How to Earn ~7% APY From Raisin

Raisin, a fintech partner of banks, is running a limited‑time promotion with Everbank that locks a 4.10% APY for 90 days and adds a cash bonus ranging from $70 to $1,500 depending on deposit size. By combining the interest earned with the bonus, the effective annualized yield climbs to roughly 7% for three months. The bonus tiers start at a $10,000 deposit and top out at $200,000, with the bonus paid after the 90‑day holding period. The offer requires a new Raisin account and a promo code before April 30, 2026.

The Great COLA Debate-Maybe Not the Expected Solution.

The article argues that switching Social Security’s cost‑of‑living adjustment (COLA) from the CPI‑W to the experimental CPI‑E would only modestly increase benefits—about $45 per month after sixteen years. While CPI‑E tracks spending of households 62+, its higher inflation assumption would...

The Sunday Best (04/26/2026)

The Sunday Best newsletter highlights three key pieces of content for physicians: a guide on retiring at 55, a lifestyle piece on boating as a post‑career pursuit, and an analysis of the “spending guilt” many doctors feel once they have...

MiB: David Gardner, Co-Founder, The Motley Fool

David Gardner, co‑founder of The Motley Fool, sat down for a Masters in Business interview to promote his new book, “Rule Breaker Investing: How to Pick the Best Stocks of the Future and Build Lasting Wealth.” He walked through the...

Investing Fundamentals: A Simple Guide for Beginners

The article breaks down investing fundamentals for beginners, stressing that cash left in savings loses value to inflation and that owning shares or diversified index funds can preserve purchasing power. It explains how stocks are bought through brokerages and why...

New Online IRS Tax Debt Tool Helps Taxpayers Find the Best Way to Pay

The Internal Revenue Service has introduced a new online Tax Debt Help tool on its Get Help With Tax Debt page. The interactive questionnaire asks six financial‑status questions and then recommends the most suitable resolution, such as a temporary collection...

Tax Planning as the Backbone of a Durable Retirement Income Plan

A durable retirement income plan hinges on proactive tax planning, not just cash‑flow generation. While tax preparation reports past liabilities, tax planning strategically shapes withdrawals, Roth conversions, and Social Security timing to manage taxable income over decades. Without coordination, retirees...

Ask Tom Anything - April 2026

Thomas A. Gorczynski’s April 2026 "Ask Tom Anything" post launches a subscriber‑only tax Q&A series. The tax specialist invites paid readers to submit questions on filing, strategy, or practice management, noting he may not answer every query. The article includes a...

10 Real Assets vs 10 Fake Assets (Most People Get This Wrong)

The post contrasts ten "real" assets that generate cash flow with ten "fake" assets that drain money, arguing that wealth hinges on what you buy, not how much you earn. Real assets include rental properties, dividend stocks, REITs, index funds,...

Warren Buffett Explains Passive Income: Making Money While You Sleep

Warren Buffett frames passive income as the long‑term result of owning high‑quality businesses and letting compounding work, not a quick‑cash hack. He emphasizes front‑loading effort—saving, learning, investing—and then allowing assets to generate cash flow for decades. Buffett’s own portfolio, from...

Cash On The Barrel

The Heisenberg Report highlights that a 25/25/25/25 portfolio—equal parts equities, bonds, commodities and cash—is delivering a 26% annualized return so far in 2026, outpacing the traditional 60/40 mix. The surge is largely driven by a 33% rise in the S&P...

Investment 101 With The Building Financial Podcast

The Macro Butler appeared on The Building Financial Podcast to deliver an Investing 101 crash course, emphasizing that starting early outweighs trying to be overly clever. The discussion highlighted compounding as the silent engine of wealth, and argued that investors...

The Disposition Effect: Why Losing Investors Keep Getting Worse

New research on 189,530 Chinese retail investors shows that prior losses amplify the disposition effect by roughly 10%, while prior gains dampen it. The bias—selling winners early and holding losers—creates a self‑reinforcing “doom loop” that hurts portfolio performance, especially for...

A Beginner’s Guide to Investment Diversification

The article offers a beginner‑level overview of investment diversification, explaining how spreading capital across asset classes—such as property, stocks, bonds, and crypto—reduces portfolio risk. It outlines a common crypto allocation model (60% stablecoins, 30% medium‑risk coins, 10% emerging projects) and...

Why Precious Metals Remain a Smart Financial Choice

Precious metals such as gold, silver, platinum and palladium are being promoted as reliable stores of wealth amid economic uncertainty. Their historical performance shows they can outpace inflation and hold value when equities and bonds falter. The article highlights both...

Podcast with Morgan Housel on Money in Your 40s and Beyond

Todd Wenning of Flyover Stocks hosted Morgan Housel, author of The Psychology of Money, for a deep‑dive on personal‑finance challenges faced in one’s 40s and beyond. The conversation highlighted the scarcity of guidance tailored to this age group, despite its...

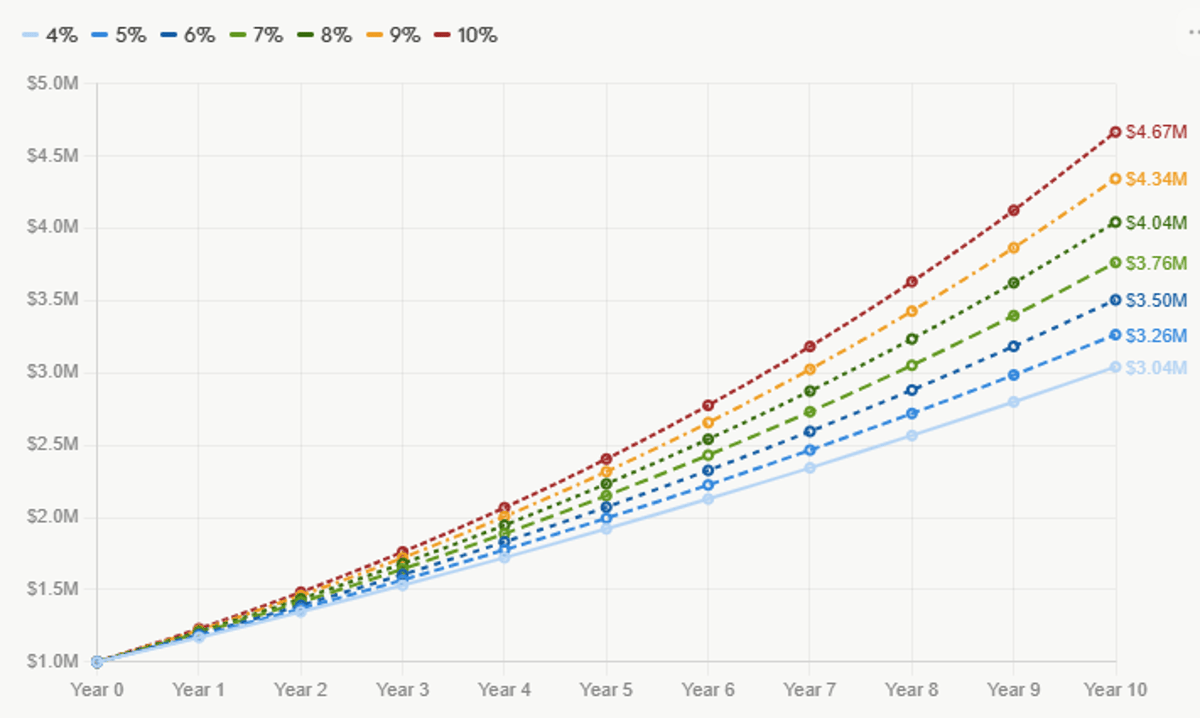

How Do You Retire at 55?

A 45‑year‑old earning $300,000 annually has $1 million saved and contributes $130,000 each year, aiming to retire at 55. Using the 4 % rule, a $3.5 million portfolio would cover the current $12,000‑per‑month lifestyle, and a 10‑year projection shows that target is reachable...

Charlie Munger Advice: Top 4 Tips To Become The First Millionaire In Your Family

Charlie Munger outlines a four‑step framework for anyone aiming to become the first millionaire in their family. He stresses self‑improvement as the foundation, then urges aggressive frugality to amass the first $100,000, which unlocks the power of compounding. Once that...

Rethinking the “Right” Time for Social Security

The author, who could have started Social Security at 62, delayed filing until age 67 based on conventional advice, changed course after a close friend received a terminal diagnosis. He and his brother claimed benefits at 64½, noting a break‑even...

At the Money: Looking Beyond Market Cap Weighted Indexes

Rob Arnott, the founder of Research Affiliates, argued that market‑cap‑weighted indexes like the S&P 500 suffer from concentration risk, costly “flip‑flop” trades, and a bias toward over‑priced mega‑caps. He promoted fundamental‑weighting—using sales, profits, book value and dividends—to better reflect a company’s...

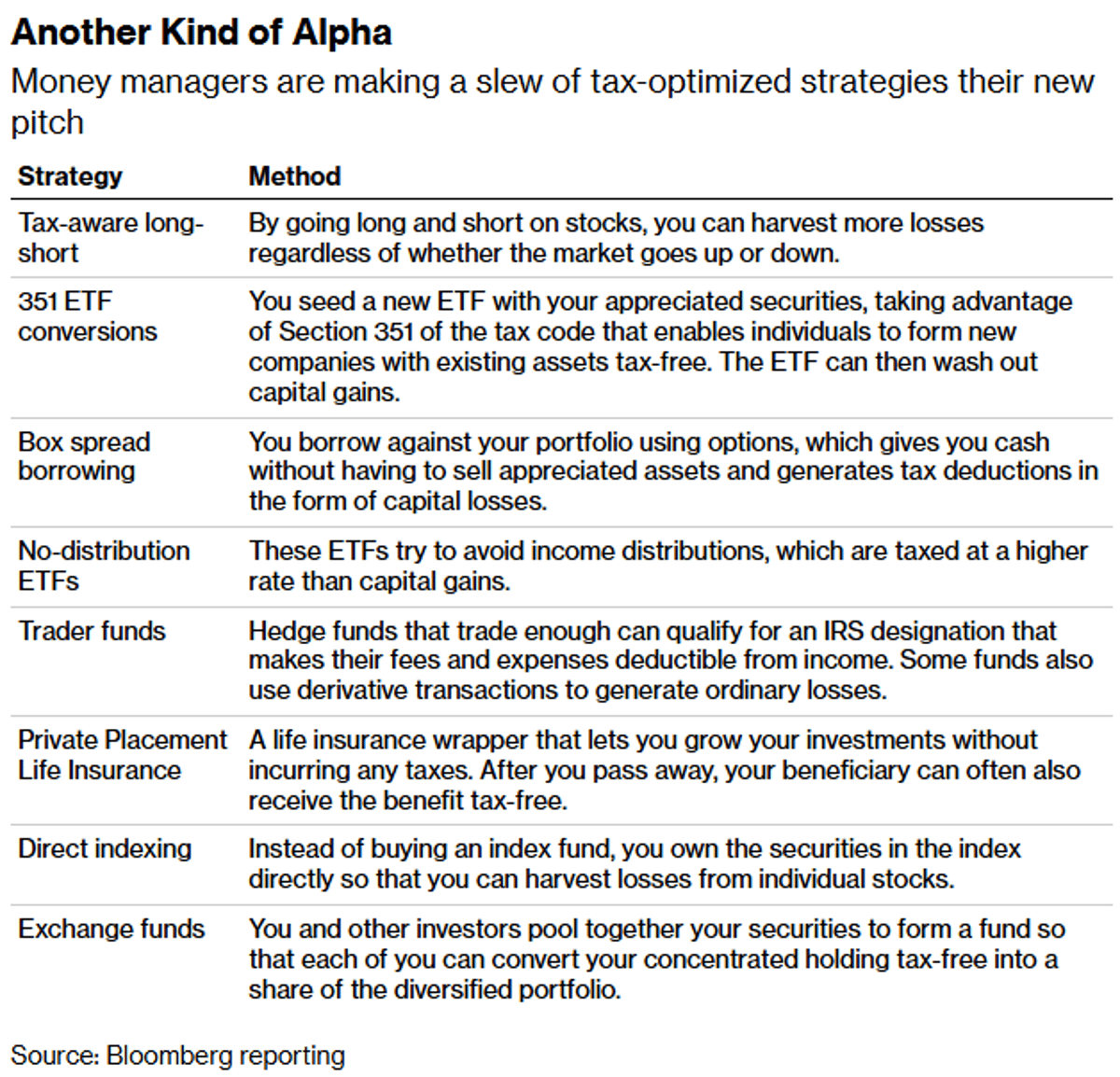

Tax Alpha

Over the past two decades wealth managers have moved from product‑centric sales to holistic, goals‑based advice, and most have abandoned the pursuit of pure market alpha. Indexing now dominates fund flows, with active mutual funds seeing sustained outflows while index...

Closing The Implementation Gap: A Formula For Exploration Meetings That Lead To Better Client Follow-Through

Financial advisors often see clients ignore well‑crafted recommendations, not because the plans are too complex, but because they fail to engage the client’s unconscious motivations. Scott Frank explains that the traditional Rider‑focused approach overlooks the "Elephant" – the emotional, habit‑driven...

Will Labor Go ‘Back to the Future’ on Property CGT?

The Albanese government is expected to restore the pre‑1999 capital gains tax (CGT) framework for property investments, taxing real gains—adjusted for inflation—at the investor’s marginal tax rate. This would replace the current system that levies nominal gains at 50% of...

XEQT vs VEQT vs ZEQT: Why XEQT Looks Like the Winner

The Canadian market now offers three flagship all‑equity ETFs—iShares XEQT, Vanguard VEQT and BMO ZEQT—each bundling U.S., Canadian, European and emerging‑market stocks. Back‑tested data shows XEQT slightly outpacing the others, but this edge relies on a fixed U.S. equity weighting...

Hidden Surcharge

A recent HumbleDollar post highlights a little‑known Medicare surcharge that can turn a single extra dollar of income into an effective tax rate exceeding 1,000 percent. The surcharge, known as the Income‑Related Monthly Adjustment Amount (IRMAA), kicks in when a...

Portfolio Update – 04/20/2026 (All-Time High)

The investor’s portfolio reached a new all‑time high, posting a 22.0% gain year‑to‑date, far outpacing the S&P 500’s 4.2% rise. Returns since inception in January 2024 total +559.8%, with 2024 delivering +173.0% and 2025 +98.1%. The performance comes without options or leverage,...

🎥 AlphaCore Wealth Advisory's Dick Pfister - Wealth Management with Alpha at Its Core: Live From iCapital Connect

AlphaCore Wealth Advisory CEO Dick Pfister appeared on the iCapital Connect Alts Pulse podcast to discuss how his firm blends wealth management with private‑market access. Drawing on 25 years of trading and advisory experience, Pfister explained AlphaCore’s origins, its technology‑driven...

Physician Spending Guilt During Retirement: How to Make the Most of Your Hard-Earned Money

Physicians are retiring with unprecedented financial strength, yet many grapple with guilt when they begin to spend their savings. The article explores why this anxiety persists despite solid retirement accounts and offers practical steps to reframe spending as a reward...

The Hidden Cost of Convenience: Why Balanced Mutual Funds May Be Costing You Hundreds of Thousands

A new study of 1,260 balanced mutual funds managing about $1.6 trillion finds they consistently lag low‑cost index portfolios. Researchers examined 32 years of performance across four equity‑allocation tiers and discovered lower returns, weaker risk‑adjusted metrics, and negative net alpha after...

6 Financial Tools Nobody Taught You in School (But You Really Need to Know)

The article outlines six essential financial tools—savings accounts, bonds, stocks, bank wealth‑management products, mutual funds/ETFs, and insurance—explaining how each works, its risk‑return profile, and ideal use cases. It emphasizes that most people lack formal education on money management, leading to...

Blackstone’s “Advisor Pulse” Survey: 90% of Financial Advisors Double Down on Alternatives:

Blackstone’s latest Advisor Pulse survey shows that 90% of U.S. financial advisors are either maintaining or increasing their exposure to alternative investments despite volatile public markets. The data signals a structural shift away from the traditional 60/40 equity‑bond mix toward...

3 High-Conviction Assets to Accumulate in 2026

The author warns that both equities and crypto are entering a corrective summer phase, with the S&P 500 likely topping near 6,100 points before a typical 4.5‑year cycle pullback of 20% or more. In this bear‑market backdrop, the post highlights...

Adviser Links: Shadow Advisers

Charles Schwab is rolling out a $5 block‑trade fee and AI‑driven client agents in June, while expanding its Pledged Asset Line lending to 45 RIAs. Wealth.com announced a $65 million Series B round led by Schwab, and OpenAI acquired Hiro Finance to...

MB520: The Wealth Leaks Costing You Thousands Every Year (And Why Your Advisors Miss Them) – With Andrew Majd

In a recent interview, Andrew Majd of Dew Wealth Management outlines a three‑pillar wealth framework—protect, grow, and manage—highlighting that many high‑income individuals unknowingly leave costly gaps in their financial plans. He stresses that missing insurance, inadequate estate structures, and limited...

What to Do After Losing Money on a Real Estate Investment

The article guides investors who have lost money in a passive real‑estate syndication through a practical recovery roadmap. It first urges investors to determine whether the asset is merely distressed or a total loss, as this drives tax treatment and...

The Market Is a Great Guru: Vinod Sethi on The Long Game

Vishal Khandelwal has launched a new hardcover, *The Long Game*, featuring reflections from thirty veteran investors on patience, process, and compounding wealth over decades. Simultaneously, his YouTube series *The One Percent Show* is rebranded as *The Long Game* to better...

Is FIRE Feasible? Explaining The “Financial Independence, Retire Early” Movement

The Financial Independence, Retire Early (FIRE) movement encourages savers to amass enough assets to quit work decades before the traditional retirement age. Its core formula combines aggressive saving—often 50‑70% of income—with the 4% withdrawal rule, which implies a portfolio 25...

The Ticking Clock

The article outlines how major asset classes perform across the Global Liquidity cycle. Equities tend to rise when liquidity expands, while cash dominates during contractions. Commodities typically peak in the late‑cycle, and long‑term bonds excel at the trough. The piece...

The 4 Pillars I Used To Build Wealth (Not Luck, Not Hype)

Clever Girl Finance outlines four pillars—earned income, investing, real estate, and entrepreneurship—as a systematic approach to building wealth, emphasizing starting with one pillar and layering others over time. The article stresses that wealth is not luck but a structured, consistent...

Prompting Your Way to the Beach (Using Just 10 Prompts)

The post introduces a 10‑prompt framework that helps solo entrepreneurs reverse‑engineer their ideal retirement lifestyle before calculating a lump‑sum target. By asking detailed lifestyle questions first, the method produces a concrete monthly cash‑flow estimate, which then informs a tax‑advantaged business...

Staying Rational

Adam Grossman argues that investors should anchor decisions in intrinsic value rather than short‑term market noise. He notes the U.S. stock market’s historical P/E of about 16, meaning a full‑year earnings loss would only shave roughly 6% off a company’s...

Index Investing In China

The article breaks down the fragmented landscape of Chinese equity markets, explaining that investors must choose among multiple exchanges—Hong Kong, Shanghai, and Shenzhen—each with its own flagship index. By analyzing seven major indices as of April 14 2026, the author shows stark...

Housing Is Not an Afterthought in Retirement

Housing is often sidelined in retirement planning, even though it is most retirees' largest asset. The article stresses that a home serves both as a place to live and a financial lever that can fund spending, reduce risk, or preserve...

Economic Commentary Q2 2026: Markets Reawaken to Risk

Ron Albahary, CIO of LNW Advisors, released the firm’s Q2 2026 Economic Commentary, noting that markets are reawakening to risk after a period of caution. The report cites renewed inflation pressures, heightened geopolitical shocks, and rapid AI‑driven disruption as key...

Do Retirees Really Struggle Financially? Why and What to Do?

Surveys from T. Rowe Price, Goldman Sachs and the Center for Retirement Research show retirees typically live on 60‑66% of their pre‑retirement earnings, with 57% saying they are as well‑off or better than before. Replacement needs vary sharply by income: low...

Why The Key to Building Wealth Is Investing in the Stock Market According to Warren Buffett

Warren Buffett argues that stocks are the most reliable path to lasting wealth because they represent ownership in productive businesses that generate real cash flow. He emphasizes the power of compounding, noting that modest returns can snowball into substantial fortunes...

The Merits of Mediocrity

Investors who aim for modest, consistent performance often outpace high‑risk, short‑term traders over long horizons. The piece argues that avoiding the bottom quartile and preserving capital lets compounding generate superior wealth, echoing Warren Buffett’s view that a handful of outsized...

Trust Planning for Washington High Earners: ING, NING, and DING Trusts Under ESSB 6346

Washington will launch a state income tax on residents whose AGI exceeds $1 million in 2028. High‑earning Washingtoners can use non‑grantor trusts—often called ING, NING, or DING—sited in Nevada, South Dakota, or Delaware to shift portfolio and passive investment income out...

The Marriage Penalty in ESSB 6346: Why Two Unmarried Washington Earners Can Save $40,000 a Year

Washington's ESSB 6346 imposes a 9.9% tax on household income exceeding $1 million, creating a built‑in marriage penalty for dual‑high‑earner couples. A pair earning $700,000 each would pay roughly $39,600 annually, or nearly $600,000 over a 15‑year career, solely because they...

How I Actually Decide to Put Real Money Into an Investment

The author outlines an eight‑step framework for turning investment ideas into real capital allocations, emphasizing disciplined position sizing over mere idea generation. Early screening focuses on low EV/EBIT, price‑to‑book and cash‑flow metrics, while quick‑kill criteria weed out unclear or risky...