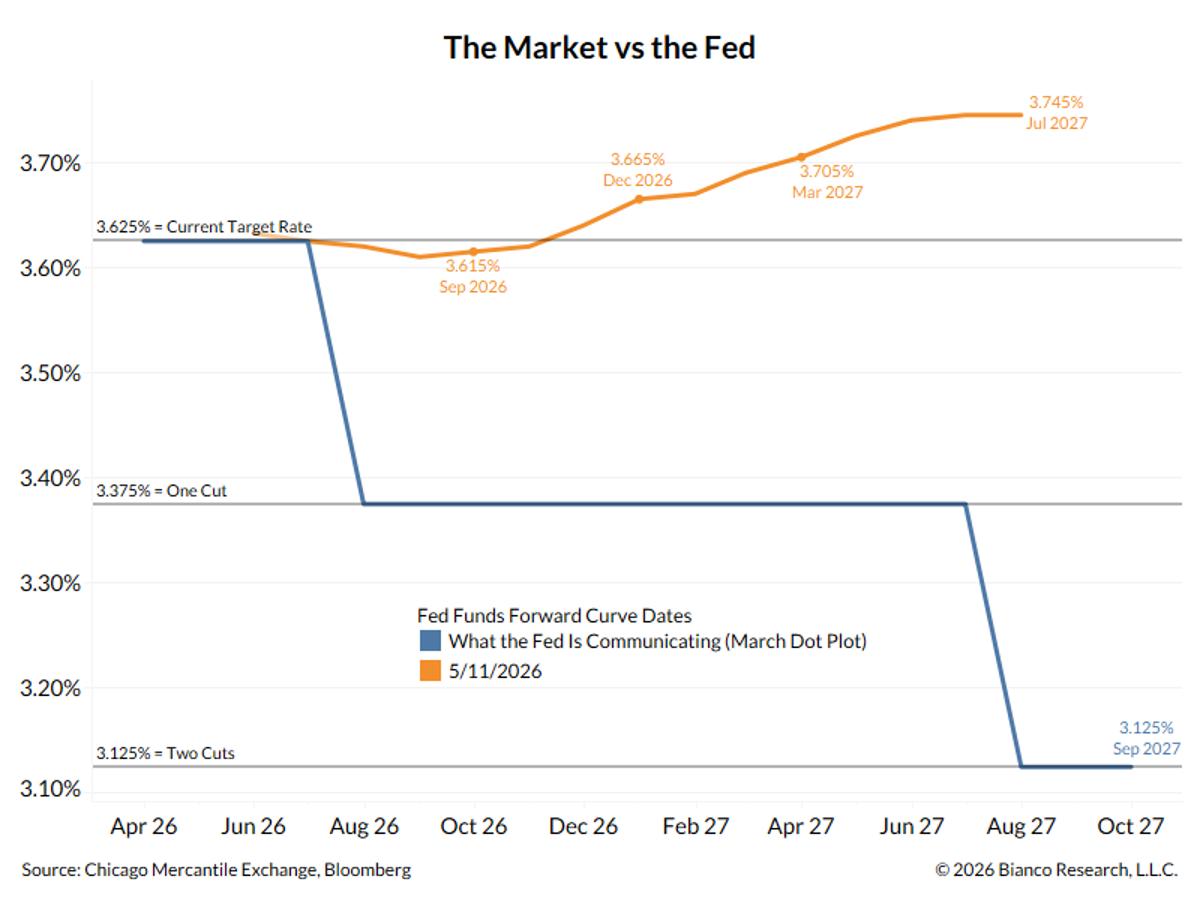

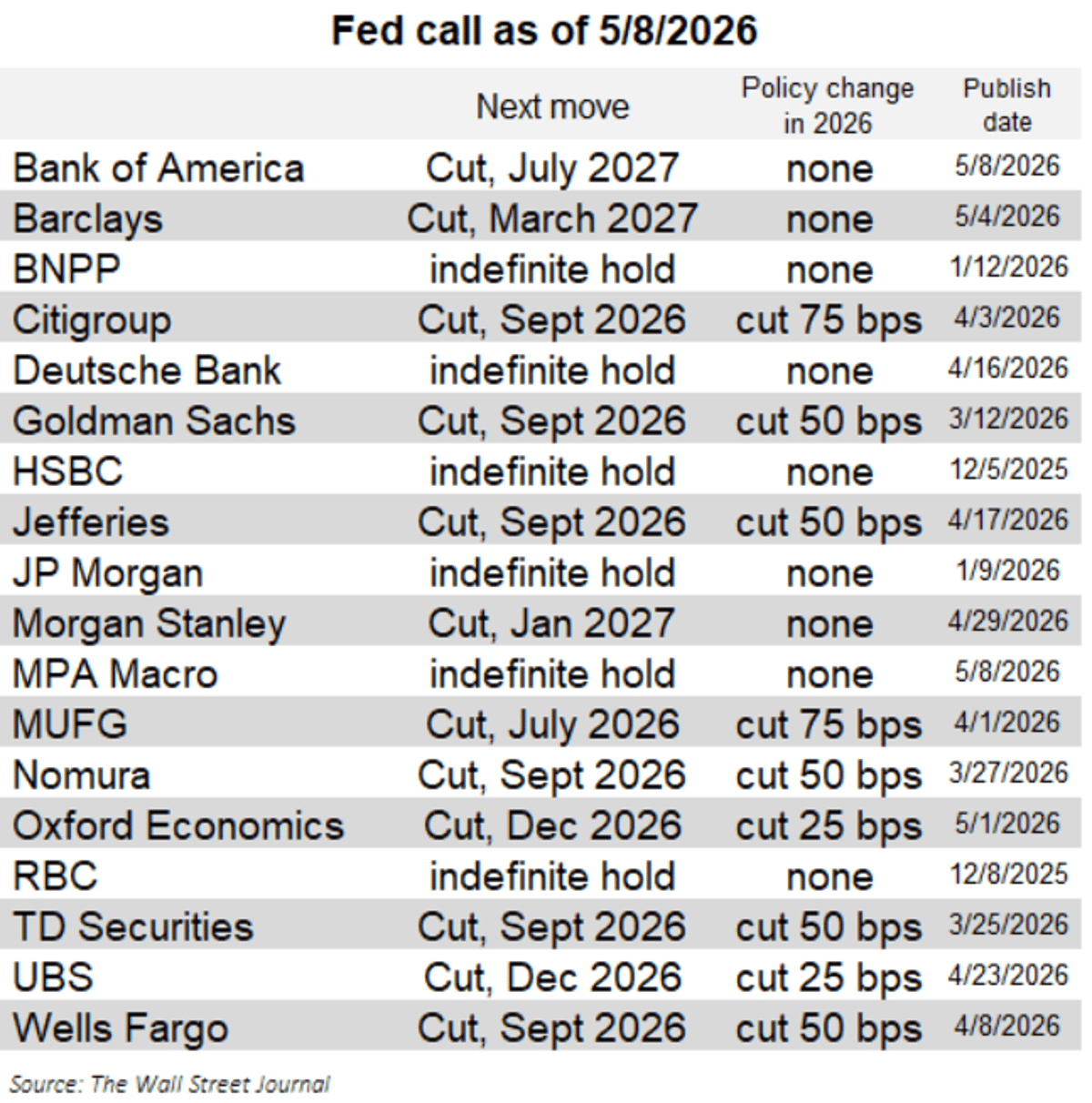

Fed Signals Cuts, Market Expects 2027 Hike—New Chair Faces Mismatch

The blue line is what the Fed is communicating. 2 rate cuts this year. The orange line is what the market is pricing in, a rate HIKE by Summer 2027. Warsh starts as Fed Chairman on Friday. High on his agenda is reconciling market perception with the Fed’s forward guidance. https://t.co/gBnw09BTTp

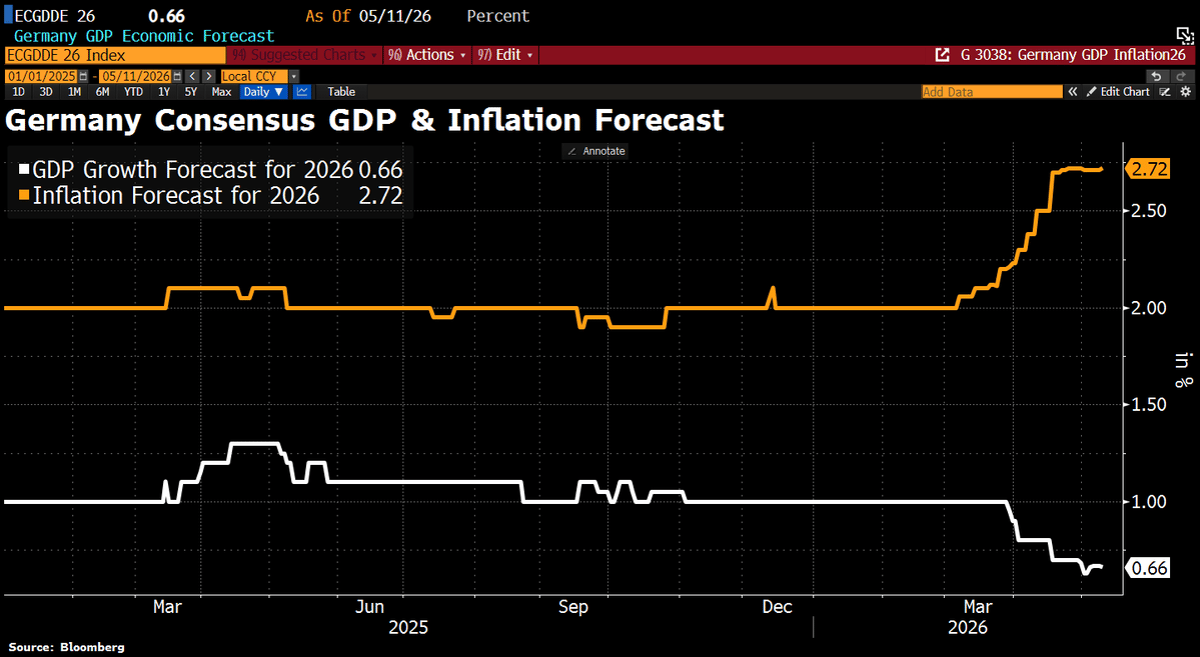

Germany Faces Stagflation as Growth Slows, Inflation Rises

Good Morning from Germany, which appears to be heading towards stagflation. Consensus GDP forecasts for 2026 have been revised down from more than 1% to just 0.66%, while inflation forecasts have climbed above 2.7%. Against this backdrop, the ECB is...

Fed Cuts Don’t Guarantee Bond Rallies, History Shows

For years, a familiar pitch has followed every Fed cut: rates are dropping, so bonds should rally. But history is a little messier than that. Bond outcomes do NOT move in a predictable manner just because the US Fed changes policy. Source:...

China Acquires US Defense Assets Cheaply as Americans Fund Deficits

“Dollar dominance” as defined by many here on X = China buys up the US defense industrial base on the cheap while US Boomers & Banks buy negative real yielding USTs to finance US deficits (aka lose capital on a...

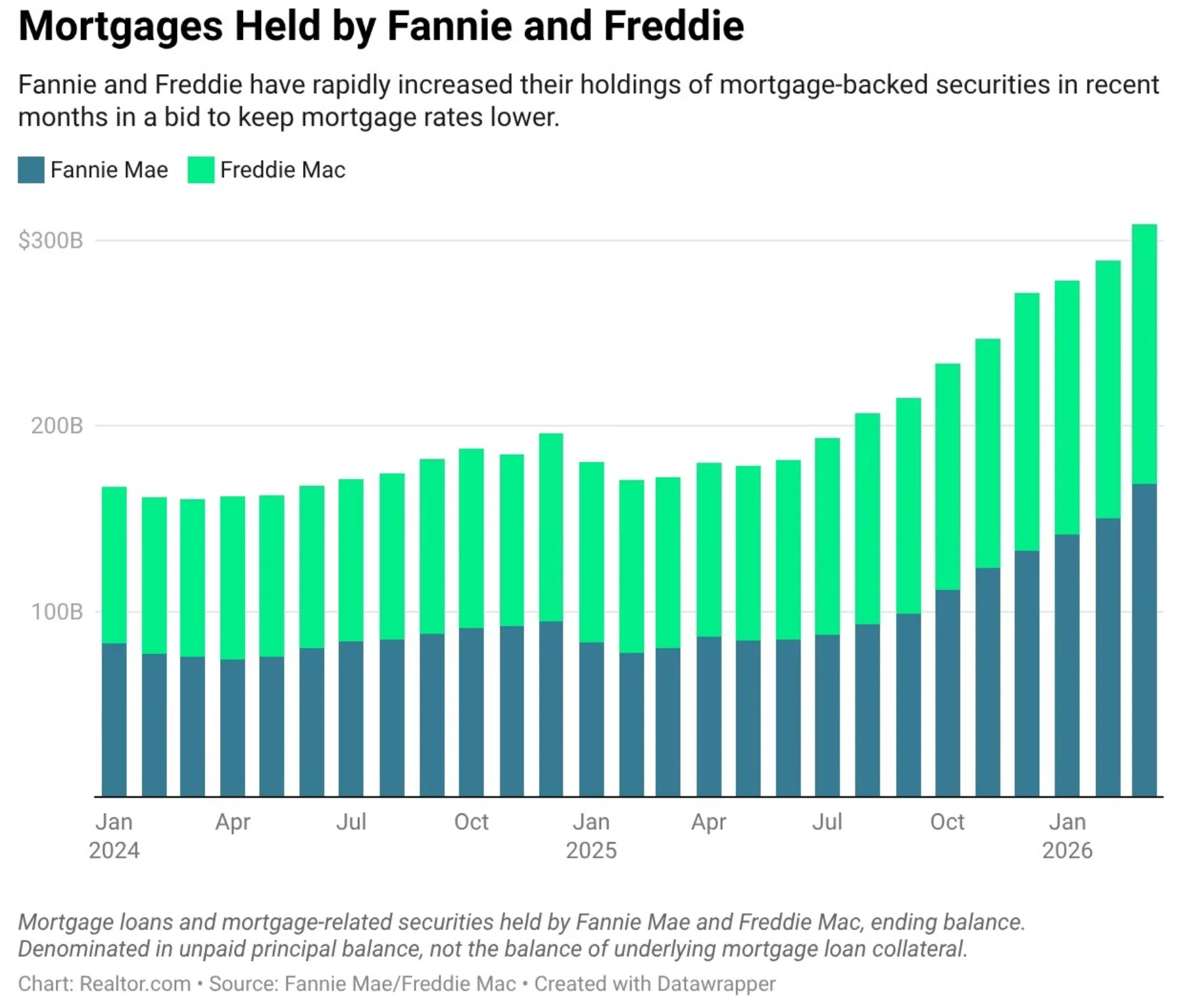

MBS Buying May Not Significantly Lower Mortgage Rates

I wonder if these MBS purchases have kept mortgage rates lower than they otherwise would be. Would the 30-year fixed be ~6.75% today instead? Problem is other administration policies, e.g. tariffs, war, etc. basically absorb and offset any of the benefit.

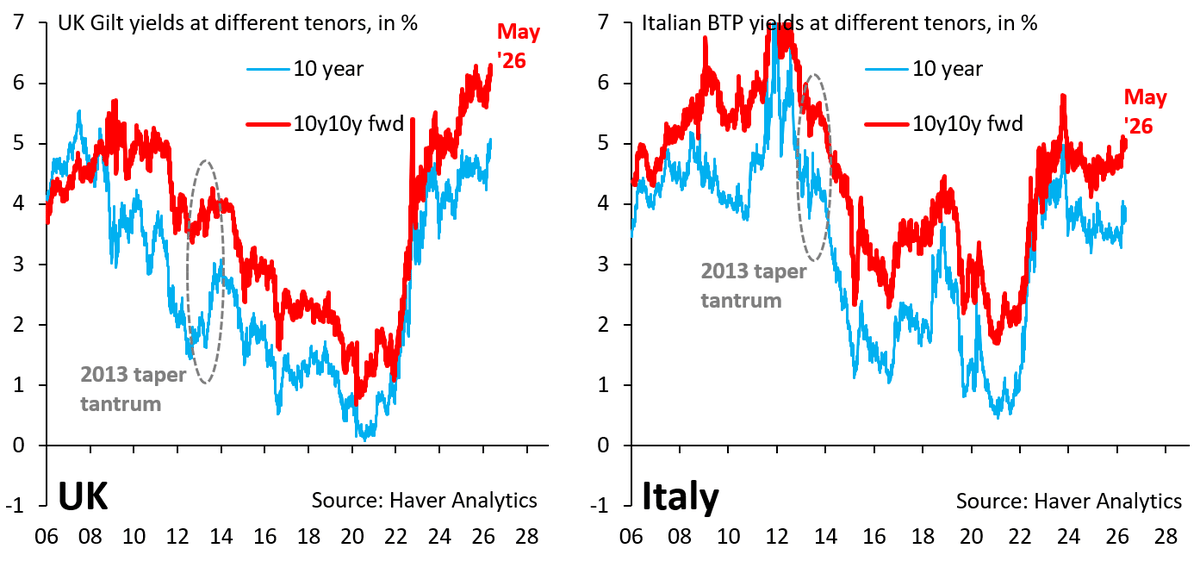

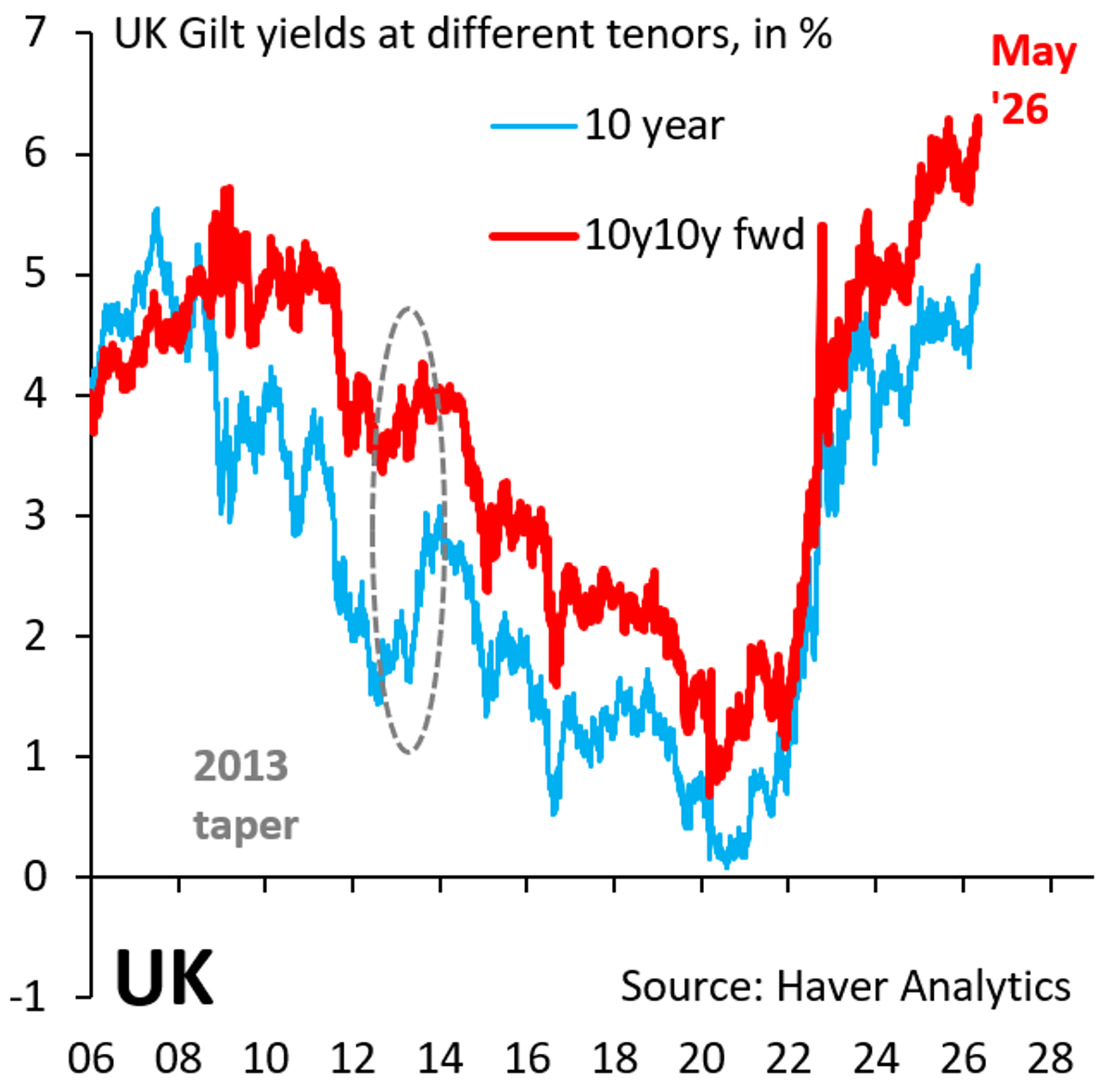

UK Yields Exceed Italy, Not a Weakness, ECB Cap Effect

The UK's long-term gov't bond yields (lhs) are now far above those of Italy (rhs). This doesn't mean the UK is in worse shape. It's just a reflection of past ECB actions to aggressively cap Italian yields. I talked about...

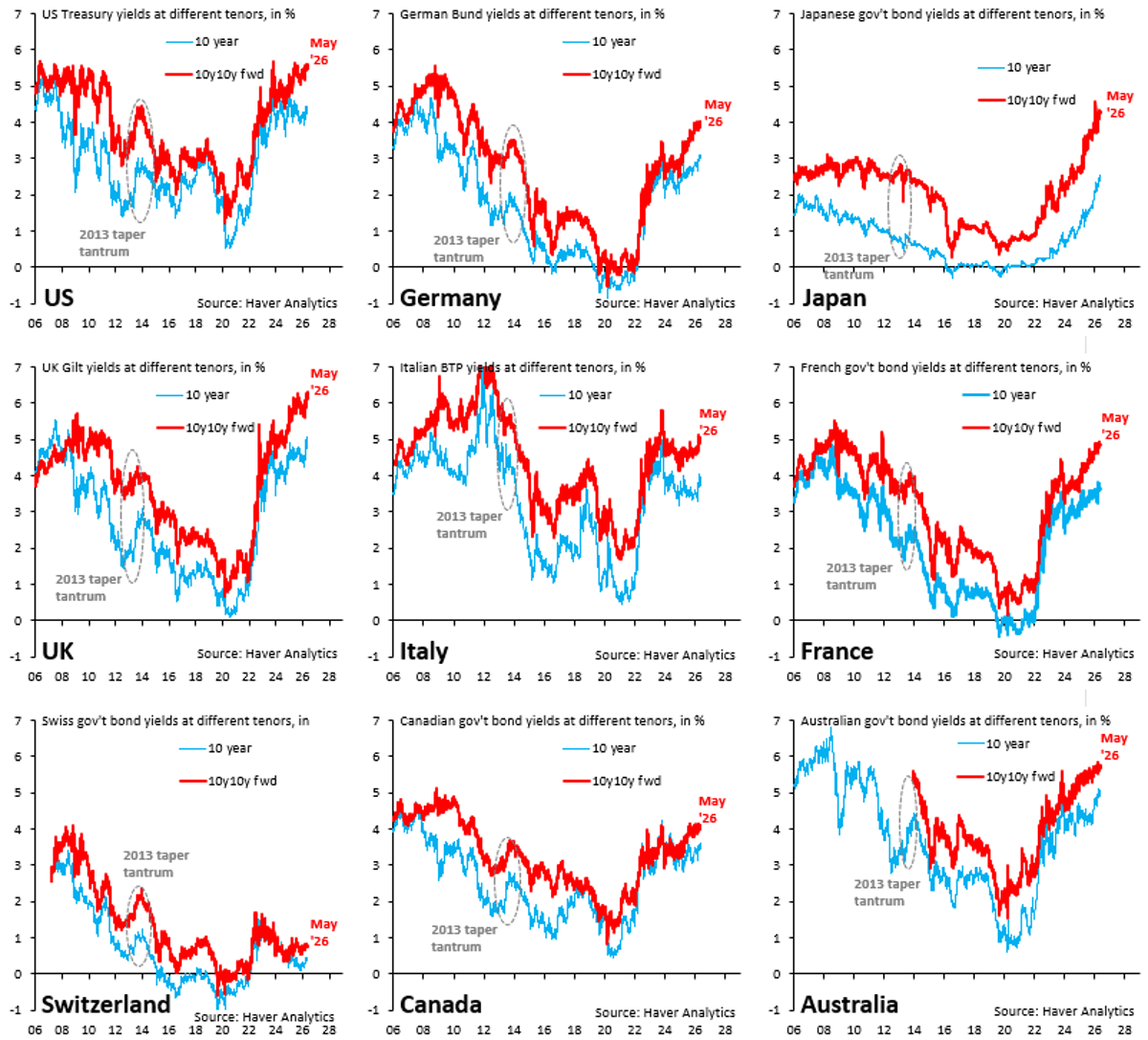

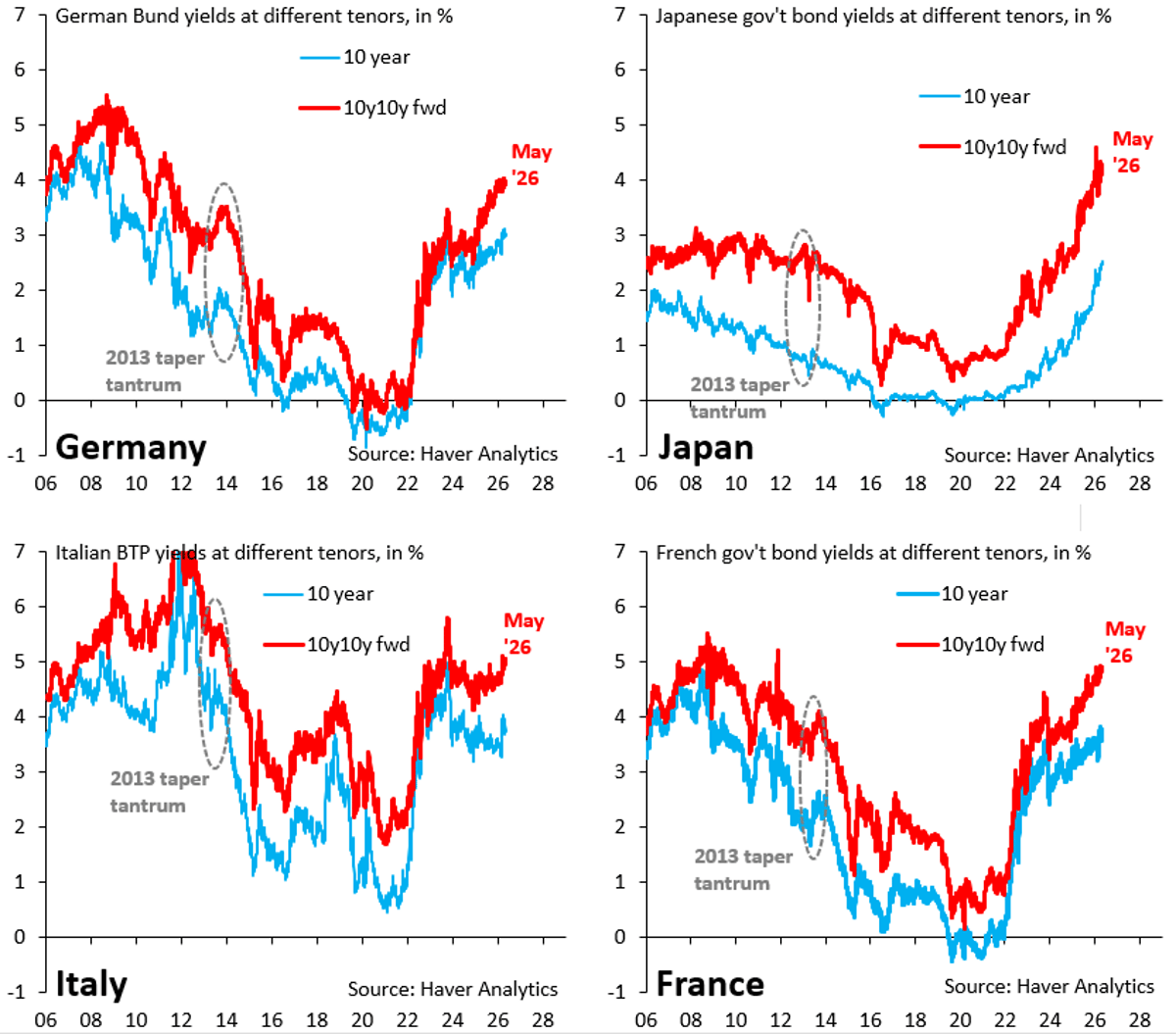

G10 Long-Term Yields Hit Record Highs Amid Debt Surge

In the UK, long-end yields are at all-time highs, but - if you look across the G10 - that's true for many other countries as well. The US, Japan, France and Australia all have the highest yields in a very...

AI Deflationary Shock Flattening Yield Curve Amid Oil Rise

One of the more interesting signals in the data right now is that the yield curve continues to flatten despite a significant increase in oil prices on a trailing three-month basis. Historically, in a more traditional economic cycle, an energy...

Waller Warns Productivity Surge Could Raise Borrowing Costs

Fed's Waller: starts by trashing Goolsbee's model -- anticipated productivity will be associated with higher borrowing costs if 'everyone' scrambles to invest, acting as a dampener.

Goldman Delays Final Fed Cuts to Late 2026, Early 2027

“We are pushing back the final two Fed rate cuts in our forecast by one quarter to December 2026 and March 2027.” - Goldman

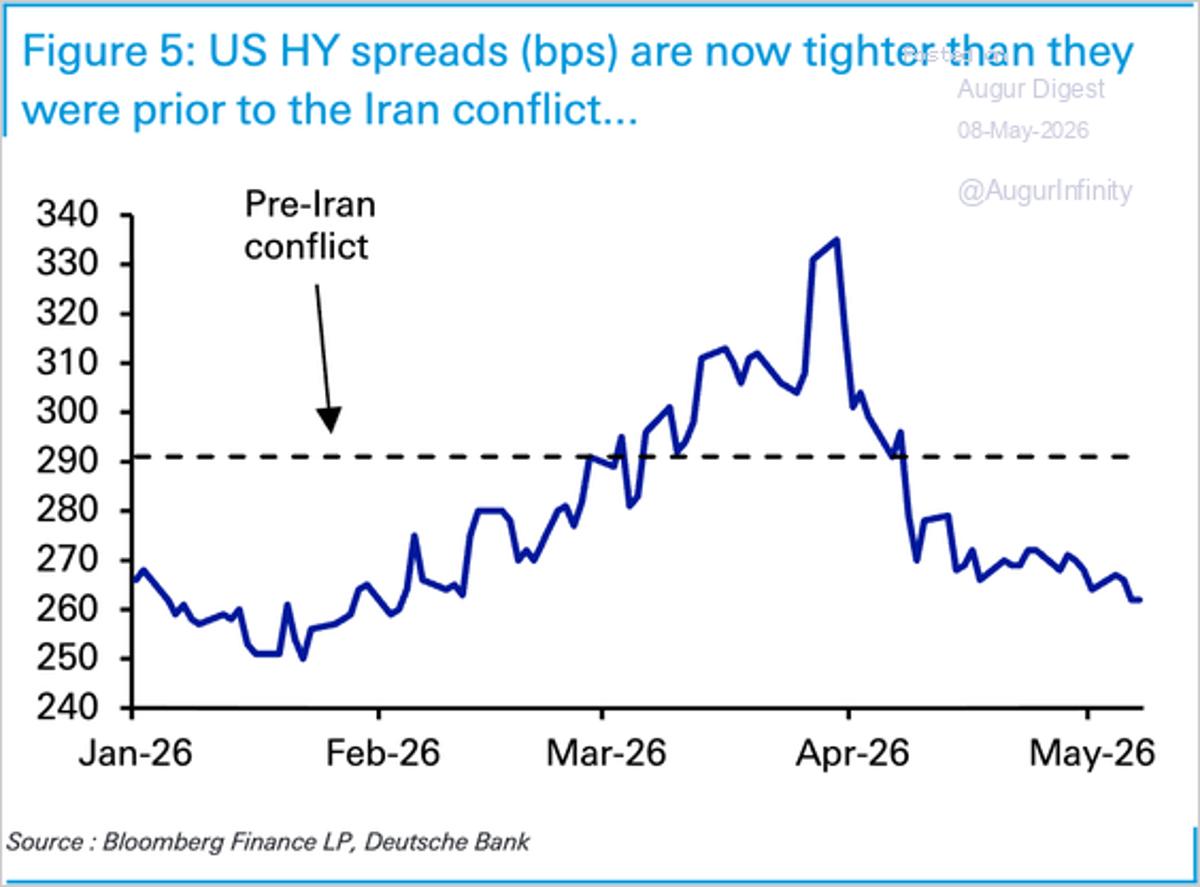

High‑Yield Spreads Hit Pre‑Iran Conflict Lows Globally

DB: US high-yield spreads are now tighter than levels prior to the Iran conflict... in Europe too @augurinfinity https://t.co/Yu7IqKp2Aw https://t.co/s9fwrJSPan

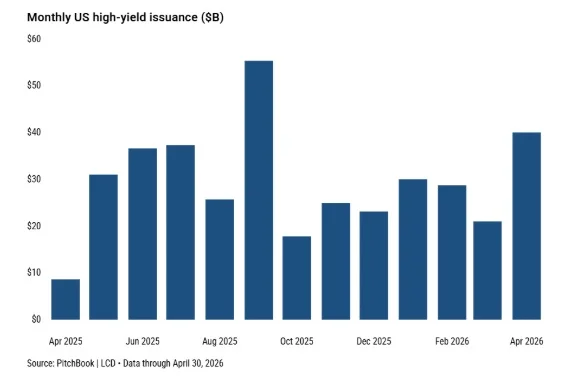

AI Infra High‑Yield Bonds Double, Outpace 2025 Forecast

High-yield bond issuance for AI infra: 2025 full year: $13.5B 2026 YTD (through April): $26.6B Already doubled last year's total and ahead of most full-year estimates Source: Pitchbook

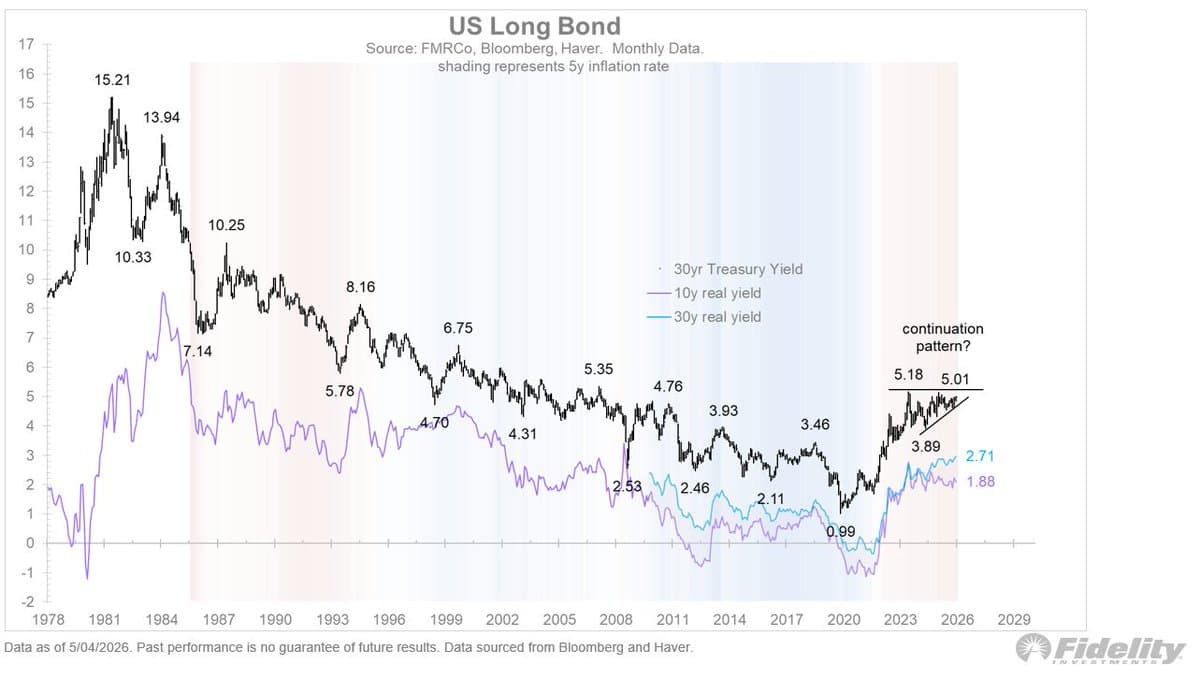

10-Year Yield Above 4.5% Signals Trouble Ahead

All this may be happening when the long bond is coiling inside what looks like a bearish continuation pattern. Real rates are rising, as are inflation expectations via the TIPS market. Remember: nothing good happens above 4.5% (for the 10-year)....

Half of Fed Forecasters Now Expect No Rate Cuts This Year

More sell-side firms and Fed watchers are removing/delaying cuts from their outlook, including a couple forecasters after the April NFP. Half now see no cuts this year (and risks are clearly tilted to this group continuing to grow given inertial...

Bond Investors, Fed Use Different Treasury Valuation Models

Bond investors and Fed policy makers use different models on how to look at Treasuries, @HannoLustig says. @HooverInst

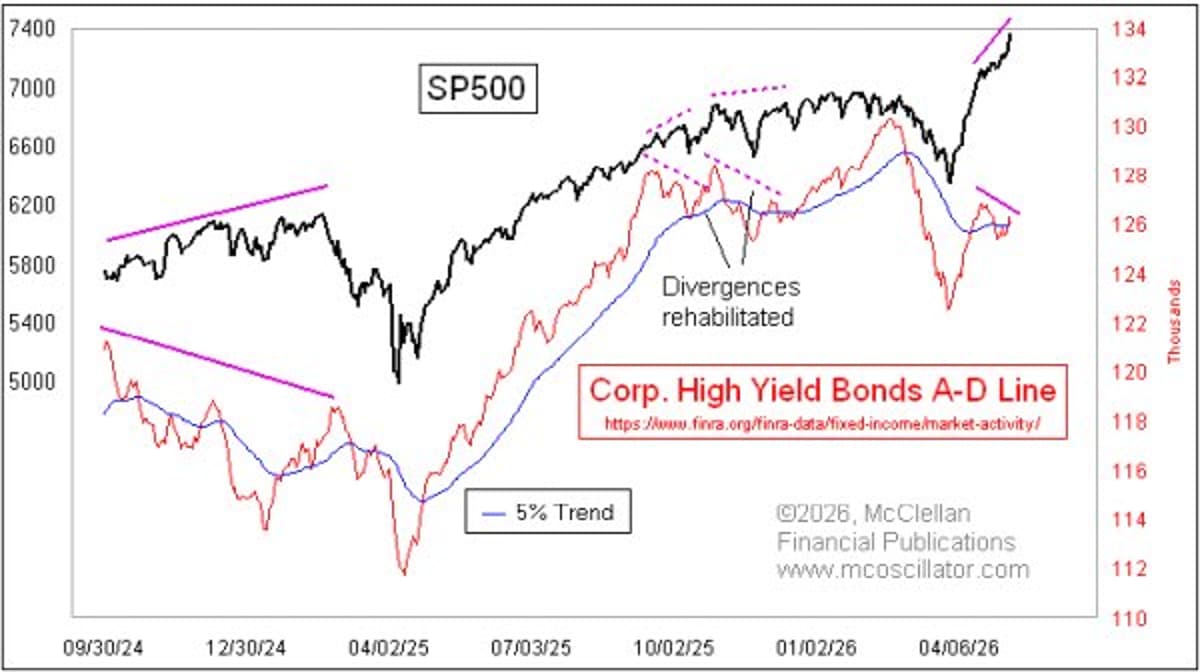

Bearish Bond Divergence Signals Liquidity Stress Ahead

Curious… “The daily Advance-Decline (A-D) Line for high yield corporate bonds is making a bearish divergence versus the SP500. This is a concern because it conveys a message saying that there are liquidity problems.” @McClellanOsc I would say this is a...

BofA Delays Fed Rate Cuts to 2027

"We push the two cuts in our Fed forecast out from Sep-Oct '26 to Jul-Sep '27. The data simply don't warrant cuts this year." - BofA

Sticky Inflation Turns Junk Bonds Into Attractive Carry

Geopolitics & sticky inflation are creating a wild bond market. The surprise? It’s making high-yield "junk" bonds look attractive for carry. Defaults stay low, so investors are reaching for that extra yield. 📈 HighYieldBonds

Janus Henderson Shifts to Defensive Stance After Q1 Edge

Janus Henderson Flexible Bond Fund slightly edged its benchmark in Q1 📈. Managers leaned into risk-on trades like corporate bonds & Japan duration, but are now playing defense—trimming duration & staying cautious on high-yield. A "two-way market" ahead with tariffs...

War Headlines Dampen Usual Pre‑auction Buying Optimism

Normally a nice level to love tap a few 5s before 3y auction on Monday, but war news and weekend headlines tough to ignore

Gundlach Pushes Demand for His Own Holdings

Already taken 3x calls this morning on this nonsense story. Just Gundlach trying to generate demand for something he already owns. Create liquidity and get lower coupons bid up on the spline.

US Treasuries Focus on Soft Wages, Steady Unemployment

USTs keying on soft wages and steady UER and shaking off headline beat. It seems

Issing in the Wind: Otmar Issing’s Strategy Explained

I call it Issing in the wind, after the guy - Otmar Issing- who came up with this strategy

Oil Shock to Accelerate Long‑Term Yield Rise

I'm doing my usual live stream tomorrow morning at 9 am (ET). I'll be focusing on all things debt, especially the rise in long-term yields and why the latest shock - the rise in oil prices due to the war...

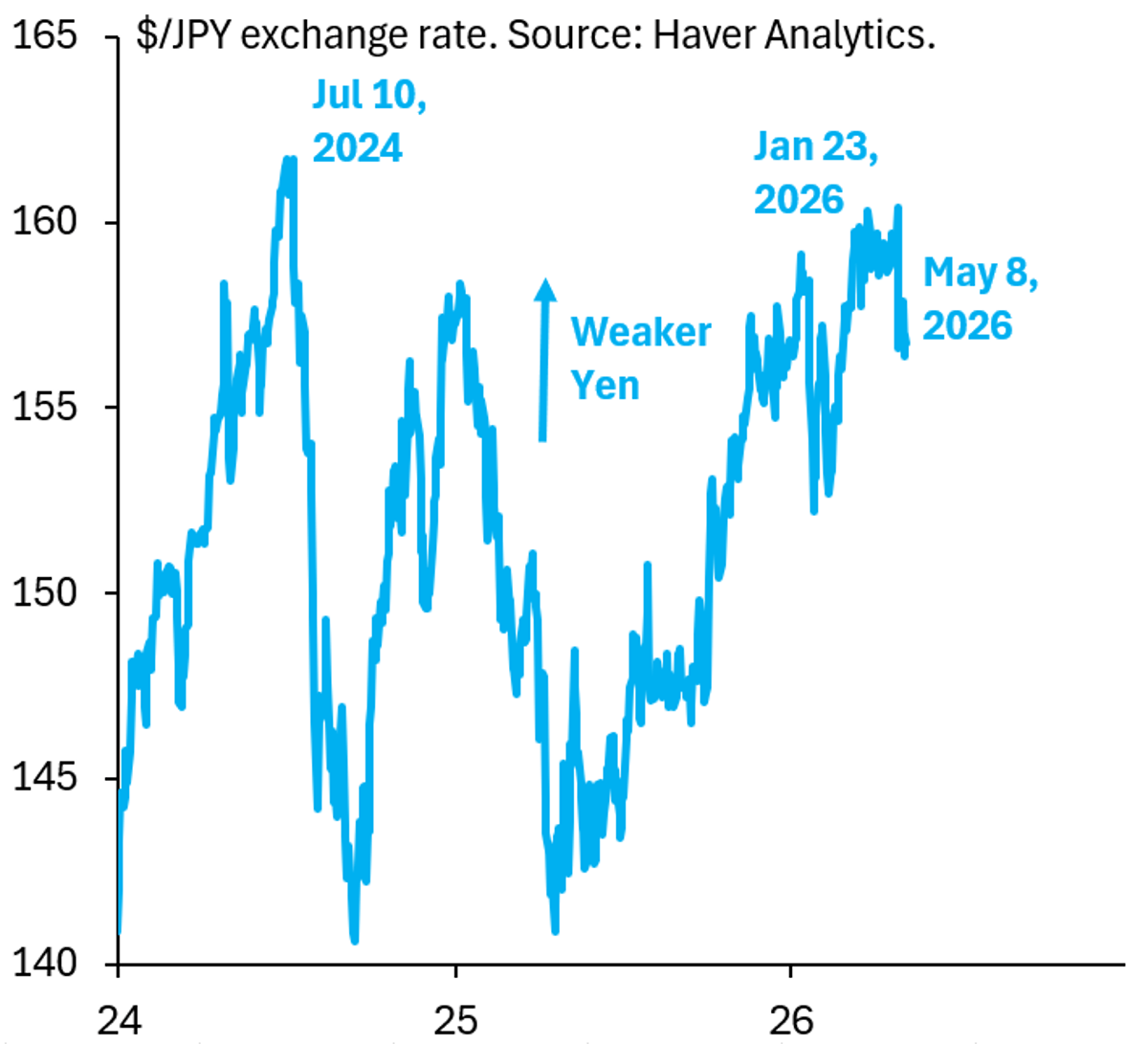

BoJ JGB Purchases Neutralize FX Intervention, Yen Slides

The Yen is already falling again. Markets know Japan's official FX intervention can't work as long as the BoJ is buying JGBs to cap yields. That JGB buying puts depreciation pressure on the Yen, so intervention just gives markets a...

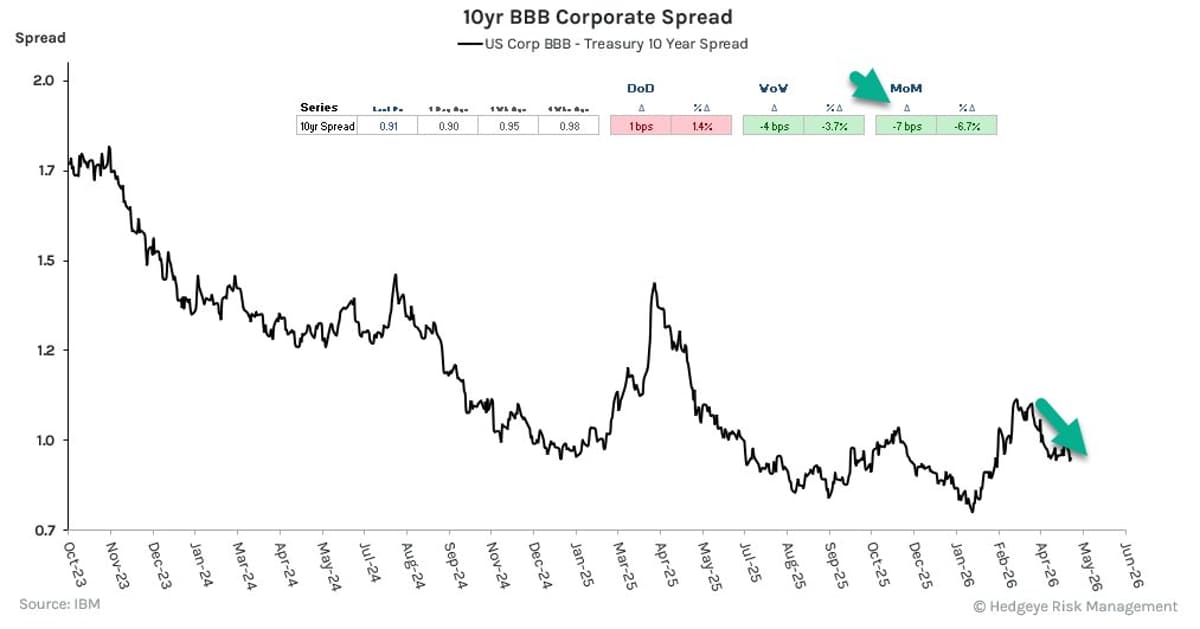

Rising Spreads, Falling

US Corporate Spread "risk" is the inverse of Profit Growth - we remain long High Yield https://t.co/IbOVfjy8fw

No Rate Cuts

Until the conflict ends, no rate cuts. You would need to see a big rise with duration with jobless claims data for the hawks to budge now

BoE Embraces Rising Yields, Forces Tough Fiscal Choices

Rising yields are the only way governments will ever make unpopular decisions to bring fiscal policy under control. The Bank of England is alone among the G10 central banks in letting this play out and deserves kudos. The UK will...

Norway Hikes Rates 25bps; Earnings up, Inflation Risk Flagged

Norway raise their Interest rates by 25bps. Enjoy the earnings but bear in mind flag 2 due to inflation risk. Monitoring closely. Always getting ahead of the curve with data.

JPMorgan and Ripple Execute First Tokenized Treasury Redemption

Ripple and JPMorgan just completed the first cross-border tokenized Treasury redemption on the XRP Ledger. This is a big real-world use case for on-chain Treasuries. Big institutions are now settling real money directly on blockchain. RWA momentum is speeding up. https://t.co/00UFITs8d9

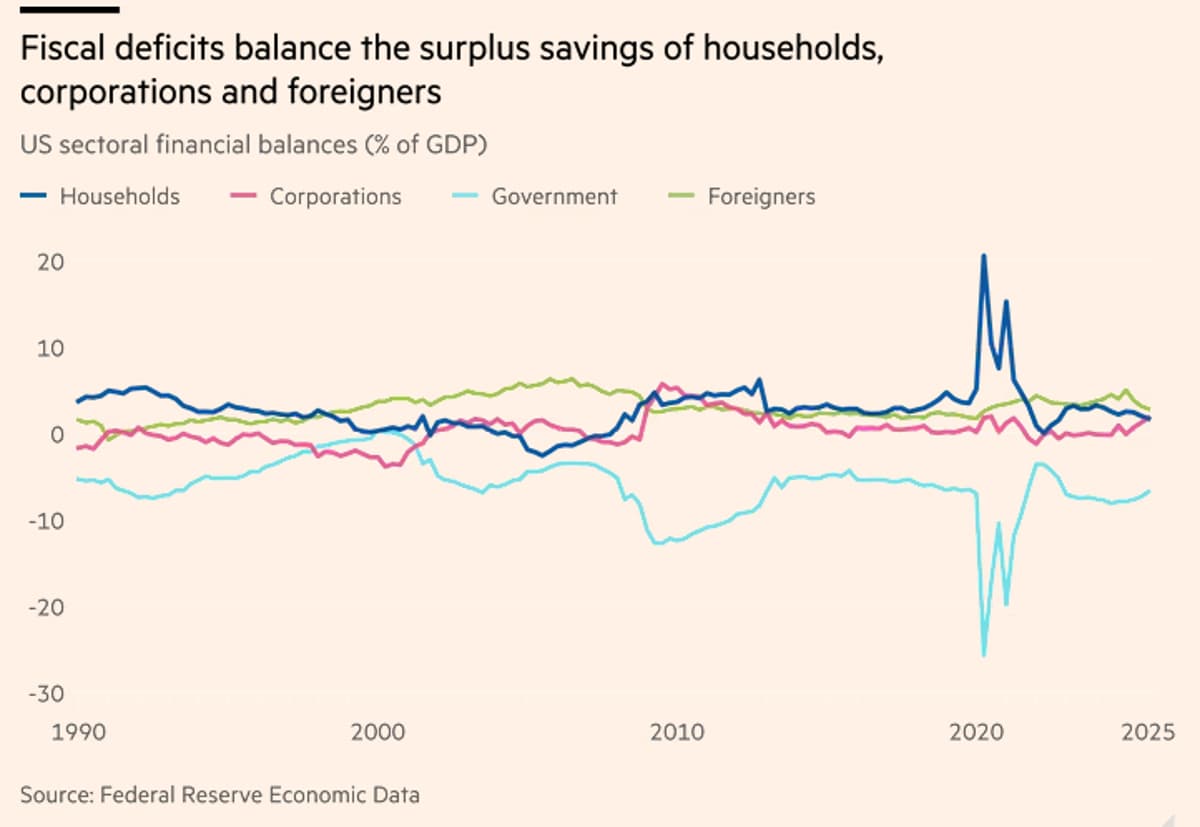

US Government Borrowing Now Mirrors External Deficits

"net US liabilities reached 24 per cent of global output in 2024 against a mere 6 per cent in 2008, and... the US private sector has moved into balance. So, the domestic counterpart of its external deficits today is borrowing...

Skipping Low-Rate Debt Terming Proved Costly

And NO terming out the debt when rates were low was NOT a good idea

Yield Spikes Don’t Predict Iran Peace Deal Leaks

"Professor, don't you find it curious that a new US-Iran peace deal leaks almost every time the 10y UST yield breaks 4.4% on the upside?" "Actually, if I think about it, I don't find it curious at all." https://t.co/aMqLenpJp8

Rate Hike Odds Drop, Swap Spreads Widen, Bonds Rally

Bond trader friendly moves this morning: '27 hike odds lower, swap spreads wider, long-end bid.... Y'all should be happy now.

QRA Unchanged as Treasury Sticks to Yellen‑style Bill Strategy

QRA no change in auction sizes, no change in language, @SecScottBessent continues to follow the Yellen playbook and rely on 20%+ bills outstanding to suppress interest rates. That said this was entirely expected

Policymakers' Stock Market Control Sparks New Inflation Risk

Introducing the Yield Smile. Just like the dollar smile, but for bond yields in a fiscal-dominant world. Move too far down in stocks and deficits blow out, move to strong in the economy and inflation remains persistent. Policymakers are now directly managing...

Sandisk Beats 30‑Year Treasury Over 30% of 2026

Sandisk’s return has exceeded the peak 30Y Treasury yield year-to-date (5.03%) on more than 30% of trading days in 2026! Think that dynamic is one of the reasons why it’s been difficult to see anyone get jazzed up about rotating...

Easing Tensions Historically Trigger Bond Price Declines

i'm old enough to remember the days when headlines suggesting easing tensions and less uncertainty would mean bond prices fell... https://t.co/KaynvMrU0Q

UK Gilts Rise on Oil Dip Amid US‑Iran Deal Hopes

A better morning for UK gilts as oil prices fall sharply after a US media report that America and Iran are “very close” to a deal. While the drop in yields is welcome, expect continued volatility in the days ahead, driven...

US Yield Rise Pressures Indian Stocks, Watch 10‑Year

Rising US bond yields have had a negative effect on Indian stock markets in the recent period since 2024. This pattern may persist till it does not. Right now US yields are nudging higher and that is a pressure point...

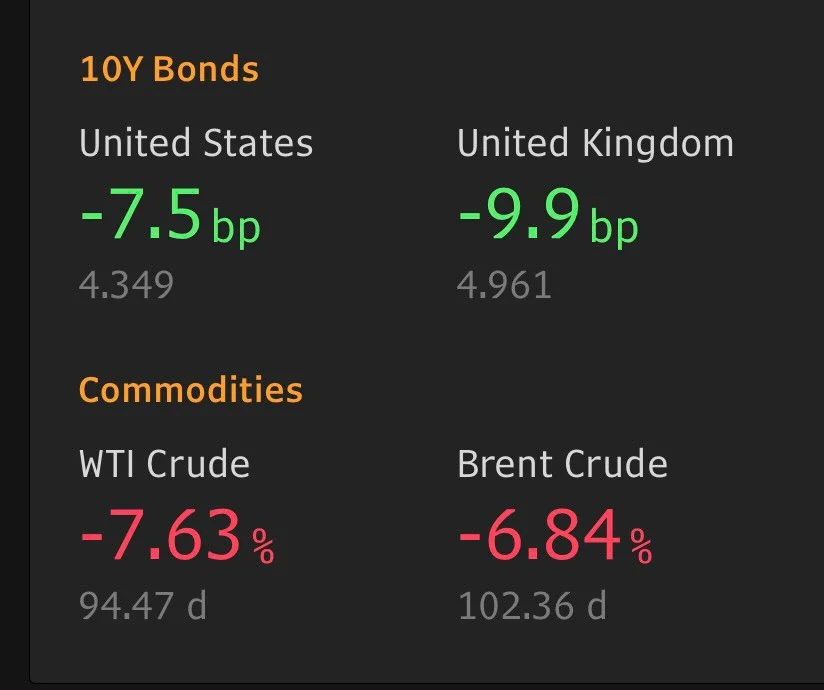

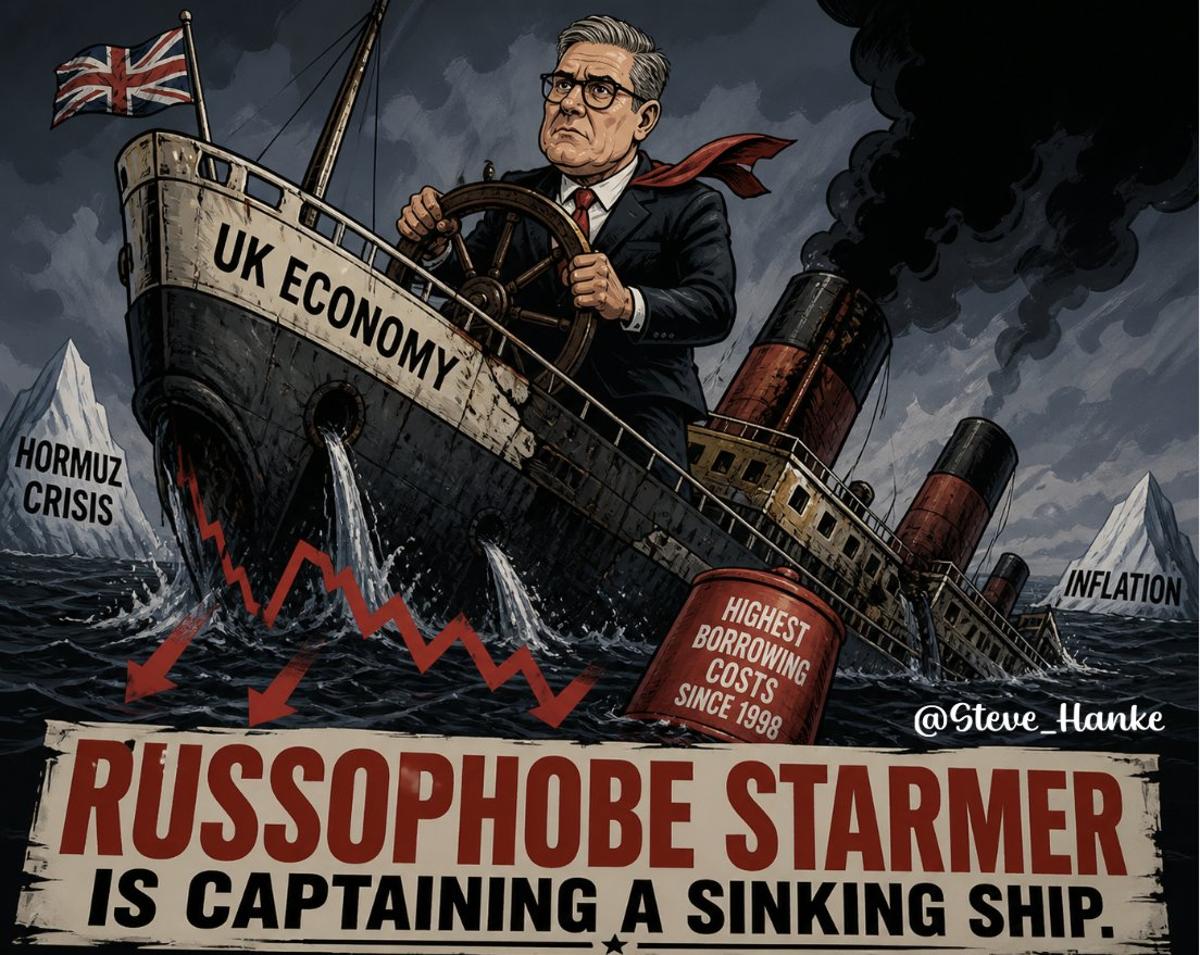

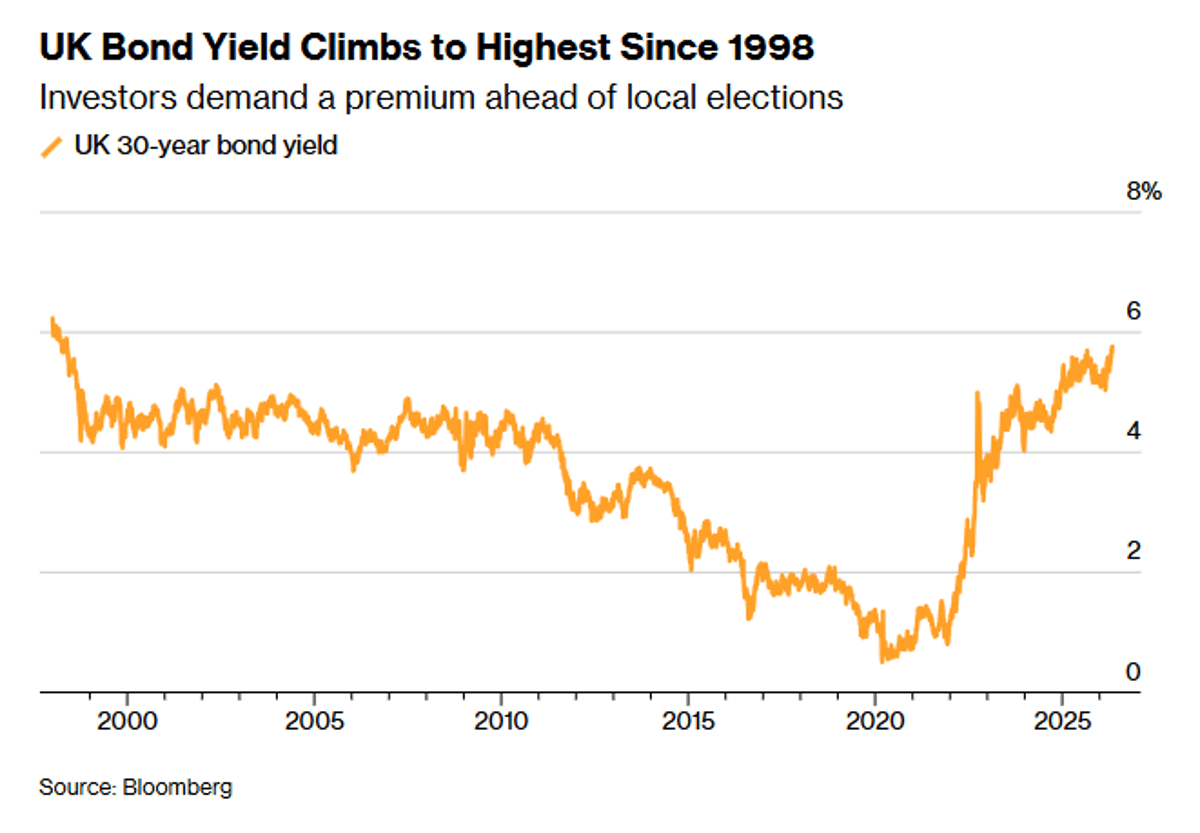

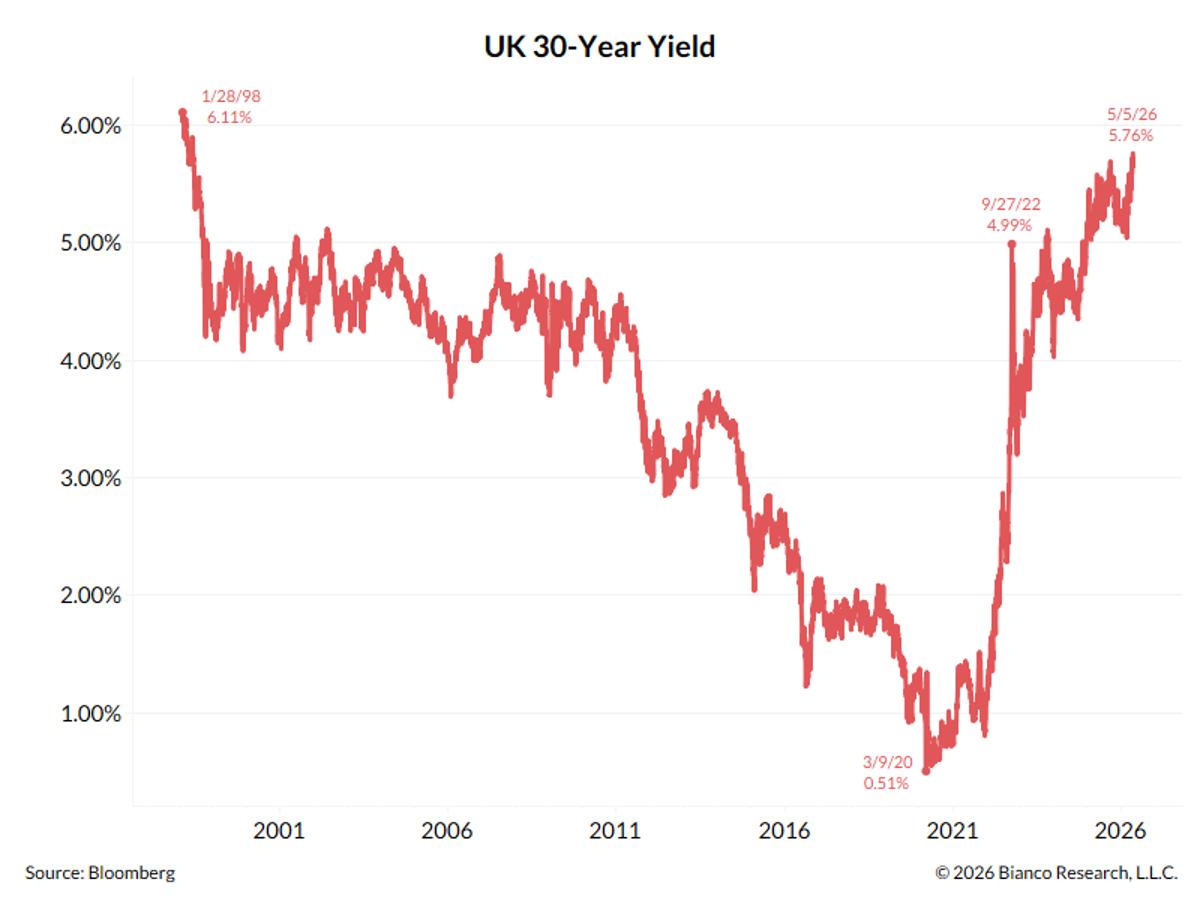

UK Long-Term Borrowing Costs Reach 1998 High

UK long-term borrowing costs hit their HIGHEST LEVELS since 1998. RUSSOPHOBE STARMER IS CAPTAINING A SINKING SHIP. https://t.co/BBGoJG8ZMz

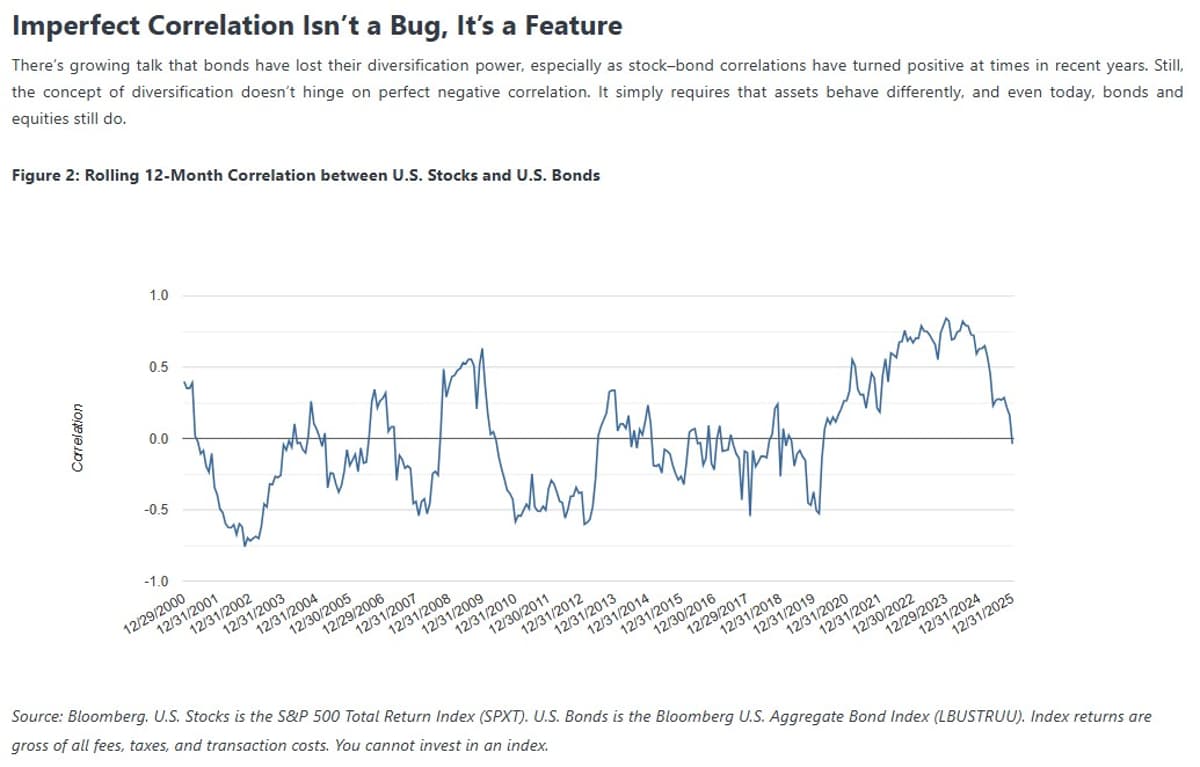

Bonds Still Offer Real Returns and Diversification

Man advisors are so insanely negative on bonds. Bad takes everywhere... Facts: - Yes, stock/bond correlations have become positive at time. Yet the concept of diversification doesn’t hinge on perfect negative correlation. It simply requires that assets behave differently, and even today,...

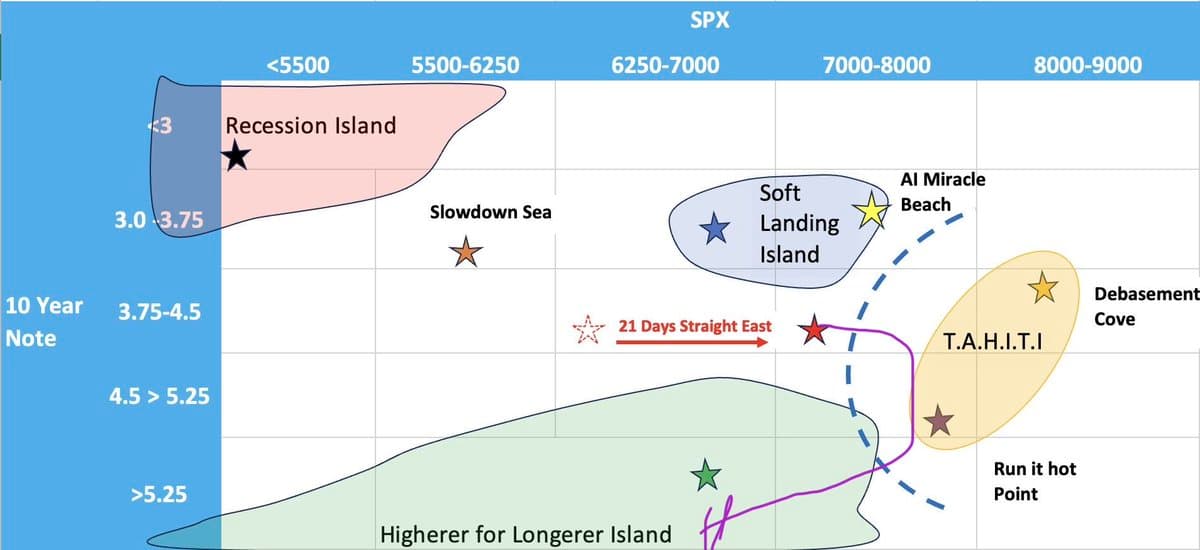

Blue Line Signals Urgent Need for Rate Cuts

Narrative status That blue dotted line needs rate cuts or coupon auction cuts SOON Following that purple line now 28 days. Dipping east south east https://t.co/mcOBDLMz1a

UK Long‑dated Yields Hit 28‑year High on BoE Hike Bets

The yield on long-dated UK debt climbed to a 28-year high as traders bet on more Bank of England interest-rate hikes https://t.co/1j1HJapqBI

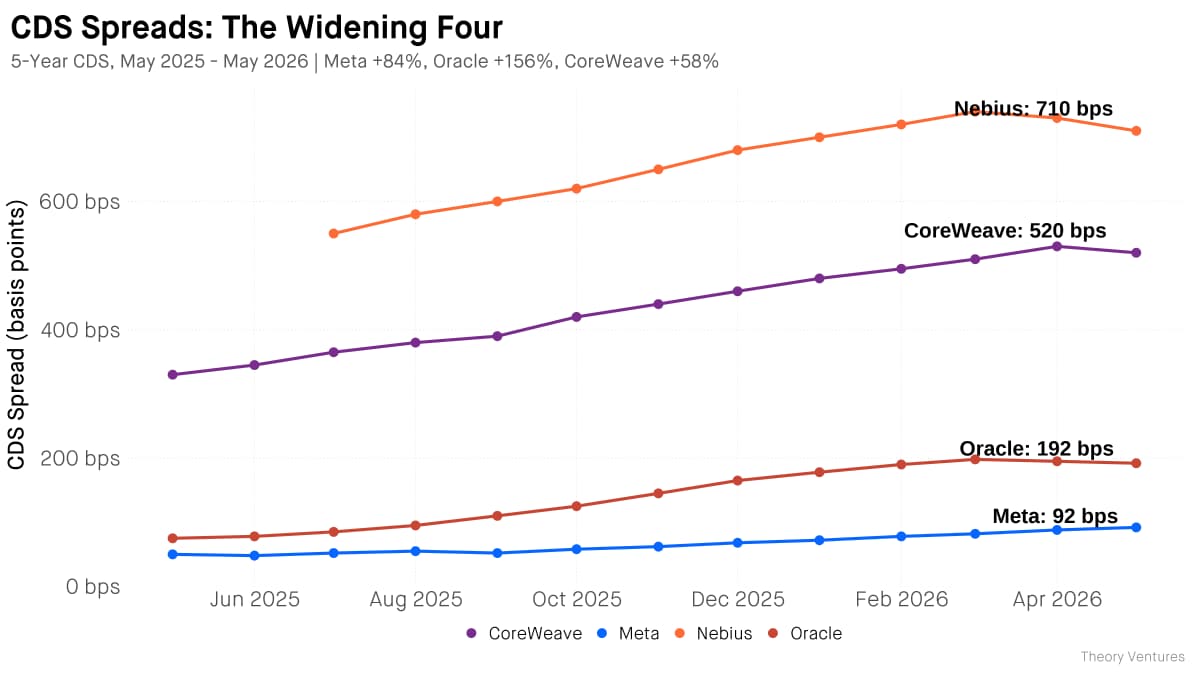

Credit Spreads Vary 42x Across Data Center Firms

The credit market is the harshest judge of risk. Looking at credit default swaps of data center companies, a few things stand out: • The market is starting to believe there is less risk (although still very high) for Nebius and CoreWeave...

QRA's Pause Fuels Asset Rallies, Inflates Debt

The last time the QRA mattered we pivoted from short to long when Janet decided to stop increasing coupon issuance. Every QRA since has left issuance unchanged. Tomorrow will be no different. It's suppressed bond yields from going...

Potential Multi‑Rate Hikes Create UST & SOFR Opportunities

Should the Fed in the next 12 months decide that it needs to hike rates, high odds it will need to hike more than once and more than 25 bps. UST and SOFR curves offering interesting opportunities

UK 30‑Year Yield Hits Highest Level Since 1998

UK bond selloff pushes 30-year yield to the highest since 1998 https://t.co/CNMg8iGy9M via @highisland https://t.co/jvM4S0LRPZ

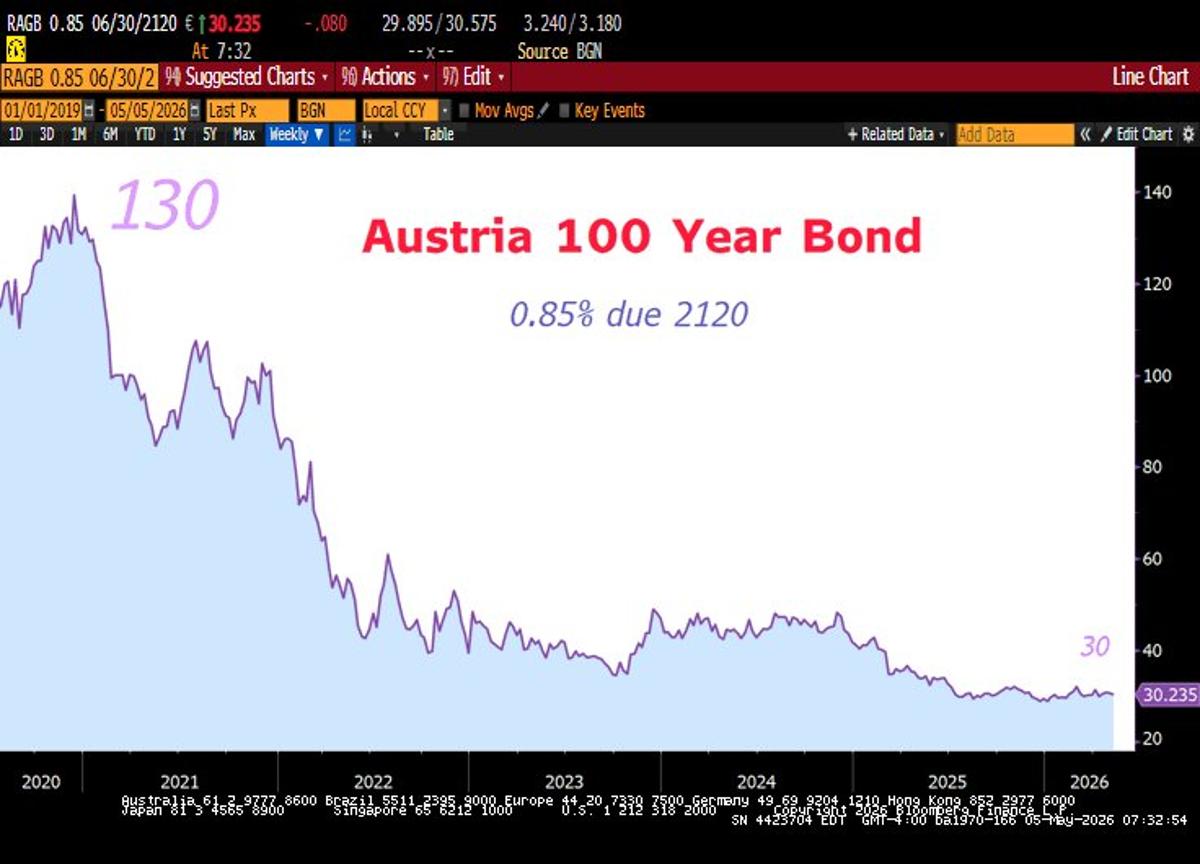

From Near‑Zero to 6%: Bond Yields Surge

In 2020, with global interest rates near 0%, Austria sold this hundred-year bond to investors. Today, the United Kingdom is offering almost 6% (5.77%) for 30 years, think about that. https://t.co/6DDMRv4cEL

UK 30‑Year Yield Peaks at 5.76%, Highest Since 1998

*UK 30-YEAR YIELD CLIMBS TO 5.76%, HIGHEST SINCE 1998 -- On September 27, 2022, the 30-year UK hit 4.99%. This was so intolerable that UK Prime Minister Liz Truss was forced to resign. Today, the UK's 30-year yield is 77 bps higher. https://t.co/NotUU2B1Gv