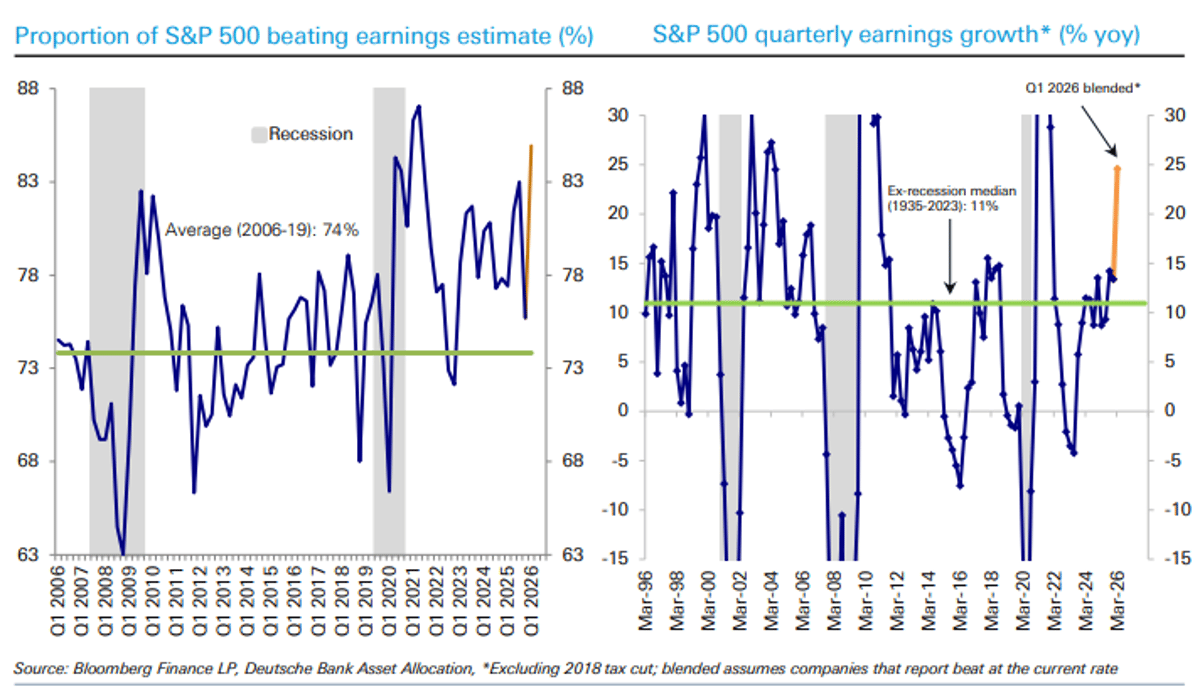

All 11 Sectors Poised for YoY Earnings Growth

"This is one of the best earnings seasons in 20 years...All 11 top-level sectors are expected to show YoY earnings growth for the first time in 4 years:" Deutsche Bank research https://t.co/46b3tizXQO https://t.co/wjeNquRQNZ

HSW Looks Cheap if Iran Hit Avoided, Risks Remain

#HSW AGM Update says no material impact on revenue from Iran conflict but does say Europe offsetting softer Asia. ShareScope showing fwd p/e 8.8 falling to 7.1 and fwd Divvy 2.9% rising to 3.9%. If they escape a hit from...

NuWays Trims Target to €250, Keeps Buy on DO & CO

$DOC - Holding Equity Small Caps FI NuWays sets DO & CO price target at EUR 250, keeps buy rating NuWays reiterated BUY on DO & CO, cut 12-month target price to EUR 250 from EUR 266, citing a more cautious near-term...

Stable LNG FSRU Infrastructure Drives Strong Returns

LNG FSRUs: Stable Infrastructure Returns in the Booming Global LNG Market – Top Fleet Owners to Watch Investment case is compelling for top fleet owners (with 6 Charts and a table) Link: https://t.co/UY0J7Gk8Ox

Identify Dividend Kings, Aristocrats, and Champions

Dividend Kings: Companies that have increased their dividends for at least 50 consecutive years. 👑 Dividend Aristocrats: Companies that are part of the S&P 500 and have increased their dividends for at least 25 consecutive years. 💵 Dividend Champions: Companies...

Japan's Hikari Leads Capital Allocation; Binjiang Delivers Growth, High Yield

Pitches for: - Hikari Tsushin: “probably has the best capital allocation record in Japan at scale by far” - Binjiang Service Group: “grew revenue 22% and 15% in the two most recent years… 8-9% dividend yield”

Overlooked Small‑Cap REIT $PINE Offers Compelling Opportunity

The REIT market as a whole has struggled under the high interest rate environment over the last couple of years- But that has led to some REITs becoming quite interesting opportunities. I believe $PINE is one of those REITs, but also a...

Nebius Earnings Depend on Q1 Operating Cash Flow

Nebius’ next earnings could hinge on one key number: Operating Cash Flow. Strong OCF = self-funded growth. Weak OCF = possible dilution. All eyes on Q1. 📉 NBIS

Research Hunts Truth; Validation Shields Ego

The difference between research and collecting validation: Research is hunting for the truth, whether it goes for or against your position. Validation is filtering for takes that confirm what you already believe. One protects your portfolio. The other protects your ego.

Golden Summit Emerges as Long‑term Successor to Fort Knox

Kinross’ Fort Knox is running low on ore as main pit depletes. Manh Choh helps short-term, but next-door Golden Summit $FVL.TO is the logical long-term fit: massive 29+ Moz resource, same geology, highway access. 50k m drilling in 2026 toward...

AI‑Driven Power Demand Boosts AMD and Electrification

AI Food chain of AI + DC +grid + power theme: $AMD: 1Q DC +57% y/y & server CPU revenue guide +70% in Q2 bc of demand for EPYC processors and AI infrastructure. It’s happening throughout technology, industrials, utilities and power...

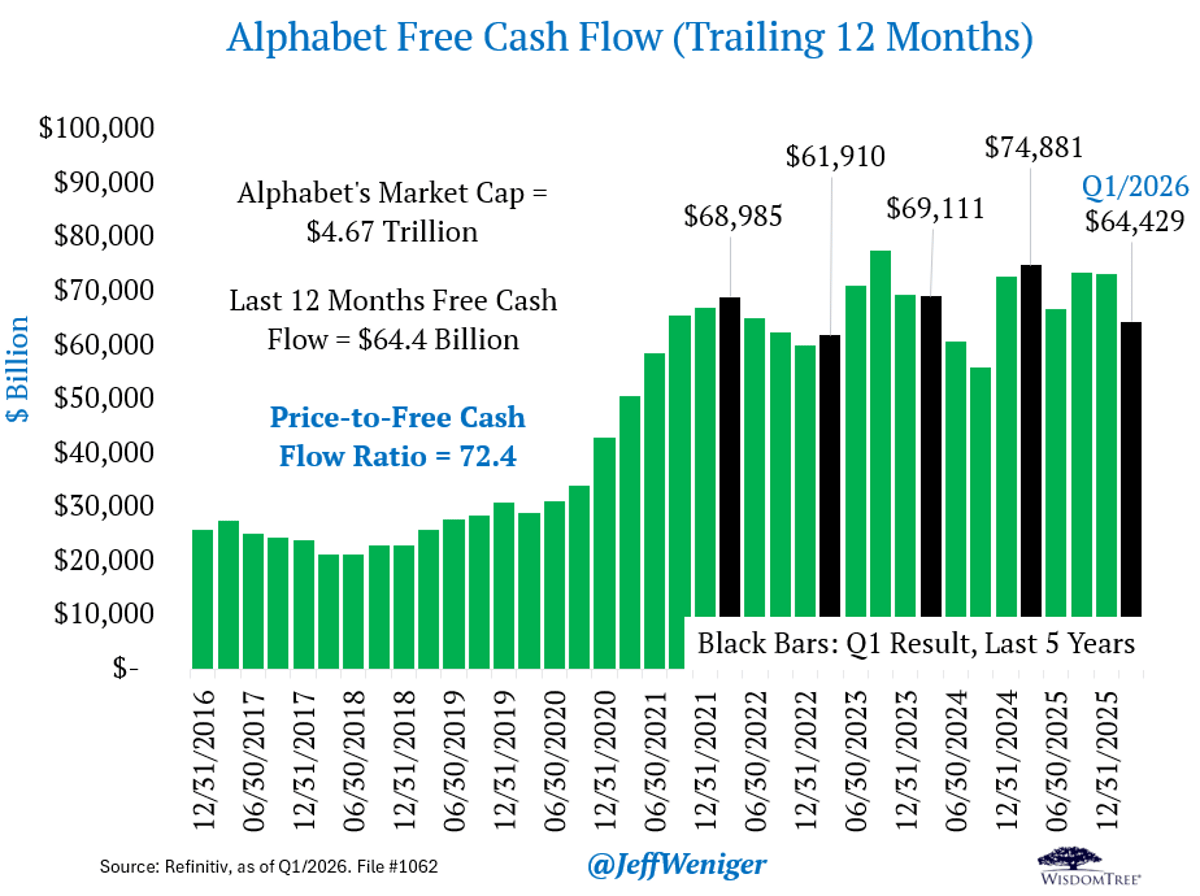

Alphabet's 72× FCF Valuation Risks Stagnant Cash Flow

With a $4.67 trillion market cap, Alphabet trades for 72.4 times free cash flow. The capital expenditure ramp-up has been droning on since Covid, leaving FCF in sideways limbo for a couple years now. How long the market will give...

AMD's Server CPU TAM Surges, Revenue Soars 70%

Some color from the $AMD call that wasn't in the release. -Server CPU TAM revision. From ~18% annually (FAD November baseline) to >35% annually, reaching >$120B by 2030. This is a structural reframe. -Q2 server CPU revenue guide: >70% YoY. -Q1 server...

Long-Term Portfolio Soars on MU, INTC, SNDK Gains

Simple strategies applied for the long term. Main $IBKR account which contains Weekend Trend Trader and Trade Long Term Portfolios. The latter is on a tear due to the likes of $MU, $INTC and $SNDK. https://t.co/zXSYjoNEU4

AMD Forecasts 35% YoY Rise in Server CPU Market

$AMD @LisaSu conviction that CPU server TAM 35% YoY driven by agentic. This is actually going to be more fun to track than GPU/ASIC volumes YoY :)

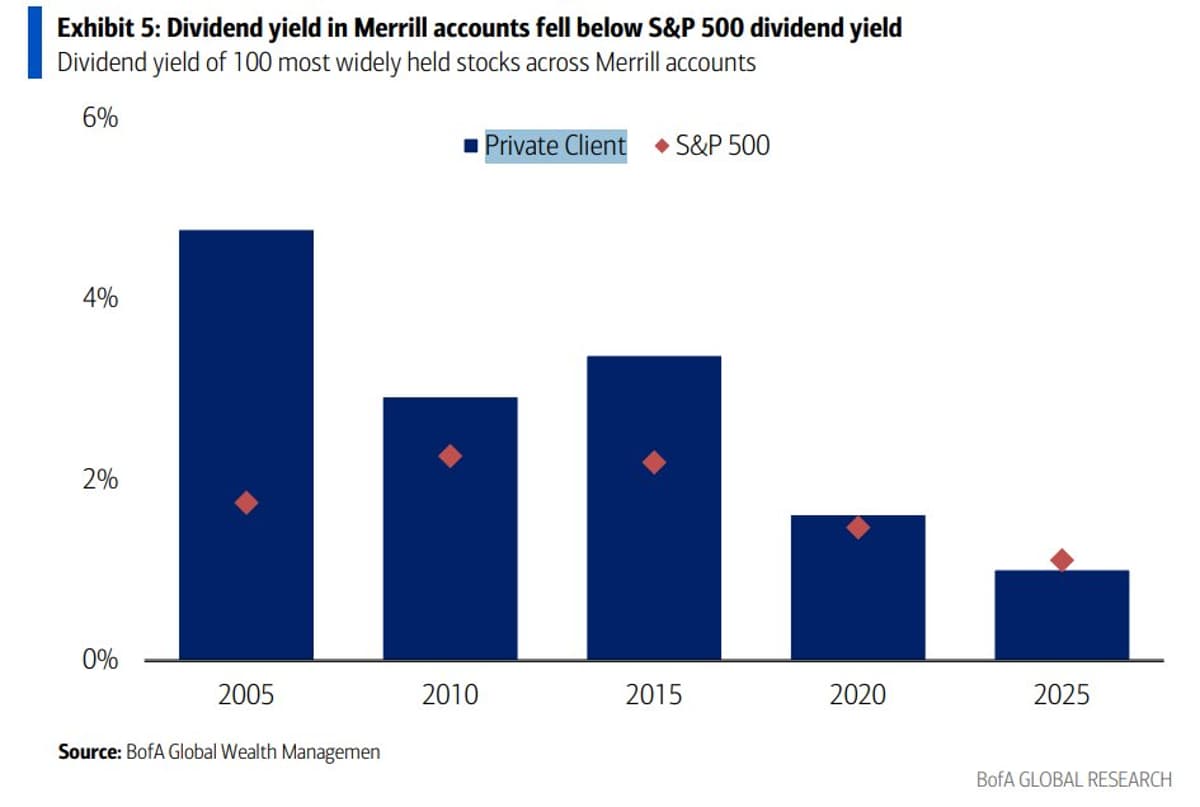

Dividend Yields Plunge From 5% to Under 1%

Whither yield investing? Dividend yield of 100 most widely held stocks across Merrill accounts was near 5% in 2005... under 1% today BofA https://t.co/5Qvx9oWTwH

Airbnb Overvalued at 29× Earnings, Wait for Entry

Airbnb at $140? Too pricey for me. Great company, but 29x earnings with mature growth is a risky bet into earnings. I’d rather wait for a better entry. 📉 ABNB

Yardeni Predicts Rally Will Persist Into Next Year

Ed Yardeni tells CNBC the market rally has legs and will continue into next year. He's optimistic on equities despite recent volatility. https://t.co/tknBHpCZ0W

Invest with Downside Focus, Not Hopeful Upside

Smart investors don't sleep well because they own great businesses. They sleep well because they know what could permanently destroy them, and haven't bought it. 1️⃣ Identify the real downside, not the hopeful upside 2️⃣ Margin of safety is insurance against your own...

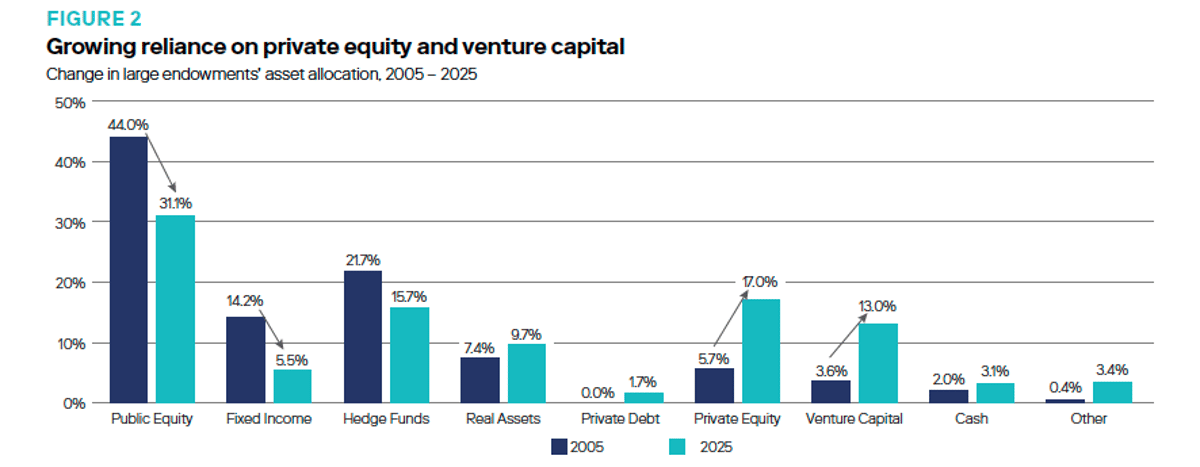

Endowments Boost Private Market Allocation by 22.4%

Over the past 20 years, large endowments have upped their VC/PE/PC allocation by 22.4 percentage points Mainly at the expense of public equity and fixed income... via @neubergerberman https://t.co/hR6yaFPBn7

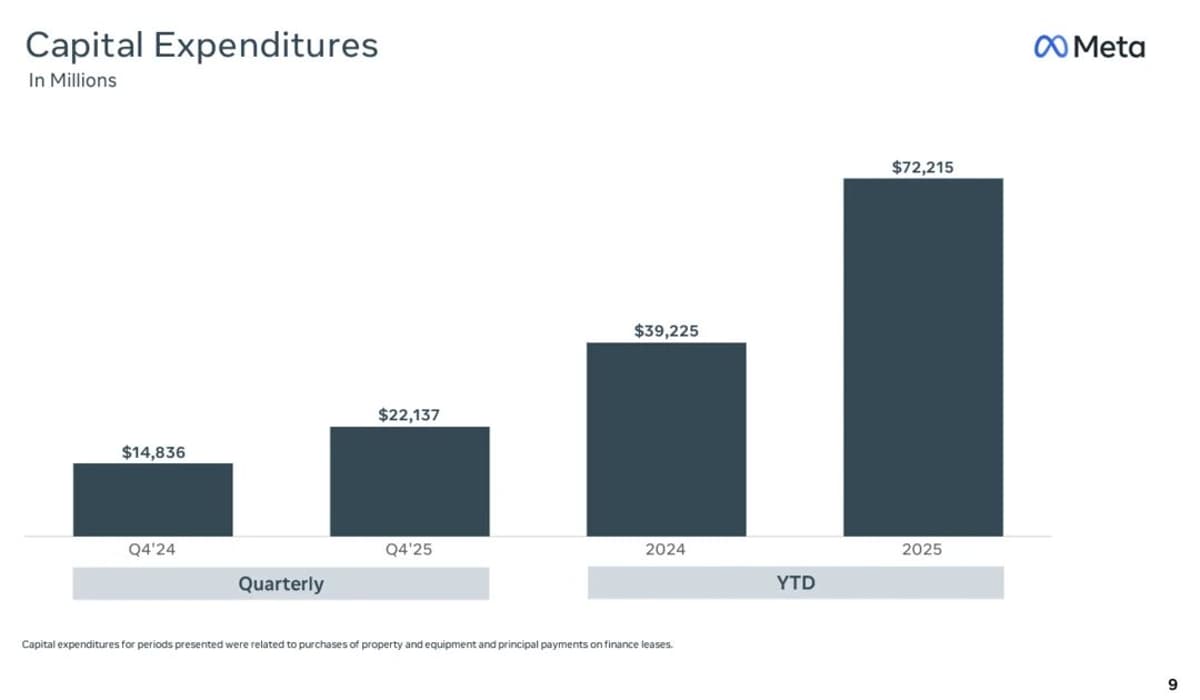

Meta Q1 Beats Forecast, Spends More on Capex

Meta's first quarter results handily topped expectations and came with the usual rise in capital expenditures. Here’s what you need to know https://t.co/l5qNyVhKBT #ArtificialIntelligence #Innovation #Technology #Tech #TechNews https://t.co/EodEGuDNKL

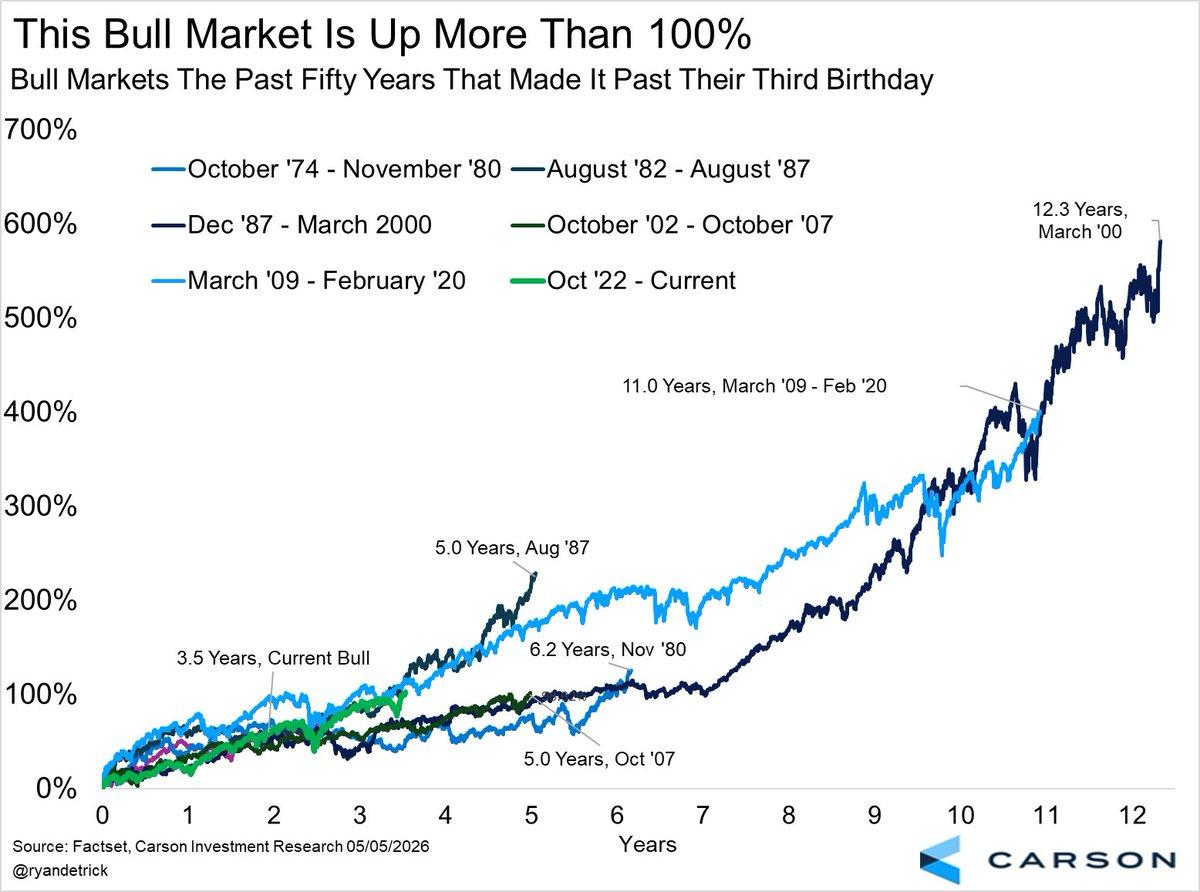

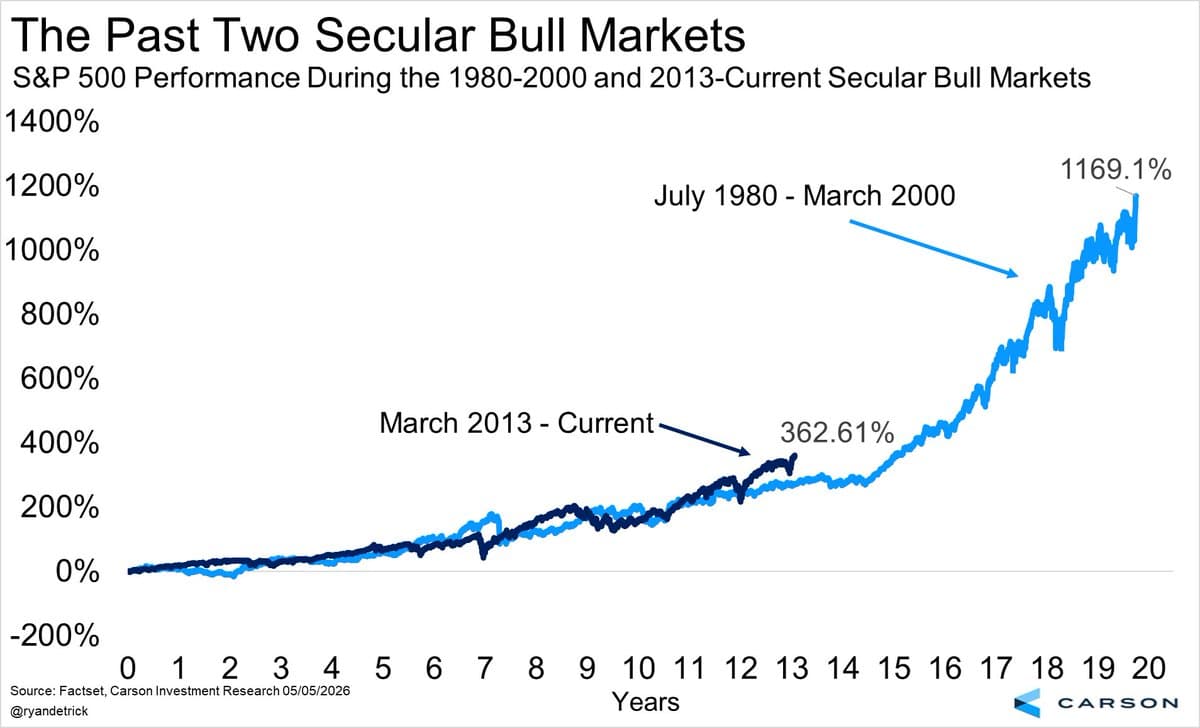

S&P’s 103% Rise Mirrors Past Bull Market Patterns

From the Oct '22 lows, the S&P 500 is up nearly 103% after today. Here's what the previous five bull markets that made it this far looked like. The bottom line? Years more of gains would be perfectly normal. https://t.co/FTzh4IWKYf

13-Year Bull Market Surpasses 80s/90s Gains

This secular bull market started in March 2013 and after today's latest new high is up 362.61% in just over 13 years. This one is now running above the '80s/'90s secular bull, but that one had a lot left. Will this...

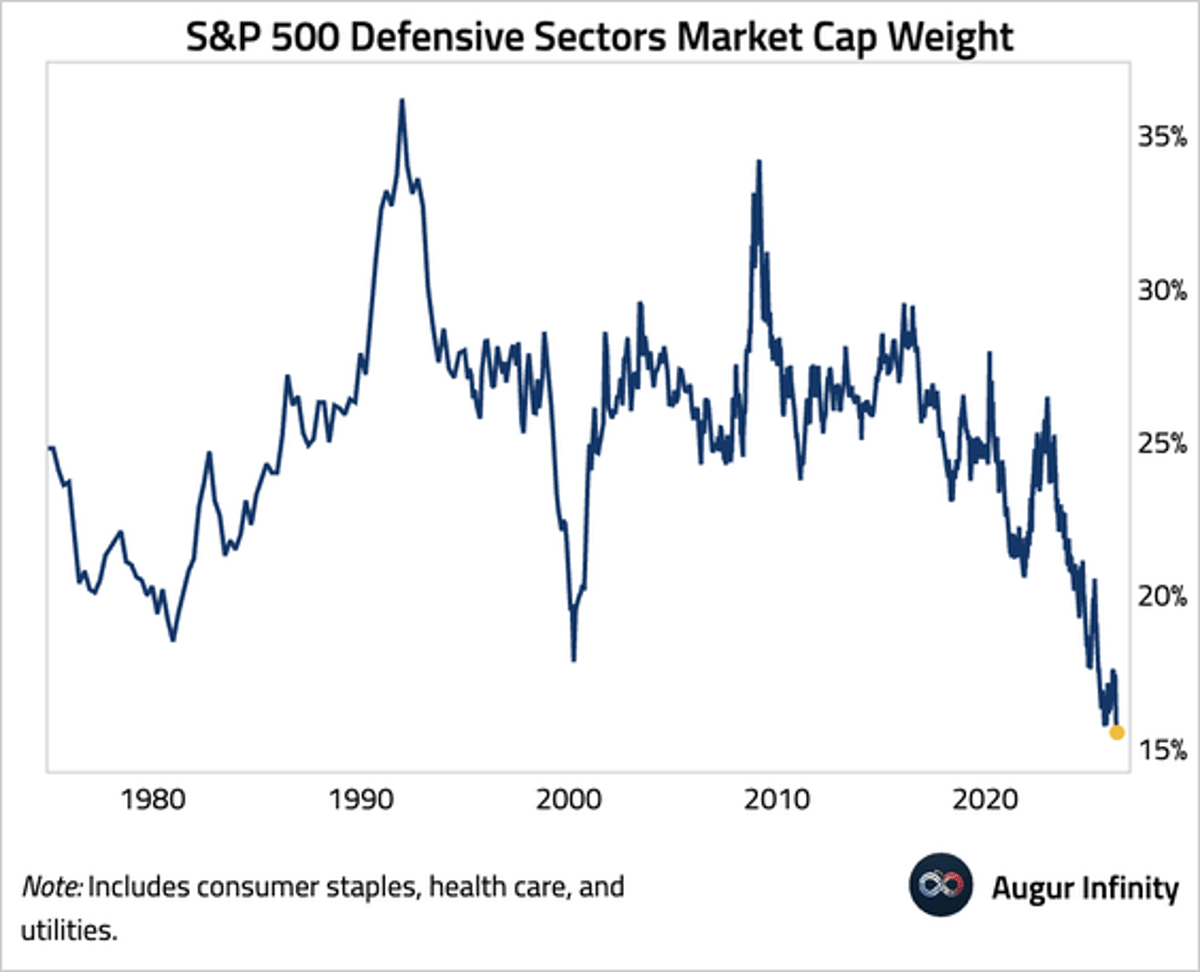

Defensive S&P 500 Sectors Hit Record Low Weight

The market cap weight of defensive sectors in the S&P 500 has fallen to a record low @augurinfinity https://t.co/KvIcxIReRU https://t.co/N5uatfPACb

Hold on Fundamentals, Trim when only Price Spikes

Saw this question on Reddit this week: "What do I do when a stock goes up 50% - do I sell or let it ride?" Here's the framework I use: 1. Did the fundamentals improve or just the price? If revenue/margins/insider buying all improved...

Unlock 10x Returns: Fisher’s 5 Growth Secrets

Warren Buffett once said he was "85% Graham and 15% Phil Fisher." Most people study Graham’s value metrics, but they ignore the 15% that actually leads to finding stocks with 10x potential. I just reread Fisher’s "Common Stocks and Uncommon Profits."...

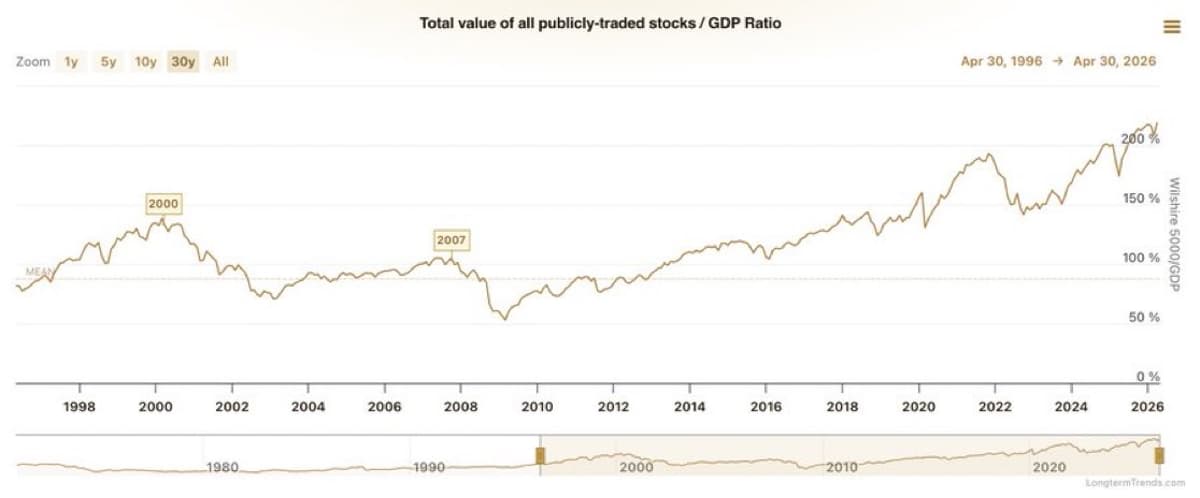

Market Hits Record Valuation, Buffett Indicator Tops 227%

Stock Market reaches it’s most expensive valuation in history after the Warren Buffett Indicator hits 227%, surpassing the Dot Com Bubble and the Global Financial Crisis: https://t.co/c3rpLbz8So

Rising Crack Spreads Boost PSX: Watch for Cup Handle

$PSX Daily. Quality refinery stock. With "crack spreads" rising, and earnings out of the way for this name, makes sense to keep this on watch long. Ideally a few more days of a "handle" forms after "cup." https://t.co/ohiGjv3H4S

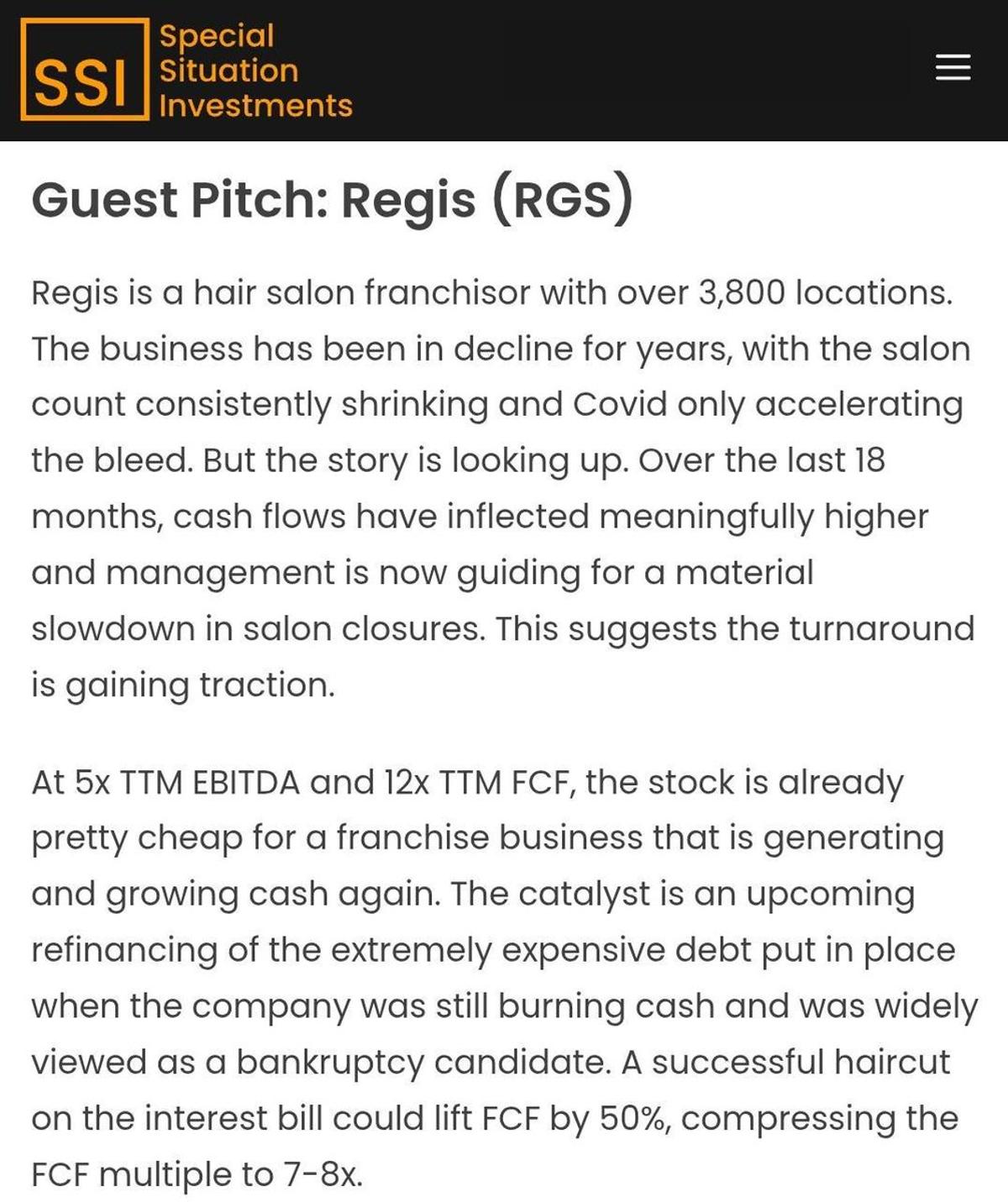

RGS Turns Around: FCF Rising, Refinancing Could Cut Valuation

$RGS, a hair salon franchisor, is crossing the Rubicon in its turnaround. FCF inflecting, closures slowing, massive refinancing incoming. Already cheap at 12x TTM FCF. If refinancing succeeds in cutting interest, co trades at 7-8x FCF. Full pitch: https://t.co/wcFgp9Utv7 https://t.co/XKWI6URRHG

Secular Bull Market Likely Continues for Years

We are in a secular bull market that could have many years left. I've been saying this since 2013 and don't think it is over yet. I discussed it all in our latest @CarsonResearch blog. https://t.co/NZH0IouJr4

Market Mispricings Are a Shopping List, Not a Warning

Most people think the casino and the stock market are different places right now. They're not wrong. Buffett sees it too. The difference: casinos don't occasionally misprice great businesses at 40 cents on the dollar. That's not a warning. That's a shopping list.

AMD Poised to Beat Estimates; Watch GPU Ramp

$AMD reports after close. Consensus ~$9.84B / ~$1.30 EPS (+32% rev, +35% EPS). Stock up 74% in April sets a high bar. I think they will beat. I’m watching a few things: MI355 ramp, MI400/Helios timing, Meta 6GW progress, EPYC...

Mega IPOs Push New Billionaires Toward US Asset Purchases

the equity supply/demand picture could definitely be complicated by the behemoth IPOs this year. but then i ask, what do newly minted multimillionaires and billionaires do with a flood of liquidity? marginal propensity to consume nearly topped out… i think they...

US Stocks Hold Steady as Europe Drags, Global Outlook Bullish

Vanguard global stock index is up about the same amount as the US market this year. Europe is acting as a drag so far this year with other markets (eg Brazil) outperforming strongly. Seems like international investors have got comfortable with...

Use a 351 Exchange to Tax‑Defer NVDA Holdings

Your client has $2M in NVDA they won't sell. "The taxes will kill me." Most advisors stop there. The 351 Exchange breaks the trap. Tax-deferred. ETF-based. Liquid day one. https://t.co/0ev7Bt8ru8

Cloudflare’s Pre‑Earnings Run Highlights Long‑Term Software Bet

Nice push for here Cloudflare making a pre-earnings run over this long-term 225 supply area. Echoing what I’ve said all year, this remains my favorite software investment idea. (long) $NET https://t.co/Zsw2Aiq1bH

ROK Beats Forecast,

$ROK: strong beat/raise driven by Discrete +mid teens, Hybrid +HSD, Process +MSD. Org g double expectations at 9%, OM beat by 225 bps and +350bps y/y. Key ARR +6% and software +HSD makes this less cyclical going...

IREN's Mirantis Acquisition Could Lift Its Benchmark Rating

Definitely have to see the $IREN acquisition of Mirantis as a way to move them up the @SemiAnalysis_ benchmark list. Time will tell, but I'm sure this will move them from not-recommended. WIth all neoclouds' ability to leverage software for...

Holding MU Would've Yielded 10x Gains, Pabrai Missed

A few years ago, $MU was Mohnish Pabrai's largest holding at 80% but sold it in 2Q23 Hindsight is 2020, but if he simply just did nothing and held, he would be up ~10x

Diversified Mix Outperforms SPY Without Leverage

In 2026 you haven't needed leverage to beat $SPY in fact even at 30% cash you matched $SPY. All you have needed is a diversified portfolio of 10% Gold, 10% Commodities, 25% Major Index Stocks, and 30% Nominal bonds...

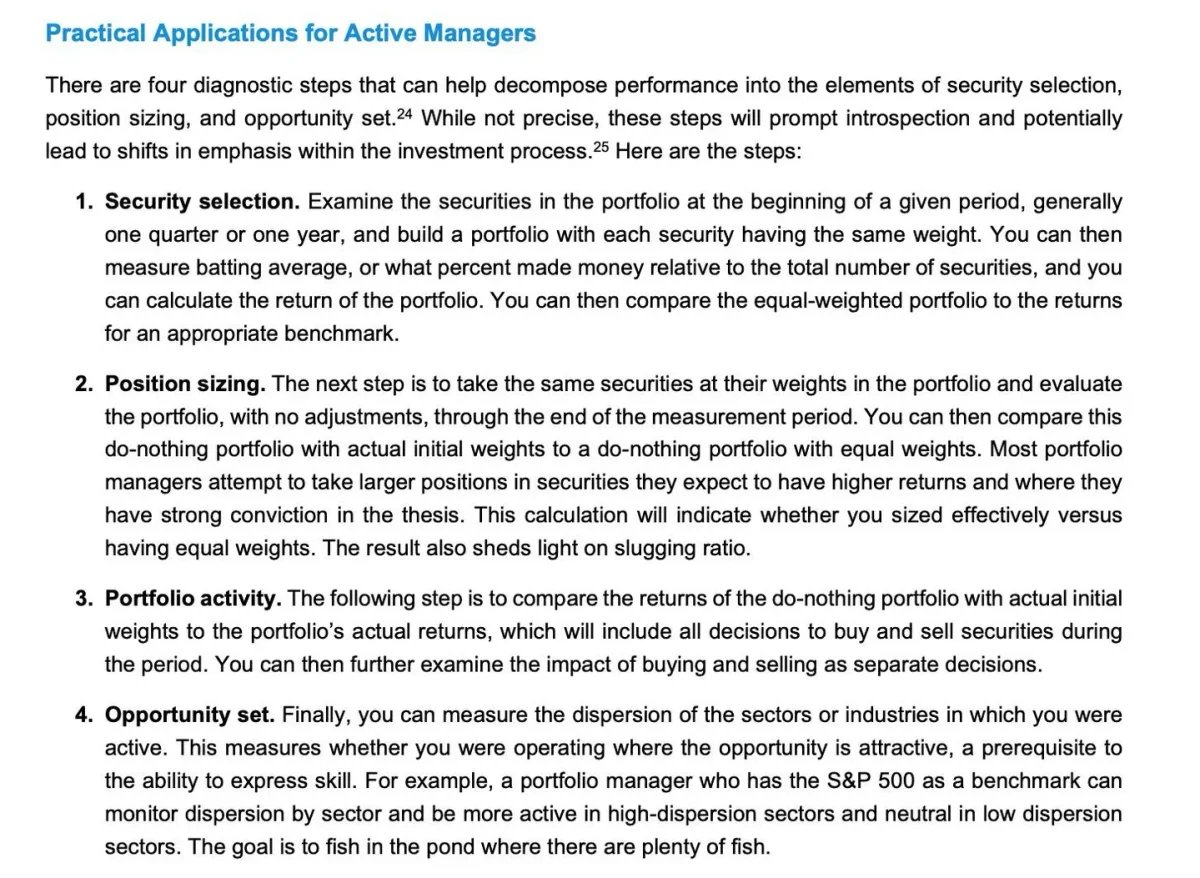

Four Key Steps to Measure Investment Performance

Michael Mauboussin's 4 steps to measuring performance 1. Security selection 2. Position sizing 3. Portfolio activity 4. Opportunity set

Buffett's Rule: Prioritize Fundamentals, Shun Flashy Stocks

Billionaire investor Warren Buffett's strategy? Stay away from flashy stocks, and assess fundamentals to find undervalued ones. https://t.co/qsceHG36d7

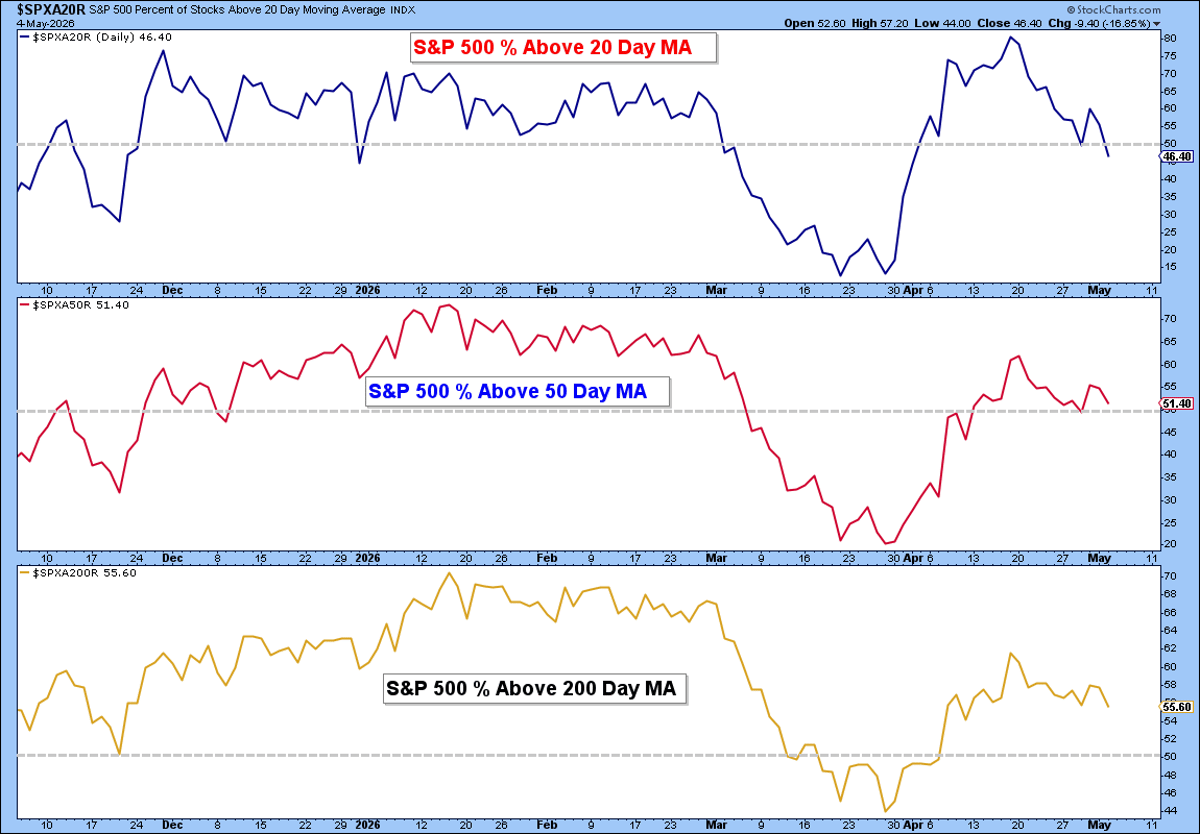

S&P 500 Bread

Not a call to be bearish just a data point to be aware of. Breadth weakening under the surface for the S&P 500. https://t.co/LcO3zUQv6W

Young Millionaires Ditch Complex Advice for Simple Index Funds

I am happy to see more young multi-millionaires abandoning the illusion of excess investment returns sold by advisers pushing complex strategies for the simplicity of target date index funds in retirement accounts and $VTI / $VXUS, and a municipal bond...

Diversify with Gold and Commodities to Hedge Future Uncertainty

If you didn't own commodities and gold in your portfolio the last two years your portfolio missed the big moves in those assets which blew away SPX. GLD, TLT, GSG, and SPY are all gonna have shitty 10 year windows....

Talk to Management Early to Uncover Deal‑Breaker Insights

When investing in small public companies you can’t afford to wait until the end of your due diligence to talk to management. Why? Oftentimes one management conversation unearths differential insights that make the company completely un-investable or 3x more interesting...

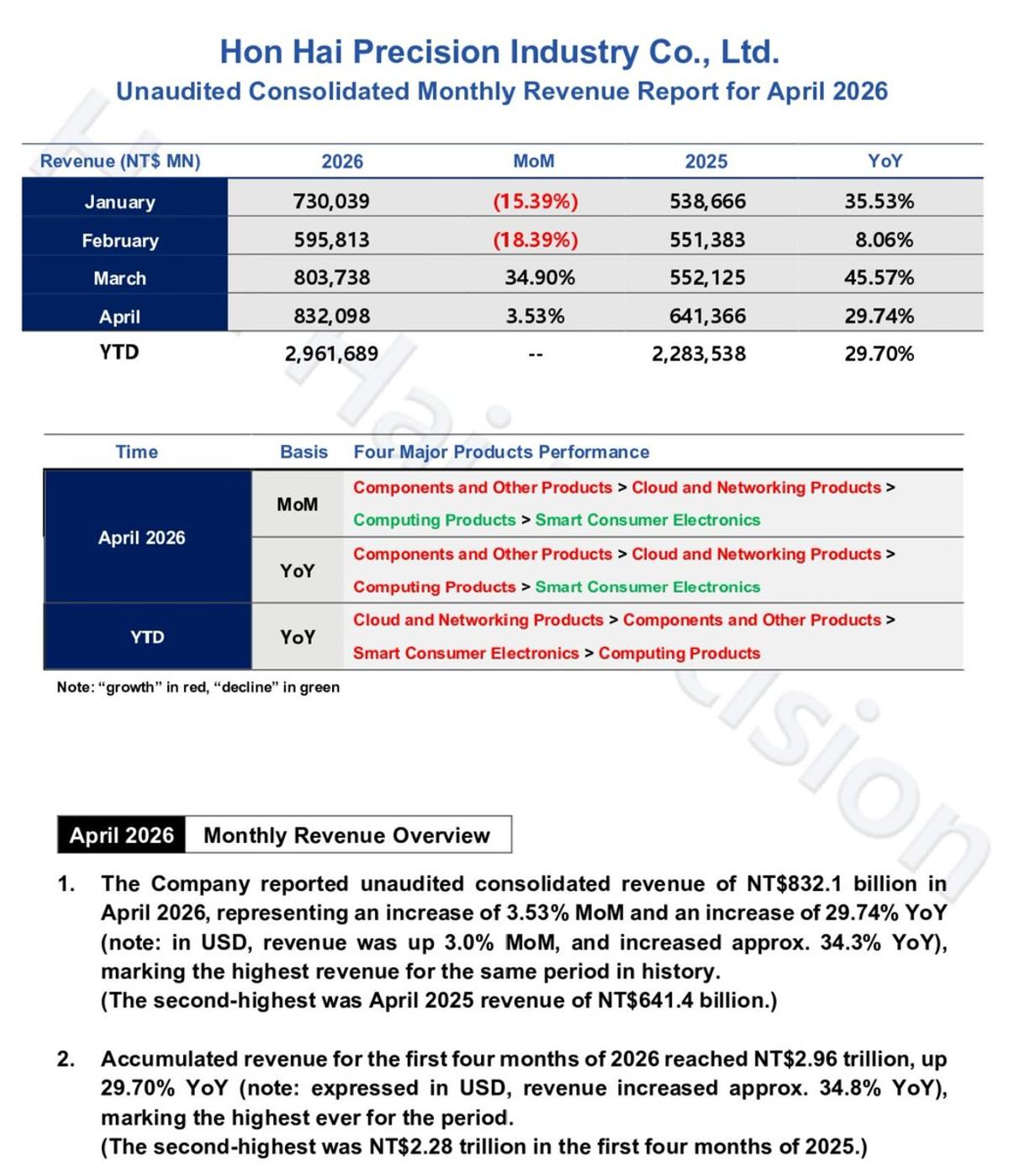

Foxconn Revenue Jumps 35% YTD Despite Base Effect

Just in: Hon Hai (Foxconn) revenue up 35% YTD (USD terms) Slight weakness in consumer electronics, but only because of a higher base the month prior. Some important things to remember: 1/ https://t.co/Gx6A1kdlF0

Over Half of NASDAQ Top 100 Boost Earnings 50% YoY

NASDAQ: 54 of the 100 have reported an epic y/y Earnings Acceleration of +50% https://t.co/3jhMeGis8O

Patience and Diversification Beat Hype; No Shortcuts

Sorry your goals take decades. Sorry diversification means missing the moonshot stock your friend won’t shut up about. Sorry market timing hasn’t worked for anyone, no matter who promised you it would. Sorry the boring portfolio outpaces the exciting one over 30 years. Sorry...

US Refining Tightness Fuels 2026 Margin Surge

US refining squeeze = opportunity: Post-2020 COVID closures + no major new builds since 1976 = tight capacity. Utilization ~90%, strong crack spreads boosting margins. Refiners like $VLO, $MPC, $PSX thriving in 2026.