.S. Federal Tax Returns Using Loadable AI Tax Modules

Perplexity has expanded its Computer AI platform with dedicated tax modules that can automatically draft U.S. federal tax returns on official IRS forms, review professionally prepared returns for errors, and create custom tools for complex scenarios such as rental portfolio...

Does QSBS Avoid Washington’s New 9.9% Income Tax? (Yes — For Now)

Washington’s ESSB 6346, effective 2028, imposes a 9.9% income tax on household AGI above $1 million. Because Section 1202 excludes qualifying small‑business stock gains from federal gross income, those gains never enter AGI and thus escape the state tax. The article illustrates...